There was a time when I was obsessed about credit cards. When I first started work, and I was making peanuts every month, signing up for new credit cards just for their S$200 welcome bonus was pretty amazing. S$200 on a S$3000 salary is about 6.67% of the monthly salary, which is no joke.

Over time, as my salary went up, the welcome bonus as a percentage of my net worth became less attractive (at this point, I also had just about every credit card out there). But because my expenditure also went up, the potential rewards from the credit card also went up, and it became more important to choose cards based on my spending pattern, and preferred reward.

To put it simply, if you’re going to spend S$1000 each month anyway, you might as well get something back for it, whether its air miles or cashback.

Of course, with credit cards there are a couple of points to note:

Pay bills promptly – Treat your credit card like a debit card. Make every payment promptly. The late payment fees are pretty ridiculous (about 24% per annum effective interest rate), so the moment you fail to pay your bill on time, or you rely on the credit function of the credit card, you’re paying the bank so much in lending fees that you’re effectively subsidising the rewards for all the other users who are paying on time. So yes, try to be the one who is enjoying the benefit, not the one who is paying for it.

Everything can be waived, mostly – Regardless of what the bank says, most annual fees can be waived, if you call them and make enough noise. This applies to late payment charges as well. Some banks are easier than others (usually the foreign banks like HSBC and Standard Chartered), while the local banks require more effort (OCBC and UOB especially), but you can usually get just about anything waived if you have enough perseverance.

Basics: Miles Card

There are 3 kinds of credit cards. A Miles card, a Cashback card, and Rewards card.

Miles cards give you airline miles in exchange for spending. Cashback cards give you a small amount of cash back. Rewards cards give you reward points denominated in the bank’s reward currency, which can then be exchanged for products / vouchers based on the bank’s exchange rate.

Personally, I suggest only going for Miles or Cashback cards. Rewards cards are ridiculously complicated, and incredibly hard to compare across banks, because each bank has different reward points and different redemption rates. It’s far easier to stick with an easy to use currency like airmiles or you know, cash.

Whether to use a miles card or a cashback card is really up to your personal preference, whether you like miles or cash more.

I know some people who absolutely swear by miles cards.

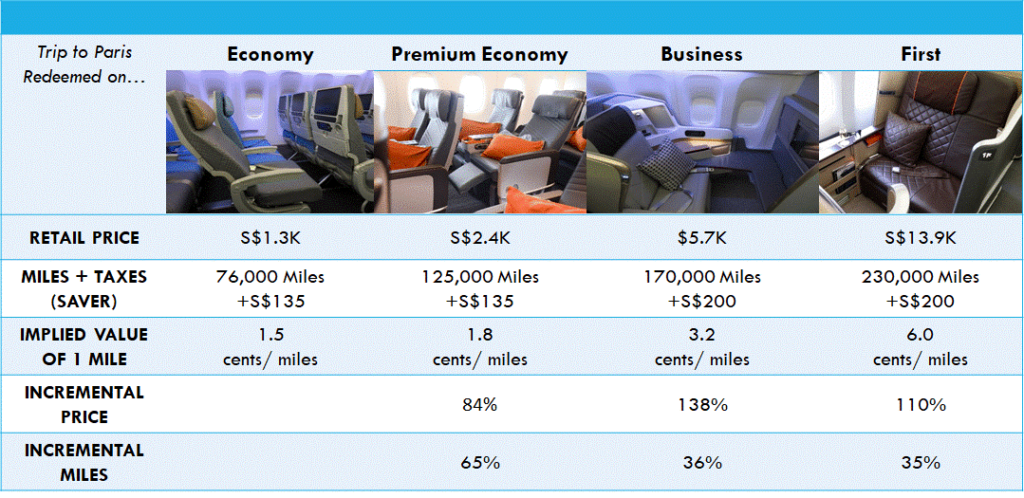

To understand why, you just need to take a look at the chart from Milelion below.

Essentially, if you fly to Paris on economy, the ticket costs S$1.3k or 76,000 miles + S$135. So the implied value of 1 mile is 1.5 cents.

If you fly to Paris on first class instead, the ticket costs S$13,900, or 230,000 miles + 200. The implied value of 1 mile is now a whopping 6.0 cents.

What this means very simply, is that if you want to get the most bang for your buck, you should be using your air miles for long haul flights, and on premium classes (Business or First Class). Once you do so, miles actually become ridiculously worth it (probably more than cashback cards):

- Economy/Premium Economy: 1-2 cents per mile

- Business Class: 4-6 cents per mile

- Suites/First Class: 6-9 cents per mile

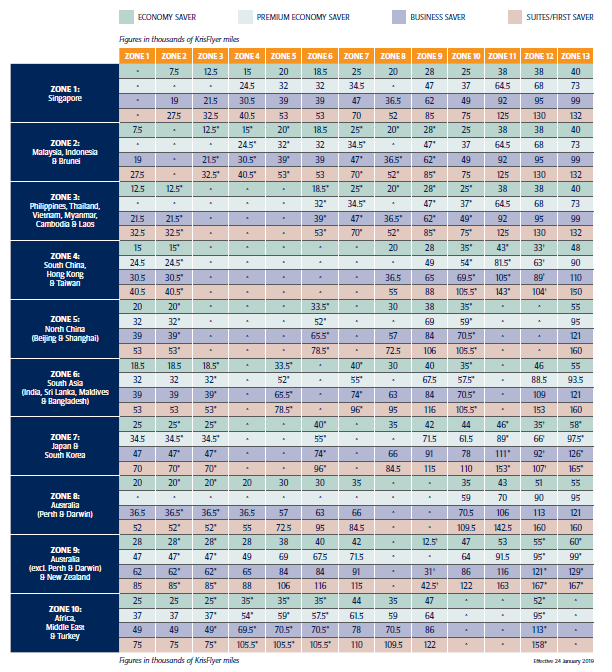

The latest exchange rates for miles are set out below:

So yes, if you’re a miles card kind of guy, chances are you’ll be a miles card guy for life. Because once you exchange all your miles for a fancy first class flight to Paris that costs S$14,000 retail price, you’re probably never coming back down to earth to use anything else.

Most people I know would also never spend their cash on a business or first class flight, but with their miles they are more than happy to do so. So yes, there is also that psychological aspect of miles not really being “cash”, making it that much easier to spend.

Comparison of Cards

I’ve benchmarked 6 different miles cards in this article, which to me represents the most popular / mainstream miles cards available to the Singaporean consumers today.

I’ve set out their annual fee and minimum income below as well.

| Annual Fee | Minimum Income | |

| Citi Premier Miles Visa | Annual Fee: S$192.60 | S$30,000 (Singaporean/PR) or S$42,000 (Foreigner) |

| UOB PRVI Miles Visa Card | Annual Fee: S$256.80 (First Year Fee Waiver) | S$30,000 (Singaporean/PR) or S$40,000 (Foreigner) |

| American Express Singapore Airlines KrisFlyer Ascend Credit Card | Annual Fee: S$337.05 | S$50,000 (Singaporean/PR) or S$60,000 (Foreigner)

|

| Standard Chartered Visa Infinite Credit Card | $588.50 including GST. This annual fee is strictly non-waivable. | S$150,000 (Singaporean/PR) or S$150,000 (Foreigner)

|

| American Express Singapore Airlines KrisFlyer Card | S$176.55 (inclusive of GST) waived for the first year | S$30,000 (Singaporean/PR) or S$60,000 (Foreigner)

|

| DBS Altitude Visa Signature Card | S$192.60 (Principal card) waived for the first year | S$30,000 (Singaporean/PR) or S$45,000 (Foreigner)

|

Couple of key points to note:

- All 4 cards, the Citi Premier Miles Visa, the UOB PRVI Miles, the Amex Krisflyer, and DBS Altitude are mainstream cards, with S$30,000 minimum income and the usual annual fee of about S$200.

- Amex Krisflyer Ascend is a slightly premium card with S$50,000 income and S$300 annual fee

- Standard Chartered Visa Infinite Card is a premium card with S$150,000 income and S$588 annual fee that is strictly non-waivable.

Miles Earn rate

| Miles earned per S$1 local spend | Miles earned per S$1 overseas spend | |

| Citi Premier Miles Visa | 1.2 | 2 |

| UOB PRVI Miles Visa Card | 1.4 | 2.4 |

| American Express Singapore Airlines KrisFlyer Ascend Credit Card | 1.2 | 2 (June and December only) |

| Standard Chartered Visa Infinite Credit Card | 1.4 | 3 |

| American Express Singapore Airlines KrisFlyer Card | 1.1 | 2 (July and December only) |

| DBS Altitude Visa Signature Card | 1.2 | 2 |

The earn rate for the cards are set out above. Key takeaways:

- Standard Chartered Visa Infinite Credit Card – The standard chartered card has the best earn rates with 1.4 miles per S$1 local spend, and 3 miles per S$1 overseas spend. Unfortunately because of its premium card status, with a high annual income threshold and high annual fee that is not waivable (S$588), this card is best suited for high spenders. So you really should know what you want out of this card before signing up for it. It’s probably best for those with a higher income, who travel often for work, and charge large amounts to their credit card while overseas.

- UOB PRVI Miles Visa Card – This is probably the best mainstream card in terms of earn rate. The 1.4 miles per S$1 local spend is exactly the same as the Standard Chartered card, and the highest in this comparison. The overseas earn rate is slightly lower at 2.4 (versus 3), but what you get in exchange, is an annual fee that can be waived, and a far lower income threshold.

- Citi Premier Miles Visa, DBS Altitude Visa Signature Card – The next best tier will be the Citi PMV, and the DBS Altitude, at 1.2 miles per S$1 local spend, and 2 miles per S$1 overseas spend.

Welcome Gift

I’ve summarised the key welcome gifts below (it’s not exhaustive, so for the full list do check on the card websites).

| Welcome Gift | |

| Citi Premier Miles Visa | $200 NTUC Fairprice vouchers, Takashimaya vouchers or Grab promo codes upon approval for new customers only.

Get 30,000 bonus miles with annual fee payment (first year – S$192.60) + spend a min. of $7,500 within the first 3 months for NEW cardholders. |

| UOB PRVI Miles Visa Card | $50 cash reward when your card is approved.

Get up to 12,000 welcome miles when you sign up and make a min $4,000 spend in 1st 60 days of card approval, valid till 14 July 2019. Register via SMS and limited to first 2,000 spenders. |

| American Express Singapore Airlines KrisFlyer Ascend Credit Card | Apply via MyInfo and get S$50 Capitavouchers.

Receive 5,000 welcome miles on first spend on card. Spend $10,000 within 3 months of card approval and receive 27,000 miles. Spend another $10,000 between 4th to 6th month of membership and receive additional 27,000 miles. Receive an exclusive bonus of 6,500 additional KrisFlyer miles for all applications upon S$10,000 spend within the first 3 months of Card approval. |

| Standard Chartered Visa Infinite Credit Card | Get $100 cash when your card is activated – for new customers only! Existing customers get $50 cash.

Receive 35,000 welcome miles with payment of annual fee ($588.50). |

| American Express Singapore Airlines KrisFlyer Card | 5,000 KrisFlyer miles the very first time you charge to your Card.

Receive 7,500 KrisFlyer miles when you spend S$5,000 in the first 3 months, and an additional 7,500 KrisFlyer miles when you spend S$5,000 in the 4th to 6th month of Card Membership. |

| DBS Altitude Visa Signature Card | 10,000 welcome miles (with min. spend of S$2,000/month or first three months), extra 10,000 miles with annual fee payment |

There’s a lot of gimmicks with the welcome gifts, but personally, this is how I see it:

- Citi Premier Miles Visa – The Citi PMV card has the best welcome gift. It’s basically S$200 cash upfront once the card is approved. And if you’re able to spend S$7,500 in the first 3 month, and you pay the annual fee, you get an additional 30,000 miles. Assuming a 6 cents conversion rate, that 30,000 miles actually works out to be about S$1,800 in dollar value, which is not too bad indeed!

- American Express Singapore Airlines KrisFlyer Ascend Credit Card – If you’re a really big spender, Amex Krisflyer Ascend has a pretty amazing welcome gift. It’s basically 38,500 miles if you spend S$10,000 within 3 months, and another 27,000 if you spend S$10,000 in the next 3 months. That’s a whopping 65,500 miles if you can hit the spending targets.

- UOB PRVI Miles Visa Card – If you’re not a big spender, UOB PRVI is a good choice. You get S$50 just to get the card approved, and you can just ignore the welcome miles if you can’t hit S$4000 spend in the first 2 months.

Other Considerations

A reader left an amazing comment on the other considerations to look out for when picking a miles card. Have extracted it in full below, for the benefit of all readers:

There are other things to consider, e.g. redemption fees. Most of the cards (actually all except for Amex Krisflyer series) charges S$25+ per redemption, and you can only redeem miles in multiples of 5k or 10k. Even though most people won’t redeem very often but it is still a discount on the reward you get.

Amex Krisflyer series automatically credit the miles you earn to your Krisflyer account at no charge each month. However, Krisflyer miles do expire in 3 years but usually miles in your credit cards don’t.

Also there’s a Citi PremierMiles Amex card, it doesn’t have much welcome bonus as the Visa version but it gives you 1.3 miles per dollar (with higher annual fee and income threshold).

Battle of Cards

To sweeten the deals, Singsaver is now running a “Battle of Cards” promotion. The full rules are set out here, but the crux of what you need to know is this:

- From 29 Apr, Mon – 12 May, Sun, there is a battle of cards contest organised by Singsaver.

- The following cards will be competing (basically the first 4 in the table above):

- Citi Premier Miles Visa

- UOB PRVI Miles Visa Card

- American Express Singapore Airlines KrisFlyer Ascend Credit Card

- Standard Chartered Visa Infinite Credit Card

- If you sign up for one of the cards via the Singsaver links below, and it turns out to be the most popular card (the most signups), you win an extra S$50.

- The S$50 is on top of all the welcome gifts set out above, so you don’t lose anything by participating.

I know it’s a bit of a gimmick, but hey, if you get it right it’s basically free cash, so if you’re in the market for a new miles card, there’s no reason to not join this contest.

The signup links for the cards are below. Don’t forget that the Battle of Cards only starts on Monday 29 April, so I would highly suggest waiting until then to apply for it:

Campaign Page

Citi Premier Miles Visa Card

UOB PRIVI Miles Visa Card

AMEX KrisFlyer Ascend

Standard Chartered Visa Infinite Card

AMEX KrisFlyer (not part of the battle of cards contest, but you can signup anyway)

Recommendation

My personal recommendation would be this – I think the most popular card will likely be either the Citi PMV card, or the UOB PRVI Miles card. They are both mainstream cards, with low annual fees that can be waived, and lower income thresholds. The miles earn rates are also highly competitive.

Between the two, go with Citi PMV if you want the S$200 welcome gift, and a decent miles card. If you can spend S$7500 in 3 months, the welcome gift is too good to pass up.

Otherwise, if you want a card with the best earn rate going forward, and are less concerned about the welcome gift, go with UOB PRVI.

And if you’re a really big spender, or if you have a wedding coming up (such that you can hit S$20,000 spend in 6 months), go with Krisflyer Ascend, the 65,500 miles is ridiculously good.

Closing thoughts

We talk about investing a lot on this site. But while we do, it’s important to recognise that at the end of the day, money is just money. Money can do a lot of things, but until you actually exchange it for goods or services, it’s not really going to make you happy.

So it’s important not to forget to enjoy the finer things in life. Sometimes, you really have to slow down and take the time to smell the roses. You don’t want to lie on your death bed with your millions in networth wondering how different life could have been.

If you’re a travel aficionado, and you love travelling around the world, a miles credit card is probably the best way to redeem premium flight tickets on the cheap. Travelling business class all the way to Paris or London can feel pretty amazing if you’re redeeming it for “miles”, because it doesn’t really hit your wallet (and the value for money is great). So yes, if you’re into travel, I highly suggest getting one of the cards above, if you haven’t already gotten them.

Share your thoughts in the comments section below! I respond personally to all comments!

Enjoyed this article? Do consider supporting the site as a Patron and receive exclusive content. Big shoutout to all Patrons for their generous support, and for helping to keep this site going!

Like our Facebook Page and join the Facebook Group to continue the discussion! Do also join our private Telegram Group for a friendly chat on anything investing related!

There are other things to consider, e.g. redemption fees. Most of the cards (actually all except for Amex Krisflyer series) charges S$25+ per redemption, and you can only redeem miles in multiples of 5k or 10k. Even though most people won’t redeem very often but it is still a discount on the reward you get.

Amex Krisflyer series automatically credit the miles you earn to your Krisflyer account at no charge each month. However, Krisflyer miles do expire in 3 years but usually miles in your credit cards don’t.

Also there’s a Citi PremierMiles Amex card, it doesn’t have much welcome bonus as the Visa version but it gives you 1.3 miles per dollar (with higher annual fee and income threshold).

That’s an amazing comment, thanks for sharing! I’ll update the article to take this into account.

Hey FH,

I know that your post is a targeted campaign for SingSaver air miles cards signups via affiliate links, but you are doing your readers a disservice by brushing off the Rewards cards :

Citibank – Citi Rewards

OCBC – Titanium Rewards

DBS – Woman’s Card

UOB – Preferred Platinum

The above 4 all have ample opportunities to earn 4 miles/dollar with easy-to-distinguish spend categories plus simple redemption procedures. Give them some love in your next post, maybe? 😛

Hi Turtle Investor!

Thanks for dropping by. Interesting point, I didn’t really look into rewards cards for this post. Do you use rewards cards for miles? Surely there has to be some catch, it can’t be that Rewards cards offer such a significantly better reward rate vs miles cards.

Cheers.

No catch per say but each card comes with different spending T&Cs – most SG mile chasers make the vast majority of their miles with rewards cards, meaning there is no way you can ignore these when writing about miles cards 🙂

Take the UOB Preferred Platinum for example – that one gives 4 miles/$ for every Paywave transaction you do up until $1k. Now calculate how much spending it would take to reach 4,000 miles/month with the cards above 🙂

The cards above are only valid when the Rewards cards fail you – which is usually after having maxed them out.

Haha thanks for the heads up. Probably need to update this article to take into account rewards cards then. Never realised they were so good for earnings miles.

Cheers.

Great article!There’s also a new UOB KrisFlyer credit card that just got announced coupla days ago that seems comparable to the above.

Oh yes you are right. The earn rates are pretty similar to those above (1.2 per S$1 local spend. 3 per S$1 foreign spend).

Cheers!

https://www.uob.com.sg/personal/krisflyer-uob/credit/features.html

Hello FH,

Not to forget, Citi Premier miles doesn’t expire! That itself is a great seling point!

Great point, thanks for sharing!

Good summary. Couple of points to take note. First is the validity or expiry date of the points/miles. Especially for moderate to low spenders as reaching 50k-100k takes a while and need to make sure the miles/points on credit card still stay there. Second one is the earn rate per dollar vs in different blocks. This is totally on the purchase pattern. For example, UOB calculates in $5 block (UN$3.5 or 7 miles per every $5 spend), and if the spend tend to go in between and it’s a loss over multiple transactions (I did a calculation and majority of my expenses tend to fall in between 5-10).

Great comment! Those are really good points to take note of, perhaps I’ll do a revised post to include all these considerations.

Cheers.