With rapidly rising interest rates, financial assets around the world have started to reprice.

Singapore is no exception, as SGX Stocks and REITs have started to sell-off.

But with crisis, usually comes opportunity.

If this continues, we could be seeing quite interesting opportunities open up in 2023.

What might be an absolutely terrible macro climate in 2023, could turn out to be a juicy environment for fundamental stock pickers.

So… what are the Top 5 Dividend Stocks or REITs to keep an eye on in 2023?

Note: This post is sponsored by Syfe. All views and opinions in this post are from Financial Horse.

Please note that this is not financial advice. If you are in doubt as to the action you should take, please consult your financial advisor.

Top 5 Dividend Stocks/ REITs to buy in 2023 (as a Singapore Investor)

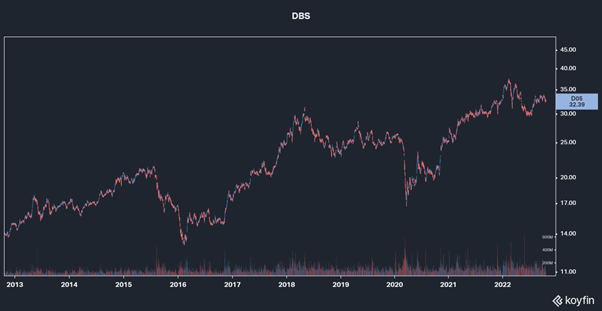

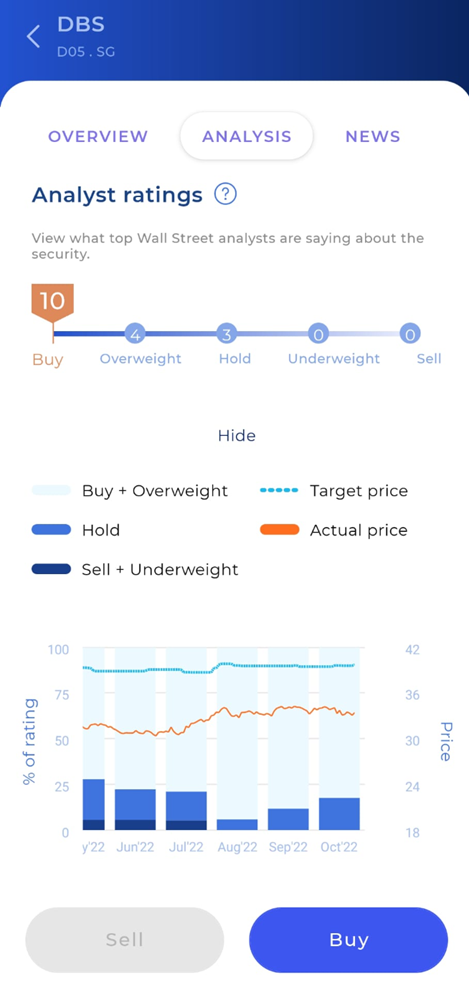

1. DBS Bank (D05)

So many of you have asked me for my views on DBS Bank.

Let’s reason from first principles.

How do banks perform when interest rates go up?

Banks make money from lending money out, so when interest rates go up, their net interest margin goes up due to rising spreads.

This is good.

What worries me about this Singapore dividend stock?

But if interest rates go up too much, then we have a recession.

That means loan defaults, which is bad for banks.

So… rising interest rates are good for banks, up to a certain point.

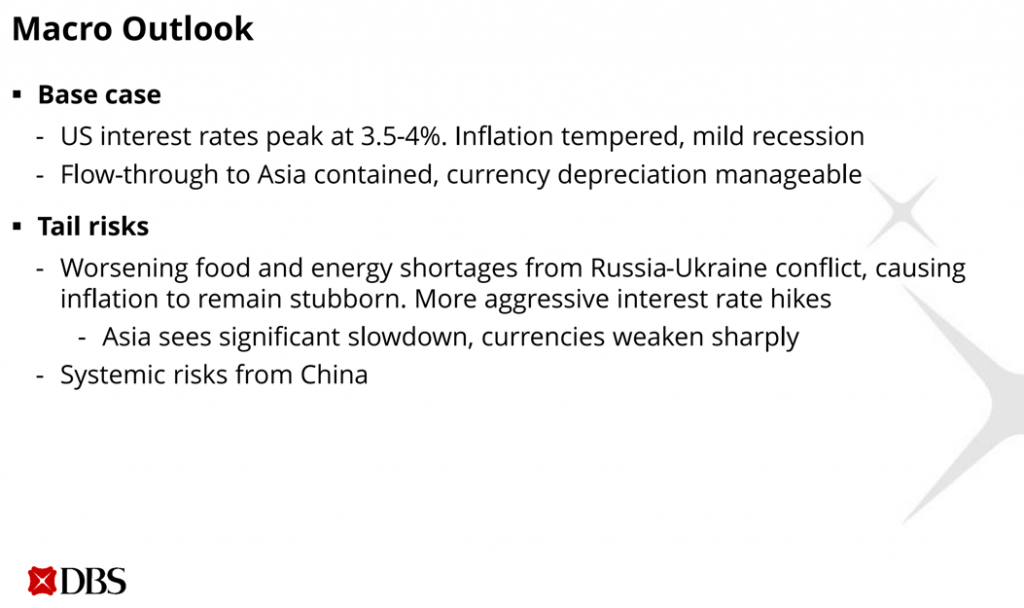

You can look at the assumptions that DBS uses below.

3.5 – 4.0% peak US interest rates, inflation tempered, mild recession.

Flow through to Asia contained, currency depreciation manageable.

I don’t know about you, but that sounds a lot like a “soft landing” to me.

With US labour still strong, and Futures markets pricing in a peak of 4.75% – 5.0% US interest rates, I’m not sure how realistic DBS’s base case is.

That said, if we do get a recession, the million dollar question is how bad will the recession be.

In 2020 governments stepped in with huge fiscal support and things like loan payment moratoriums. This was unprecedented and kept loan defaults low.

If we get a big recession in 2023, will we see the same?

What price is worth watching for this Singapore dividend stock?

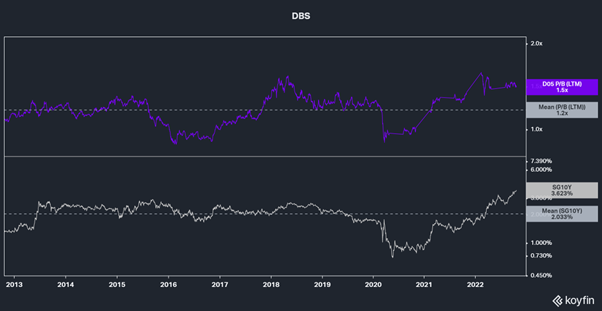

Book value for DBS is about $22 which would be interesting if we get there.

In any case, just look at DBS’s 10 year Price/Book chart, plotted against the 10 year SGS yield.

Banks are about as cyclical as it gets.

Buy when they fall below average book values, sell when they go above.

Some of you may argue this time is different because higher interest rates are good for banks. And you may point out that bank capital ratios are very strong this time around because of the post-2008 regulations.

That’s possible, although I vaguely recall investors saying that before every bank crash the past 20 years.

Time will tell.

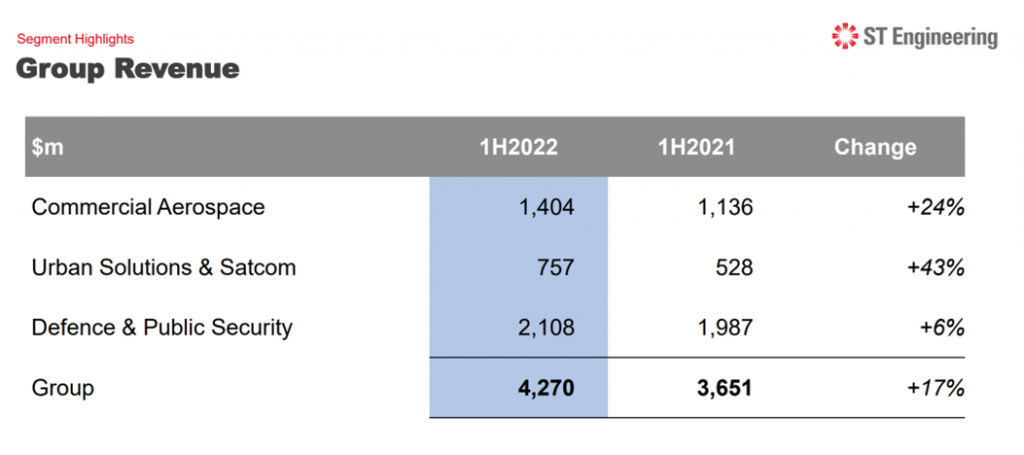

2. Singapore Technologies Engineering (S63)

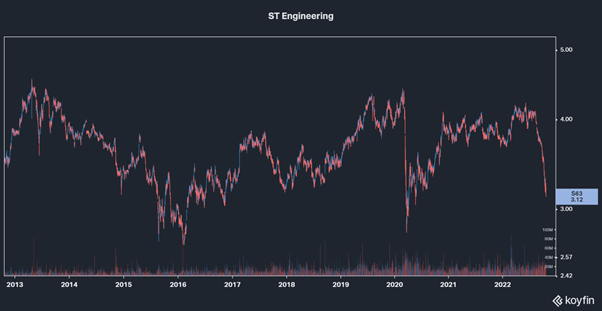

From it’s high of $4.1, ST Engineering has dropped 24% to $3.12

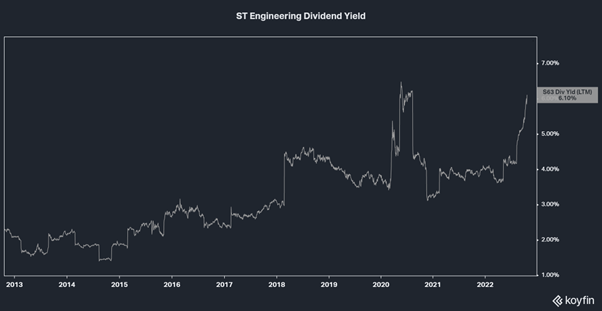

At this price, it trades at a whopping 6.1% trailing 12-month dividend yield, which is close to the COVID levels:

For a company that is heavily exposed to the more recession proof defence business, this is interesting.

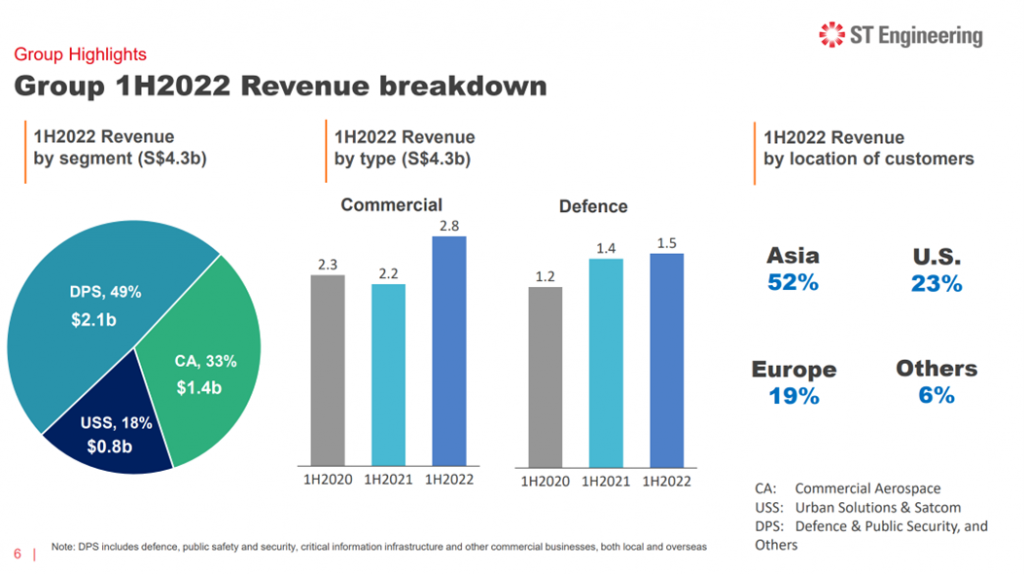

Revenue growth is pretty solid as well, looking at these numbers you wouldn’t be able to tell that this stock just sold off 24% and trades at a 6.1% dividend yield.

What worries me about this Singapore dividend stock?

That said, nobody buys a stock for the past 12 months.

It’s the next 12 months that you look at.

ST Engineering just spent $3.6 billion to buy Transcore in late 2021 (a US mobility company).

So they took on a lot of debt to buy a US mobility company, right before what might be a big US recession.

The market is not a fan of big transactions these days especially with the rising cost of financing (see SATS).

How ST Engineering integrates Transcore, whether they can reap any “synergies” moving forward – that will be key.

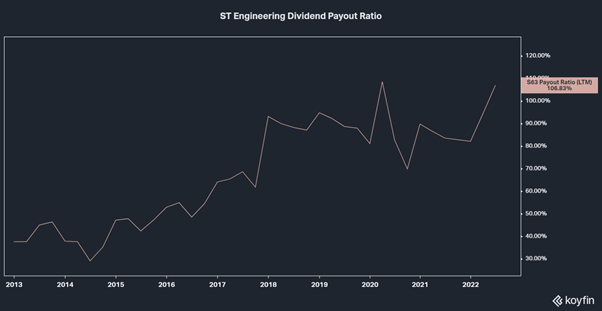

And look at ST Engineering’s dividend payout ratio.

With a 106% dividend payout ratio, will ST Engineering be able to sustain their dividend going forward?

Especially if we head into a 2023 recession?

Big question mark.

What price is worth watching for this Singapore dividend stock?

That said, at the right price, every stock is worth looking at.

ST Engineering has very long term support at the $2.6 – $2.7 range, could be worth watching if we get there.

Looking for an easy, low-cost way to buy US and Singapore stocks?

Syfe Trade can now be used for SGX Trading!

Get free cash credits with Syfe Trade.

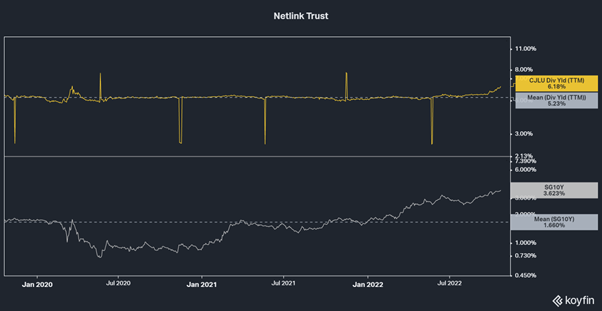

3. Netlink NBN Trust (CJLU)

Netlink Trust is as boring as it gets.

This is a $3 billion market cap business trust, that owns the fibre connections in Singapore.

Each time you use the fibre connections, Netlink gets a small fee.

It’s a stable monopoly business, but on the flipside, prices are highly regulated so don’t expect much growth.

What worries me about this Singapore dividend stock (business trust)?

Like I said, it’s probably best to think of Netlink Trust as a bond, because growth potential is very weak (prices are regulated by IMDA).

So you are buying a bond style product, in the fastest rate hiking cycle in 20 years.

Don’t forget that for bond yields to go up, the price needs to drop.

So yeah… I would watch the interest rates closely.

What price is worth watching for this Singapore dividend stock (business trust)?

That said, it all comes down to the price.

Long term yield spread is about 3%.

Assuming a peak 10 year SGS of 4.0% – 4.5%, you’re looking at about 7.0% – 7.5% yield on Netlink Trust.

Works out to high 60s, low 70s.

Long term support is in the 70s too.

That could be interesting.

Valuations are NOT a timing tool

That said, I do want to caveat that valuations are NOT a timing tool.

All valuations do is to tell you whether a stock / REIT is cheap or expensive, relative to historical prices.

A cheap stock can get cheaper, an expensive stock can get more expensive.

So whether the price levels set out in this article are hit in 2023, I frankly don’t know.

Much will depend on the macro conditions the next 12 – 18 months.

So be flexible, and don’t be dogmatic.

If the macro conditions change, don’t be afraid to change your mind.

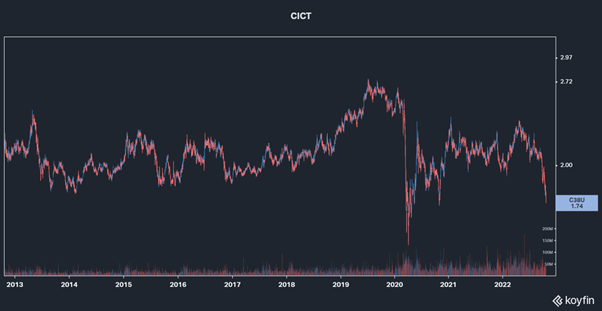

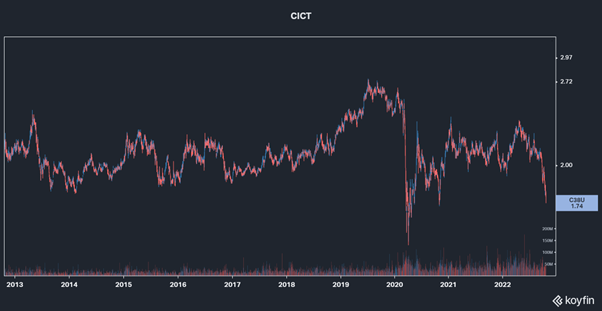

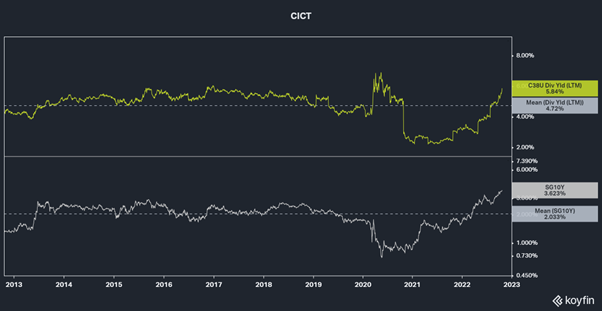

4. CapitaLand Integrated Commercial Trust (C38U)

I’ve been talking about the risk of an Asian Financial Crisis 2.0 (in terms of currency devaluation) for a while now.

For savvy investors, that could open up opportunities to buy Asian REITs (Daiwa House Logistics Trust anyone?).

For investors who want to play it safe, sticking with Singapore real estate might be a safer play.

After Mapletree Commercial Trust’s merger with Mapletree North Asia Commercial Trust – Capitaland Integrated Commercial Trust (CICT) is probably the biggest (and purest) Singapore retail/office REIT.

What worries me about this Singapore REIT?

The concerns with REITs are not new, and you can check out my fuller views here.

Real estate is very sensitive to interest rates (not in a good way).

And with REITs, you’re throwing on leverage to buy real estate.

Rising interest rates are as deadly as it gets for REITs.

Until the Feds pivot meaningfully, the pain may not go away.

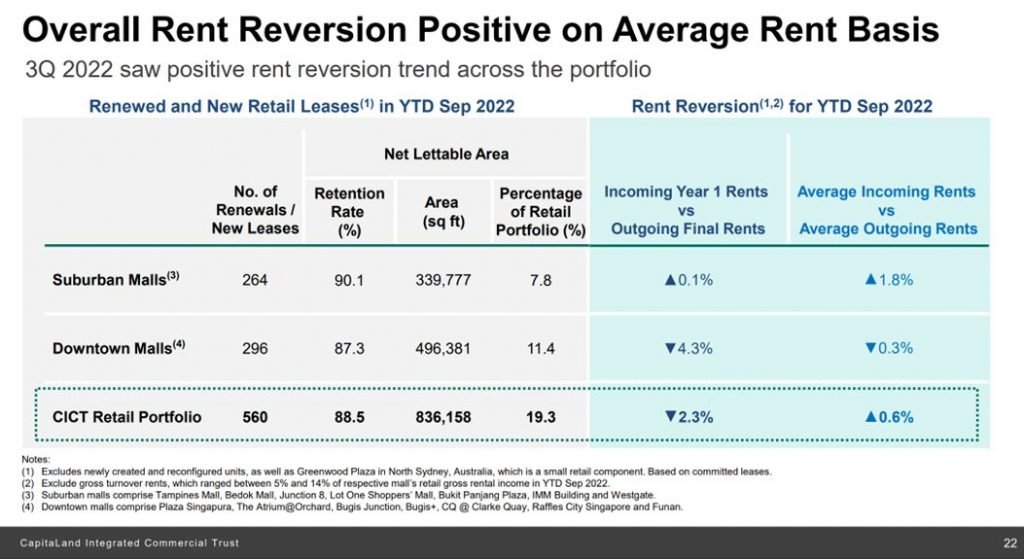

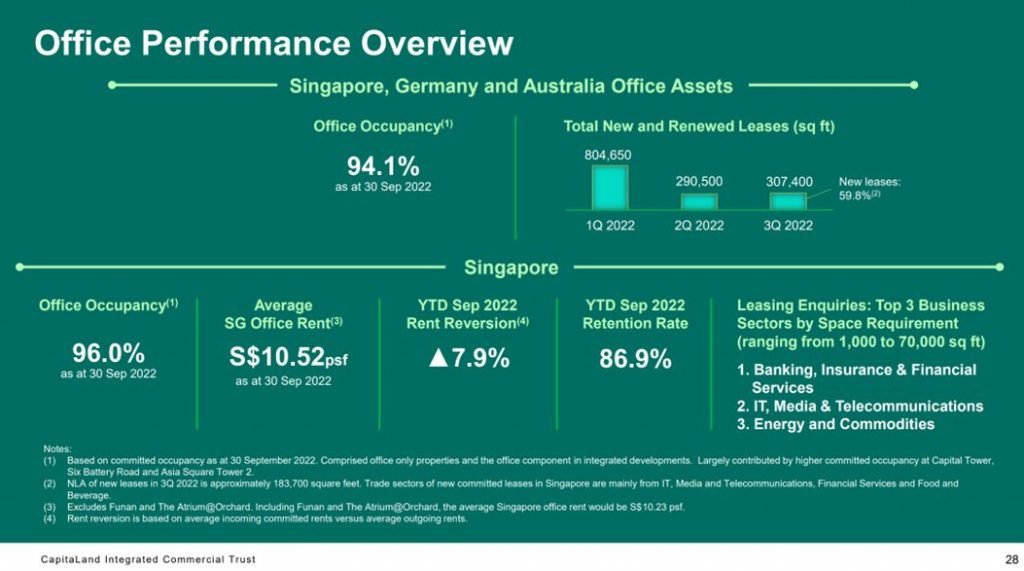

Rental Growth?

Some of you have asked me whether the rental growth can offset the impact of rising interest rates.

My simple answer is that rental growth will matter in the mid term, but in the short term, with this pace of interest rate hikes – interest rates are the dominant factor to watch for now.

If you dive into the rental reversion numbers, you’ll find that the incoming year 1 rents are actually down slightly for the retail portfolio.

With office rents, yes there is positive rental reversion, but don’t forget that these leases tend to be signed long term, so it takes years before you can “refresh” your entire lease portfolio at higher rates.

So yes, rental growth will matter mid term, and you need to watch out for it as a long term investor.

But short term, watch interest rates.

What price is worth watching for this Singapore REIT?

The COVID lows was $1.5s, which is worth watching if we ever get there.

That works out to a 7% yield, which is about a 3.0% yield spread (assuming peak 10 year SGS of 4.0% – 4.5%).

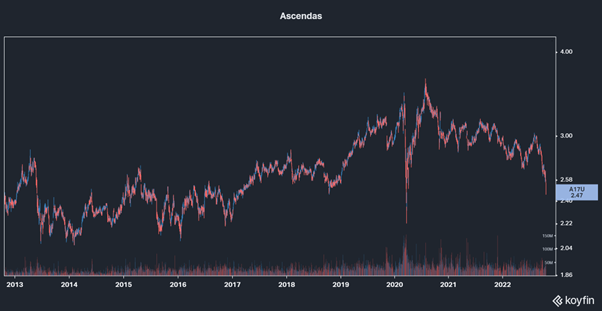

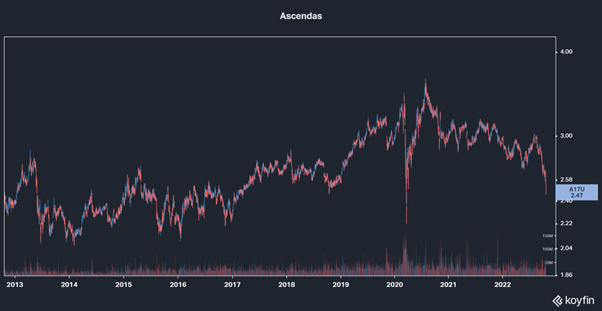

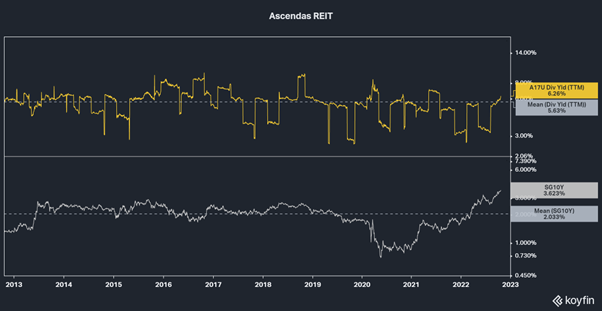

5. Ascendas REIT

And if I had to pick one REIT to get exposure to Singapore industrial property, Ascendas REIT is probably my choice.

The CICT equivalent, for industrial properties.

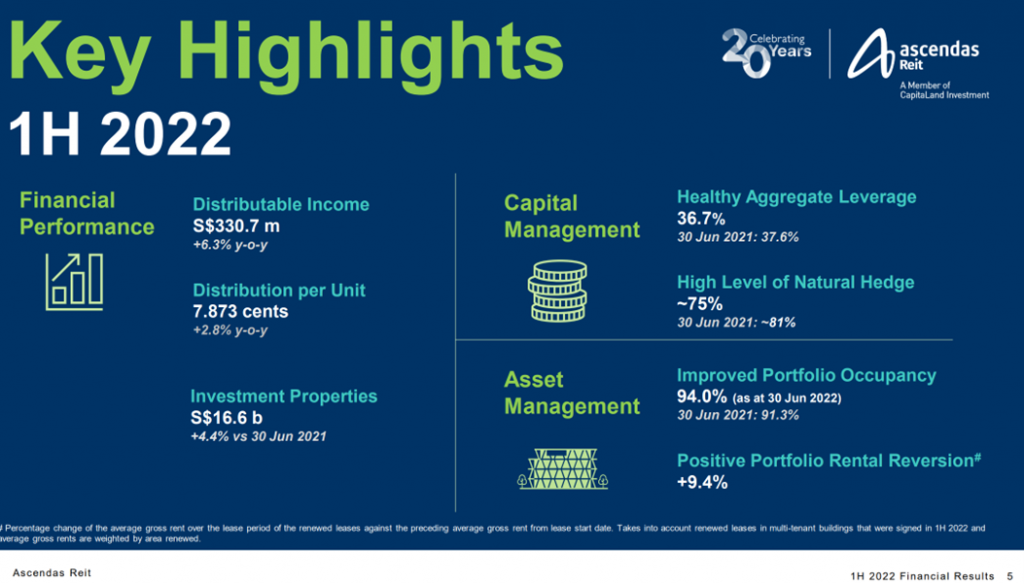

Rental reversions are pretty strong too, up 9.4%.

What worries me about this Singapore REIT?

Rising interest rates of course.

But I already discussed this above, so I won’t belabour the point.

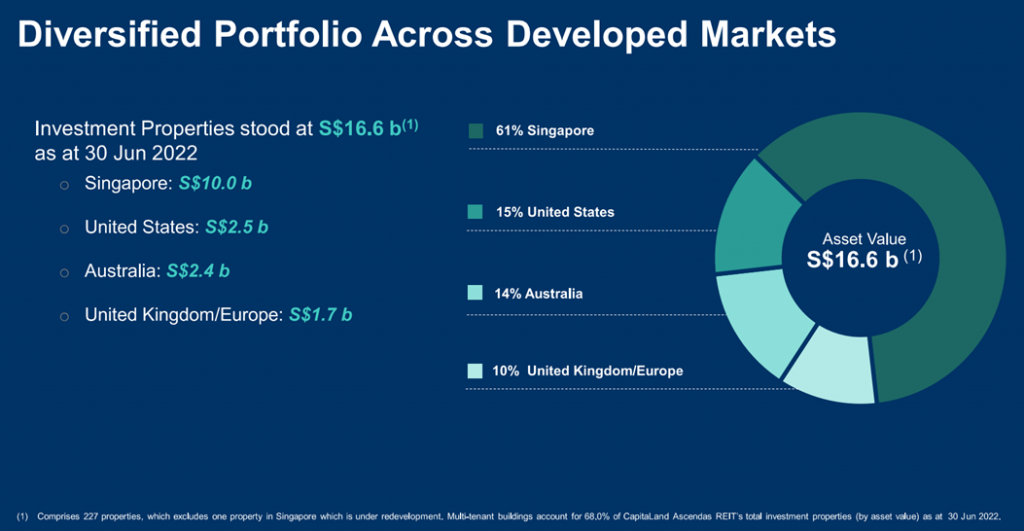

And after a decade of M&A, only 61% of Ascendas REIT is Singapore properties these days.

The rest is US, Australia, and UK/Europe.

This means you’re looking at almost 40% non-Singapore real estate exposure.

Exposure that might suffer quite a bit in the next 12 – 18 months.

So you want to be careful with your valuations here.

Yes, Ascendas REIT is a much bigger REIT than it was 5 years ago. But a lot of that exposure is overseas exposure, which is much more volatile than Singapore real estate.

What price is worth watching for this Singapore REIT?

Ascendas REIT has very long-term support at the $2 – $2.2 range.

At that price, it would be about a 7% yield, which is a 3% yield spread (assuming peak 10 year of 4.0%).

Could be interesting.

How to buy SGX Dividend Stocks/ REITs

Did you know? Syfe Trade can now be used for SGX Trading!

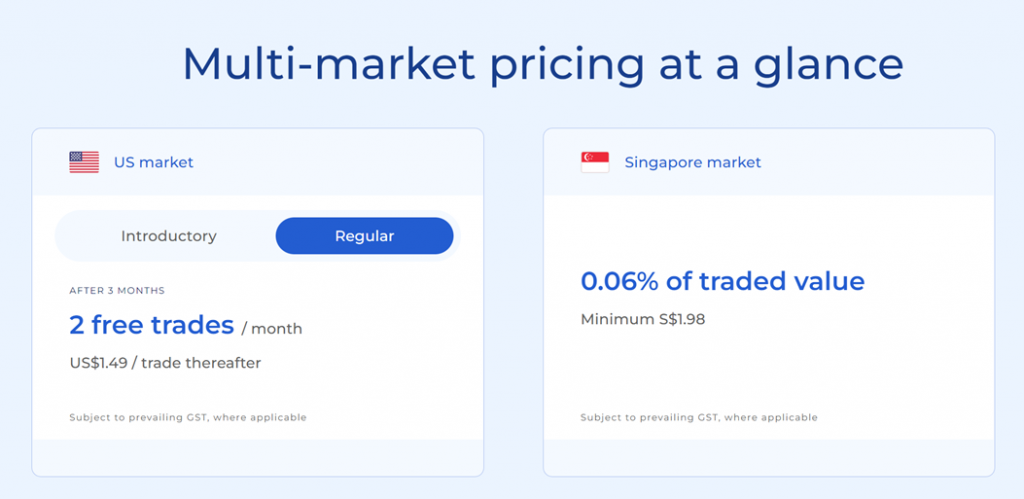

Syfe Trade is a homegrown, MAS-regulated broker that offers easy and affordable access to the US and Singapore markets.

Key highlights are:

- Easy to use: Even for first-time investors

- Affordable: No more paying up to S$25 per trade. Syfe charges 0.06% of trade value with transparent pricing and no hidden or platform fees. (This is on par with other digital brokers)

- MAS Regulated: Syfe is MAS-regulated and based in Singapore

- Attractive sign-up offer: New Syfe Trade users will receive S$50 cash credits within a limited offer period to buy any SGX stock / ETF they want (min funding of S$1,000)

- 24/7 live customer support whenever you need it

Pricing is competitive, at 0.06% of traded value (minimum S$1.98).

There are no platform fees and no withdrawal fees so your dividends can be withdrawn anytime if you wish.

Syfe Trade also offers market news and analyst ratings to help you make informed decisions.

If you’re looking for an easy and fuss-free trading experience, Syfe Trade checks all the boxes.

Sign Up Offer

From now to 30 October 2022, get a S$50 welcome gift to buy any stock / REIT of your choice.

Simply download the Syfe app and sign up using the code “TRADESG“. This is open to all new to Syfe investors who deposit a minimum of S$1,000 in their Syfe Trade account.

Download Syfe app here!

Note: This post is sponsored by Syfe. All views and opinions in this post are from Financial Horse.

The content here is for informational purposes only and should NOT be taken as legal, business, tax, or investment advice. It does NOT constitute an offer or solicitation to purchase any investment or a recommendation to buy or sell a security. In fact, the content is not directed to any investor or potential investor and may not be used to evaluate or make any investment.

Do note that this is not financial advice. If you are in doubt as to the action you should take, please consult your stock broker or financial advisor.

This advertisement has not been reviewed by the Monetary Authority of Singapore.

Dear FH

Thanks for your views. I differ and strongly so for perhaps the first time with you!

In fact, except for DBS which is rising and might even go higher imminently if next week results excel, I have started adding to my positions in ALL the stocks that you discussed! In fact, I will add more of each of them if there is a dip even if mild, slowly and steadily

The rate cycle is almost on the verge of peaking and an US recession will be milder than anticipated. The fed might raise only 75 and then 50/25 in December

This will be construed as a fed pivot. Earnings are excelling in the US. Even if you argue that the recent rate rises will hit them early next year only, by that time the SPY will be at around 4200 if not more. The rest of the markets including SG will go higher with our three banks gaining more than lose out. At that stage, say Q2 2023, the earnings take a hit- the market will fall from a higher level of 4200 plus and by that time the rate cycle will go lower facilitating fast recovery!

Only a major macro event like a war in the Taiwan strait or resurgence of the pandemic , will upset things

I will steadily buy and lock into yields at this level with each draw down day and harvest the yield plus potential capital appreciation

Although I know that capital erosion is a distinct possibility, in the longer term, the benefits far outweighs the risks

In fact, I added STE at 3.12, added Wilmar, UOB OCBC as well as AsReit, CICT, KREIT, FLCT, FCT, MPACT, MIT, KIT, Sabana , CLCT Suntec and will keep doing so

The rates are about to peak and plated before they come down in mid 2023

If the rates go lower, there is a soft landing, all will go up including the banks

I am optimistic and cautiously bullish

Best wishes

Garudadri

Hi Garudadri,

Great comment as always. I have been pondering the same myself.

I think the main concern I have with this view, is that:

1. Assuming we get a Fed “Pivot” in Nov/Dec. What happens next to inflation? If inflation stays at the 3-5% range next year, are the Feds still going to cut rates? If so what will happen to the long end, once bond investors realise inflation this decade is going to stay high.

2. While I agree that the rates bear market is over (or at least the bulk of it is over), the end of the rates bear does not necessarily equate to the start of the bull market. Without QE or rates back to zero, where is the tailwind for equities going to come from? Economic growth wise we are quite likely to be headed into a 2023 recession, so earnings growth might be muted too.

Meanwhile, you’re getting 4%+ risk free from T-Bills or 2Y Treasuries. The longer this goes on, the more we may see institutionals reallocate money into Fixed Income.

Just to add, in the Scenario 1 I described above, I agree that buying stocks is the right move.

REIT/Bond Proxies will become a lot more tricky, if the long end is going to go unhinged.

Even if so, I prefer to wait for the signal from the Feds before buying.

Who knows, we might get that signal this week!

What do you think about SATS? Is it a buy after the fall?

SATS has many of the same problems as ST Eng, in having paid up a lot for a western company, right before a recession.

Whether they can reap synergies or how successful the integration will be is key, but the track record for TLCs in doing so is spotty.

SATS has the additional problem of having to do a big dilutive fundraise to pay for the acquisition.

It might be a good play for certain investors, but I’ll probably pass for now.

Hi

Not sure if this was for FH

I have never held SATS and have no intentions of buying it as there are much better opportunities available! FH might have a different view?

Garudadri

Just shared views above!

I think this is one of the target richest environment for stock pickers in a long time. So investors can afford to be stingy with capital.

Be patient, and only swing if the risk-reward looks great.

When I can get 4%+ risk free on T-Bills, I am a lot less desperate to deploy capital.

Have you considered Vicom as an alternative to netlink?

The dividend is quite a bit lower though. Never looked closely at this stock in the past, might have a closer look.

There was mention on the payout ratio of STE in the article. Netlink has an even higher ratio than STE. There will be you similar concern on Netlink dividend sustainability?

Well between the two I would probably be more worried about STE. But that doesn’t mean Netlink’s dividend is risk free.

So to answer simply – yes, you do need to look into Netlink’s dividend sustainability as well.