For some reason, I get a lot of questions on Keppel Infrastructure Trust.

Here’s one of the most recent questions I received recently:

Hi FH,

would you be doing an update on KIT (Keppel Infra Trust) ?

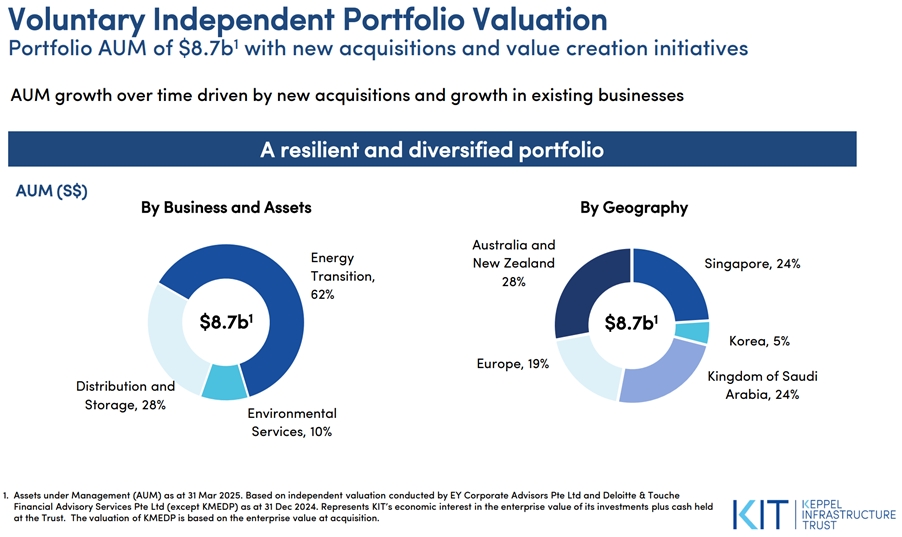

KIT will be acquiring an approximate 46.7 per cent stake in subsea cable solutions provider Global Marine Group (GMG) from Keppel Infrastructure Fund (KIF)

thanks

Long time readers know that I hold a position in Keppel Infrastructure Trust that I bought about 2 – 3 years back.

I bought in the 40s range, so yes I am technically underwater if you compare the buy in price.

But this business trust has been paying a 10-15% dividend yield a year for the past few years (including special dividend).

So after factoring in the dividend yield, this investment has actually done pretty well for me all things considered.

So let’s have a closer look at Keppel Infrastructure Trust, and whether I will add to my position.

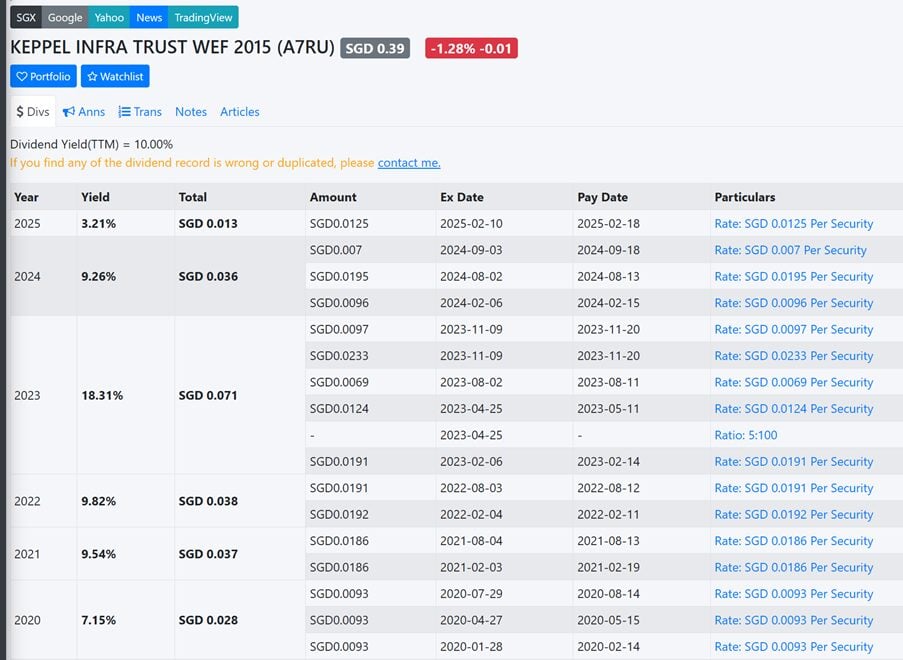

Price action for Keppel Infrastructure Trust is not pretty

Here’s the long-term price chart for Keppel Infrastructure Trust.

Spoiler alert – it’s not pretty.

You can see how it’s in a long-term downtrend.

And has broken below all major supports (holding at the 0.39 support now), and sits below all key moving averages.

But… Keppel Infrastructure Trust pays a trailing 10% dividend yield at this price

That said, the dividend is very, very juicy.

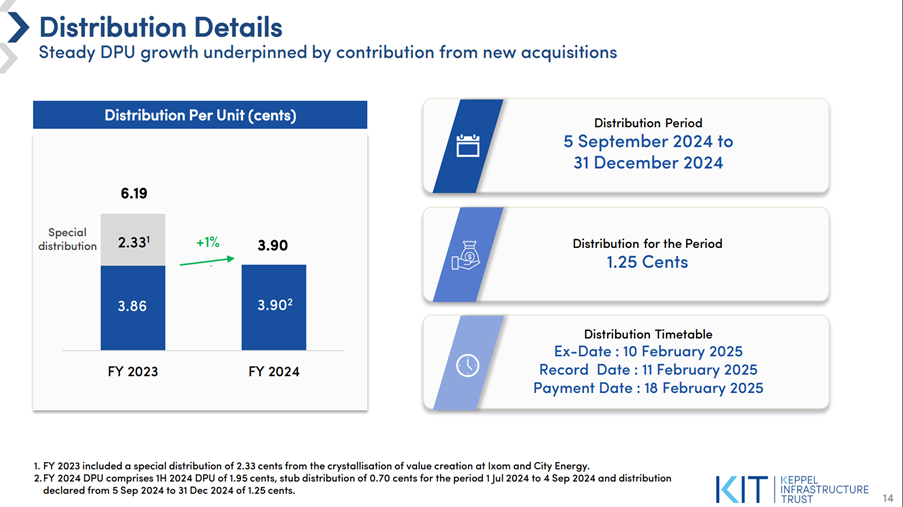

You’re looking at 3.90 cents in DPU for FY 2024.

Using the latest 0.39 share price, that works out to a solid 10% dividend yield.

The same dividend was 3.86 in FY 2023, so you can’t even argue that the DPU is declining.

In fact in FY 2023, if you include the special one-off dividend, that’s a 6.19 cents DPU which is a 15.9% dividend yield.

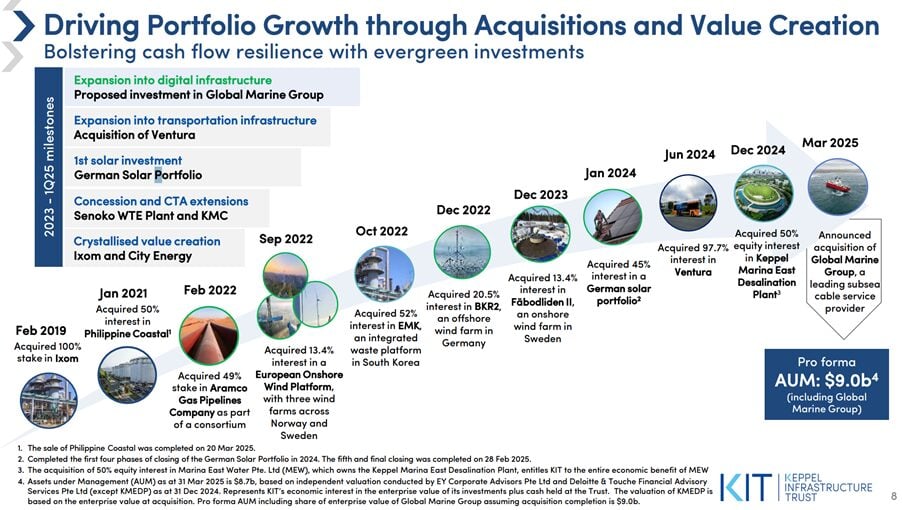

Recent Divestments by Keppel Infrastructure Trust

Remember how I had a lot of comments on Keppel Infrastructure Trust buying an Australian bus company, and how I was worried there would be no real synergies with the business?

Well – there’s a development, because Keppel Infrastructure Trust has now announced that they are selling a 24.62% stake:

Here’s the announcement (emphasis mine):

Keppel Infrastructure Trust to divest partial stake in Australian bus service business Ventura, for A$130 million

Singapore, 10 June 2025 – Keppel Infrastructure Fund Management Pte. Ltd. (KIFM), as Trustee-Manager of Keppel Infrastructure Trust (KIT), is pleased to announce that KIT will be divesting a 24.62% stake in Ventura Motors Pty. Ltd. (Ventura), the largest bus service business in the State of Victoria, Australia to private investment funds managed by Samsung Asset Management (Samsung). The sale consideration of the transaction is A$130 million (or approximately S$109 million), which is approximately 19% higher than the amount paid by KIT at acquisition for the relevant stake.

Post transaction, KIT and Andrew Cornwall, CEO of Ventura, will continue to hold stakes of 73.06% and 2.32% respectively in Ventura.

KIT acquired a 97.68% stake in Ventura in June 2024 for an enterprise value of A$600 million. Headquartered in Melbourne, Australia’s largest city, Ventura has a fleet of about 900 buses and 12 strategically located depots and has the largest market share of public bus services in Victoria, operating approximately 530 routes out of Melbourne’s ~1,200 total routes and transporting more than 42 million people annually.

Mr Kevin Neo, CEO of KIFM, said, “As part of KIT’s value creation strategy, we are pleased to be able to realise the upside in Ventura’s value through the divestment of a partial stake to Samsung. This divestment, coupled with our earlier divestment of our 50% stake in Philippine Coastal Storage & Pipeline Corporation, both amounting to approximately S$301 million, will bolster KIT’s financial strength and agility, and enhance KIT’s ability to capture further opportunities through strategic capital recycling.”

Very, very interesting indeed.

The sale at a 19% premium is definitely nice, as this is the exactly what you want to see as a unitholder (the fund manager buying low and selling high, not the other way around).

But the sale of a minority stake, to bring in a partner, just 1 year after buying Ventura.

That really got me thinking about what is Keppel Infrastructure Trust’s longer term acquisition strategy here.

And for that, let’s look at some other recently announced transactions:

- The sale of Philippine Coastal

- Acquisition of Global Marine Group

Divestment of Philippine Coastal

If you look back at the timeline.

You’ll realise that Philippine Coastal was acquired by Keppel Infrastructure Trust in 2021.

So they’re selling the investment just 4 years later, which is a pretty short-term holding period for a business trust where you would usually expect them to be long-term investors.

Similar reasoning with Ventura above, where KIT is selling the 24% stake just 1 year after acquiring the asset.

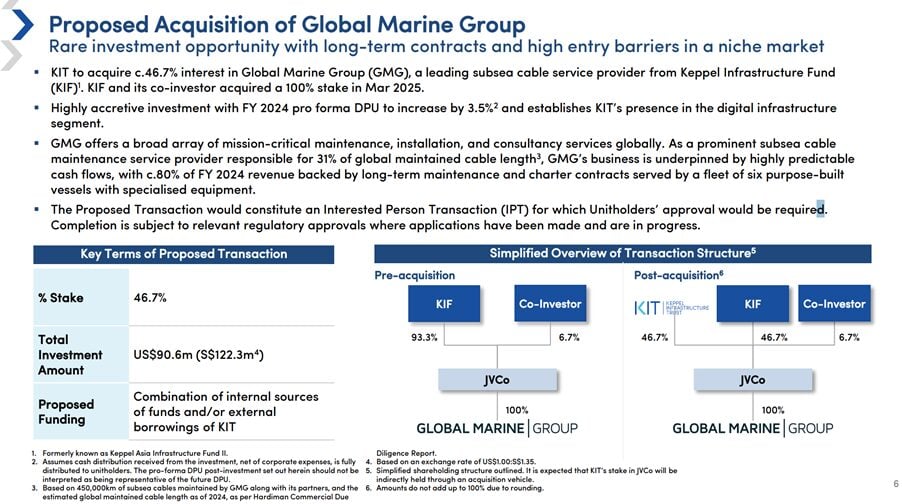

Acquisition of Global Marine Group

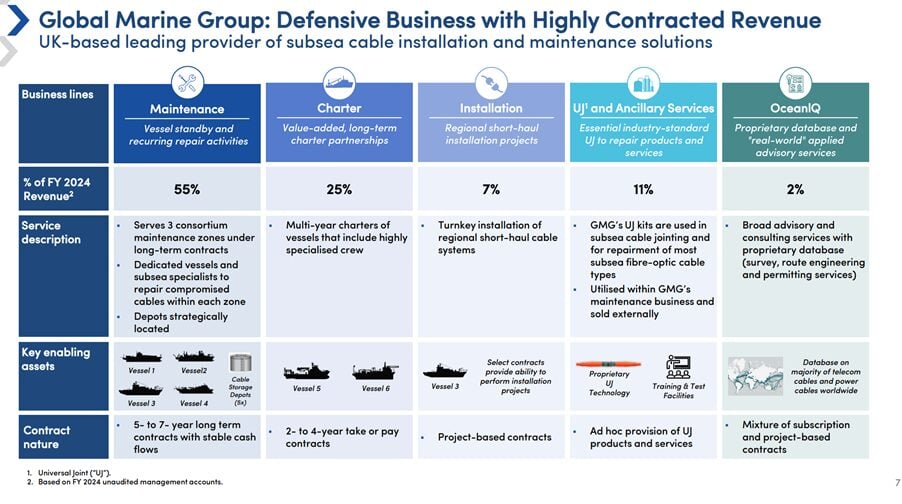

And then we have the acquisition of Global Marine Group (emphasis mine):

Key Investment Details

- KIT to acquire c.46.7% interest in Global Marine Group (GMG), a leading subsea cable service provider from Keppel Infrastructure Fund (KIF). KIF and its co-investor acquired a 100% stake in Mar 2025.

- Highly accretive investment with FY 2024 pro forma DPU to increase by 3.5% and establishes KIT’s presence in the digital infrastructure segment.

- GMG offers a broad array of mission-critical maintenance, installation, and consultancy services globally. As a prominent subsea cable maintenance service provider responsible for 31% of global maintained cable length, GMG’s business is underpinned by highly predictable cash flows, with c.80% of FY 2024 revenue backed by long-term maintenance and charter contracts served by a fleet of six purpose-built vessels with specialised equipment.

- The Proposed Transaction would constitute an Interested Person Transaction (IPT) for which Unitholders’ approval would be required. Completion is subject to relevant regulatory approvals where applications have been made and are in progress.

Key Terms of Proposed Transaction

| Term | Details |

| % Stake | 46.7% |

| Total Investment Amount | US$90.6m (S$122.3m) |

| Proposed Funding | Combination of internal sources of funds and/or external borrowings of KIT |

For what it’s worth I think this is a decent asset with long term recurring cashflow.

But my concern is largely similar to that with the Ventura acquisition.

As a Singapore based fund – what competitive advantage, or what value add does Keppel Infrastructure Trust bring to the table?

How sound is the long term acquisition strategy of Keppel Infrastructure Trust?

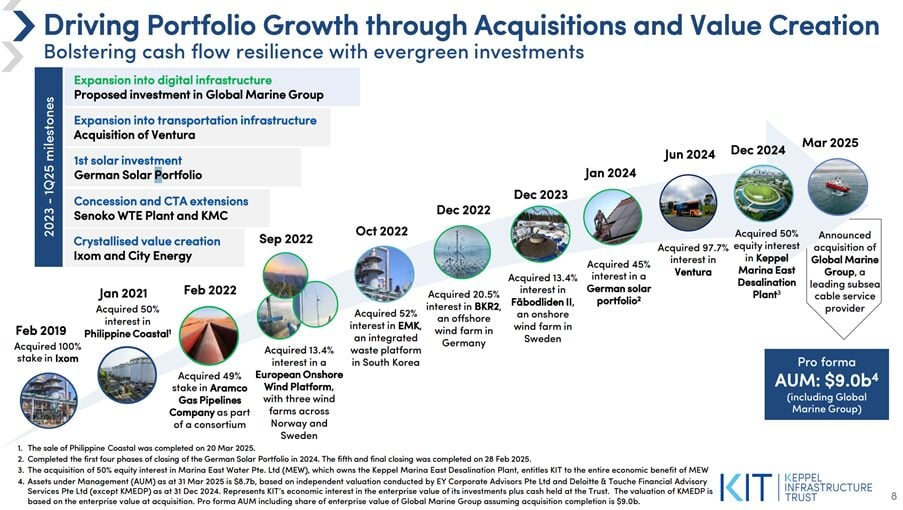

I asked ChatGPT to summarise all acquisitions / divestments made by KIT in the past 5 years.

Adding in picture form as the table may not display well on mobile:

Table in text form:

| Year | Move | Asset | Sector | Location | Size (S$ approx.) |

| 2021 | Acquire | Philippine Coastal Storage & Pipeline (80 %) | Liquid-fuel storage | Philippines | S$ 445 m EV (US$334 m) (reuters.com) |

| 2022 | Acquire | Aramco Gas Pipelines Co. (minority note) | Gas transmission | Saudi Arabia | S$ 336 m (US$250 m) commitment (sbr.com.sg) |

| Acquire | SingSpring Desalination (remaining 30 %) | Water desalination | Singapore | S$ 12 m (links.sgx.com) | |

| Acquire | European On-shore Wind platform (JV) | On-shore wind | Norway/Sweden | S$ 86 m initial equity (JVCo) (wpcms.kepcorp.com) | |

| Acquire | Eco-Management Korea Holdings (52 %) | Waste-to-energy & recycling | South Korea | S$ 666 m (100 % stake) (keppel.com) | |

| Acquire | Borkum Riffgrund 2 offshore wind (≈25 % via JV) | Off-shore wind | Germany | S$ 445 m joint purchase (keppel.com) | |

| 2023-25 | Acquire (5 closings) | German rooftop-solar portfolio (45 %) | Distributed solar & storage | Germany | S$ 159 m max commitment (kepinfratrust.com) |

| 2024 | Acquire | Ventura Bus Services (≈99 %) | Public transport | Australia | S$ 540 m EV (A$600 m) (keppel.com) |

| Acquire | Marina East Water (50 % equity; 100 % economics) | Dual-mode desalination | Singapore | S$ 355 m EV (~50 % stake) (kepinfratrust.com) | |

| 2025 | Acquire | Global Marine Group (46.7 %) | Sub-sea cables | Global | S$ 122 m (US$ 90.6 m) (growbeansprout.com) |

| Divest | Philippine Coastal (exit 50 % joint stake) | Liquid-fuel storage | Philippines | S$ 598 m EV on sale (links.sgx.com) |

As to patterns that emerge from the acquisition strategy over the past 5 years?

This is what ChatGPT had to say:

- Pivot to “future-proof” infrastructure.

Post-2021, >60 % of fresh capital went into renewables (wind, solar), energy-transition pipelines and water assets, shrinking legacy fossil-fuel exposure. - Contracted cash-flows first.

Every buy carries 20-25 year feed-in tariffs, water-purchase or availability-based payments, or CPI-linked transport contracts, locking-in visible free cash to back distributions. - Global diversification via club deals.

Stakes span 8 countries and are often syndicated with Keppel Capital funds or third-party partners, letting KIT write smaller cheques (S$80-450 m) while accessing multi-billion-dollar assets. - Active capital recycling.

The S$598 m Philippine Coastal exit after EBITDA growth funded the 2025 digital-infrastructure entry (Global Marine) without overstretching the balance sheet. - Sponsor pipeline advantage.

Many assets (Marina East, Global Marine, Ventura partial sell-down) are proprietary Keppel ecosystem deals, reinforcing KIT’s role as the listed, perpetual-capital arm for Keppel’s sustainable-infrastructure build-out.

In one sentence: KIT is systematically rotating from domestic utilities into a globally diversified, long-tenor, inflation-linked portfolio of energy-transition, water and digital assets—then recycling mature assets to fund the next wave of growth.

My thoughts on the acquisition / divestment strategy?

And you know what.

Maybe the ChatGPT answer is not perfect.

But it actually gets you 80% to the answer that you need.

And then you do the last 20% of the thinking yourself.

I agree with the points raised by ChatGPT on:

- Pivot to “future-proof” infrastructure

- Contracted cash-flows first.

- Global diversification via club deals.

- Active capital recycling.

- Sponsor pipeline advantage.

That’s strategy, and I agree this is broadly what Keppel Infrastructure Trust is trying to do.

Where it gets more nuanced, is the execution.

Execution is where you translate a vision into reality.

And it doesn’t matter how beautiful your vision is – if you cannot make it reality.

And there I do have my concerns.

I still find that a lot of the assets being acquired, while good as standalone assets, I’m just not super convinced where Keppel Infrastructure Trust’s value add comes in.

There’s no real synergy in the portfolio, it’s just a disparate portfolio of infrastructure assets scattered all over the world.

Follow Financial Horse to avoid missing any post!

Is this a bad thing?

Sure, you may argue that this isn’t a bad thing.

And that you just buy into Keppel Infrastructure Trust as basically a passive long term investor of infrastructure assets.

But then the active trading in and out of assets by KIT also suggests that they are not purely passive, and they are active in some ways.

Long story short, I get what they are trying to do, I just have my concerns on execution.

And for what it’s worth – share price (leaving aside the dividend) suggests that the market is somewhat skeptical.

Financial Results of Keppel Infrastructure Trust

Here are the latest financial results for Keppel Infrastructure Trust.

I always get questions on how to interpret the financial results.

The key to note is that this is a business trust not a REIT, so you need to view it more like a company (with lumpy earnings) rather than a REIT with smooth cash flow.

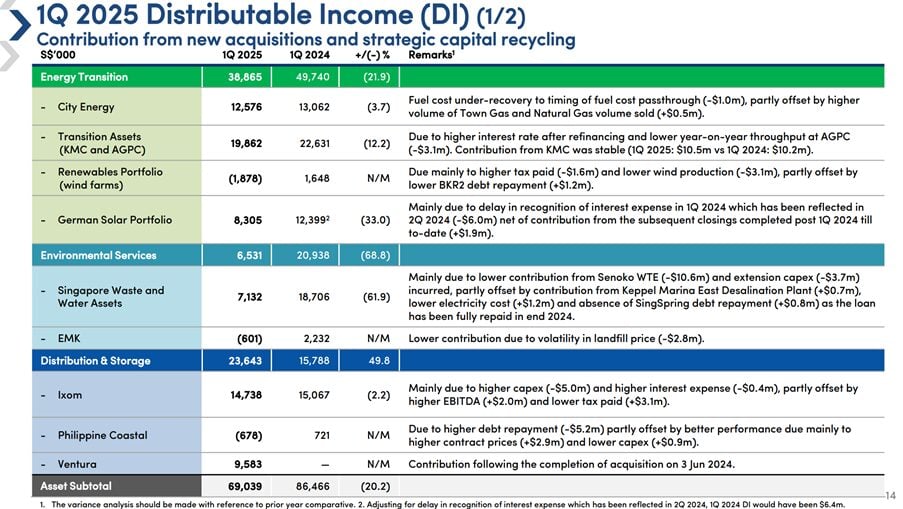

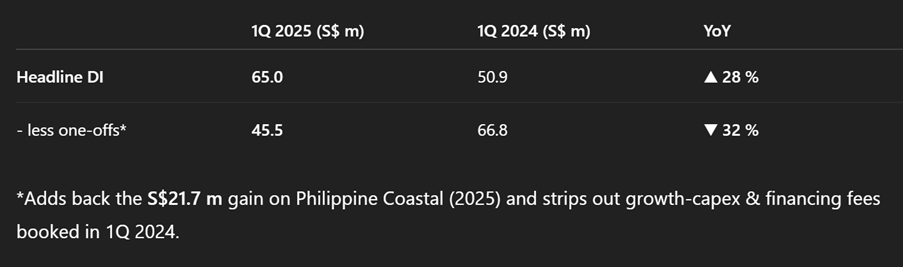

My personal takeaway, is that the headline numbers are flattered by a disposal gain, while underlying cash flow softer.

Distributable income surged +27.7 % YoY to S$65.0 m after booking a S$21.7 m gain on the March sale of Philippine Coastal.

Stripping that one-off, core distributable income fell 31.9 % to S$45.5 m:

This was mainly on lower contributions from Senoko WTE, weaker wind output and higher interest expense on renewables, partly offset by first-time earnings from Ventura and later solar closings:

| Segment | YoY Δ (S$ m) | Key drivers |

| Energy Transition | -10.9 | Higher interest at AGPC/KMC (-S$3.1 m) and low wind output (-S$3.1 m). |

| Environmental Services | -14.4 | Senoko WTE (-S$10.6 m) plus extension capex (-S$3.7 m). |

| Distribution & Storage | +7.9 | Ventura added S$9.6 m, offsetting Ixom softness and higher Philippine Coastal debt service. |

Ventura’s first quarter already contributes 15 % of DI.

Yet until wind, WTE and solar output normalise—and Keppel Marina East desal plant ramps up, core DI will stay below last year’s run-rate.

Bottom line – KIT’s 1Q headline cash looks healthy, but strip out the sale gain and core earnings are down one-third, mainly on energy-related assets.

New acquisitions like Ventura are cushioning the blow; but more operating recovery (or further acquisitions) is needed for DI to grow.

Balance sheet is okay, but not amazing

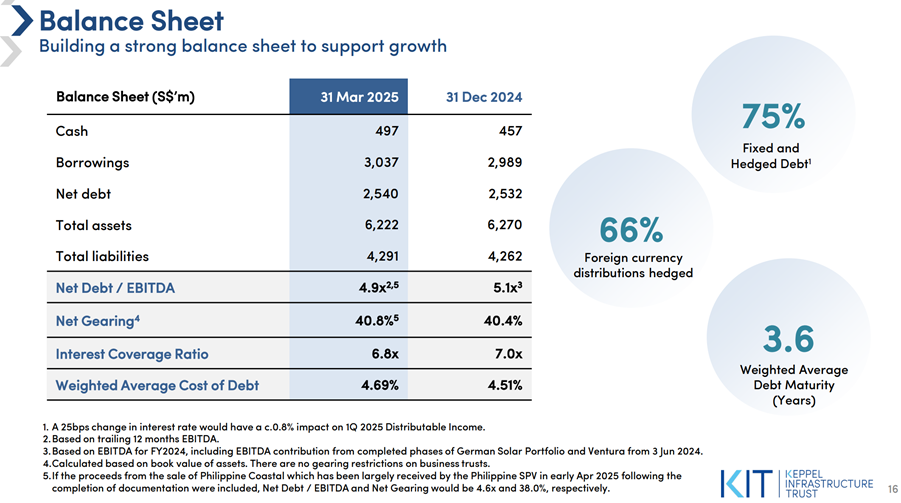

Here’s KIT’s balance-sheet quality at 31 Mar 2025.

ChatGPT’s view:

- Balance-sheet strength is solid and trending better: leverage metrics are edging down, and pro-forma ratios improve further once Philippine Coastal proceeds are fully booked.

- Liquidity and rate safety nets are robust: three-quarters of debt is on fixed or swapped rates, and interest cover of almost 7 × leaves ample cushion even if base rates stay higher for longer.

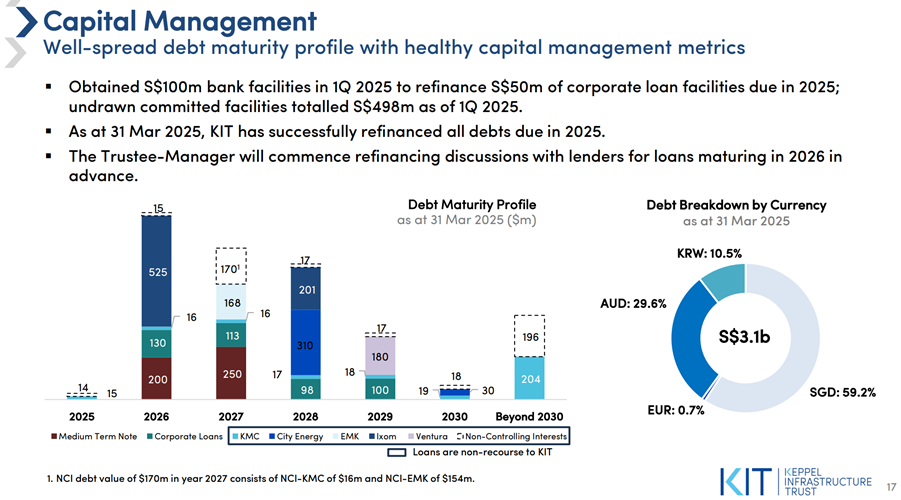

- Key watch-points:

- Refinancing window – 3.6 years is reasonable but means ~28 % of debt matures every year; management will need to stagger upcoming maturities carefully.

- Cost of debt drift – weighted cost has risen 18 bp since Dec-24; further climbs could pressure distributions if not offset by earnings growth.

Bottom line: For a yield-focused infrastructure trust, KIT’s balance sheet looks conservatively geared, well-hedged and able to fund incremental growth without immediate equity dilution. Continued deleveraging after asset sales should strengthen credit metrics further.

For what it’s worth, I think ChatGPT goes a bit overboard on this one.

Yes the balance sheet is okayish, but I don’t think it’s amazing or “conservatively geared”.

But hey – maybe that’s me being a conservative horse.

Primarily SGD debt – for a primarily overseas portfolio

Note also that Keppel Infrastructure Trust is primarily funded with SGD debt (59%) for a portfolio that is only 24% Singapore.

In the event that the SGD strengthens (which is pretty possible in the years ahead), this could cause issues.

Will I buy more Keppel Infrastructure Trust at 10% dividend yield?

So… long story short.

Will I buy more Keppel Infrastructure Trust?

The long term charts are trending down, and below all key moving averages.

That’s not good, and suggests a falling knife (for now).

I would really want to see if the 0.39 support holds.

But assuming it holds?

You know what.

Actually looking at everything above.

I might just go out on a limb and say that at 10% dividend yield, maybe, just maybe, there is a sufficient margin of safety for me to add to my position in Keppel Infrastructure Trust.

I have my concerns about Keppel Infrastructure Trust as shared above, but at 10% dividend yield, maybe I could be convinced that risk-reward is attractive enough.

But this is a really big maybe.

I haven’t made up my mind on this just yet, and as always I reserve my right to change my mind any time.

As always, I’ll share updated views on FH Premium, with updates as and when I decide to buy (or not buy) Keppel Infrastructure Trust.

You can also see my full personal portfolio on FH Premium.

This post is written on 12 June 2025 and will not be updated going forward. My latest views on markets, my Stock watchlist and full Personal Portfolio, are shared on FH Premium.

Few observations or comments on KIT to ponder,

1) Has it ever crossed your mind that despite 10 acquisitions (per your tabulations), which KIT claimed every acquisition is “yield accretive” since 2021, but the yield accretion does not seems to translate into increase in DI or EBITDA over the years. Q: Where does the yield accretion goes to?

2) If the yield accretive acquisitions does not serve to increase the DI or EBITDA overtime, then is the distribution yield of abut 10% sustainable in the long term?

3) Most acquisitions are funded by debt as the equity yield is abt 10%, which is prohibitive to fund thru EFR, how much more headroom can KIT go acquisition hunting via debt alone? Will the growth or acquisitions come to a standstill once it hit the debt limit?

Some quick thoughts from me:

1) DPU has been roughly flattish the past 4 years. I think that’s decent for a BT. Yield accretion assumes no change in earnings for the rest of the assets, which is not a realistic assumption for a BT.

2) That’s the million dollar question that I tried to address in this article. Personal view is that probably not. But the question is what % of that 10% is sustainable. Because even if it drops to 8%, if share price stays flat, that’s still a decent return.

3) Good question. As you can see they have moved to divest assets, so it doesn’t look like a one way street. If share price recovers they will prob do EFR, which does imply an upside cap to how high share price can go.

Hi sorry for being naive, but you mentioned $3.90 dividend per share and $0.39 price per share so if I use these figure the dividend yield would be 1000% and not 10% ?

I think he means 3.9 cents dividend and 39cent share price.

I sold bulk of the shares at 55cts when I realized that KIT has been paying more than it earned. I wonder if anyone even know how many new shares KIT had issued using the excuse of buying more and more companies! The CEOs are all short terms where their main objective is to deliver big fat management fees for Keppel Ltd (by buying more companies), if this primary KPI is not met, the CEO will be removed.

Based on the current 39cts, the so called 10-15% dividends actually come from your own pocket. I have ZERO CONFIDENT that KIT will be able to earn more than its payout based on the direction that it is heading, where Keppel Ltd is its priority rather than its other shareholders.

Fair enough! I have similar concerns, the questions is whether at 39 cents there is a sufficient margin of safety. You may well be right.