The September FH Stock Watch went out over the weekend.

As promised – I wanted to use this article to share latest macro views, and on where value lies in this market.

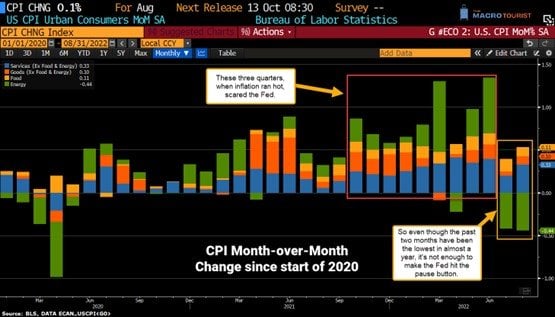

Latest CPI Print was a big deal

Let’s talk about the elephant in the room.

The latest US CPI print that came out last week, was a pretty big deal.

Now to understand this CPI report, we need to understand the difference between headline inflation, and core inflation.

Very simply:

Core inflation is the change in the costs of goods and services but does not include those from the food and energy sectors. Food and energy prices are exempt from this calculation because their prices can be too volatile or fluctuate wildly.

So the difference is that headline inflation includes food and energy costs, which core inflation does not.

The latest CPI report showed:

- Headline inflation up 0.1% month on month, up 8.3% from last year

- More importantly – Core inflation up 0.6% month on month, up 6.3% from last year

This means that headline inflation is starting to slow down because oil prices are coming down.

But the bigger problem – is that core inflation is still going very strong, driven primarily by a tight labour market.

A tight labour market is driving strong wage growth, which drives strong services inflation – which drives core inflation.

And really, that’s the key problem for the Feds now.

They need to break the labour market, so that services inflation can start to come down.

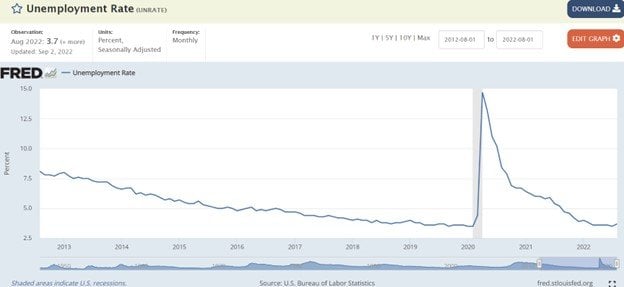

The problem though, is that the labour market for now is still very strong.

Month on month wage growth is very strong, and unemployment at 3.7% has barely even ticked up.

Job openings still vastly outnumber the unemployed.

Just look at the recent rail-union deal, where they agreed to a 24% wage hike over 5 years, and a while bunch of benefits for medical leave etc.

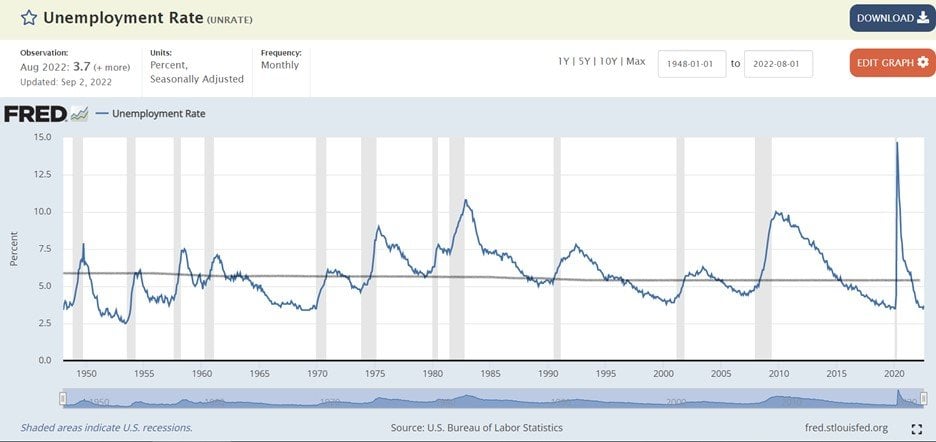

To meaningfully break the current wage growth inflation, the Feds probably need to bring unemployment above 4%, and likely above 5% (current rate is 3.7%).

We may even see peak employment at 6% (marked by the line below) which gives you an idea of where things may need to go.

What does this mean for markets?

TLDR – US inflation is proving more sticky than expected.

Like we’ve been saying on FH for a while now, the Feds need to hike interest rates higher, and for longer than expected.

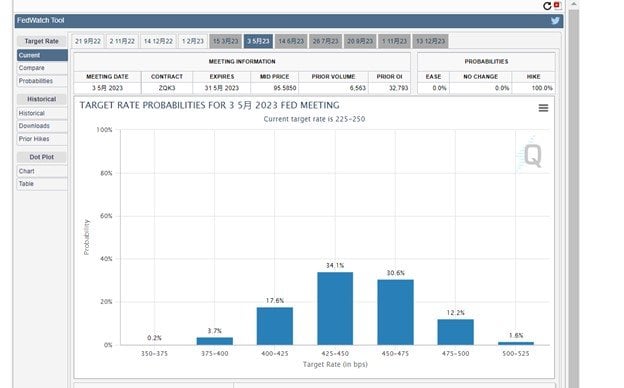

And finally, after the past week, the market is starting to wake up to this reality.

As things stand, the market is pricing in a peak Fed Funds rate of 4.5% this cycle.

And that to me, brings us much closer to the end game here.

Personally I think the Feds may even need to go to a 5% peak Fed Funds Rate this cycle.

But whatever the case, the markets are finally starting to price in the final path the Feds are likely to take.

Which of course, is an absolute disaster for risk assets.

What happens next?

The Feds hiking this much this fast has the potential to break many things in the market.

So far we’ve only seen valuations for financial assets start to come down.

As this plays out, expect:

- Corporate earnings to get impacted (as consumers cut back on spending due to inflation and higher interest expense)

- Refinancing risk and higher borrowing costs (companies borrow at risk free + a spread, both of which will increase dramatically)

- Potential currency crisis (with the Fed Funds Rate at close to 5%, there are few economies in the world that can keep up – which means currency depreciation for those countries relative to the USD)

And as all of the above plays out, the risk of a liquidity crisis will continue to build.

I’ve been quite bearish since Jan 2022, and it still looks like things need to get worse before they get better.

Sidenote: Ray Dalio had a good article last week on inflation. It’s a good read and worth your time, but the gist is that he thinks that interest will need to go to the higher end of the 4.5% – 6% range this cycle.

And he thinks that interest rates at 4.5% will trigger a 20% drop for stock prices on average.

His numbers differ slightly from mine on the terminal rate, but the broad direction is the same.

Where does value lie in this market?

A few months back (around June-July) I said there was a tradeable bounce in commodities and cyclicals (eg. banks).

Back then, the market was pricing in a 2022 recession, which in my view was too early.

The economy is more resilient than people are expecting, as seen in the strong labour market.

This means that while a recession will come, a recession is more of a 2023 story, and less of a 2022 story.

Which opened up an opportunity to trade commodities and cyclicals back then.

However, this trade has now played itself out.

With the massive August rally in commodities and cyclicals, that tradeable opportunity has played out.

Where we are now, I think it may be best to just stay out of the way until the rate hikes and QT play itself out.

I see broadly the 2 options as:

1) Stay in cash

Latest 6 month SGD T-Bills yield 3.32%, and they may get close to 4% by year end.

If you can get 4% risk-free just by staying in T-Bills, frankly that’s not too bad an option.

Just wait out the volatility, wait for the Feds to flip dovish, then start buying.

2) Short the market

Because this is an inflationary bear market, you can’t trade it like 2008 (or any other recession the past 40 years).

In 2008 Treasuries were a good hedge against the declining stock market.

But this time around Treasuries won’t work because inflation means interest rates will go up despite the declining stock market.

So traditional hedges like Treasuries won’t work so well this time around. Treasuries can go down together with stocks.

Which means that if you truly wanted to hedge positions, you need to go short.

But shorting in a bear market is a dangerous proposition as the bear market rallies are very real, so you want to be very careful with risk management.

Opportunities for a long only investor?

If you wanted to go long, I would generally be quite cautious here, at least until the macro plays itself out.

That said, there are 3 asset classes I wanted to discuss in greater detail:

1) Commodities Supercycle?

I’ve been saying for a while that with commodities I am mid term bullish, short term uncertain.

The problem with commodities in the short term, is that there is a very real possibility of a global recession in 2023.

Can commodities go up in a recession?

Yes it can, and it has in the past.

Do I necessarily want to bet heavily on commodities going up in a recession?

Maybe not.

And therein lies the problem.

I think this decade will be inflationary.

I think the only sustainable solution in the mid term, is for global governments to print a lot of money to get themselves out of the debt problem. At the same time, the decoupling between the west and the east is going to require brand new supply chains, and massive investment into infrastructure. The shift to renewables too will require massive investment – all of which require commodities.

Coupled with a decade of underinvestment in commodities capex, I think commodities have the potential to go up a lot more in this decade.

Alternatively, you can also see it as the value of paper money that needs to drop, relative to commodities.

So while I like commodities with a mid term perspective, short term I really am a bit cautious.

2) REITs – Rising Interest Rates spell doom for REITs?

I’ve been thinking and thinking about how REITs will do in an inflationary decade.

So I took a closer look at the performance of REITs in the US in 1970s, the last time inflation was actually a problem.

And the lesson there, is this:

- Rising interest rates can really crush REITs – refinancing risk and increased borrowing costs are very real

- But – good quality real estate can be an inflation hedge

The 1970s saw a 20% nominal drop in commercial real estate prices in the US, as rising interest rates led to refinancing difficulties for real estate owners, and slowing economic growth led to increased vacancies and weak rent growth.

But after the 1970s – real estate recovered very well, especially for high quality real estate in good locations.

So my takeaway, is that if you buy REITs, you want to (1) buy high quality real estate in good locations and (2) pick strong sponsors.

(1) is so that the real estate can hold its own in inflation and weakening economic growth, and (2) is so that the REIT does not go insolvent.

Don’t be penny wise pound foolish and buy REITs from a weak sponsor, unless they are deep value bargain.

That said, even if you do buy good quality REITs, I doubt if REITs will do as well this decade (inflation adjusted) as they did last decade, simply because of rising interest rates.

The one scenario I see REITs as doing very well is if the Feds keep interest rates artificially depressed while inflation is high (low real rates). Although in that scenario I think you probably make more holding commodities than REITs.

I will still buy REITs of course, but I may not necessarily be overweighting REITs in my portfolio.

I think the key with REITs this decade is to get the timing right. You want to get them as cheap as you can, hopefully in the depths of a liquidity event.

3) China – Different credit cycle from the West?

A couple months back, I saw the other area of value is China.

China is tricky.

As things stand, China banks trade at a ridiculous 8.8% yield.

For the record, the risks with China are very real, and include:

- Real estate debt crisis

- COVID zero

- Xi Jinping

- US sanctions

That said, China is also showing that they could be a hedge against the US/European assets, as China is the only big central bank out there easing monetary policy in the face of US tightening monetary policy.

You do want to position size carefully though.

If the doomsayers are right and we do see a China invasion of Taiwan, expect sanctions similar to those we saw on Russia, which could mean most of these investments written down to zero.

As always – love to hear what you think!