I’ve been getting quite a few questions for my latest views on banks.

As we all know, bank earnings (and share price) has been very strong in 2024.

But with the Feds (and global central banks) on a rate cut cycle – will 2025 be as kind to the banks?

As shared with FH Premium subscribers, I now think there is a risk that if not properly handled by policy makers, inflation may return in 2025, which could wreak havoc on the Fed rate cut cycle.

With all the uncertainty in play, is OCBC Bank at 1.25x book value and 5.8% dividend yield a good buy?

Let’s dive in.

Price Action for OCBC Bank remains bullish

Price action for now remains bullish.

OCBC Bank’s share price has been trending up since March 2024, and remains in an uptrend today.

Share price is up almost 20% in 2024 alone (excluding dividends).

Zooming out into the weekly chart – share price has clearly broken out of the 2021-2023 range it was stuck in for 2 years.

OCBC Bank’s Earnings are solid no doubt about it

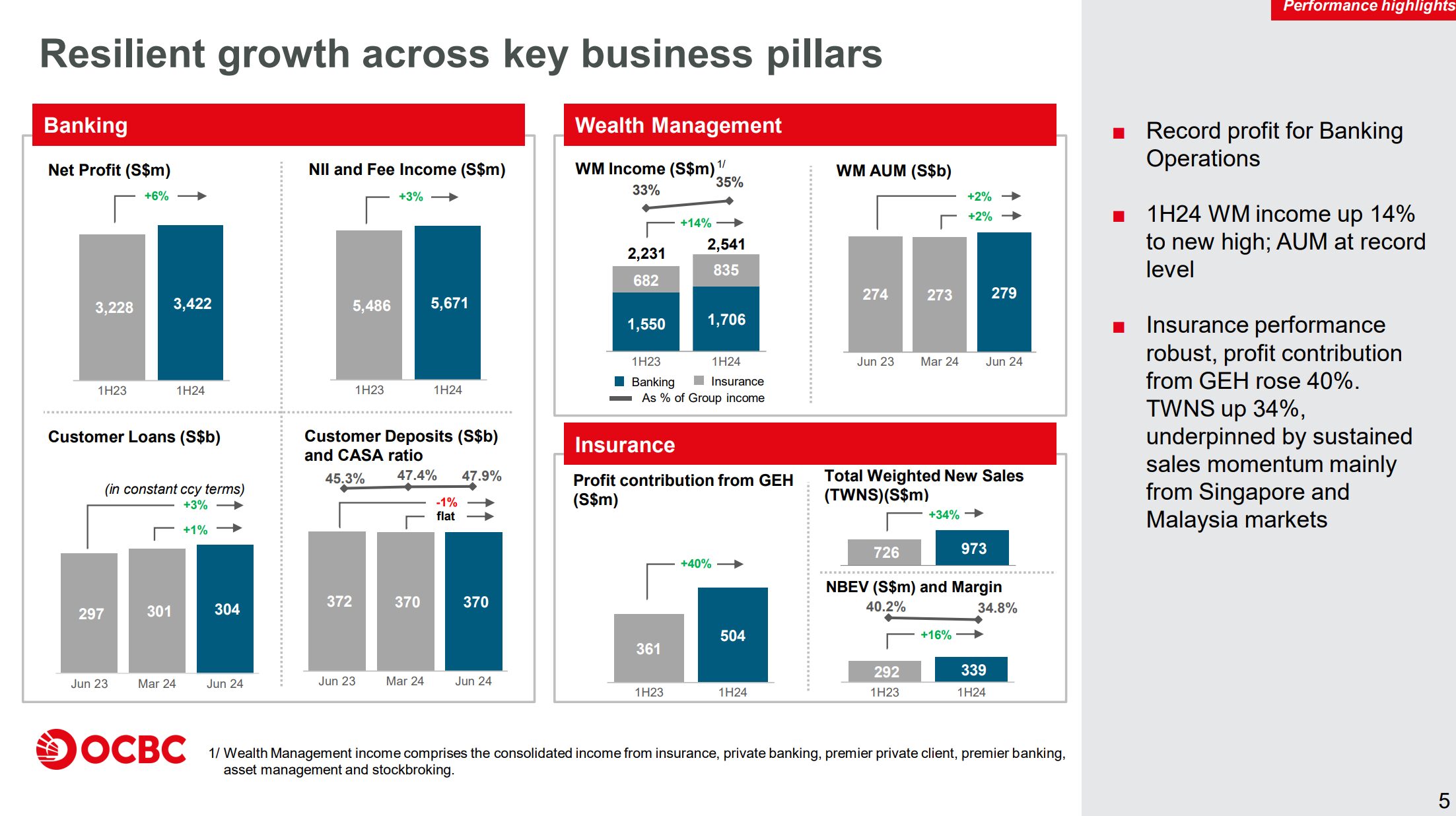

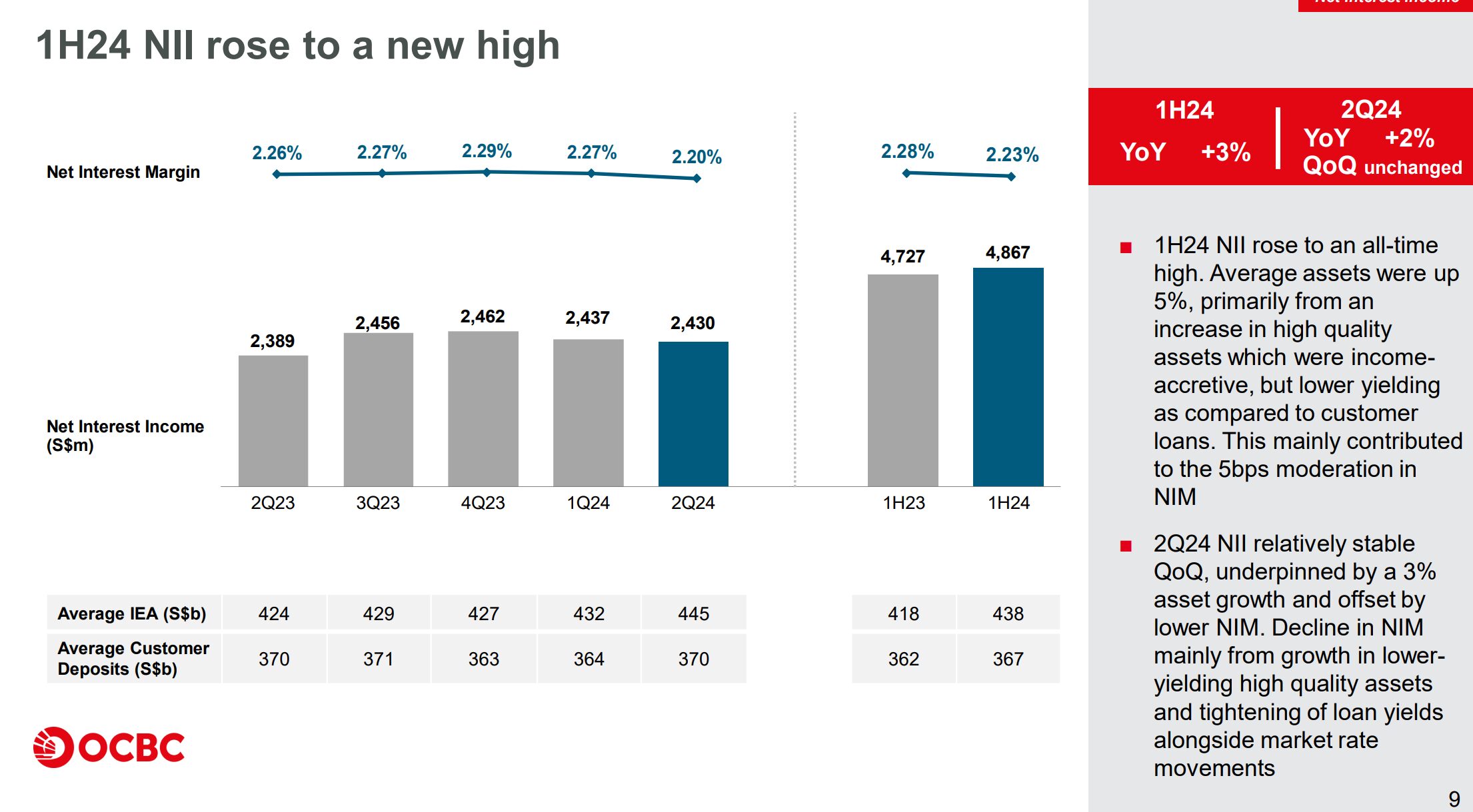

I extracted some charts below from the 1H24 earnings, but frankly I don’t think there is much to discuss there.

Across the board, OCBC’s earnings are solid, there’s no doubt about that.

The core earnings business remains very strong, with 1H 24 NII coming in at all time highs (although net interest income peaked in 4Q 2023).

Other business lines for OCBC are doing well

Wealth Management income is up 14% on a year on year basis.

Insurance is up 40% on a year on year basis.

According to OCBC this is due to strong sales momentum from Singapore and Malaysia, which I suppose reflects the strong economic performance for both countries.

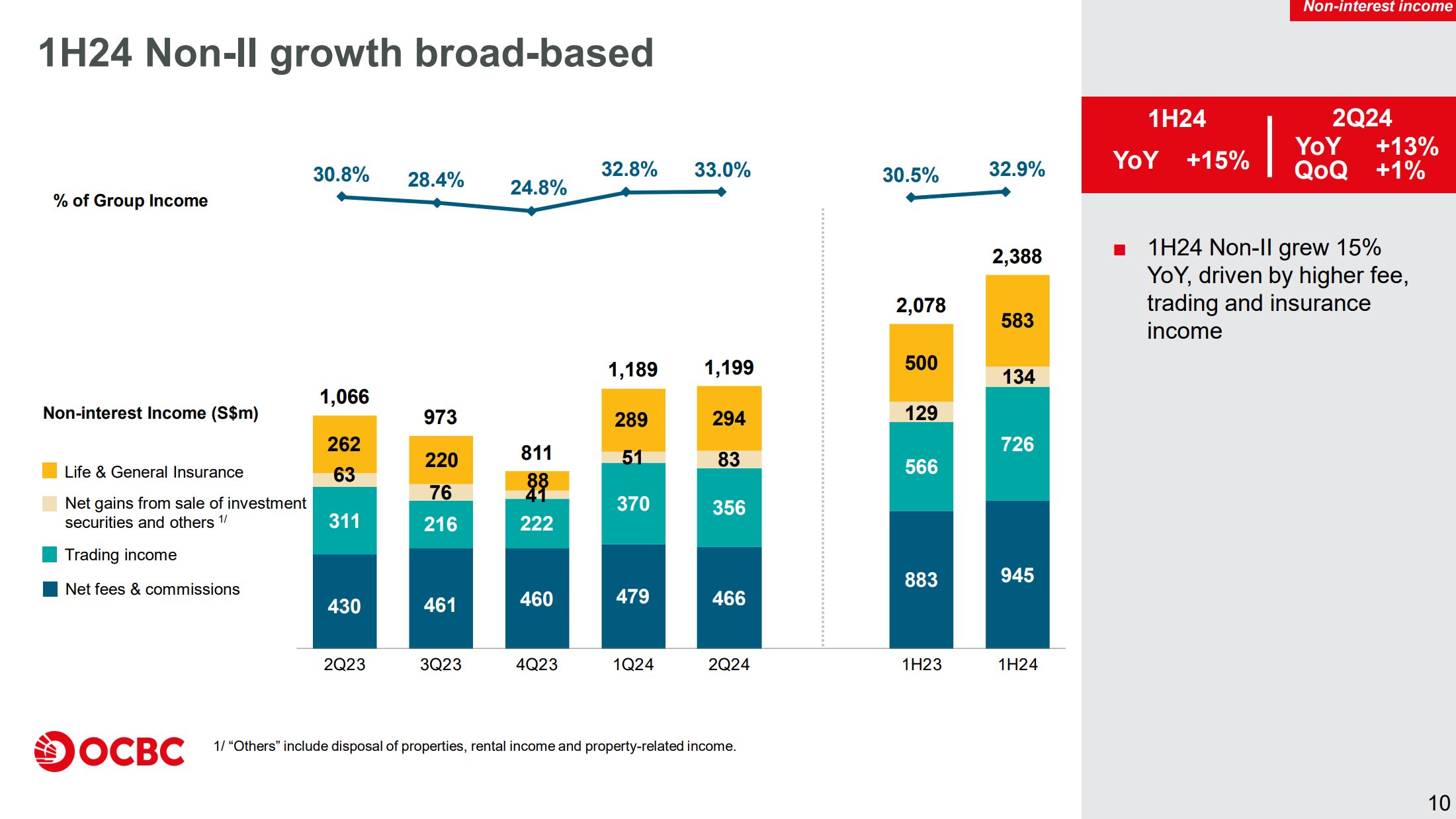

Total non-interest income is up 15% year on year, driven by higher fee, trading and insurance income.

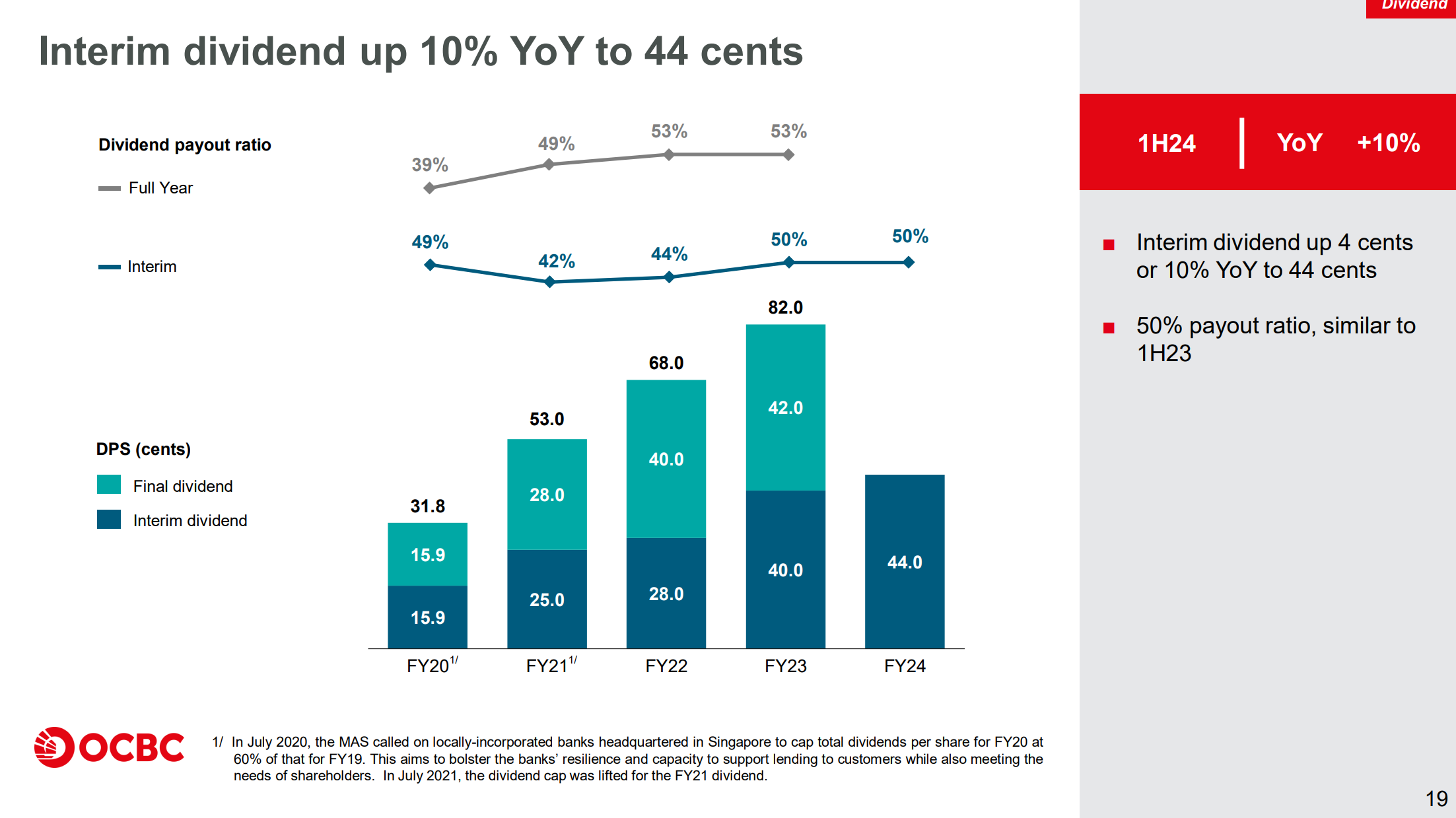

OCBC pays a 5.8% Dividend yield – at a 50% Payout Ratio

Because OCBC Bank’s earnings are so strong.

They raised their dividend 10%, while still maintaining the same 50% payout ratio.

This is why investors are so bullish, because if earnings growth stays strong, there could be further dividend increases.

Annualising the latest 44 cents dividend works out to about a 5.8% dividend yield.

But the risk is going forward?

But hey – you don’t need me to tell you that bank earnings today are solid.

And as Stanley Druckenmiller said.

Nobody invests in stocks for their earnings today.

You need to imagine where the earnings will be in 18 months time, and you invest on that basis.

18 months from today puts us roughly in mid 2026.

What would bank earnings look like then?

There is a risk inflation may return in 2025?

As shared with FH Premium subscribers, I now think that the Feds 50 bps might have been a mistake.

It led to the market overwhelmingly pricing in a soft landing, which could become self-fulfilling (once credit spreads start going down and translating into borrowing costs).

And if animal spirits resume in earnest (just look at crypto prices of late), I could really see this starting the clock running on the potential return of inflation in 2025.

How could this play out for bank earnings?

Let’s game this out.

Short term, the market is still overwhelmingly pricing in rate cuts.

Yes, less rate cuts are being priced in, but we’re still looking at baseline another 5 rate cuts to come (1.25% in rate cuts) over the next 9 months.

That will bring short term interest rates down.

But… long term interest rates have been picking up?

At the same time, long term interest rates are picking up as the market starts to price in higher inflation / more resilient economic growth in 2025 and beyond.

You can see how both the Singapore and US 10 year yields have retraced most of the Fed rate cut decline (and more):

But a steeper yield curve can be very strong for the banks – assuming no recession

This creates what is known as a steeper yield curve, as the differential between the long and short term interest rates increases:

This can be pretty bullish for bank stocks.

Reason being that banks borrow short and lend long.

If short term interest rates go down, they can pay depositors lower interest rates.

And yet because of higher long term interest rates, they can lend out at a higher interest rate to borrowers.

So a steeper yield curve can lead to higher net interest margins for banks.

So far at least, this hasn’t played out – but definitely something to watch out for in the next few quarters:

Things are seldom so simple?

But as we all know, things are seldom so simple.

The complexity is that rising long term interest rates have the potential to slow economic activity.

Higher long term interest rates will impact asset prices, and translate into higher borrowing costs, reversing the entire cycle above.

So if long term interest rates surge higher, you do want to be very careful on how that would impact asset prices (and the economy).

This cycle, each time the US 10 year yield goes into the 4.5 – 5.0% range it has created problems for asset prices which then flowed over into the economy, so that is a risk to watch out for.

Why do I spend so much time discussing US monetary policy?

Now I always get a lot of questions as to why I spend so much time discussing the US economy when analysing the Singapore banks.

The background is that because the MAS chooses to control SGD’s FX strength, MAS loses the ability to control domestic interest rates.

So Singapore interest rates are market determined – and they track US interest rates very closely.

Which means that if you want to understand the path for SGD interest rates, you need to understand the outlook for US interest rates.

There’s just no way around it.

So… will Bank stocks drop in 2025?

Now some of you have asked whether bank stocks will drop in 2025, but I’m not sure if that is the right question to ask.

The better question might be – how much will you lose if you are wrong and bank stocks drop, vs how much will you make if you are right and bank stocks go up?

And what are the probabilities of each event?

For that some analysis on valuations is required.

Valuations of OCBC Bank

The long term Price/Book chart of OCBC is set out below.

OCBC trades at 1.25x book value today.

What’s the upside for OCBC Bank?

Let’s say things get really crazy – we get a soft landing, steeper yield curve, and economic growth roars in 2025-2026.

Maybe OCBC goes back to the 2018 peak of 1.55x book value.

That’s about 24% upside.

Don’t forget the 5.8% dividend yield.

You’re looking at maybe 30% upside in this scenario.

What’s the downside for OCBC Bank?

What if things head south?

We get a recession, Feds slash interest rates.

0.80x book value was the COVID bottom, and I don’t think we go back there unless it’s a very bad recession.

Let’s say 1.0x book value as the downside risk.

That’s about 20% capital loss.

There is the 5.8% dividend yield to cushion some of the downside, but no doubt dividend will be cut in this scenario.

Let’s say 20% downside risk in this scenario.

What’s the probability of each event?

So 30% upside if you’re right, 20% downside if you’re wrong.

If it were a 50-50 chance of both outcomes that would be a no brainer in itself.

But in reality – what’s the probability of each event?

Well you tell me.

My personal views?

I would add that the next 3 weeks are going to be absolutely crucial to watch – as it sets the tone for the next 4 years.

If Trump wins, the Feds continue cutting, and markets react positively to both events – I would be really worried for the return of inflation in 2025 (although the short term could be bullish).

If Harris wins, it’s probably less bullish for the economy in in the short term, and it would depend more on how other factors (eg. Fed rate cuts, China stimulus) play out.

Follow Financial Horse to avoid missing any post!

Why did I buy OCBC Bank?

In the spirit of full disclosure – I myself hold a position in OCBC Bank, and I added to the position recently.

But I do want to caveat that I do not run a large position in OCBC Bank in my portfolio.

I know some of you have 50% of your portfolio in the Singapore banks, and I am not one of those (my full portfolio shared on FH Premium).

This matters because yes while I bought more OCBC Bank, if the share price drops by 50% the next 12 months, it would actually be a net positive outcome for me as I would be more than happy to load up in that scenario.

For guys who already hold a good chunk of Singapore bank stocks, a scenario like that would make you very nervous.

So that’s the nuance that you need to appreciate.

Is OCBC Bank a good buy?

But coming back to the stock.

There is no doubt in my mind that the historical earnings for OCBC are very solid.

The question is what happens next.

If we get a mix of a soft landing / inflation in 2025 – 2026, I could see OCBC’s earnings holding up pretty well.

The core lending business should stay strong supported by a steeper yield curve, and you may even see stronger loan growth in that scenario.

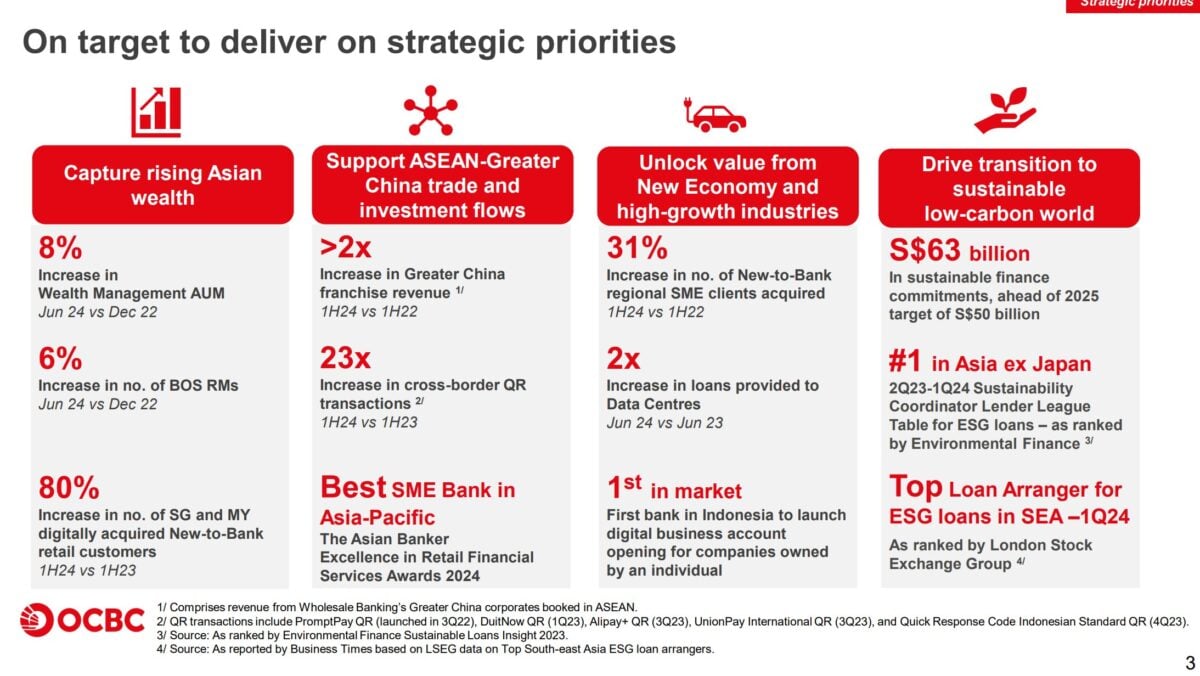

In terms of growth going forward this is what OCBC is targetting:

- Capture rising Asian wealth (wealth management)

- Benefit from ASEAN-Greater China trade and investment flows

- Unlock valaue from new economy / high growth industries

In a soft landing / inflation I could see these things continuing to perform well.

How will the Singapore economy perform?

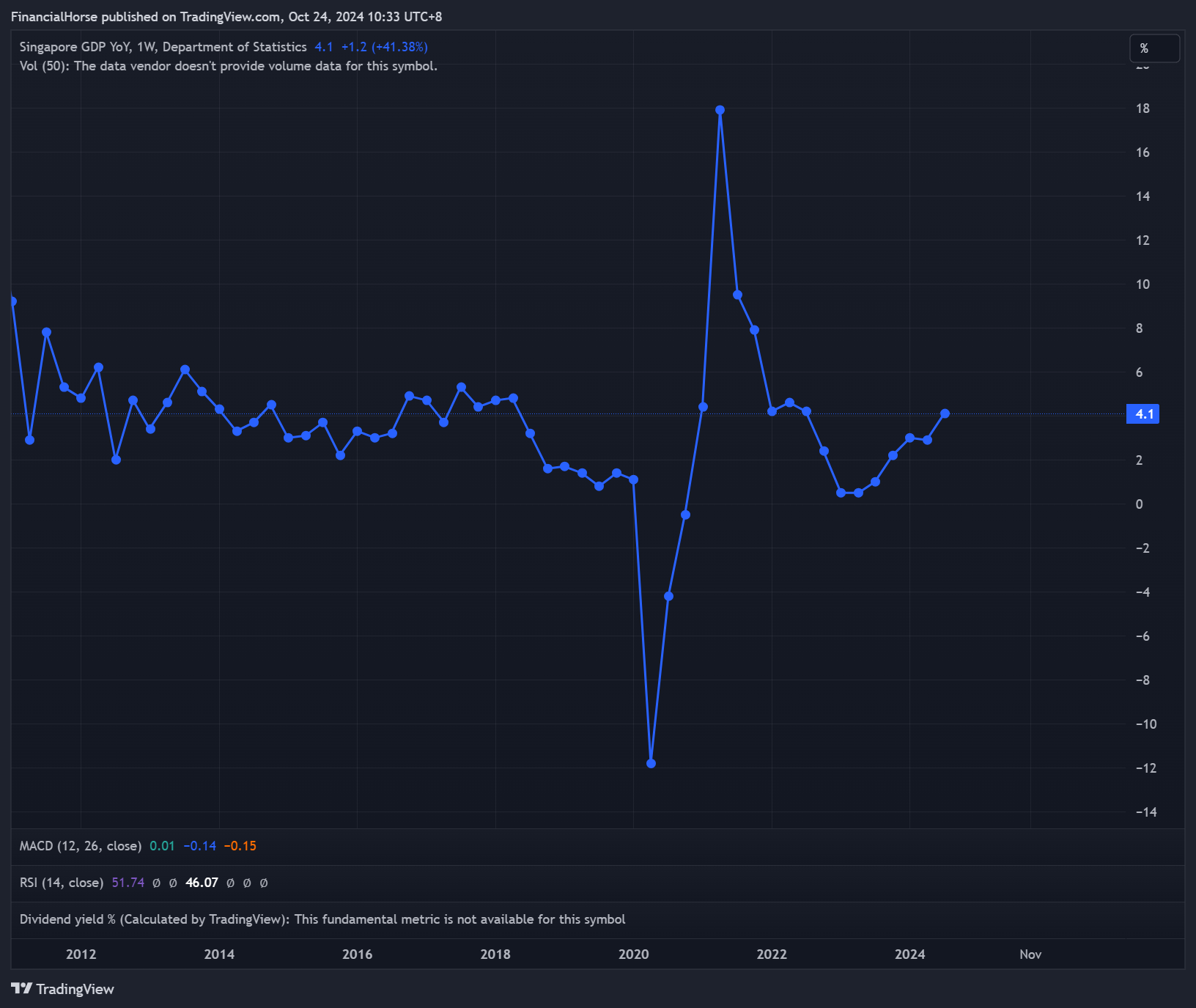

For what it’s worth, Singapore’s GDP growth remains pretty solid so far.

GDP growth picked up to 4.1% year on year, and looks to have bottomed in the first half of 2023.

If this holds, that is bullish for Singapore banks as it could translate into higher loan growth as short rates come down.

Is OCBC Bank the most attractively valued Singapore bank today?

I also like that OCBC Bank is perhaps the most attractively valued Singapore bank today.

Relative valuations below – and I’m sorry but I just find DBS Bank richly valued at 1.78x book value today.

It’s like what Jamie Dimon said about buying back JP Morgan stock at 2x book value – “We’re not going to buy back a lot of stock at these prices”.

Yes I know that DBS has world beating ROE, but I struggle to buy a meaningful amounts of DBS Bank at close to 1.8x book.

With OCBC Bank at least it trades a lot closer to book value – less downside if you’re wrong.

| Bank | Dividend Yield (%) | Book Value (x) | ROE (%) |

| DBS Bank | 5.5 | 1.78 | 17.0 |

| UOB Bank | 5.3 | 1.14 | 12.2 |

| OCBC Bank | 5.8 | 1.23 | 13.4 |

So… why not buy more OCBC Bank stock?

I guess looking at the above it would come across as me being very bullish on OCBC Bank.

So why not back up the truck on OCBC Bank?

I think fundamentally it goes back to the point that if the upside scenario above plays out.

That we get a soft landing, steeper yield curve, economic growth roars in 2025-2026.

There are going to be asset classes that will perform a lot better.

Bitcoin for example, or US Tech stocks, or commodities.

Heck even gold is up 33% this year and blown past the performance of all 3 bank stocks:

So yes, Singapore bank stocks are great from a diversification perspective.

But for now a good chunk of my portfolio is in stuff like US Tech, Bitcoin, Commodities etc that could perform even better in the upside scenario (see my full portfolio on FH Premium).

But I do not deny that those asset classes have much higher volatility and require more active risk management, and not suitable for everyone – in which case banks like OCBC could be an alternative.

Whatever the case, I would love to hear what you think.

Is OCBC Bank a good buy today? Will bank stocks drop in 2025?

This post is written on 25 Oct 2024 and will not be updated going forward. My latest views on markets, my Stock watchlist and full Personal Portfolio, are shared on FH Premium.

Hi

Thanks. Been looking at bank stock recently, based on current book value , Ocbc still slightly higher but the downside risk still seems better control. Worse is below 0.8 book value which unlikely unless big impact occur. If inflation head back, fed likely will increase or revert back interest rate but however they also need to worry about recession… China and US trade war and increase taxes have made export and import challenging… if recession came in, increase interest rate will be serious matter….

Thank you, appreciate the comments!

For OCBC share price, the rise has not been linear. If investors look back, OCBC share price was given a jolt with the announcement of voluntary unconditional offer for Great Eastern Holdings on 10 May 2024. The market had reacted very positively as OCBC share price rose to a 5-month high to reach $14.50 back then (normally shares of the acquirer would drop). Investors probably felt that the acquisition of Great Eastern is a major feather in the cap for CEO Helen Wong.

The privatisation of GEH would be a significant, yet a low-hanging fruit for the CEO Helen Wong. She would have achieved a feat not accomplished by previous CEOs – David Connor and Samuel Tsien. As Great Eastern has evolved to become a crown jewel for OCBC, the acquisition is definitely a strategic move. It would also cement OCBC as a leading financial powerhouse.

Regards,

Gerald

https://sgwealthbuilder.com

Interesting comment. I suppose you need to overlay this with the macro as well, as there were a lot of changes in the interest rate / inflation outlook during the same time period.

I do agree that the GEH privatisation is a good move though. OCBC has a lot of excess capital, and they bought GEH at a good price.

Thanks for the detailed post as always. 2 questions:

1) Why pick OCBC over UOB? Is it the dividend yield and ROE? Since UOB’s P/B is lower.

2) Which brokerage would you recommend for local stocks?

Many thanks!

Personally I use DBS Vickers Cash Upfront, but FSMOne or POEMs are decent options too.

OCBC – I like OCBC for certain reasons as shared, but UOB is a decent pick as well. From a macro perspective they are very similar plays (all 3 banks).

I agree. At 1.8X to book value, I would not touch DBS at all. OCBC and UOB would be an easy pick. I think UOB forward earnings prospects is probably slightly better but thats a feeling just based on the prospect of Citi Wealth Banking business adding to the earnings a little more in 2025.

Thanks, appreciate the input very much!