So… Endowus has cut their fees for their Fund Smart Platform from 0.6% (cash) / 0.4% (CPF & SRS) to 0.3% p.a for single fund portfolios.

Does this make them the better choice vs Syfe vs StashAway vs FSMOne?

What does this mean for investors who are already buying unit trusts / mutual funds across other platforms?

Let’s find out.

Note: This post was sponsored by Endowus. All views and opinions expressed in this post are from Financial Horse.

Basics: What is Endowus Fund Smart

Endowus has 2 main product offerings:

- Advised portfolio solutions – The usual roboadvisor offering. You input your age, your investment amount, your risk appetite, and your goals. And Endowus will suggest a portfolio for you. The fees start from 0.6% p.a. (cash) / 0.4% p.a. (CPF & SRS).

- Fund Smart – For investors looking to complement their overall portfolio with thematic / sector specific unit trusts. You can buy these funds listed in the Endowus Fund Smart page. Think of it like a marketplace for funds, with fees being reduced to 0.3% p.a. for cash, CPF and SRS for single fund portfolios.

For both product offerings, you can buy using cash, CPF and SRS.

This is actually a main highlight of Endowus – because no other SG-based robo advisor allows you to invest all 3 of the core Singaporean wealth pillars (cash, CPF, SRS) in one platform digitally.

Endowus is the only allowed digital advisor that can currently do that.

Endowus is also the first to give exclusive access to the Infinity S&P 500 and the Infinity Global Stock Index Fund for CPF because they rebate all trailer fees (kickback commissions paid by fund managers) to clients, which reduces the total expense ratio to a level acceptable for CPF funds.

Endowus Fund Smart Fee Reduction Explained

x

x

The change this time is that Endowus has reduced the fees for their Fund Smart Platform from the original 0.6% (cash) / 0.4% (CPF & SRS) to 0.3% p.a for single funds.

Very simple and very clean.

Implications of the Fee Reduction

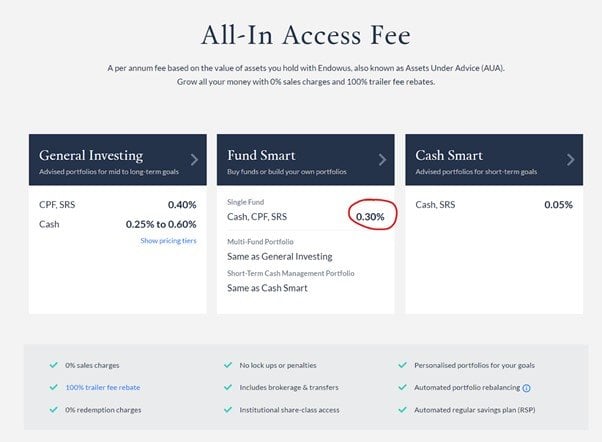

Endowus has a great table that lists all the funds they have on their platform and sets out all the fees you pay.

This is one of the main highlights of Endowus – their transparency around fees.

Every fee you pay is displayed very clearly to you when you create the portfolio.

I’ve extracted some information from the table below:

![]()

The box in red shows how much you’re saving, by investing with Endowus.

In other words – as long as the column circled in red is higher than 0.3%, you’ll save money by investing with Endowus with a single fund portfolio.

As you can see, it generally varies from fund to fund, but by and large themajority of funds will be cheaper at Endowus even after the 0.3% platform fee.

How does Endowus give you cheaper fees?

The way Endowus cuts the fees is by (1) giving you access to the institutional fee class, and (2) by giving you all trailer fee rebates they receive from the fund manager.

Institutional fee class means you get the fees that institutional investors would pay.

Trailer fee rebates are like a “referral fee” that financial institutions get for referring you to the fund manager. While most other platforms like FSMOne will keep this trailer fee, Endowus will rebate it all back to you.

If you’re shopping around for a fund, it’s worth checking the price on Endowus here before you buy – there’s a good chance it’s lower in cost on Endowus.

Compared vs other platforms

To illustrate this – I took a fund from UOB as an example, United Asia Pacific Real Estate Income Fund.

On one platform, the annual expense ratio is 2.38%.

At Endowus, the all-in cost is 1.39% + 0.3%, totalling 1.69%.

Overall, you would have saved 0.69% in fees right there.

Endowus Q&A on Fund Smart

Endowus very kindly offered to answer any questions I had about Fund Smart, so I threw them a couple:

- Fund Smart with the 0.3% platform fee included means that it may be more expensive than some other platforms without a platform fee. How should your clients reconcile this – should we check each fund on Endowus vs Dollardex/POEMs before buying?

Endowus: Cost sensitive clients may be inclined to invest in funds based on getting it at the lowest cost possible, and we very transparently provide the information for them to make that decision.

We are by far the cheapest platform for the majority of the funds that are available on Fund Smart with the all-in-one fee of 0.30% p.a., and it is in our clients’ interest to keep all their investments consolidated on one platform for ease of management.

- Fund Smart has low fees currently to build market share. As investors, how do we know that Endowus will not raise fees down the road once you build a dominant market position?

Endowus: We are the first within the unit trust investing platform space to offer trailer fee rebates, and are the first to lower our platform fees.

Our clients and anyone interested in starting an account with us should know that we are committed to always being aligned to our clients interest because of our commitment to being transparent and being fee-only.

Other platforms and traditional advisors have been profiting from trailer fees for many years, without rebating cost efficiencies from the scale of their business to clients, while negotiating for bigger trailer fees from the fund managers.

As a digital platform, we are confident that our business can scale more efficiently from an operational angle, and that this 0.30% p.a. access fee for single fund portfolios will stay as we continue to deliver on other products on the platform that will support our clients’ growth.

- Fund Smart is very complex, with a ton of funds to choose from. How do you suggest investors integrate Fund Smart into their portfolio?

Endowus: As it is, we have already down-selected a curated list of investable funds for our clients, prioritising the best-in-class funds in the entire investable universe of more than 1,000 funds.

Clients should look at our investment fund list and choose the investment strategies that suit how they want to build a satellite portfolio, and then invest in funds based on that.

- Does your core management team use Fund Smart or the Advised Portfolio? Why?

Endowus: We mainly invest in the Advised Portfolios, be it Cash Smart, ESG portfolios or core advised portfolios.

We believe that successful investing is highly dependent on having a long term view on the market, and being diversified is critical to that.

The advised portfolios work best for that purpose.

Choosing between ETFs vs Active Funds

The big question for investors would be how to decide between using a passive ETF, and using an active fund via Endowus.

And the way I see it is this:

- ETFs are best for efficient markets like US – If I’m investing in the US, the S&P500 or NASDAQ100 are very efficient, not much need for an active manager

- Active Funds (Endowus Fund Smart) are best for inefficient markets If I’m investing in fixed income products, Emerging Markets, ESG, where it is far harder to index, then there is real value add from an active manager.

And that’s exactly how I would use Endowus Fund Smart – for more inefficient markets like bonds (fixed income), emerging markets, and Environmental, Social, Governance (ESG) investing.

How would I invest with Endowus Fund Smart?

Now imagine for a moment that I didn’t love investing so much.

Imagine that I just want to live my life in peace and quiet, and automate my investments into a buy and forget portfolio.

How would I do it, and how would Endowus Fund Smart fit into my portfolio?

How would I fit Endowus Fund Smart into my portfolio?

This was what I came up with:

- ETFs: S&P500, NASDAQ100 (QQQ), MSCI China (2801)

- Funds: ESG Fund, and a Bond Fund

- Cash: Money Market Fund

Here’s how I would do it.

ETFs

ETFs for the S&P500, NASDAQ100 are very efficient, very cheap and have fantastic liquidity.

I can’t use SRS or CPF for these though, so I would buy with cash.

VUSD for S&P500 (superior withholding tax treatment vs SPY), and QQQ or VGT for NASDAQ tech exposure.

MSCI China because that is what I found to be the best ETF for broad based exposure to China for now.

Funds

For active funds, I would get ESG funds and Bond (fixed income) exposure

Both are not easy to get exposure via ETFs and best done via an active manager, hence the choice to go with active funds via Endowus Fund Smart, rather than an ETF.

Cash

The rates on bank accounts are absolutely horrible these days.

So apart from cash I need to access on a moment’s notice, any cash that can be locked up for a week or two I’ll probably put into a money market fund via Endowus.

Options are:

If I’m feeling adventurous, I might even use Cash Smart Ultra for an even higher yield on the cash.

Which Bond Fund to use?

The Bond Fund depends on my risk profile.

If I’m older and more conservative, it’ll go into a developed market bond fund, such as the PIMCO Income Fund.

If my risk appetite is higher, I might use an emerging market bond fund, obtained through the filters on Endowus Fund Smart.

If my risk appetite is really high, I’ll probably skip the Bond Fund entirely and put it all into an ESG Fund.

The great thing about Endowus is that all the funds on Endowus Fund Smart are pre-curated by the Endowus CIO (ex Morgan Stanley) and his team.

Of course, this doesn’t mean you can skip your own due diligence. But in any case, all the fund docs are very easily available on Endowus for your review.

Which ESG Fund to use?

Likewise with the ESG funds.

All pre-selected, and all big names from the likes of PIMCO, JP Morgan, Schroders etc.

Case Study of how to use Fund Smart to assemble your ideal portfolio

Expanding on the basic framework above, here are some case studies on how various types of investor can utilize Endowus Fund Smart

Young investor growing wealth

You may choose to skip the bond fund entirely, and go with pure equities.

You probably want to start off with a very diversified equity fund to get broad access to the markets and dollar cost average in.

Some of the funds that they may invest in include:

- Dimensional World Equity Fund, basically the VWRA equivalent with a factor tilt

- Dimensional Core Equity Fund basically the IWDA equivalent with a factor tilt

Middle-aged investor saving for kids education

Middle-aged investors who have big upcoming expenses may want to be slightly more conservative, and have bigger allocation to bonds. They may also be willing to try out more thematic funds given they have better experience with markets:

Thematics Subscription Economy Fund

Retiree looking to preserve wealth

For retirees, they can’t afford to take much risk with their money, hence a big chunk has to go into bonds, and developed market, short duration bonds at that.

You can use the filters to help you find the funds you need:

That’s the beauty of Endowus Fund Smart.

Regardless of what you already have (or don’t have) in your portfolio, you can then locate the fund from Endowus Fund Smart to round up your portfolio.

FH x Endowus Referral Code

When you create your account from this Endowus Referral Code, you will get S$10,000 managed free for 6 months ($20 equivalent).

If you’re keen to try out Endowus Fund Smart, don’t forget to use it!

Closing Thoughts – How does Fund Smart fit into the ecosystem after this fee reduction?

With this change, Endowus took a great platform to buy funds, and made it even better.

Previously the access fee charges was 0.6% / 0.4%, now it is 0.3%.

For those of us who plan to use active funds to complement our portfolio, whether it’s for ESG or Bonds or Emerging Markets (which are not efficient to ETF), Endowus Fund Smart is a great option to check out after this.

Love to hear your views!

Note: This post was sponsored by Endowus. All views and opinions expressed in this post are from Financial Horse.

The content here is for informational purposes only and should NOT be taken as legal, business, tax, or financial investment advice. It does NOT constitute an offer or solicitation to purchase any investment or a recommendation to buy or sell a security. In fact, the content is not directed to any investor or potential investor and may not be used to evaluate or make any investment. If you are in doubt as to the action you should take, please consult your stock broker or financial advisor.

We do not undertake or represent to any person to ensure the correctness and completeness of any information or data, nor to update them for currency with the passage of time. Our analyses, opinions and views are subject to change without notice, and we do not undertake or represent to any person with regard to their correctness, completeness or currency. Past performance may not be an accurate or complete indicator of, and does not guarantee, future performance. This advertisement is not reviewed by Monetary Authority of Singapore.

why is it > 0.3% to save money by investing with Endowus?

“The box in red shows how much you’re saving, by investing with Endowus.

In other words – as long as the column circled in red is higher than 0.3%, you’ll save money by investing with Endowus with a single fund portfolio.”

Because the platform fee for Endowus is 0.3%. So to make it worthwhile, the fees need to be 0.3% cheaper on Endowus vs other platforms. It probably is for most of the funds though.

You mentioned that we can’t use SRS or ETF for S&P500 ETF which I agree, but could this be replaced via a fund instead such as Lionglobal Infinity US500 offered in Endowus Fundsmart to utilize the SRS/CPF?

Any thoughts on what the downside could be other than higher fees in funds vs SPY/VOO ETF which have very low expense ratios?

Yup – the downsides are higher fees and *slightly* worse liquidity.

It’s definitely an option, but I guess my point is to look at the portfolio holistically. If you need to split your portfolio between US, China and Singapore – one option is to use the cash portion to buy US/China ETFs, then use the CPF/SRS portion to buy Singapore stocks (which are permitted).

But of course this depends on individual asset allocation. If your cash is already maxxed out then year I agree something like the Lionglobal Infinity US500 could be a good alternative. 🙂

i see..

what are your thoughts in using CPF for their fundsmart infinity SP500? instead of advised portfolio.

The answer needs to tie into your existing portfolio, and what you already own.

CPF investments should be viewed holistically in that way. So if you use the advised portfolio, you need to decide how it fits in, as it may overlap with what you already own.

Hi FH, sorry I think I posted the question on the comments section of the wrong article. Once again, thank you for your article and your insights!

I was just wondering if it would be cheaper to use Endowus Fund Smart (0.3%) to replicate the Dimensional Funds allocation by MoneyOwl (0.5/0.6%).

Haha no worries.

Reply below as well:

Hi Jon,

That’s a really good question. I haven’t looked too closely into this, but off the top of my head that would be definitely possible actually. 🙂

The whole point of Fund Smart is that it allows you full control to replicate any portfolio you want.

Do you have real life experience of Endowus providing trailer rebates for SRS and CPF? Is it in the form of additional units in Dec month only? Thanks.

Let me check with Endowus on this for their reply. 🙂

Reply from Endowus: Trailer rebates will be given once we received from UOB Kay Hian, normally it will be distributed to 6 months from the quarter end.