I recently received this query from a reader (published anonymously with consent):

Dear Financial Horse,

I am writing to request for further assistance to building a diversified portfolio. I have read stock analysis and calculations of the US largest companies on the stock markets, I have no clue where to begin because of the ever-changing dynamics of the political and economic environment. I do not know the history/trend of their performance unlike experienced investors.

My reason for wanting to invest in securities is because I would like to save up enough to buy a condominium in five years’ time. Yes, it may sound ambitious or even greedy but I want to give my mum the best in the world. Although I love my 9-6 job, my salary will never get me close. At 28 years old, I am willing to take the risk to invest my savings, leaving my CPF untouched.

I currently have DBS vickers which I intend to purchase local stocks and REIT with. As mentioned in another email, I am thinking of starting a SAXO account for overseas stock. I am currently trying their demo. Another concern is will the earnings from US ETF be taxable? I know dividend from US stock will suffer withholding tax.

I hope you can advise me how to go about building a portfolio and recommend me some stocks (both local and overseas) to start with. From there I will do research and whatever I decide to purchase will be entirely my decision and not hold you accountable.

Thank you for taking time to read my lengthy email and I wish you a good weekend.

It’s a very interesting question, and one that I wanted to tackle via a full article. Let’s break his profile down further:

- He has basic investing knowledge and experience. Accordingly, the investments should not require advanced investing expertise.

- He wants to save up for a condo downpayment in 5 years. Assuming conservatively a S$1 million condo, that’s a S$250,000 downpayment after the recent changes to LTV limits.

- He is 28 years old and his salary will not get him close to his financial goal. Unfortunately I don’t have information on how much savings he has thus far, and how much he can save each month.

- He will leave his CPF untouched.

- He is looking at local stocks, REITs, and overseas stocks.

To address his question on whether US ETF dividends are subject to withholding tax, the answer is a resounding yes (30% withholding tax, although he can reduce it to 15% by buying Irish domiciled ETFs). I recently wrote a guide on this, do take a look for more information.

Investing your way to a condo downpayment

There are 2 schools of thought when it comes to saving up for a condo downpayment:

- “Kiasi” (afraid to die) mentality: With a 5 year timeframe, stocks are too volatile. Accordingly, I should focus purely on safe, risk-free instruments, and focus efforts on saving more by increasing income or reducing my expenses.

- “YOLO” mentality: My salary alone will never get me there. My only hope is to go all-in on stocks, and hope that a 5 year bull run generates enough returns for my downpayment.

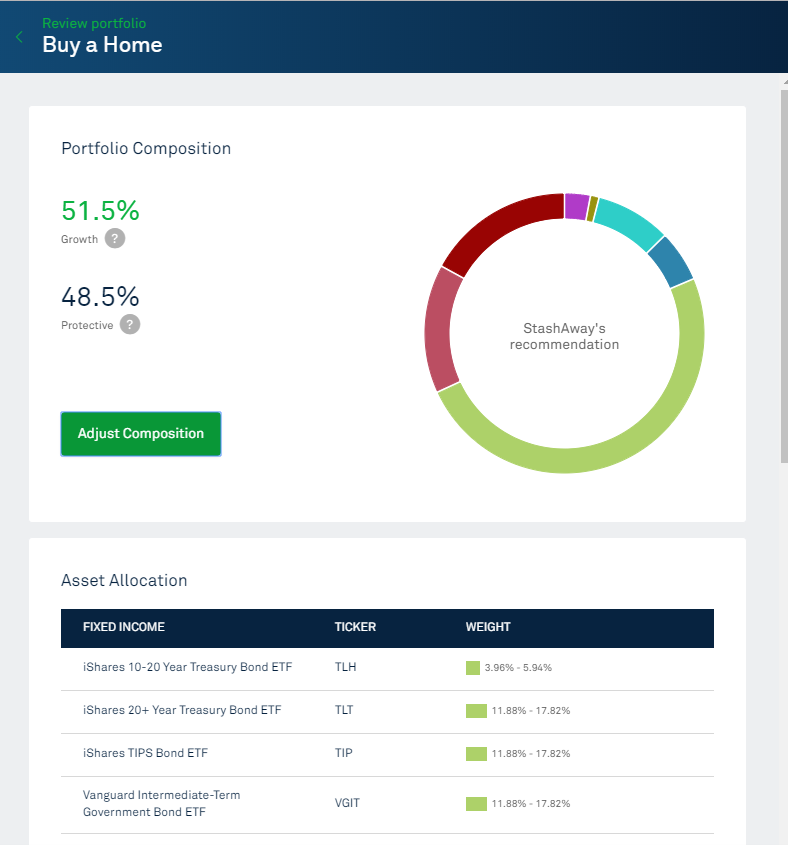

StashAway (“Kiasi” portfolio)

With that in mind, I went to StashAway, selected my investment objective as “Buy a Home” in 5 years, and they generated the following asset allocation for me:

Text version below:

| FIXED INCOME | TICKER | WEIGHT | |

| iShares 10-20 Year Treasury Bond ETF | TLH | 3.96% – 5.94% | |

| iShares 20+ Year Treasury Bond ETF | TLT | 11.88% – 17.82% | |

| iShares TIPS Bond ETF | TIP | 11.88% – 17.82% | |

| Vanguard Intermediate-Term Government Bond ETF | VGIT | 11.88% – 17.82% |

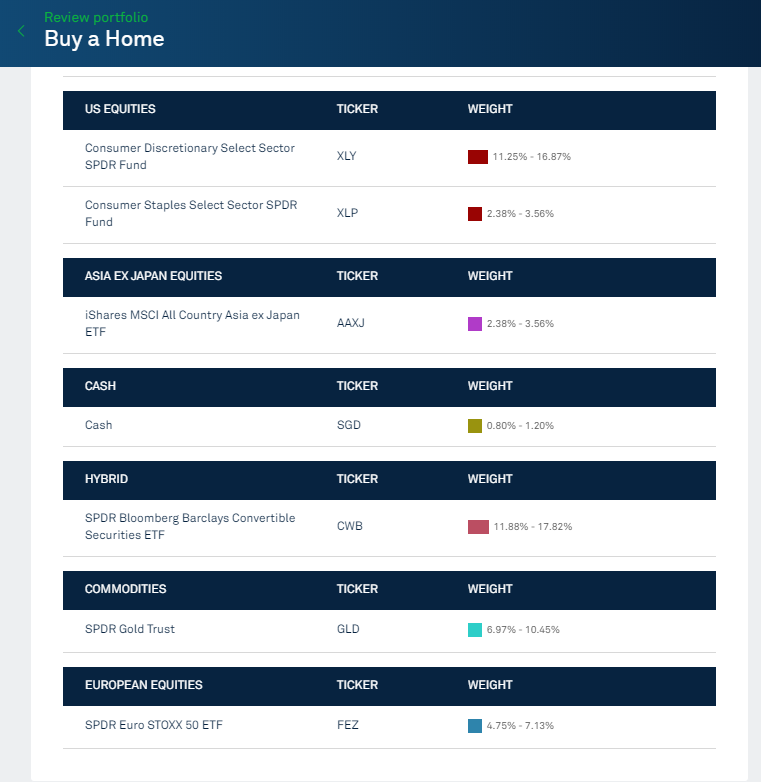

| US EQUITIES | TICKER | WEIGHT | |

| Consumer Discretionary Select Sector SPDR Fund | XLY | 11.25% – 16.87% | |

| Consumer Staples Select Sector SPDR Fund | XLP | 2.38% – 3.56% |

| ASIA EX JAPAN EQUITIES | TICKER | WEIGHT | |

| iShares MSCI All Country Asia ex Japan ETF | AAXJ | 2.38% – 3.56% |

| CASH | TICKER | WEIGHT | |

| Cash | SGD | 0.80% – 1.20% |

| HYBRID | TICKER | WEIGHT | |

| SPDR Bloomberg Barclays Convertible Securities ETF | CWB | 11.88% – 17.82% |

| COMMODITIES | TICKER | WEIGHT | |

| SPDR Gold Trust | GLD | 6.97% – 10.45% |

| EUROPEAN EQUITIES | TICKER | WEIGHT | |

| SPDR Euro STOXX 50 ETF | FEZ | 4.75% – 7.13% |

To be fair, this is a very interesting asset allocation, and one that I really liked personally. Broadly, it’s a 60% bond, 10% gold, 30% defensive stocks portfolio. This is firmly in the “Kiasi” mentality. If you want a safe portfolio without too much hassle, its actually a pretty good option. You can just set it up, credit money to it monthly, and let it handle all the purchase and rebalancing.

Of course, I do have a few gripes with this allocation:

- There’s a fair bit of forex exposure here, which can work for or against you.

- Singapore stocks and REITs are currently trading at quite attractive valuations, so I would want to have some exposure to them. Holding SGD denominated investments also reduces forex risk.

“YOLO” portfolio

For the “YOLO” mentality portfolio, I came up with the following 100% stock allocation:

| STOCK | TICKER | WEIGHT | |

| US NASDAQ ETF | QQQ | 40% | |

| Global ETF | IWDA | 40% | |

| STI ETF | ES3 | 20% |

I do have to caveat that this is a high risk portfolio. If there is a market drawdown, you could well experience losses in excess of 50% of your principal. However, given that the thinking behind this portfolio is to go all-in on the market to maximise future returns (at the expense of risk), I think it does achieve its goals, while still being a relatively straightforward portfolio to buy and maintain.

What would Financial Horse do?

The 2 portfolios above serve to illustrate both ends of the spectrum, being a conservative “Kiasi” portfolio and an aggressive “YOLO” portfolio.

Of course, no article will be complete without Financial Horse sharing his personal thoughts on what I would do in such a situation, so I shall gladly oblige. Please note that this decision depends greatly on your risk appetite, your current financial situation, and attitude towards life. I leave it to you to judge whether this is appropriate for your situation.

But putting all that aside, this is what I would do:

Investment Portfolio

I’m a bit of a “Kiasi” guy (I’m a lawyer after all), so my hypothetical portfolio will reflect that:

| Stock | TICKER | WEIGHT | |

| US NASDAQ ETF | QQQ | 15% | |

| US S&P500 ETF | SPY | 15% | |

| DBS (Singapore Stock) | D05 | 10% | |

| Mapletree Commercial Trust (Singapore REIT) | N2IU | 15% | |

| Risk Free Assets | Split between Singapore Savings Bonds (SSBs), or DBS Multiplier/UOB one as appropriate. | 45% |

Thinking behind this portfolio:

The 30% exposure to US stocks is to gain exposure to the higher growth US equity market, and forms the riskier part of the portfolio.

The Singapore REITs serve as a diversification into real estate for the portfolio, while generating decent yield. I picked Mapletree Commercial Trust because I really like this REIT, and it offers exposure into the retail and commercial space (check out my previous article on MCT). I understand that 1 REIT is a bit too concentrated, but given that his starting capital is likely to be small, adding too many counters here would increase brokerage costs. It’s better to start with 1 good REIT, and then slowly expand into more counter. That said, over time, I would want to work towards the following portfolio: Split between MCT (2 parts), Ascott Residence Trust (1 part), Mapletree Logistics Trust (1 part), Netlink Trust (1 part). This offers a more diversified portfolio within the REIT/BT space with exposure to a range of asset classes.

DBS is included because that is just about the only Singapore stock I am comfortable including in such a portfolio (UOB/OCBC are fine too, it’s a personal preference between the 3 local banks). In a rising interest rate environment, bank earnings should improve which should boost share price, and this may offset some of the impact if REITs were to decline due to rising interest rates.

I also included 40% in risk free assets because we are quite late in the economic cycle, and I’m not comfortable going all-in on the market at this time. With SSBs yielding 1.78% first year (2.57% over 10 years), and DBS Multiplier/UOB One yielding up to 2.4%, cash is a pretty decent alternative these days too. Priority will go to DBS Multiplier/UOB One for the higher interest rates, just pick the account where you can easily hit the targets, or open both. If you’ve maxed out both accounts or can’t be bothered to hit the targets to earn higher interest, you can use SSBs instead.

Professional life

To me, investing should only be one part of the puzzle. Equally important is your earnings and savings rate. For me, I would continue to work hard in my professional life. Regardless of what you may think, working hard, having a good attitude, and actively sourcing for new job opportunities can increase your income drastically. Don’t adopt a defeatist mentality towards your professional life. If you can’t even convince yourself that you need a payraise, how do you convince a future employer of the same?

Expenses

Needless to say, cut down on unwanted expenses. If you want to save up for a condo to give your mum a better life, there will need to be some sacrifices in your personal life. Try to reduce your expenses as much as you can. Every dollar saved is a dollar less that you need to earn from investments. That Starbucks coffee or avocado toast should go.

Side Hustle

With the rise of technology these days, starting a side hustle is easier than ever. Work on a hobby that you are passionate about in your free time, and figure out how to monetise it. It could be anything from selling Taobao goods on Carousell to freelancing as a photographer to driving a Grab. The world is your oyster, and there are countless opportunities for an enterprising young man to earn extra income on the side. I started Financial Horse earlier this year because investing is my passion, and I have absolutely no regrets.

Mental State of Investing

Having said all these, I feel that I should touch on the mental state of investing. Investing in stocks in a high risk endeavour, and in a market crash you can easily see 50% of your gains wiped out. If you are a beginner investor, you may not be able to stomach those losses without panic selling. This is compounded by the fact that you urgently need the cash for the condo downpayment.

Ask yourself this, if you put S$100,000 of your hard earned money into an ETF, and it falls in value to S$50,000, what would you do? If you are likely to sell, then perhaps stocks are not for you, and you may want to stick to lower risk investments until you achieve your financial goal of buying a condo.

Property as an investment

I also wanted to touch on property as an investment. I understand that you want to buy a condo to give your mum a better life, but have you considered getting a BTO instead? An equivalent BTO will go for half the price, and there are many attractive financial incentives to lessen the burden.

This would allow you to get a nice apartment, while also freeing up a huge amount of liquidity that you can invest for the longer term. This gives you more time to save up, and for the investment returns to compound, and you can purchase a condo further down the road when you are financially more stable. Don’t forget that with the recent spate of property cooling measures, it seems clear that the government doesn’t want residential properties to become an investment product, so your future returns may not be fantastic from an investing perspective.

At the end of the day though, I won’t profess to know everything about your personal situation, and I won’t pass judgment on your financial goals. If you think a condo is what you want, by all means go for it.

Of course, to complicate the matter, don’t forget that property prices do not trade in a vacuum. Condo prices are likely to move in tandem with global asset prices, and if the economy and global markets are strong, condo prices are likely to trend upwards. At the same time, if there is a global market crash, even though you may suffer losses on your stocks, property prices may trend downwards and reduce the amount you need on your downpayment. Regulatory change also plays a part, and a future change to the LTV ratio could easily reduce (or increase) the amount of cash you need on your downpayment (it used to be 20% on a first home, but this just got increased to 25%).

Closing Thoughts

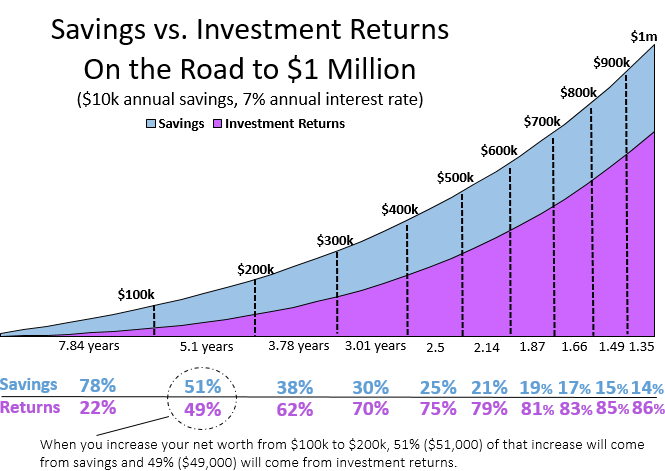

I have a feeling that you are looking at investments as a magic pill, in your quest to buy a condo. That’s a dangerous mentality that is no different from gambling. Have a look at the chart below. Assuming S$10,000 annual savings at a constant 7% return annually (which isn’t fully accurate because short term returns from the market may be lumpy), even after 7.8 years only 22% of that comes from your investments. The other 78% comes from your savings.

With a 5 year timeframe, that equation is going to be skewed even more heavily towards your savings. I think the moral of the story here is clear. Investing is important, but it’s not going to solve your problem on its own. Focus on earning more in your professional life, spending less in your personal life, and earning side income on your weekends. Then take this money, and invest it prudently in a safe, diversified portfolio. If you do these, you will well be on track to buying your mum a condo. It may take you 2 or 3 years more than your 5 year timeframe, but sometimes, it’s better safe than sorry. If you go all-in on the market now and there is a crash, it can set you back another 5 years on your journey.

Good luck on your journey!

Financial Horse has a set of 7 Commandments for Successful Investing, that I ask myself before making every investment, and that I will never break regardless of the situation. Enter your email below to receive a copy in your inbox!

[mc4wp_form id=”173″]

Enjoyed this article? Like our Facebook Page for more great articles, or join the Facebook Group to continue the discussion!

Hi FH, your recommended portfolio does not add up to 100%. Are u suggesting the last 5% to be cash?

The cash portio was meant to be 45%. I have corrected this. 🙂

Hi Financial Horse, awesome and interesting write up! You are the bestz!

For the fun of it….can I suggest a 3rd option? The reader can get married fast and get his/her new wife/hubby to chip in half (50%) of S$250K….hehe.

Hahahah… that definitely works too. 😉

if 1 starts to explore into liquidity, concentration risk , commission & miscellaneous charges. There’s really no point to buy a property for investment , but for self stay.

Agreed, especially with the latest cooling measures, which signifies the government’s intention to move away from property as an investment. For this case though, it seems that the reader wanted to purchase a property for him and his mother, so I guess that’s about as good a reason as one can ever have to buy a property.

These months are the best times to invest a condo because of the following: Prices are the lowest. Discounts are greatest during these months, thus, prices are lowest. More sellers, less buyers.

Agreed. Although that said, the secondary market usually requires some time (6 to 12 months) to adjust to the revised market sentiment. Some of the asking prices in the resale market looks quite unrealistic today, and I suspect better buying opportunities may pop up next year.