Well, in case you missed it – the Iran war is “over”.

For stock markets, the Iran war being “over” has been all but priced in since Trump chickened out in early April.

But this week, with the signing of the MOU, oil markets finally got the memo.

And yet because oil price has been high for so long, markets have shifted from pricing in rate cuts at the start of the year, to now pricing in rate hikes.

With big implications for markets.

So… with all that is in play, how would I invest $1 million today?

It’s been ages since I’ve done a no holds barred macro piece tying into how to invest my own portfolio.

Exactly what I wanted to do today.

Iran war is “over”

Here are the high-level details of the MOU signed:

- Interim deal, not final settlement — this is a temporary US-Iran framework to reduce tensions, not a full peace or nuclear agreement.

- Immediate de-escalation — both sides agree to a ceasefire.

- Hormuz reopened for 60 days — Strait of Hormuz to reopen for 60 days on best efforts basis.

- 60-day negotiation window — both sides will negotiate the detailed nuclear and sanctions terms.

- Key issues still unresolved — enrichment limits, uranium stockpile, inspections, sanctions relief, oil waivers, frozen assets, and long-term regional security remain to be settled.

For all intents and purposes, it is an agreement to agree.

But what is material is that during this period – Iran agrees to reopen the Strait of Hormuz.

I ran the analysis on FH Premium a while back and my conclusion was that the line in the sand for oil markets is July.

If the Strait of Hormuz remains closed by July, physically the world starts to run out of oil and that’s when very ugly stuff starts to happen.

Well, it looks like Trump got the memo and chickened out right before economic catastrophe.

And yes this is an agreement to agree so there are many things that can still go wrong.

But this is a very positive step in the right direction.

In COVID terms this is like the vaccine news.

Yes a lot more work still has to follow, but you can see the light at the end of the tunnel.

Stock markets have sniffed this out in early April when Trump chickened out – and has been pricing in the Iran war recovery ever since.

The difference this week – is that oil finally agreed the war is over:

How does the macro climate today differ from the start of the year?

That said.

A 4-month closure of the Strait of Hormuz, coupled with 1 month war which damaged a good chunk of Middle Eastern oil & gas infrastructure.

That has taken its toll.

And the way it has manifested itself – is via inflation (due to higher oil prices).

And that inflation has significant implications on the Fed’s ability to cut interest rates.

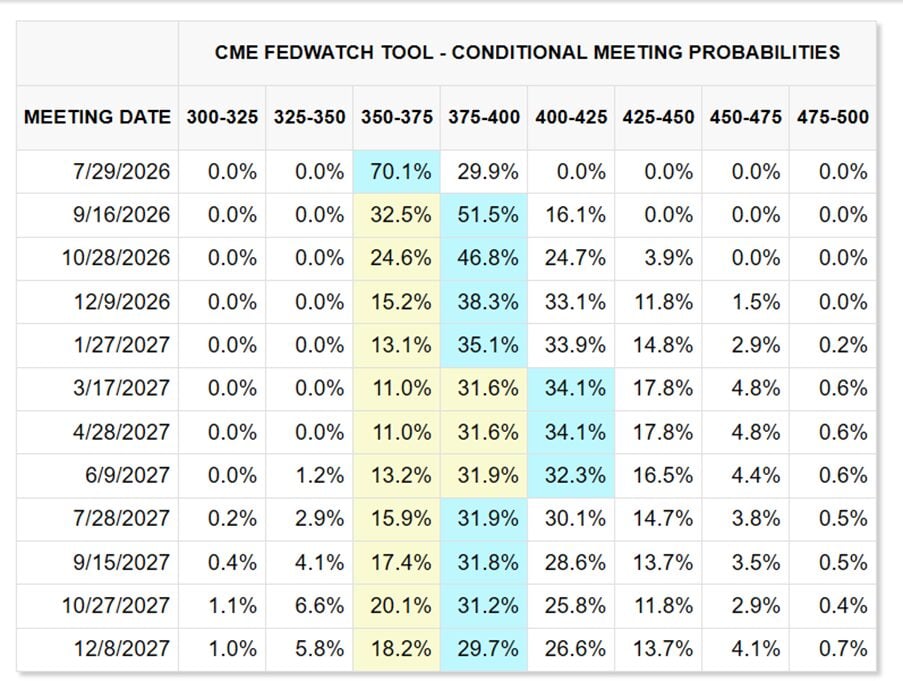

If you recall at the start of the year the market was pricing in 2026 rate cuts.

As of today – the market is pricing in 2 rate hikes over the next 12 months.

That’s a complete sea change in market expectations and should not be underestimated.

A lot of you have asked me why gold and Bitcoin are performing so poorly.

In my view – it’s down to interest rate hike expectations.

Gold and Bitcoin are a “store of value”.

They do well when cash is losing its purchasing power, and there is money printing.

But crucially – they do not pay interest.

So when interest rates go up, the opportunity cost of holding gold and Bitcoin goes up, hence the rotation out from both:

Despite the higher inflation and interest rate hike expectations.

That has not stopped AI stocks from defying gravity and going parabolic:

How would I invest $1 million today for the recovery?

Which brings us to the million dollar question (pun intended).

Given the macro climate today, how would I invest $1 million for the recovery?

Big picture asset allocation – split by buckets

Asset allocation wise, I always advocate for thinking in terms of risk buckets.

Split your portfolio by risk, starting with the safest stuff first, and build up from there.

If this were me, I might take $150,000 out from the $1 million and park that in a mix of low risk cash or bonds (things like T-Bills, Singapore Savings Bonds, maybe a bond fund).

That’s for safety and peace of mind, and to ensure I have cash set aside that I can use to pay bills without selling shares in case there is a market crash.

After that I might take $150,000 and invest in a mix of gold and Bitcoin, as a store of value / hedge.

Yes, I agree that gold and Bitcoin may underperform short term as the charts for both are trending down, and the higher interest rate climate is not good for both.

But as a mid to long term investor, I think they have a role to play in providing portfolio diversification, and a hedge against a more volatile geopolitical climate.

But given the short term underperformance, I can completely see why investors may want to reduce the allocation (or skip it entirely).

How would I invest the remaining $700,000?

So after setting aside $300,000, that leaves $700,000 that I can invest into risk assets.

Looking at my own portfolio today, I am overweight growth relative to value.

And I suppose in some ways that is by design.

Yes AI has gone parabolic and risks are elevated, but given that we remain in a bull market, it is also not straightforward to call the top.

I have made the mistakes in prior cycles in trimming growth positions too early, so that’s a mistake I need to counter-bias against.

But at the same time you look at the chart of AI stocks like Micron below, and you just have to realise there’s a risk that this could come crashing down any day.

So reasoning from first principles – I would want a >50% allocation to growth, but not be all-in as well from a risk management perspective.

I would probably go with the following allocation:

- 60% Growth

- 40% Value

Never miss a post! Follow Financial Horse by subscribing or following us on your favorite platform:

Subscribe to our mailing list for exclusive content straight to your inbox:

How would I invest the 60% in Growth Stocks?

For the growth bucket, the areas I would look at are:

- MAG7

- AI

- Tech generally

MAG7 is in a funny place today.

Stocks like Google and Apple are close to all-time highs.

And yet stocks like Meta and Microsoft are down 30% or more from highs.

Yes no doubt these stocks are going sideways, so it looks premature to pick up a big position.

But if you ask me whether there is any way for Meta and Microsoft to find a way to monetise AI given their massive distribution channels and access to all that programming talent?

I’ll willing to take a chance the answer is yes.

So I would allocate to MAG7, but some stock picking makes sense on which names to buy and how much of each to buy.

Then we have AI.

The chart for Broadcom gives you an idea of what happens when AI stocks underdeliver relative to the exuberant expectations priced in.

A massive 14% drop from Broadcom on earnings day – wiping out more than $300 billion in market cap.

That being said, you also cannot not be invested in AI today, because otherwise that you risk massive portfolio underperformance if this continues going up.

So you have to have some AI exposure, but you go in with your eyes open – diversify it with other positions, and risk manage well.

And then we have tech generally.

Stuff like Sea Limited – this is as ugly as it gets.

But that said looking at the charts, you could argue that this is forming a base, and you have the added benefit that because this sector is so badly sold-off, it now diversifies AI risk (that’s true glass half full thinking).

I think some allocation here makes sense, but of course the question is how much and what stocks, which is where the nuance and judgment comes in.

How would I invest the 40% in Value Stocks?

And then we have value stocks.

The key areas I would look at are:

- Banks stocks

- Singapore companies

- Value stocks generally

With value stocks, as a Singapore investor you just cannot get away from the bank stocks.

They pay a good dividend, they benefit from Singapore’s wealth management push, and now we have interest rate hikes which will benefit the core lending business.

I’ve talked about bank stocks to death in other articles, so I won’t belabour the point.

But even if you leave aside the bank stocks, there’s actually a lot of opportunity to be found in the other Singapore stocks.

Here’s SATS which has gone on an unbelievable run after the strong earnings performance (and the end of the Iran war).

Even SGX which I covered last week looks like it’s breaking out

Or if you want something outside of Singapore, Richemont (owns Cartier and VCA) is a position I picked up during the Iran war, which also has been doing very well.

Just to be clear, I’m not saying to go out and buy SATS or Richemont tomorrow, because both have already run up, and these are value stocks not momentum stocks so you can’t just chase.

But the point I wanted to make is that there is a lot of opportunity to be found under the surface, if you know where to look.

The market is expensive in aggregate, but individually there are a lot of great stock picks to be found.

What about China, or REITs?

Some of you may ask why this asset allocation above excludes China and REITs.

Now I myself have some small China exposure, but the exposure is very small.

The short answer I suppose is because the China economy is weak, and it looks likely to stay that way for a while as they work through their real estate deleveraging and transitioning the economy to new areas of growth.

And if you look at the chart of the Hang Seng, this is about as ugly as it gets so no way I am buying into a chart like that.

Holding some positions could make sense as a turnaround play, and especially if valuations get very cheap.

But when the charts are breaking down I think you have to size the positions small at least until there are signs of a durable turnaround.

REITs on the other hand – I actually think REITs are decently attractive today.

Ascendas REIT for example pays as >6% dividend yield, for a blue chip industrial REIT I think that’s pretty attractive.

REITs can definitely be considered for more income focussed investors, and could replace a portion of the bonds, or a portion of the value stocks.

But like I said, in a rising interest rate climate don’t expect too much capital gains from the REITs, but yield wise they still work.

Closing Thoughts – Start with First Principles

So there you have it.

The above sets out my high level thinking about asset allocation and how I would position.

Always start from the principles first, then break down into execution.

Once you have the framework, you can then decide what are the exact individual stocks to buy, and how much of each stock to buy.

My full personal portfolio, together with my position sizing of individual stocks is shared on FH Premium.

Love to hear what you think though! What would you change with the asset allocation above?

This article was written on 19 June 2026. It will not be updated going forward.

My latest macro views, as well as my full stock watch and personal portfolio, are shared on FH Premium.

Always curious about SG REITS as an expat in Singapore. In most other countries we wouldn’t really consider them but they’re hugely popular here, is this mostly just a hedge against currency fluctuations? We can also currently get around 3.5-4% in US and European money markets with almost no risk. Happy to be enlightened.

In my view it’s mainly about the yield spread. A SG MMF pays about 1.5% today, a decent blue chip REIT pays maybe 5 – 6%. That’s a decent spread vs the risk free. If a SG govt bond pays 3-4% like in US / Europe, I agree that REITs are not attractive.