As I’m sure all of you have heard by now.

We finally have a conclusion to the Credit Suisse saga.

Because UBS has agreed to buy out Credit Suisse, supported with a liquidity backstop from the Swiss National Bank.

With things like this though – the devil is in the details.

And there are two points with the “bailout” that are very concerning:

- AT1 Bondholders (CoCo) wiped out ahead of equity holders – this will trigger repricing of AT1s across the board

- The speed of the deal is astounding – how bad was the run on Credit Suisse last week?

I’m not going to mince words.

I thought the bailout was very poorly done.

The wiping out of CoCo ahead of equity holders just threw the entire rulebook (built over the past decade) for AT1 bonds out of the window.

This is going to trigger forced repricing (even selling) across the board, in what is close to a $300 billion asset class.

In a market where sentiment is already very weak.

But we’re getting ahead of ourselves.

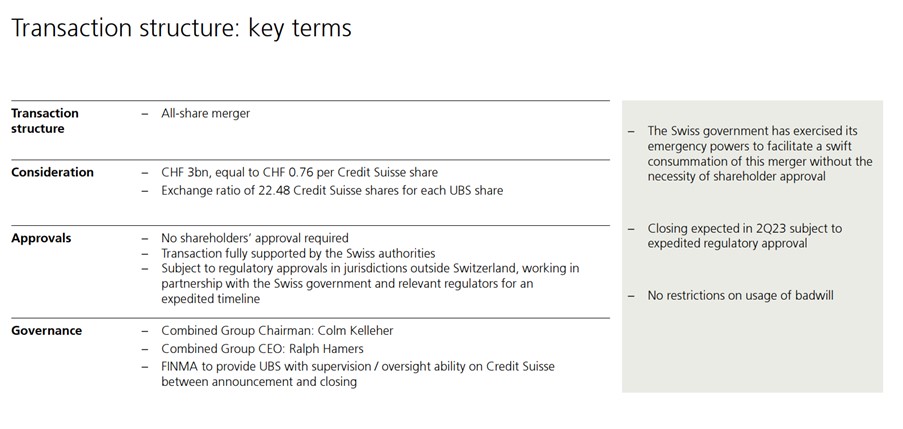

Explained: Credit Suisse bought over by UBS

But let’s start with the details of the buyout.

All Share Deal – SFr0.76 a share (60% below Friday’s close)

This is an all share deal, so Credit Suisse shareholders will get paid in the form of UBS shares and not cash.

The price is SFr0.76 a share.

Credit Suisse shares closed at SFr 1.86 on Friday, so the buyout price is a whopping 60% below Friday’s close.

Shareholders who bought last week would be looking at pretty hefty losses.

AT1 (CoCo) Bondholders wiped out

If you thought that was bad though.

AT1 (CoCo) bondholders are completely wiped out.

100% loss.

This has massive implications for AT1 pricing for banks across the board, and we’ll discuss this in much further detail below.

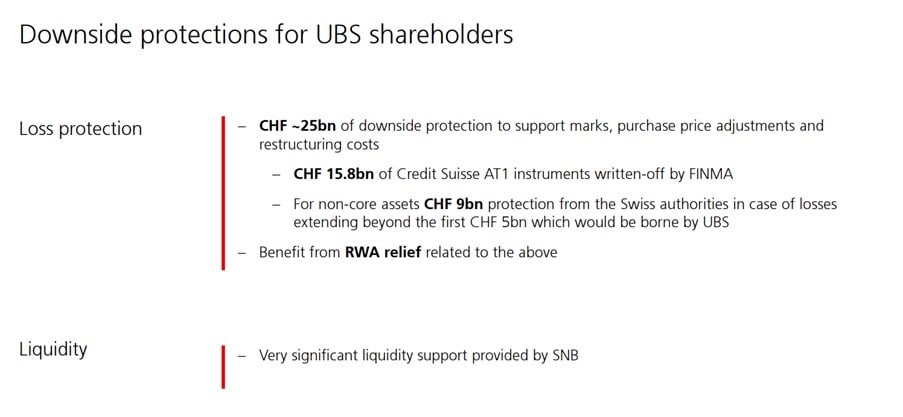

Swiss Central Bank provides a liquidity backstop

To sweeten the deal, this is what is provided by the Swiss Central Bank:

As part of the deal, the SNB has agreed to offer a SFr100bn liquidity line backed by a federal default guarantee to UBS, the Swiss finance ministry said. The government is also providing a loss guarantee of up to SFr9bn, but only after UBS has borne the first SFr5bn of losses on certain portfolios of assets.

This is a premium Patreon post. I am making it available to all readers in the hopes that this might help you make sense of what is going on.

If you find this useful, do support Financial Horse as a Patreon. You can get regular premium updates just like this, together with my full REIT and stock watchlist.

Sign up here.

AT1 (CoCo) wiped out will trigger repricing of AT1s across the board

Let’s deal with the elephant in the room.

AT1 / CoCo bondholders are completely wiped out.

While equity holders get 3 billion.

Understanding why this is a problem requires a bit of background.

Bloomberg has a great article on it, which I extract below (emphasis mine, but if it’s too technical feel free to jump straight to my summary below).

They’re called contingent convertible bonds, or CoCos — and are often described as high-yield investments with a hand grenade attached. The takeover of Credit Suisse by UBS Group AG included pulling the pin on $17 billion of CoCos, which are also known as Additional Tier 1 (AT1) bonds. This is in keeping with the idea behind the birth of CoCos in the wake of the European debt crisis. CoCos are the lowest rung of bank debt, meaning that while they produce juicy returns in good times, they’re designed to be among the first to feel pain if a bank’s troubles get bad enough. The vaporizing of Credit Suisse’s CoCo debt will strengthen the balance sheet of the newly combined bank — but could spell disaster for the wider CoCo market.

- What is a CoCo bond?

They’re essentially a cross between a bond and a stock that helps banks bolster capital to meet regulations designed to prevent failure. They’re contingent in the sense that their status can change if a bank’s capital levels fall below a specified level; they’re convertible because in many cases they can be turned into equity — shares of the bank — if the shortfall gets big enough. In other cases CoCos are written down in whole or in part.

- What are CoCos for?

They make up part of a buffer of debt and equity that’s intended to prevent taxpayers from having to shoulder the bill for a bank’s collapse. When they were dreamed up, CoCos were seen as giving banks a potentially bigger capital cushion without forcing them to issue new stock, amid concern in that many were over-leveraged. For regulators, CoCos are a way for banks to be pulled back from the brink without the cost falling on taxpayers and without diluting existing shareholders. CoCos are also known as Additional Tier 1 (AT1) bonds.

- How many did Credit Suisse have?

The Swiss lender’s holding company had 13 CoCos outstanding worth a combined $17.3 billion, issued in Swiss francs, US dollars and Singapore dollars, according to data compiled by Bloomberg. That’s just above 20% of its total debt pile. Its biggest CoCos were denominated in US dollars — it had a $2b perpetual note that could have been called in July and a $2.25b note with a first call in December. CoCos are typically undated, meaning the bond has no defined maturity but lenders can call for repayment normally after around five years. Investors price CoCos to their expected worth at their first call dates. When they’re not called — in other words, when they’re extended — prices tend to fall. The recent global market selloff has driven corporate funding costs higher, meaning there’s now a higher chance a lender could opt to skip a call because it could prove expensive to replace an existing note with a new one.

- Why were Credit Suisse’s CoCos wiped out?

UBS has agreed to buy Credit Suisse in a government-brokered deal aimed at containing a crisis of confidence that threatened to cascade across global financial markets. Because of the extraordinary government support, it will trigger a “complete write-down” of the bank’s AT1 bonds in order to increase core capital, Swiss financial regulator FINMA said in a statement on its website. In simple terms, banks need to meet a minimum requirement for the amount of their own funds and eligible liabilities, more commonly known as MREL, to support an effective resolution in the event of a collapse. If a lender’s capital ratios fall below a predetermined level, then CoCos can be written down.

- Had investors been worried about a writedown?

Yes. Prices on Credit Suisse’s CoCos had flip-flopped in the hours leading up to the announcement of a deal with UBS as traders weighed two contrasting scenarios: either the regulator would nationalize part or the whole bank, possibly writing off Credit Suisse’s AT1 bonds entirely, or a UBS buyout with potentially no losses for bondholders. In the end, it ended up being a bit of both, after the government stepped in to facilitate the merger. Given that all of Credit Suisse’s outstanding CoCos are writedown ones rather than the type that can be converted in to equity, the risk of losses was always there.

Investors had been concerned that a so-called bail-in would result in the AT1s being written down, while senior debt issued by the holding company, Credit Suisse Group, would be converted into equity for the bank. Credit Suisse Group AG had about 78 billion Swiss francs ($84 billion) of holding company debt that includes both types of notes. Bail-in-able notes were devised a few years after CoCos emerged. They do the opposite of a bailout — impose losses rather than bringing in aid.

- Why are some bondholders angry?

In a normal writedown scenario, shareholders are the first to take a hit before AT1 bonds face losses, as Credit Suisse also guided in a presentation to investors earlier this week. However, under the terms of the government brokered deal, Credit Suisse shareholders are set to receive 3 billion francs.

That’s provoked a furious response from some of the AT1 bondholders as it hasn’t accounted for the seniority of CoCos over the lender’s shares in the capital structure. And that’s a big problem for a market that would expect holders to be paid before shareholders.

- How does this impact the wider CoCo market?

The decision to ignore market convention — that shareholders are the first to take a hit before AT1 bonds face losses — could prove to be a huge blow to the $275 billion AT1 market and raises serious doubts about the prospects for other lenders’ CoCos. To compound the misery, it’s also the market’s biggest loss, far eclipsing the one other instance of a lender’s CoCos being wiped out. Back in 2017, junior bondholders of Spanish lender Banco Popular SA suffered an approximately €1.35 billion loss when it was absorbed by Banco Santander SA to avoid a collapse after failing to plug a big capital hole. On that occasion, the equity was also written off, while regulators forcibly wrote off its CoCos. Credit Suisse’s writedown is far bigger and must raise serious questions about what comes next for the market. The huge uncertainty is likely to weigh on lenders’ bond prices right across the ratings spectrum. Uncertainty about the health of several lenders in recent weeks had already weighed on CoCo bond prices, with the average AT1 now indicated at a price of just 82% of face value, one of the steepest discounts on record. Yields on Credit Suisse’s CoCos had surged to distressed levels in recent days.

In Plain English?

To summarise, CoCos, or contingent convertible bonds were invented after 2008’s Financial Crisis and 2012’s European Debt Crisis.

The thinking was that after 2008, if any bank failed again, taxpayers should not be on the hook to bail out the bank and its investors (shareholders and bondholders).

Investors (shareholders and bondholders) invest in a bank and benefit from the upside.

So if anything goes wrong, they should absorb the losses, and not taxpayers.

With that in mind, CoCos were invented.

The key features are:

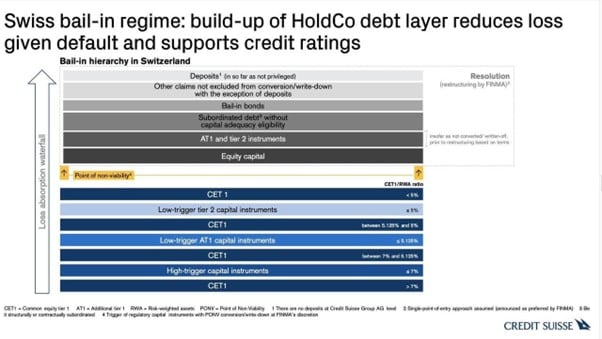

- Cocos are the lowest rung of debt, just above equity. This means that all bond holders will get paid out ahead of Cocos if the bank fails.

But Cocos get paid out ahead of shareholders if the bank fails.

You can see this expressed in chart form below:

- CoCos will fail if certain automatic trigger conditions are fulfilled – for example if the bank’s CET1 ratio (a measure of its balance sheet strength) falls below a certain threshold.

The SNB is fully within their power to do this

Just to be clear, if you go by the letter of the law, the Swiss Central Bank is perfectly within their power to wipe out CoCos.

Credit Suisse’s CET1 ratio last week fell below the trigger requirements under the terms of the CoCo.

This triggered the conditions under the CoCo, which meant the Swiss Central Bank was fully within their power to wipe out CoCos under the bond documents.

But.. you can see why CoCo holders are outraged

The problem though, is that there is a difference between enforcing the letter of the law, and the spirit of the law.

Yes, everybody knew that if you actually read the AT1 Prospectus there were a whole set of conditions under which bondholders would be wiped out.

But it’s not easy to quantify that.

The implicit belief in the market, has always been that – AT1 / CoCo will always rank ahead of shareholders in an insolvency.

This means that if the bank fails, the bankruptcy proceeds will go to bondholders first, and then CoCo holders, and then shareholders.

Rightly or wrongly, this was always the understanding.

And it’s how the CoCos were priced.

You see the problem here – If equity holders get paid out ahead of CoCos, why would anyone bother buying CoCos anymore? You’re taking on higher risk, for a fixed upside. You might as well just go straight into equity.

And therein lies the problem – overnight, nobody knows what the value of AT1 / CoCo debt is worth anymore.

But… this is not an insolvency situation?

To be very technical – you can argue that this is not an “insolvency” situation.

Credit Suisse is not bankrupt, they are being “bought out” by UBS.

Sure yeah… try telling that to the AT1 holders who are looking at a complete loss on capital now.

The fact that the Swiss Central Bank could engineer a situation like this.

Where shareholders get paid out, but AT1 / CoCo is wiped out.

Suddenly meant that there was a precedent for it, and you never know which bank would be next if it ran into difficulties.

So this is very big problem.

And for the record, this is the first time that I know of – where bank shareholders are paid out, but CoCos see complete loss.

This violates everything that people have known / assumed for CoCos for pretty much the past decade.

Why did the SNB do this?

Some of you have asked why did the SNB do this?

No easy answers there, but do note that the Saudi National Bank paid $1.5 billion for a 9.9% stake in Credit Suisse just a few months ago.

Was this done to ensure that the Saudi’s don’t get fully wiped out?

Your guess is as good as mine here.

But just last week Credit Suisse gave a presentation with the chart below, where they reiterated that CoCos will rank ahead of shareholders in an insolvency.

Imagine the outrage from AT1 / CoCo holders.

This will trigger repricing of CoCos across the board

Now remember that the market has been valuing CoCos on the assumption that they would rank ahead of shareholders in an insolvency.

Now overnight, the Swiss Central Bank has thrown that entire assumption out of the window.

For what is a $275 billion AT1 market.

Which immediately triggered a sharp repricing in CoCos across the board.

Here’s Bloomberg:

Bank of East Asia Ltd.’s 5.825% perpetual dollar note slumped 8.6 cents to 79.7 cents, which would be a record decline if maintained through the end of Monday’s trading, according to data compiled by Bloomberg. Kasikornbank Pcl’s 4% perpetual note dropped 4.3 cents to 79.8 cents, also on pace for its largest-ever decline.

DBS Group Holdings Ltd.’s 3.3% perpetual note slumped 2.5 cents to 90.4 cents, set for biggest decrease in 3 years. On average, all Asian banks’ AT1 dollar securities fell at least 1 cent, according to credit traders.

I would expect this volatility to continue to play out in the days / months ahead.

This is a fundamental rewrite of how CoCos work.

Now traders and lawyers will need to pore over the prospectus for every single CoCo to rerun their models.

And short term, investors may sell first and ask questions later.

It could get messy.

BTW – we share commentary on Singapore Investments every week, so do join our Telegram Channel (or Telegram Group), Facebook and Instagram to stay up to date!

I also share great tips on Twitter.

Don’t forget to sign up for our free weekly newsletter too!

[mc4wp_form id=”173″]

Why was the deal done this fast? (no shareholder approval required too)

The second issue, is the speed of this deal.

Remember that Silicon Valley Bank and Signature Bank only failed a week ago.

This sparked a run on Credit Suisse.

Last Wednesday, we had the Swiss Central Bank providing a $50 billion line of credit to Credit Suisse, and committing to provide more if required.

And by Sunday night, we have an announcement on UBS buying out Credit Suisse.

With the regulators coming in to waive shareholder approval requirements (for UBS) due to emergency measures.

The speed of this, is to say the least, very, very quick.

It indicates that even after the $50 billion line of credit was given, the run on Credit Suisse continued.

To such an extent that the SNB felt compelled to have a deal announced by Sunday night.

To prevent a further run on Credit Suisse.

The speed of this, is definitely worrying.

Investors will start asking questions on how bad the Credit Suisse situation must have been for the Swiss regulators to move this quickly. Which does not inspire confidence for the rest of the banking sector.

So… what happens next?

I’m not going to mince words here.

We all expected Credit Suisse to be bailed out eventually. Credit Suisse is a GSIB, so if it fails it would be systemic risk and contagion across the board

But the actual bail out – was incredibly poorly done in my view.

I get that maybe they wanted to ensure the Saudis don’t get completely wiped out.

But wiping out CoCos ahead of equity holders here just upended an entire asset class.

The Swiss have now triggered massive repricing for AT1 / CoCos across the board, which is not helping the current fragility.

And the speed at which the bailout was done, really raises questions on why the Swiss were so eager to get a deal announced before Monday’s reopen.

In any case, here’s UBS’s CDS which has shot up after announcement of the deal.

Market is not a big fan of the deal.

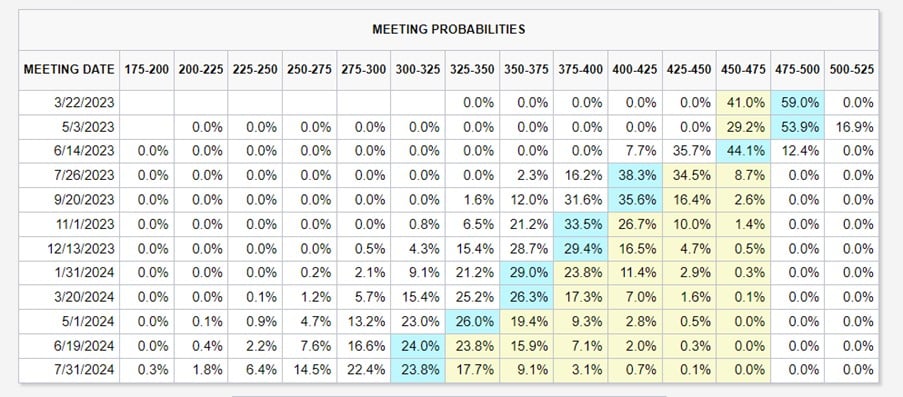

This week’s FOMC just became even more important

This week’s FOMC has now taken on critical importance.

How is Jerome Powell going to respond to this volatility?

You can see latest market pricing below.

Only 59% chance of a 25bps hike at this point.

With the market pricing in at most 1 last rate hike at this point.

Closing Thoughts: Is this a good deal for UBS?

One final note on UBS.

After buying out Credit Suisse, UBS will become one of the biggest banks in Europe.

AUM will grow to 5 trillion, making it one of the largest banks in Europe and globally.

Is this worth it given that UBS will be taking on the black hole that is Credit Suisse?

Only time will tell.

But let’s be realistic, a big part of this deal was brokered by the Swiss to avoid the failure of Credit Suisse (which would have triggered systemic risk as this was a GSIB).

This is a premium Patreon post. I am making it available to all readers in the hopes that this might help you make sense of what is going on.

If you find this useful, do support Financial Horse as a Patreon. You can get regular premium updates just like this, together with my full REIT and stock watchlist.

Sign up here.

As always, this article is written on 20 March 2023 and will not be updated going forward.

If you are keen, my full REIT and stock watchlist (with price targets) is available on Patreon, together with weekly premium macro updates. You can access my full personal portfolio to check out how I am positioned as well.

Trust Bank Account (Partnership between Standard Chartered and NTUC)

Sign up for a Trust Bank Account and get:

- $35 NTUC voucher

- 1.5% base interest on your first $75,000 (up to 2.5%)

- Whole bunch of freebies

Fully SDIC insured as well.

It’s worth it in my view, a lot of freebies for very little effort.

Full review here, or use Promo Code N0D61KGY when you sign up to get the vouchers!

– Get up to USD 500 worth of fractional shares

I did a review on WeBull and I really like this brokerage – Free US Stock, Options and ETF trading, in a very easy to use platform.

I use it for my own trades in fact.

They’re running a promo now with up to USD 500 free fractional shares.

You just need to:

- and fund any amount

- Maintain for 30 days

Looking for a low cost broker to buy US, China or Singapore stocks?

Get a free stock and commission free trading .

Get a free stock and commission free trading with .

Get a free stock and commission free trading with .

Special account opening bonus for Saxo Brokers too (drop email to [email protected] for full steps).

Or for competitive FX and commissions.

Do like and follow our Facebook and Instagram, or join the Telegram Channel. Never miss another post from Financial Horse!

Looking for a comprehensive guide to investing that covers stocks, REITs, bonds, CPF and asset allocation? Check out the FH Complete Guide to Investing.

Or if you’re a more advanced investor, check out the REITs Investing Masterclass, which goes in-depth into REITs investing – everything from how much REITs to own, which economic conditions to buy REITs, how to pick REITs etc.

Want to learn everything there is to know about stocks? Check out our Stocks Masterclass – learn how to pick growth and dividend stocks, how to position size, when to buy stocks, how to use options to supercharge returns, and more!

All are THE best quality investment courses available to Singapore investors out there!

Hi Horse, great article, thanks.

Thanks! Hope it helps. 🙂

How would you execute a contrarian trade on AT1s as a retail investor? I was looking at AT1 LN ETF by invesco. Can’t find any with Asia Bank AT1 exposure, which I would prefer as these are arguably lower risk than Europe / US.

Contrarian trade would be to buy AT1s at a high enough yield I suppose. But it is not straightforward to evaluate the risk associated with AT1s after the events of the past week.

As a retail investor, you may also not be able to buy AT1s in enough size + number to achieve meaningful diversification.