So I received this question recently:

Hi FH. My outstanding housing loan of about 650K is due for repricing. I’ve been offered 2.7% fixed rate for 2 years, and I need to get back to the bank in about a week’s time if I want to accept the offer.

I’ve in excess of 650K in my CPF OA. I’ve above 55 years old, and next year fund in my SA account will be transferred to my OA account.

My initial reaction is that I should just use my OA fund to completely redeem the housing loan and be done with that. However on further considerations I wonder if that would be the best course of action.

CPF OA gives 2.5% interest. So the additional 0.2% interest payment to the bank is a difference of about 1.3K a year. But if I do not redeem the loan, then 650K may possibly be used to generate returns higher than 2.7%?

I would appreciate if you can give me your general thoughts on this, understanding that you do not have the full financial picture.

Obviously I would not want to take excessive risk on the 650K as the loan would still eventually need to be repaid.

Would you redeem the loan in full? If not would you invest the 650K in CPF OA approved instruments, and if so which would you consider? Or would you take the 650K out from the CPF OA account to invest as there may be more options, such as bond funds, but that would mean I will not be able to return the money back into CPF for the ‘guaranteed’ 2.5% return in future?

What should be the ‘logical’ response in your opinion?

I’m fairly familiar with investing, have quite a fair bit already in the equity market, but also adding bonds the past year. I’m ok with equity risk, but not sure that too much risk should be taken for the loan quantum. Appreciate your opinion : )

What would I do – invest CPF OA or pay off the mortgage?

For obvious reasons I do not know the full financial situation of the reader, so none of this should be taken as financial advice.

But hey if this were me, and I were in a similar situation?

I would withdraw the full CPF-OA into cash – and use it to invest.

The way I see it this is basically a 2.7% loan.

Assuming I max out the loan tenure to 65, which is 10 years.

I just need to generate more than a 2.7% return over the next 10 years, and I’m in the money.

And if I am right and this decade is one of structurally higher inflation and interest rates.

I think to generate a nominal return in excess of 2.7% should be achievable.

In fact looking at latest home loan rates they can go as low as 2.40% fixed for 3 years, which would make this an even better deal.

There is some nuance from a cash flow perspective – due to monthly repayments

Note that there is some nuance to this.

The nuance is that with a mortgage there are monthly repayments, this is not a bullet repayment after 10 years.

So while you can invest the money, you still need to have enough cash on hand to meet the monthly repayments.

The second point is that whatever rate you lock in is only locked in for 2 – 3 years tops.

After that you need to refinance.

And if interest rates are very high then, and your investments are performing poorly, and you don’t have cash on hand, you may be refinancing into a tricky situation.

So I would say you need to be careful with how much cash you hold.

You want to hold enough cash to be able to have no problems with (a) the monthly repayments, and (b) the refinancing in 2 – 3 years time, even if your investments suffer.

In what situations would it make sense to pay off the mortgage?

I would say there are 2 situations where just paying off the mortgage today makes sense:

- If you are not familiar with investing

- If you want peace of mind, and don’t want to take too much risk

Nobody can answer this for you.

There is no doubt the safe approach here is to pay off the mortgage and be done with it.

But of course the upside in that scenario is low.

Which is why I always ask investors to do some soul searching.

Whether you want to get rich(er), or you want to avoid being poor.

Let’s put it this way.

If your financial situation is frozen at its current status, would you be happy?

Or are you prepared to take the risk of it getting worse, for the chance for it to get better?

Only you can answer this for yourself.

What does the rest of the net worth allocation look like?

The other question worth discussing is what is the size of the $650k debt relative to the rest of your net worth?

The lower the debt as a % of net worth, the less “risky” it is

To give a simple example.

If you had $10 million net worth.

The $650k is a drop in the pond – in the grander scheme of things.

Worst case even if you lose money on your investments, paying off the debt is not an issue.

But if your net worth is $1 million and the $650k mortgage is a huge chunk of your net worth, it becomes a lot more tricky as your ability to take risk is a lot lower.

Follow Financial Horse to avoid missing any post!

Keep the money in CPF OA or take it out to invest?

There is also a sub question on whether to keep the cash in CPF OA, or take it out to invest.

The benefit of keeping in CPF OA is that you have the flexibility to put it back into CPF OA any time and get 2.5% interest risk free.

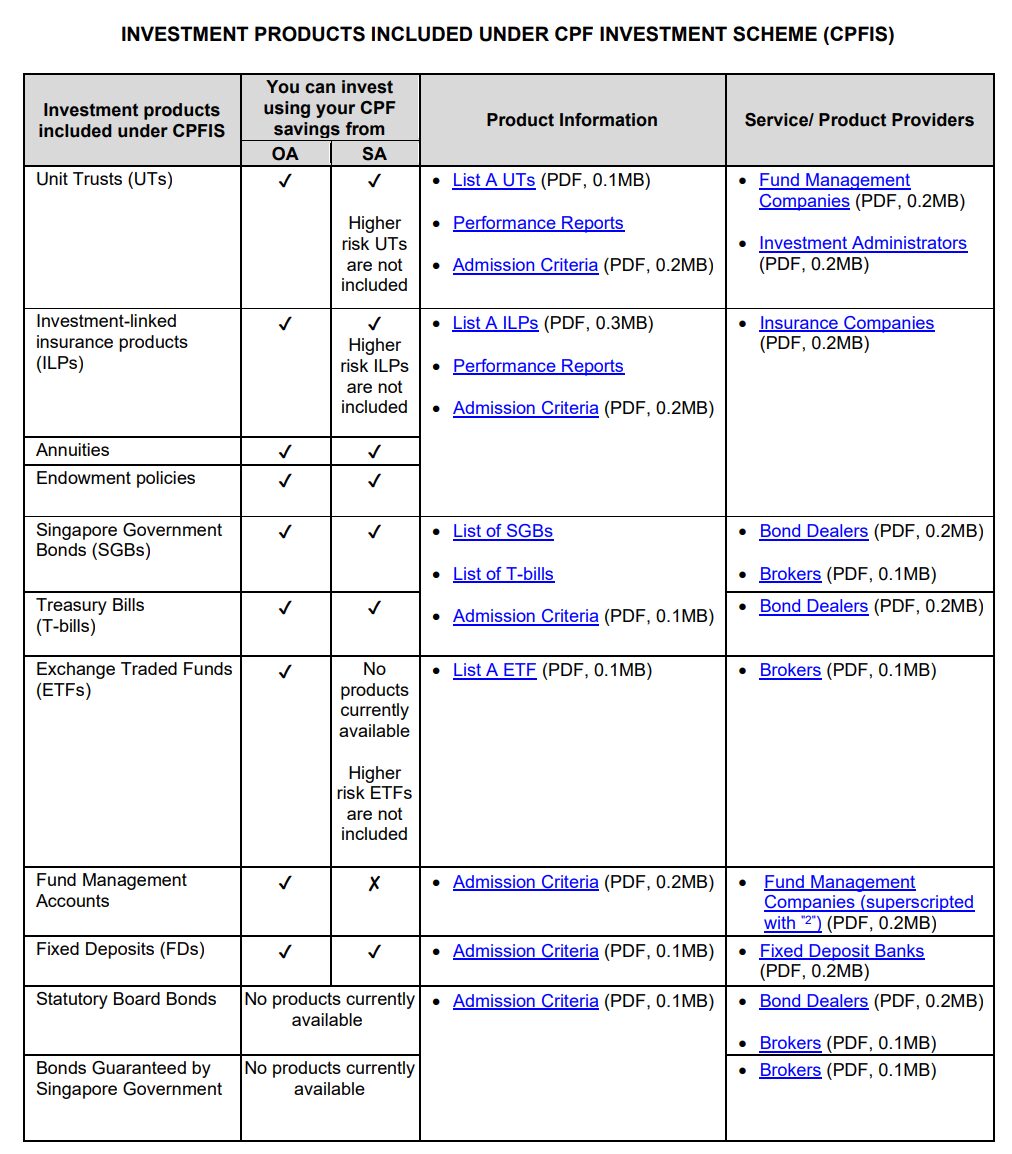

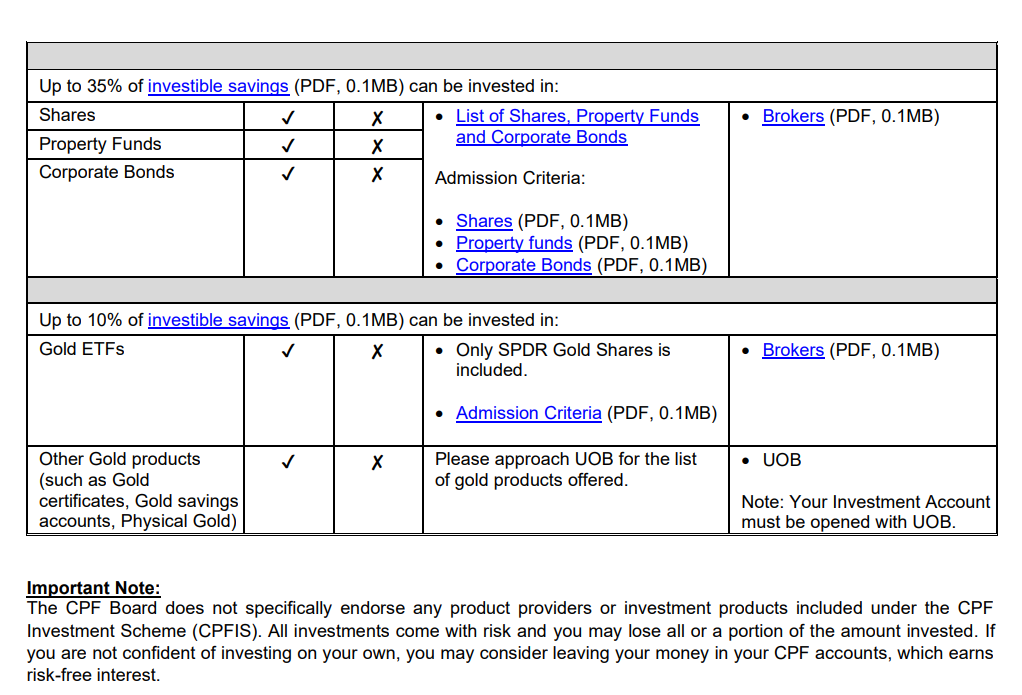

The drawback is that you can only invest in CPF OA approved investments:

However the rest can be invested with funds, and these days that includes passive ETFs like the S&P500:

My take? Keep in CPF-OA investments or withdraw in cash?

How valuable is this (the flexibility to put it back into CPF OA any time and get 2.5% interest risk free)?

I would say in 2010s when interest rates were zero bound, this was worth its weight in gold.

But I think post COVID, we are living in a very different paradigm.

I see this as a decade of structurally higher inflation and interest rates.

Which means the option of 2.5% risk free yield on CPF OA, in my view, is a lot less important this decade.

But hey that’s just how I see it.

If you’re a passive investor and are fine with the CPF OA investment options.

And you want the flexibility to keep the cash in CPF OA for a zero risk investment at 2.5%.

That’s perfectly fine too.

I would love to hear what you guys think though.

In a similar situation – would you invest the money, or pay off the mortgage?

This post is written on 25 Oct 2024 and will not be updated going forward. My latest views on markets, my Stock watchlist and full Personal Portfolio, are shared on FH Premium.

I would personally not pay back the loan. I would also not take my CPF money out as cash. At 55, you will never know what will happen in the next 30 years. Also, SA has to be taken out first before the OA. Even for OA investments, can easily outpace 2.7%, so better to have more money (via loans) at hand.

Thank you, appreciate the comments!

You have $650k, pay full settlement of hdb if the amount only $300k, the balance $200k tIransfer to RA to meet the BRS or better still Enhance, if $200 can meet Enhance thats good. The $100k withdraw from OA. Check the accrued interest in HDB. If everything ok. Good. After that then wai everything fall in place

Rather than just looking at this as an all or nothing decision, why not consider a doing both in a considered proportion. The more risk averse you are the more you allocate to paying off the loan, with the rest used for investment. I personally would do around 50/50 as there’s no guarantee what your investment returnsnare going to be.

That’s a good comment. It doesn’t need to be all or nothing, can pay off a proportion of the loan based on risk appetite.

Case 1 – if have $3m (assume) in various investments, >$650K in CPF, $650k loan, at 55, pay off the loan, have a peace of mind no more mortgage. Make your $3m fund work hard.

Case 2 – if have $500k fund, >$650K in CPF, $650k loan, at 55. Then pay off half of loan to reduce monthly loan commitment. Make the remaining $500k + $325k (CPF) work hard.

As for how to make the funds work hard, Mr FH is the guru not me 🙂

Thank you, appreciate the comments! I like this approach. Definitely need to look at the portfolio holistically.

Leveage is power tool to enable one to deploy one’s own fund to generate higher return. Moreover, at 55, the opportunity using such tool will be limited by age factor. Whether one should use OA money to pay the loan or not, depends on one’s comfort level and knowledge to use OA fund to generate higher return. Unit Trust or SG stock might be good to generate higher return. But one need to first invest in oneself to gain the knowledge of investment. There is no free lunch. I am in the same situation as you, what i did is to increase my monthly installment payment to shorten the loan tenure from 9 years to 6 years. I am using by current CPA Contribution to pay part of the installment and remaining with cash. By aim is to finish the loan in time for my retirement. My OA fund will be deployed in safer investment. T bill is era is ending, then next need to explore SG stock and UT bit by bit as one never knows when the market would crash. I am believe have enough knowledge to manage the risk to minimize but not 100% prevent of it.

Yes I agree very much with this. This needs to be a personal decision ultimately, based on the individual’s risk appetite and comfort/familiarity with investing.