You know I hate to say it.

But because of the sharp drop in interest rates.

Suddenly this month’s Singapore Savings Bonds are looking pretty attractive.

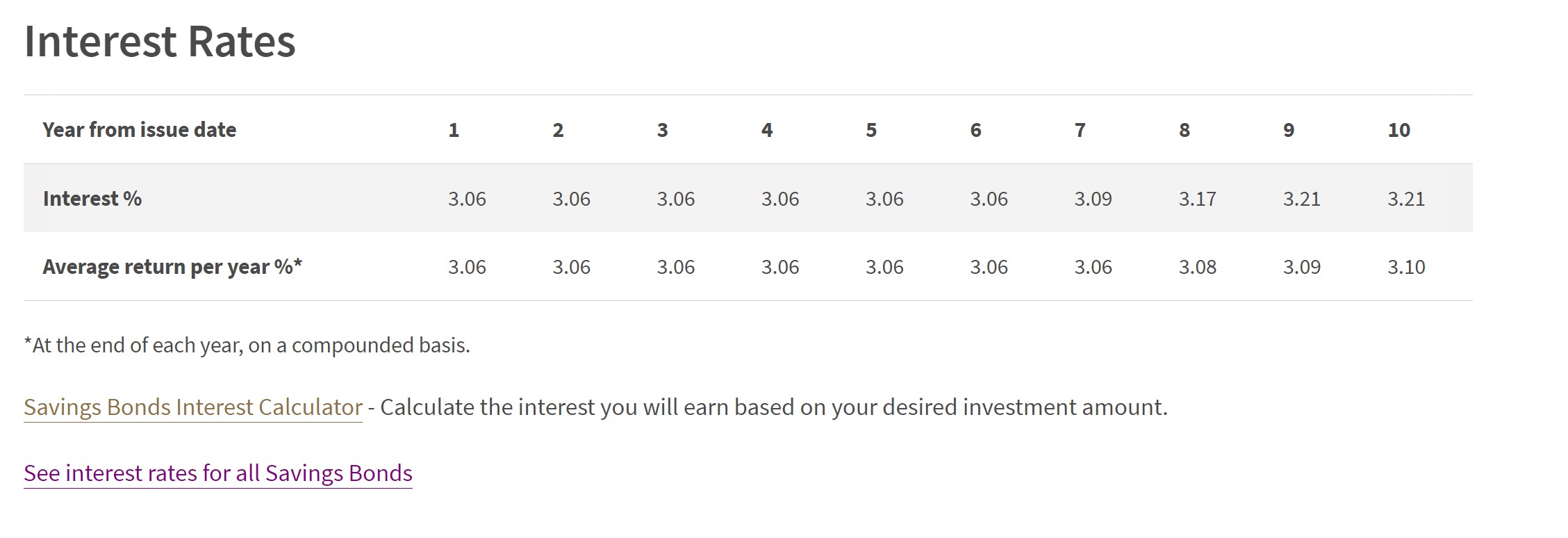

You’re getting a first year yield of 3.06%, that is locked in for the first 7 years.

That steps up to 3.10% over 10 years.

Risk free, and can be redeemed any time, and can also be held for 10 years.

With the latest 6-month T-Bill yielding only 3.34%, that’s just a 0.3% lower in yield, for all the benefits above.

And if last month’s Singapore Savings Bonds are any indication, it looks like allocation limits might be very high.

So… are this month’s Singapore Savings Bonds a good buy?

And will I be buying this month’s SSBs – to lock in yields with rapidly dropping T-Bill interest rates?

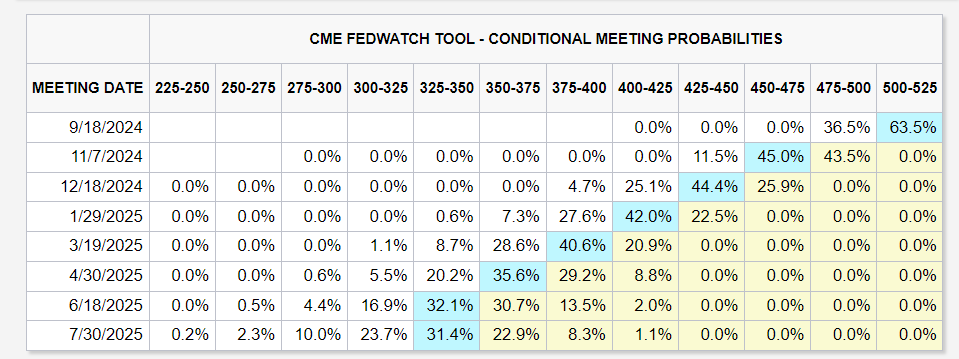

Interest rates are falling rapidly – due to expectations of interest rate cuts

Slowing US inflation and a weakening US jobs market has led to expectations over Fed rate cuts going forward.

A lot of rate cuts are being priced in at this stage – almost 2.0% in interest rate cuts over the next 12 months:

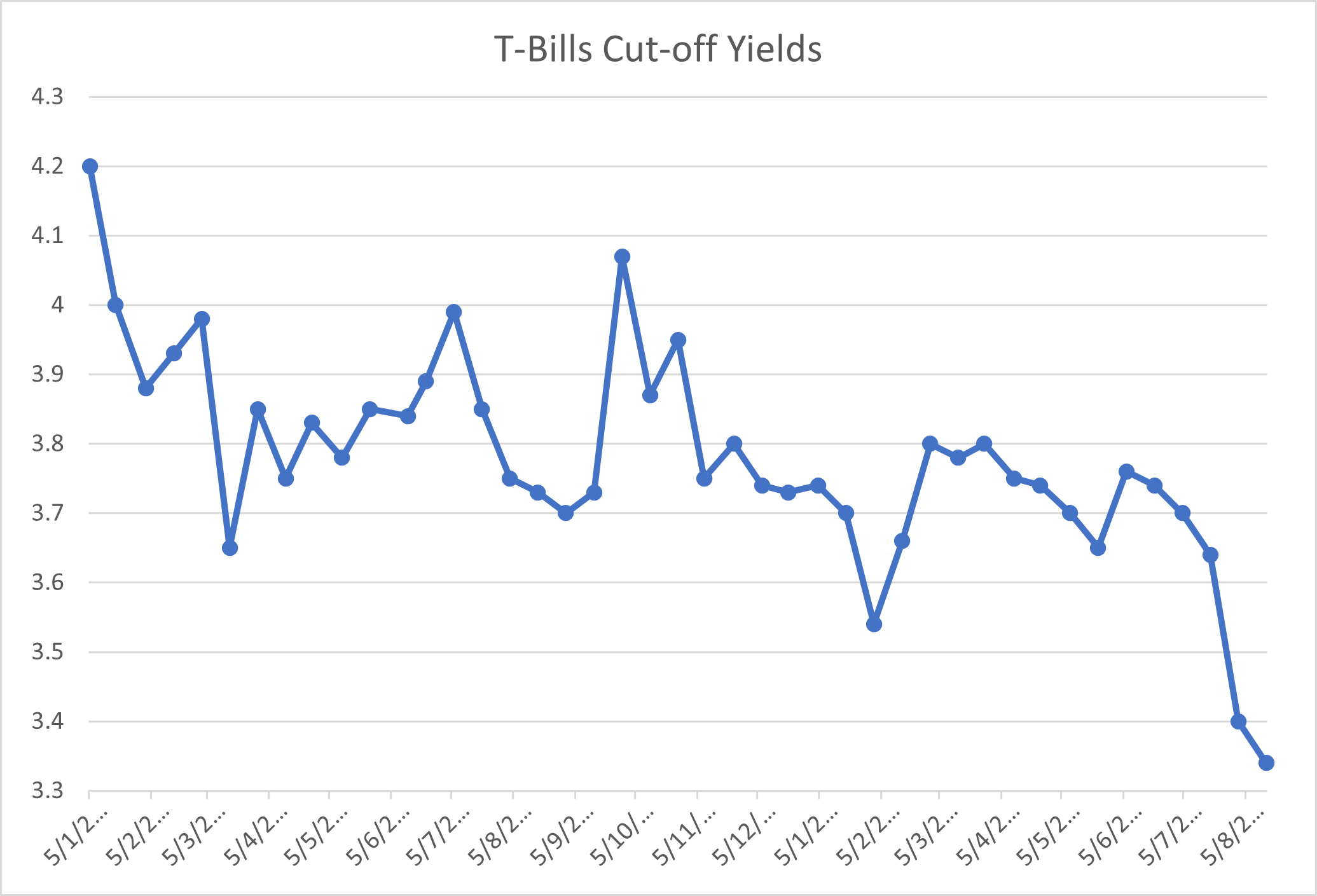

Latest 6-month T-Bills yields drop to 3.34%

Because of that the latest 6-month T-Bills yields have continued their sharp decline.

At 3.34% yield, this is the lowest it has been in the past 18 months.

Singapore 10 year Government Bond yield drops to 2.8%

Meanwhile the 10 year Singapore Government Bond yield drops to 2.8%.

Given that it was trading as high as 3.5% in April, this is a stunning drop in interest rates.

Next month’s Singapore Savings Bonds are projected to have much lower yields – 2.6% first year?

Singapore Savings Bonds yields are tied to the average yields on the 10 year Singapore government bond in the previous month.

So the sharp drop in Singapore 10 year government bond yields means that next month’s SSBs are likely to have much lower yields.

Here’s the projection, we’re looking at 2.6-2.7% first year yield for next month’s SSBs – a massive drop.

So if you’ve ever wanted to buy SSBs or missed your chance previously, this might be your last chance this cycle.

SSB yield at 3.06% is only 0.3% lower than the latest T-Bills – Locked in for 10 years and redeemable any time

This month’s Singapore Savings Bonds interest rates are below.

3.06% for the first 7 years.

Stepping up to 3.10% for 10 years.

To put things in perspective.

3.06% is only 0.28% lower than the latest 6-month T-Bills yield.

And because Singapore Savings Bonds yields are locked in for up to 10 years, they get more attractive the lower that interest rates are in 6 months.

All while being a cash instrument that is risk free, can be redeemed any time, and can be held for 10 years.

So yeah, I actually think this month’s SSBs are a pretty decent buy – because of the sharp drop in interest rates for competing instruments.

Last month’s Singapore Savings Bonds were more attractive?

For the record, yes I know that last month’s Singapore Savings Bonds were more attractive at 3.19% for the first 7 years, and actually saw full allotments.

But hey we can’t go back in time to buy last month’s SSBs, so no point crying over split milk.

Allotment limits for Singapore Savings Bonds likely to be very high

If you think about it.

Last month’s Singapore Savings Bonds had even better interest rates, and yet saw full $200,000 allotment.

That suggests you’ll see very high allotment limits (possibly full $200,000) for this month.

Do note that the auction amount this month is 10% lower at $900 million.

And interest rates have dropped sharply across the board – making SSBs comparatively much more attractive.

But all that taken into account, I would say you’re probably still going to see decently high allotments this month.

Alternative to Singapore Savings Bonds? T-Bills or Medium term bonds?

What are the alternatives to Singapore Savings Bonds today?

I would say there’s broadly 2 alternatives:

- Cash equivalents – T-Bills, Fixed Deposit, Money Market Funds

- Medium duration bonds

You can now follow Financial Horse on Google Chrome to avoid missing any posts!

Just:

- Click the 3 dots on the top right of Google Chrome

- Click Follow!

- And Financial Horse posts will now appear on your home page, under Following:

You can also follow Financial Horse on:

I also send out a newsletter at 10am every Sunday – rounding up the posts from Financial Horse for the week. Sign up below!

Cash equivalents – T-Bills, Fixed Deposit, Money Market Funds

This is basically your cash equivalents – stuff like T-Bills, Fixed Deposit, Money Market Funds.

Typically risk free or low risk, paying around 3.3 – 3.5% interest rates these days.

But the big factor is that you cannot lock in interest rates.

If interest rates drop going forward, you’re likely to be refinancing into lower interest rates.

Medium duration bonds

The alternative is to increase the duration.

So instead of buying 6 month T-Bills, you buy say a 4 year bond.

This is long enough to “lock-in” yields for a longer period, and yet not long enough that you will suffer big capital losses if interest rates go up.

For most retail investors the best way to achieve diversified exposure to bonds is to use a bond fund.

There are many options these days from the various Robo Investors.

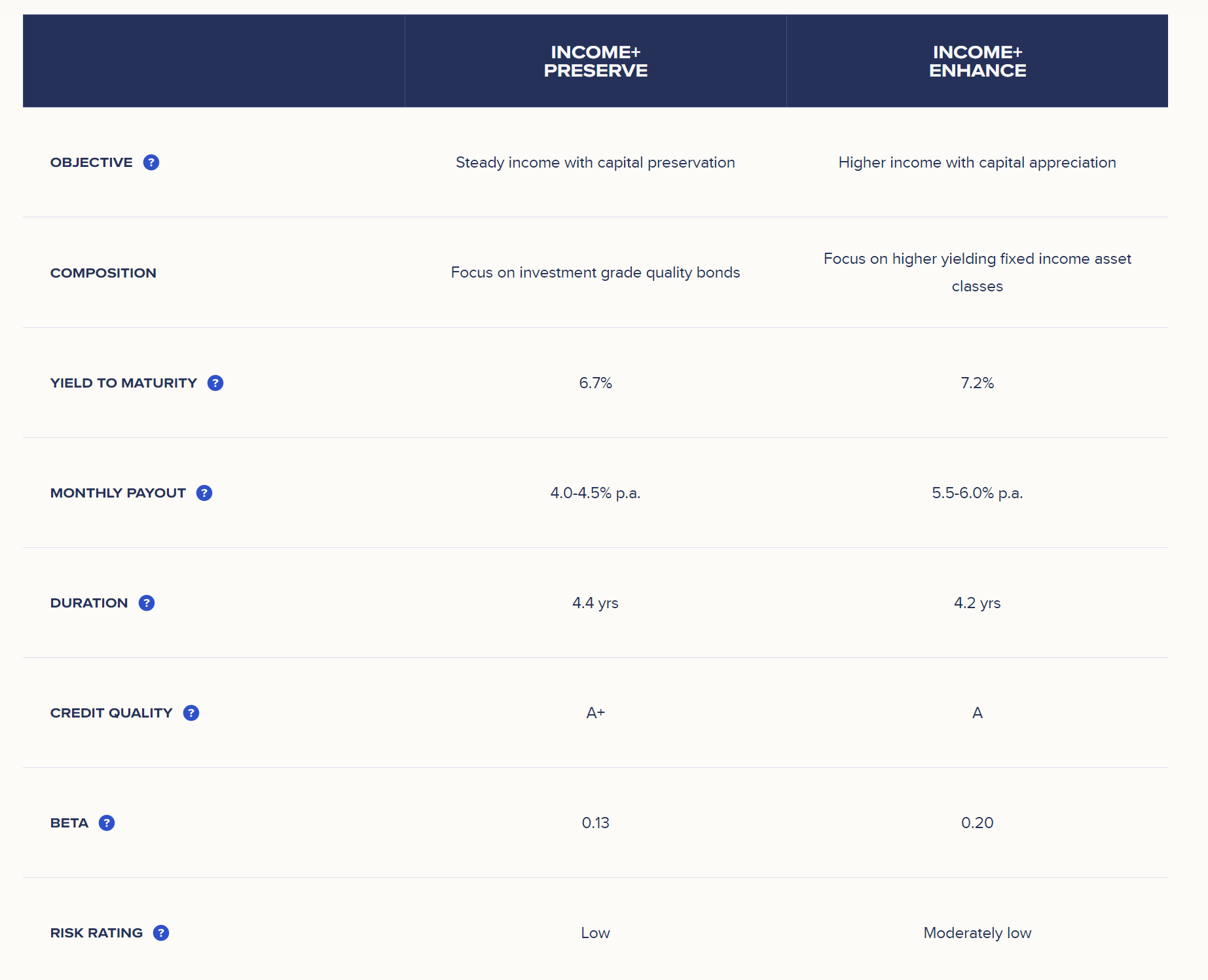

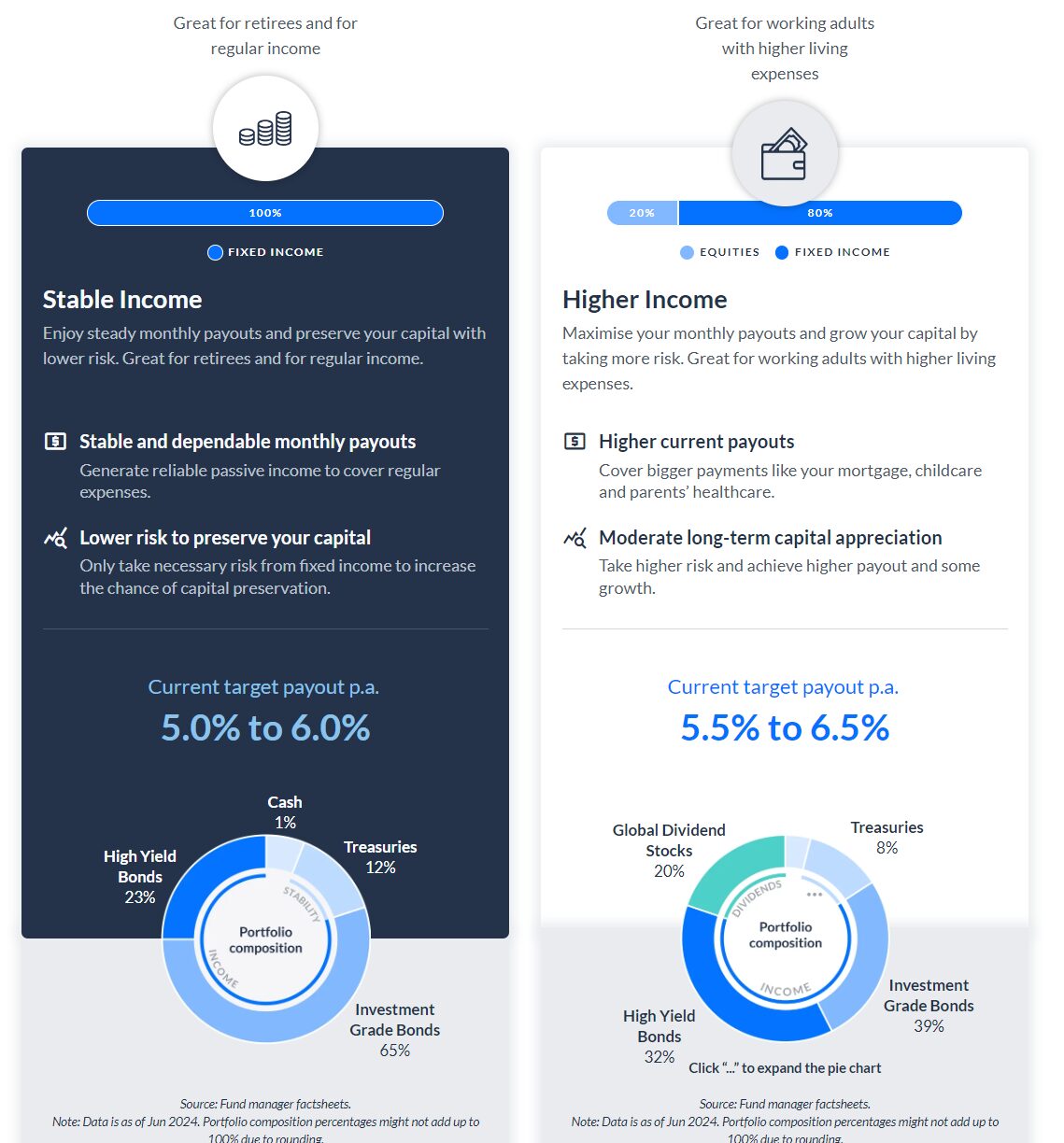

Here’s Syfe Income portfolios for example, with a target yield for 4-4.5% or 5.5-6% (depending on risk levels), with a duration of about 4 years:

Endowus has something similar with their Income portfolios.

What are the risks of investing in a bond fund?

A lot of you have asked what are the risks of investing in a bond fund.

If you pick a SGD hedged bond fund (and you should), then the FX risk is hedged away.

And because the bond funds are broadly diversified, this means the single issuer risk is also diversified away.

The key risks you take on (that cannot be easily diversified/hedged) are:

- Macro risk – bond defaults due to recession

- Interest rate risk – capital losses from rising interest rates

That’s just a risk you have to be comfortable with for these bond funds.

As of today, I would say for a low risk bond portfolio you’re probably looking at about 4%+ yield.

This would have been higher just a month or two back (perhaps as high as 5%) – but you can see how interest rate have plunged sharply since late July:

Medium duration bond funds are a decent alternative to cash if you want to lock in yields.

But of course do not that they are not risk free (see risks above).

Capital losses are possible in an economic slowdown, or if interest rates rise sharply.

Will I buy this month’s Singapore Savings Bonds?

I actually bought a decent amount of Singapore Savings bonds the past few months when they had 3.2%+ first year interest rates.

The question now is whether I need more, due to falling interest rates.

Source: https://www.ilovessb.com/historical-rates/2023-2024

I had a decent chunk of T-Bills that matured recently, that I’ve been parking in a mixture of money market funds and MariInvest for now.

I applied for the T-Bills auction with a competitive bid this week, but it didn’t get filled because yields at 3.34% came in below my competitive bid.

Now that I think about it, I’ll probably take some funds out of money market funds and put in Singapore Savings Bonds.

It won’t be a lot as I want the liquidity – I’ve been buying some REITs and Stocks of late.

But given how much cash I have sitting in money market funds at the moment, it might make sense to move a small amount of cash over into SSBs and lock in the 3.06% yields.

So that’s probably what I’ll do, but I would love to hear what you think!

Deadline to apply for this month’s Singapore Savings Bonds

For those who are keen to apply – the deadline is Tuesdy 27 August (9pm).

Same time for redemption applications.

There have been huge moves in stock prices the past few weeks, with lots of opportunity in markets.

I will be updating my stock and REIT watchlist this weekend on the names that I am keen to buy, do sign up for FH Premium if you are keen.

Never miss another post from Financial Horse!

Follow Financial Horse on:

I also send out a newsletter at 10am every Sunday – rounding up the posts from Financial Horse for the week. Sign up below!

IMHO, with REITS/Stocks possibly double ROI, I would more likely not SSB but nibble into them instead

Fair point. Just to add that I see SSB as a replacement for cash, stuff like T-Bills / Money Market Funds. Am not saying that one should move money from REITs/Stocks into SSBs.

That is more of market timing and a fundamentally different question.

Hi

Other Singdollar alternatives with longer duration than T-bill :

1) Nikko AM SGD Investment Grade Corporate Bond ETF

– Price will rise if Singapore risk-free bond yield drops.

– Can use SRS and CPF-OA to buy

2) Manulife SavvyEndownment 16 (via DBS)

– 3 years savings plan with guranteed 3.4% pa

Thanks, appreciate very much the input.