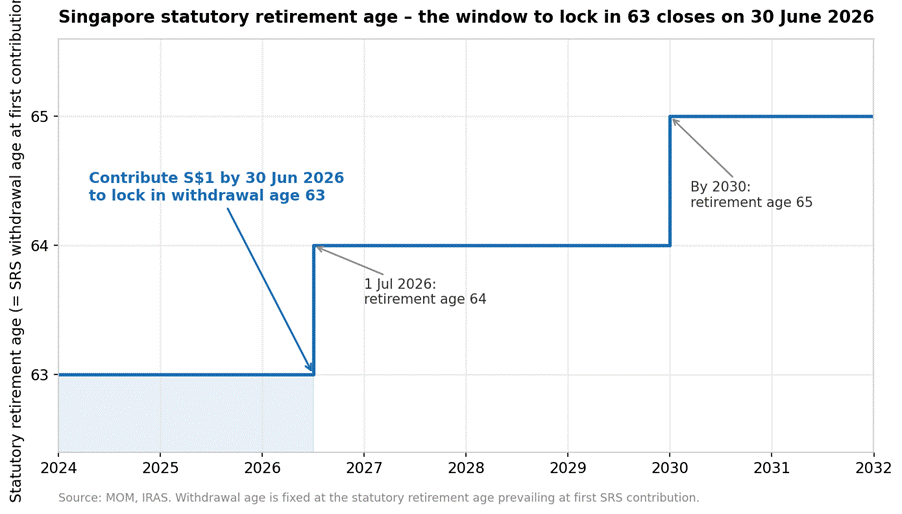

On 1 July 2026, Singapore’s statutory retirement age increases from 63 to 64.

Buried within this change is a detail that matters for anyone who has not yet opened a Supplementary Retirement Scheme (SRS) account.

Your SRS withdrawal age – the age at which you can access your SRS savings without penalty – is fixed at the statutory retirement age prevailing at the time of your first contribution.

From 1 July 2026, that age becomes 64.

In plain English – if you open an SRS account and contribute a minimum of S$1 by 30 June 2026, you lock in the current withdrawal age of 63 – for life.

That gives you penalty-free access to your SRS savings a full year earlier, regardless of when you actually start contributing in earnest.

For $1, I think that’s a no brainer.

In this article, I wanted to discuss how the SRS works, why the withdrawal age lock-in matters, and why I think the S$1 top-up before the deadline is worth doing even if you have no immediate plans to use the SRS.

A quick refresher – what is the SRS?

The SRS is a voluntary scheme that complements CPF for retirement savings. Unlike CPF, contributions are entirely at your discretion – you decide if, when, and how much to contribute each year.

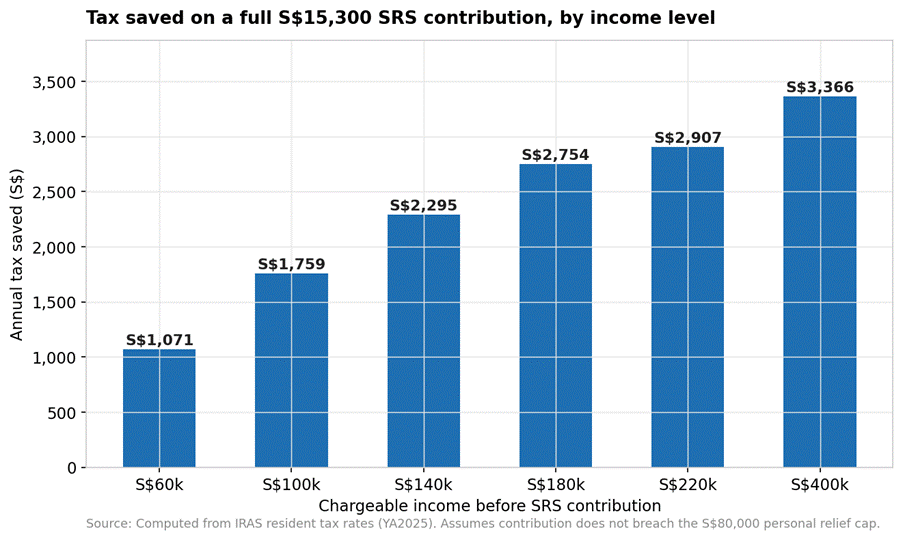

The point of doing this is simple – tax relief.

Every dollar you contribute reduces your chargeable income dollar-for-dollar, up to S$15,300 per year for Singaporeans and PRs, and S$35,700 for foreigners.

For anyone paying a meaningful amount of income tax, this is one of the most straightforward tax planning tools available.

You can see the indicative savings below for a full S$15,300 contribution at different income levels.

| Chargeable income (before SRS) | Marginal tax rate | Tax saved on S$15,300 contribution |

| S$120,000 | 11.5% | ~S$1,760 |

| S$160,000 | 15% | ~S$2,295 |

| S$200,000 | 18% | ~S$2,754 |

Note that SRS relief counts towards the S$80,000 personal income tax relief cap, so those with substantial existing reliefs should run the numbers before contributing.

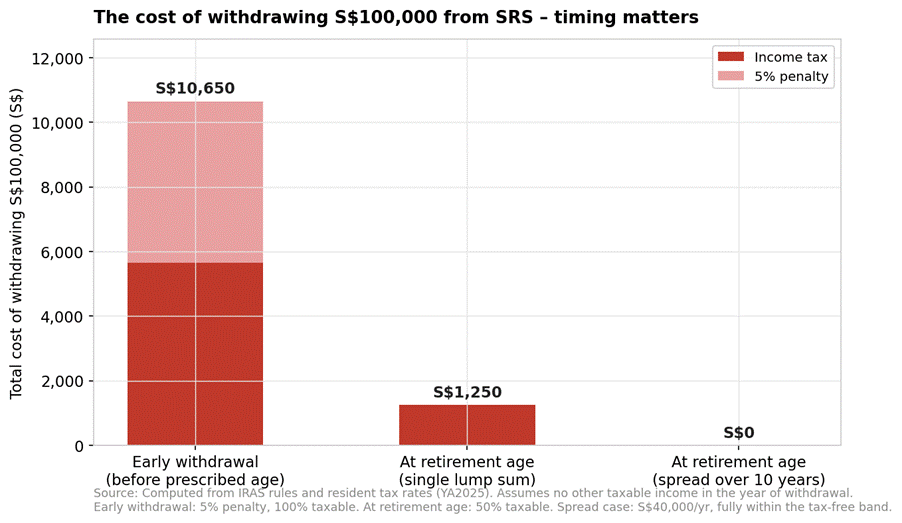

The trade-off – your money is locked up

The relief comes with strings attached. If you withdraw before your prescribed retirement age, you pay a 5% penalty on the amount withdrawn, and 100% of the withdrawal is taxable as income in that year.

That combination will typically wipe out the tax benefit, and then some.

Because for example if your marginal tax rate is 11.5%.

And you decide to withdraw $100,000.

Not only do you pay the 11.5% tax rate, you also have to pay a 5% penalty on top of that.

A 16.5% tax bill for early withdrawal – which goes even higher if you tax bracket is high.

BUT – if you Withdraw at or after your prescribed retirement age, the treatment is far more favourable.

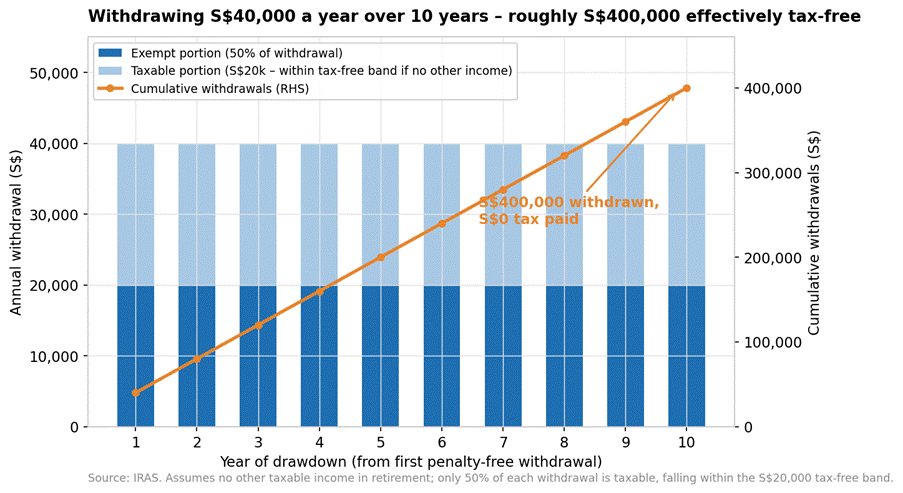

Only 50% of each withdrawal is taxable, and you can spread withdrawals over a period of up to 10 years from your first penalty-free withdrawal.

In plain English – if you withdraw S$40,000 a year in retirement with no other taxable income, only S$20,000 is taxable, which falls entirely within the tax-free band.

Spread over 10 years, that means roughly S$400,000 can be withdrawn effectively tax-free.

You get the tax deduction on the way in, and pay little to no tax on the way out.

So SRS is a very efficient tool for managing your tax bill if you manage it well.

Why the withdrawal age lock-in matters

Which brings us to the key mechanic.

Per IRAS, your prescribed retirement age is the statutory retirement age in force when you make your first SRS contribution – and subsequent increases in the retirement age do not affect you.

This is summarised below:

| Date of first SRS contribution | Penalty-free withdrawal age (locked in for life) |

| On or before 30 June 2026 | 63 |

| 1 July 2026 onwards | 64 |

| After the next legislated increase (by 2030) | 65 |

In other words, if you top up on or before 30 June – you lock in your age 63 withdrawal age for SRS for life.

Three reasons why I think this is huge if you even plan to use SRS.

1. A full year of flexibility. Locking in age 63 means penalty-free access to your SRS savings a year earlier. For those planning early retirement, that is twelve months of additional liquidity to bridge the gap before CPF LIFE payouts begin at 65 – without triggering the 5% penalty and full taxation.

2. An earlier start to the 10-year drawdown window. Your 10-year withdrawal period runs from your first penalty-free withdrawal. Starting at 63 rather than 64 gives you an extra year to spread withdrawals tax-efficiently, particularly useful in the years before other income streams kick in.

3. This is not the last increase. The retirement age is legislated to rise to 65 by 2030, with the re-employment age reaching 70. Anyone who keeps putting off that first contribution will eventually lock in 65 – a full two years later than what is available today. The window to secure age 63 closes permanently on 30 June 2026.

The cost of locking in? Effectively zero

And to be clear – there is no catch to this.

The lock-in requires nothing more than opening an SRS account with one of the three local banks (DBS, OCBC or UOB) and contributing S$1 before the deadline.

There is no obligation to contribute further, no recurring fees on the account itself, and no commitment to any investment strategy.

You are simply preserving the option to access your savings at 63 instead of 64 – an option that costs a dollar today and cannot be repurchased later at any price.

In risk-reward terms, this is about as asymmetric as it gets.

The downside is S$1 and maybe five to ten minutes of your time.

The upside is a permanently earlier withdrawal age on what could eventually be a six-figure retirement pot.

Never miss a post! Follow Financial Horse by subscribing or following us on your favorite platform:

Subscribe to our mailing list for exclusive content straight to your inbox:

One more thing – don’t leave your SRS funds idle

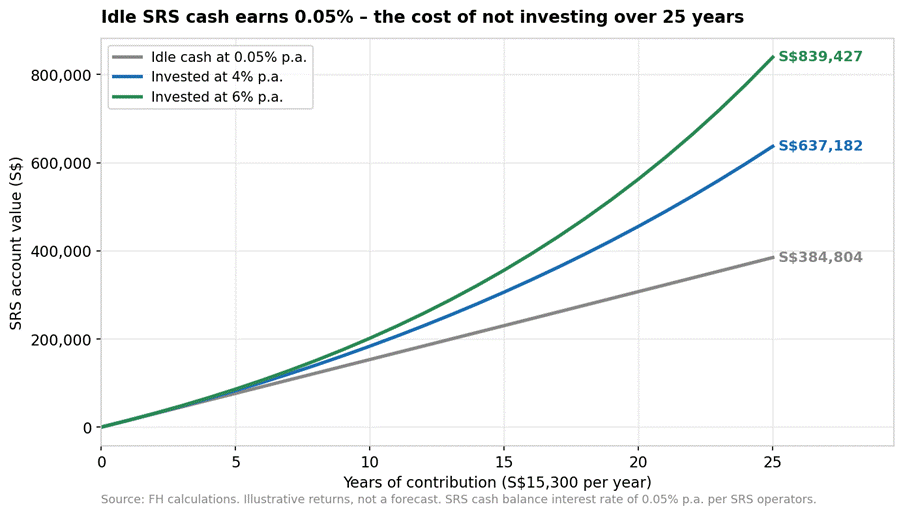

A common mistake worth flagging. Cash sitting in an SRS account earns just 0.05% per annum – and yet as at end-2024, roughly 19% of total SRS contributions (about S$3.9 billion) sat as idle cash.

Compounded over a 25 year period – the difference of investing and not investing your SRS funds is absolutely massive:

Once you start contributing meaningfully, the funds can be deployed into T-bills, Singapore Savings Bonds, fixed deposits, SGX-listed shares and REITs, ETFs, unit trusts, or single-premium insurance.

Given that SRS money is locked up until retirement age anyway, the long investment horizon is well suited to putting that capital to work.

What do I use my SRS for?

Personally I use my SRS funds to buy SGX listed stocks – think like bank stocks, REITs etc.

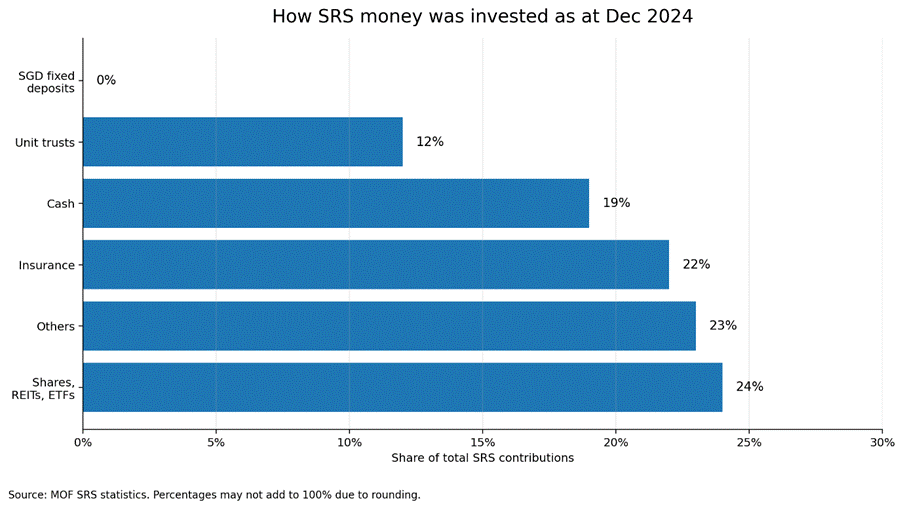

For reference – here is how other investors typically invest their SRS money – again shares, REITs and ETFs are the big one:

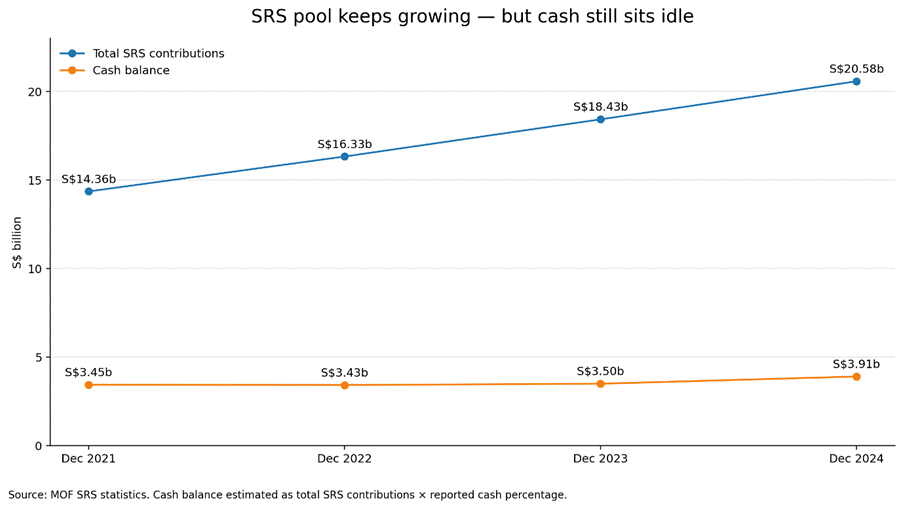

And it seems like most Singaporeans are pretty smart about it – because while SRS contributions keeps growing, the cash balance is roughly flat, indicating that most investors have been deploying their SRS funds.

But that is a decision for later. The S$1 contribution itself does not need to be invested – its job is simply to start the clock.

Who should think twice?

To be fair – the SRS is not for everyone

For example:

- If you pay little or no income tax, the tax relief is worth little to you, and locking up money until your 60s carries a real opportunity cost.

- If you may need the funds before retirement age, the 5% penalty plus full taxation on early withdrawal makes the SRS a poor fit for that portion of your savings.

- If you are already at or near the S$80,000 relief cap, additional SRS contributions may generate little incremental tax benefit.

But none of these caveats argue against the S$1 top-up itself.

Nobody is saying you need to top up $100,00 into SRS today.

You just need to top up $1 – to lock in your statutory retirement age for SRS.

This gives you optionality – and whether you use SRS or not going forward is a separate decision you can make on your own time.

Closing thoughts – a S$1 decision with a hard deadline

Most personal finance decisions involve genuine trade-offs. This one largely does not.

This is as close to a free lunch as it gets.

If there is any chance the SRS fits into your retirement picture down the road – and for anyone paying meaningful income tax, it probably should – contributing S$1 before 30 June 2026 locks in the age-63 withdrawal age at essentially no cost.

The decision on whether to contribute the full S$15,300 a year can come later, on your own timeline.

Miss the deadline, and your withdrawal age steps up to 64 – and eventually 65 for those who continue to wait.

To me it’s a no brainer.

Love to hear what you think though! Have you locked in your withdrawal age, or do you not see the SRS fitting into your plans?

This article was written on 12 June 2026. It will not be updated going forward.

My latest macro views, as well as my full stock watch and personal portfolio, are shared on FH Premium.