The thing about being a financial blogger, is that through reader questions, you can get a good idea what the flavour of the month trade is. And the past month or two, without a doubt, it has been the China trade. The most common questions I have received are (1) Is xx China stock worth buying at the current price, and (2) Which ETF should I buy if I want exposure to China ETFs. The second question is a really interesting one for me, because personally I think the long term prospects of China are out of this world. I have little doubt that much like how the 19th century was about the UK, and how the 20th century was about the US, the 21st century will be shaped by China.

Basics: What are the main China ETFs

China A shares (those denominated in RMB and traded onshore on the Shanghai/Shenzhen Exchange) are typically hard for foreign investors to get into due to tight capital controls and a heavily controlled onshore environment. I have little doubt that China will eventually open up the onshore capital markets, but unfortunately, that hasn’t happened yet. Which means that for offshore investors like us, our best bet is to use Hong Kong listed stocks of China companies. These boast much better liquidity and less stringent capital controls (basically none).

There are 2 main ETFs to do this:

- iShares FTSE/Xinhua China 25 Index (NYSEARCA: FXI) – FXI is a US listed ETF comprised of Hong Kong listed stocks of the largest China companies. With about US$4.5 billion AUM, it’s the largest pure China ETF in the world. The main drawback with the FXI though, is its high expense ratio of 0.74%, which is uncharacteristically high in today’s age of race to the bottom ETF pricing.

- Tracker Fund of Hong Kong (SEHK: 2800) – The Tracker Fund of Hong Kong is an ETF that tracks the Hang Seng Index. That’s basically all there is to it. It has about US$10 billion AUM so it’s the largest ETF tracking the Hang Seng. Expense ratio is a cool 0.09%, which is more like it.

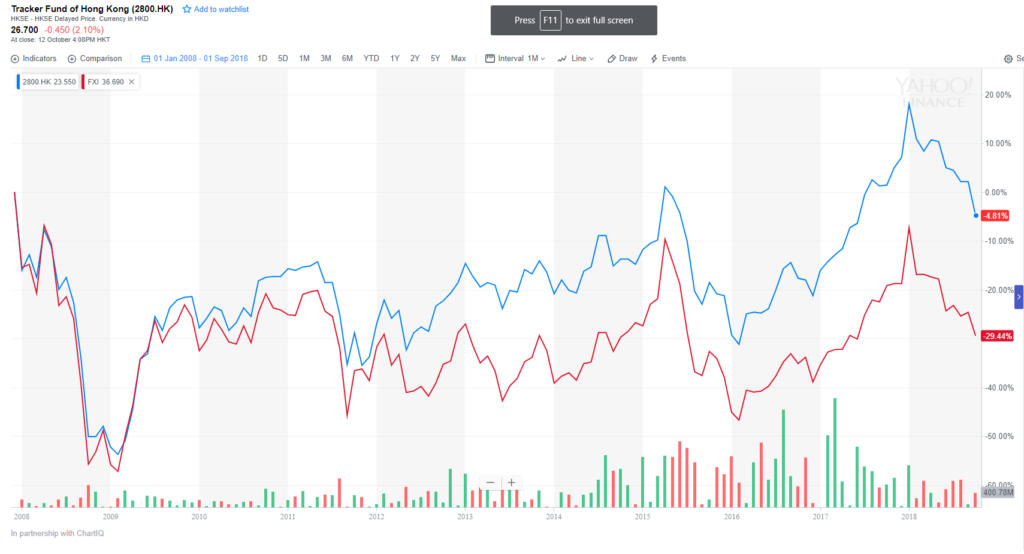

I’ll focus on the Hang Seng Index in this article, because it is my preferred way to play the Chinese market. I really like the much lower expense ratio (don’t forget if you buy the FXI, you’re basically betting that it will outperform by at least 0.65% a year, otherwise you’re just paying fees), and in the near term at least, I think the Hong Kong exposure will add some stability to the index. For reference, I’ve plotted the Tracker Fund of Hong Kong (Blue) against the FXI (Red) below, and you can see the disparity in performance. Because the FXI is 100% exposure to onshore China, the losses (and gains) will be magnified based on China’s performance.

Note: A reader has very kindly pointed out that not all big China companies list on the Hang Seng, especially those domestically-facing ones like Kweichou moutai, Midea grp, China minsheng bank. These can be accessed via an ETF that gives pure exposure to China A50 Index and CSI 300 index, such as HKEX 2822 and 3188.

Do note however, that the expense ratio for these ETFs will be higher (typically about 1%), due to the additional costs associated with the ETF investing in China A shares.

Historical Returns

I’ve plotted the long term returns of the Hang Seng (Blue) against the S&P500 (Red) and the STI (Green) below. Quick note, these charts don’t take into account forex movements and dividends, so the STI will perform a lot better than it looks in this chart.

Which index has superior performance depends greatly on the time period chosen. For example, the S&P500 had insane returns from 2008 to 2018, while the Hang Seng had some out of this world returns from 2002 to 2007. And that’s actually a good thing, because the whole point of building up global stock portfolio is that if one country’s economy is performing poorly, you’re actually well diversified and your returns from another index can juice up returns in your portfolio, smoothing out the losses. For example, if you were pure Asia stocks you would have been hit badly the past 6 months, but if you had mixed it up with some US exposure, you’re going to be sitting much happier right now.

For this arbitrary 20 year period that I picked, the Hang Seng’s performance closely matched that of the S&P500, although you’ll notice that there were many times during this 20 year period when this was not the case.

Diversification

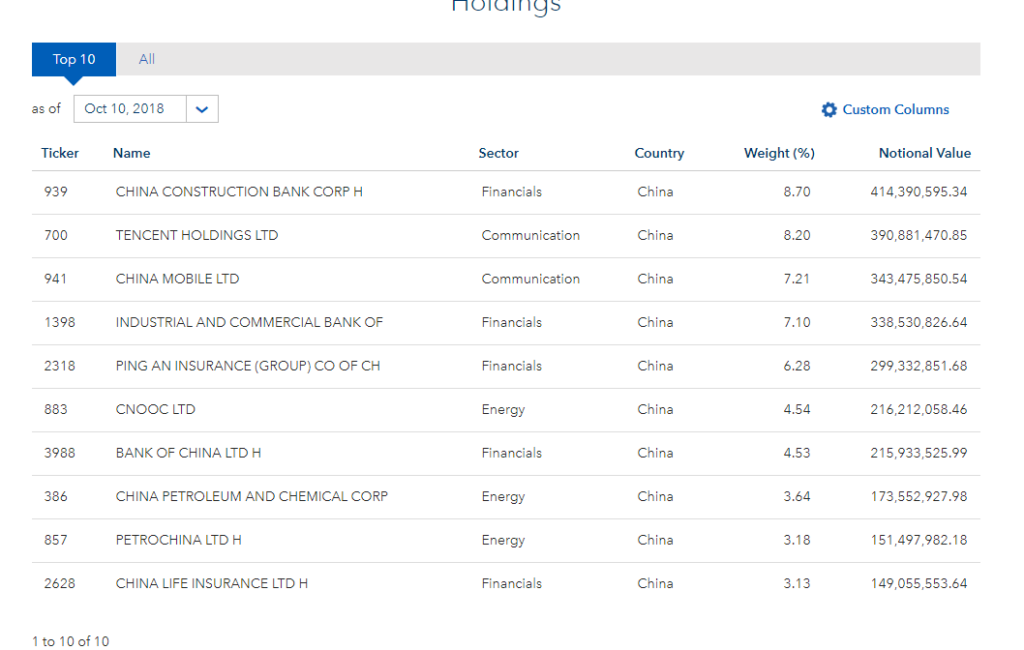

I’ve set out the top 10 constituents of the Hang Seng and FXI below.

Hang Seng

| Company | Sector | Weight |

| HSBC Holdings | Financials | 10.52% |

| Tencent Holdings (P Chip) | Information Technology | 9.28% |

| AIA Group Ltd. | Financials | 8.84% |

| China Construction Bank (H) | Financials | 7.92% |

| China Mobile (Red Chip) | Telecommunications | 5.60% |

| Ping An Insurance (H) | Financials | 4.84% |

| Industrial and Commercial Bank of China (H) | Financials | 4.56% |

| Bank of China (H) | Financials | 3.08% |

| CNOOC (Red Chip) | Energy | 3.05% |

| Hong Kong Exchanges & Clearing | Financials | 2.90% |

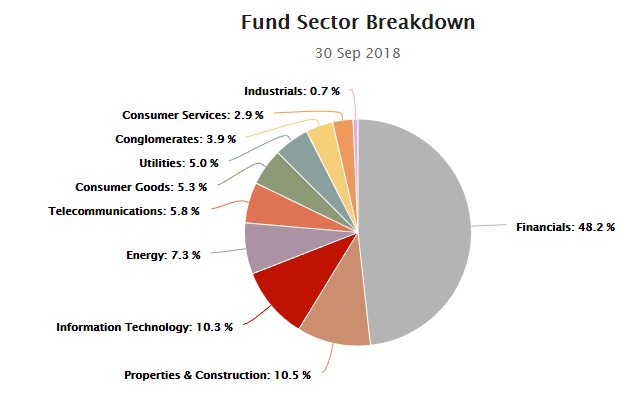

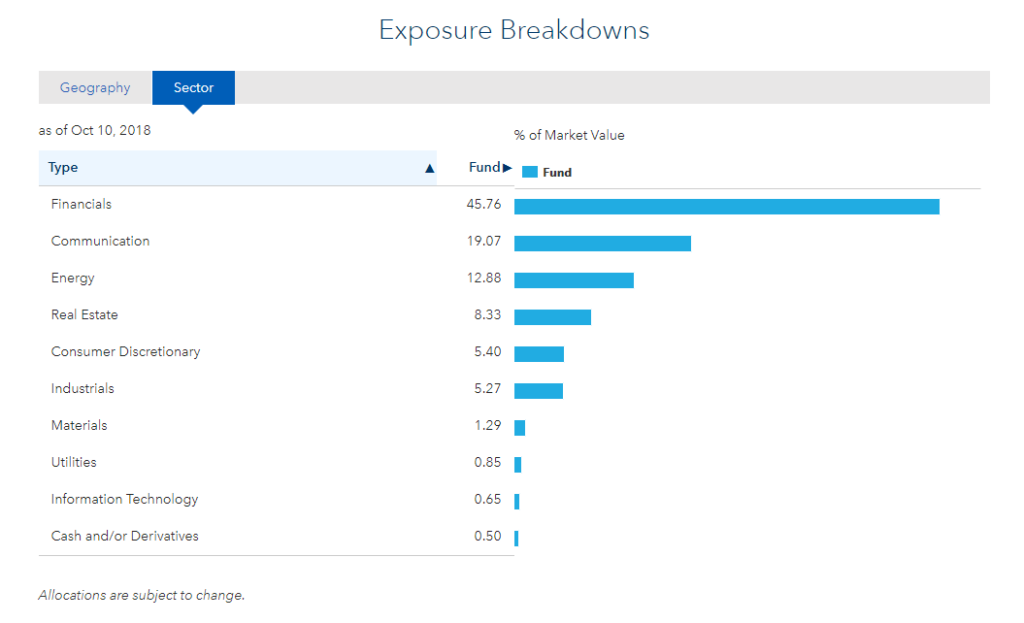

Sector diversification of both ETFs are below as well:

Hang Seng

FXI

Couple of observations:

- Dominated by Banks – Much like the STI, both ETFs are dominated by financials, which make up close to 50% of the ETF. It’s not necessarily a bad thing, because with a country as big as China, and which is still in the early phases of development, banks are a great way to gain broad exposure to the economy. But it’s worth noting from a portfolio diversification perspective.

- Overlaps between the two – The top 10 constituents of the Hang Seng and FXI have a fair bit of overlap, namely, Tencent Holdings, China Construction Bank, China Mobile, ICBC, Ping An, ICBC, BOOC etc. With the Hang Seng, you get additional exposure to Hong Kong companies such as HSBC, AIA etc, which can be both a good or bad thing, depending on how you look at it. For current purposes, it’s quite clear that both ETFs will get you exposure to the biggest names in China, with the FXI providing more concentrated exposure.

Currency movements

The Hang Seng trades in HKD, while the FXI trades in USD. The HKD is pegged to the USD. I have my suspicions on whether this peg will be removed in the future, but in the near term, I think it is unlikely, as a move like that would spark turmoil on global currency markets.

In any case, it’s important to note that with either ETF, you’re still getting underlying exposure to China companies listed on the Hong Kong exchange. In other words, your underlying earnings are denominated in RMB. So don’t be fooled by the currency your ETF is denominated in. You’re basically betting on Chinese companies that earn RMB onshore in China. And you will be exposed to RMB price movement.

China exposure

You will also be getting exposure to the Chinese economy (that’s the whole point of this trade right?). Now that’s a tricky topic that I could write a 1000 page thesis on, but still get completely wrong. So do take my analysis with a healthy pinch of salt.

My base case assumption, is that China will be a global superpower in the 21st century. China has 1.4 billion people, which to put that in perspective, is about 400 million more people than the entire US, EU and Japan put together. They have a 300 million strong middle class currently that will expand to more than 550 million by 2022. That’s more middle class consumers that the entire population of the US. And as we all know, Chinese people are ridiculously hardworking and driven. Take a nation of kiasu Singaporeans, dial up the kiasuness by 2 notches, and squeeze the population of 230 Singapores into China, and you get an idea of how dynamic and vibrant the Chinese economy will be when they hit their stride. If you’ve been to any tier 1 city recently, you’ll be able to witness first-hand the rapid transformation China underwent the past 5 or 10 years. I remember how 10 years ago we were talking about Shanghai learning from Singapore – these days I don’t even recognise the technology being used over there.

The problem though, is that just because China will be a superpower in 2050, does not tell us how that will happen. The US is the world’s premier economy today, yet it still went through a depression in the 1930, and rampant inflation in the 1970s. So as always, the devil is in the details. The current macro climate doesn’t look amazing for a big China bet. It’s always hard to predict what Trump is going to do, but it’s starting to look like this trade war is part of a broader plan to control the ascendance of the Chinese economy. In any case, the trade war is in full swing, and my personal suspicion is that it’s going to get worse before it gets better.

In the near term, there are 3 possible scenarios:

- China gives in and ends the trade war – Everybody I have spoken to on this that knows anything about China, tells me that this is an absolutely impossibility. There is no way in hell that China gives in to Trump. That would be an unprecedented loss of face and is unacceptable for China both domestically and internationally. I completely agree with them. In fact, even JP Morgan agrees with this analysis, which is why the base case they project is for US tariffs on all Chinese exports to the US in 2019 (China exports about 500 billion a year to US, current tariffs are on 250 billion of those exports).

- RMB Devaluation – Given that a full blown trade war is now the base case, the analysis will shift to how China addresses this domestically. The most natural conclusion, is a RMB devaluation. A devaluation of the RMB against the USD will offset the impact of the tariffs levied, boosting competitiveness of Chinese exports. In fact, in 2018 the RMB “depreciated” roughly 10% against the USD, which basically offset the entirety of the US tariffs levied. Given that the Feds are on a rate hike cycle, the PBOC need not even do anything, they could just let the Feds do the work for them. My suspicion is that this is the most likely path forward in 2019, which would eventually result in the RMB breaking the psychological 7.0 barrier against the USD.

- Domestic easing – The onshore credit markets are having a rough time at the moment. China has been trying to clamp down on shadow banking for a while as part of a broader deleveraging move. Coupled with the trade war, this has translated into tighter financial conditions onshore. You can see the manifestations of these in the P2P meltdown, and the recent concerns over property valuations. I suspect the most natural move is that Beijing will ease up on financial conditions in 2019, to prevent the proverbial “hard landing” that everyone keeps talking about. We will probably see a combination of scenarios 2 and 3 going forward.

So where does this leave us? It seems that in the long term, China will be the opportunity of our lifetimes. But in the short term, prospects are a bit murky. I can’t speak for anyone else, but for me, I’m keeping a close eye on the situation. I think a good buying opportunity may present itself some time in 2019, possibly when the devaluation of the RMB happens.

Closing Thoughts

If you want to bet on the China economy, your best bet is either the Hang Seng Index (using the Tracker Fund of Hong Kong) or the iShares FTSE/Xinhua China 25 Index (FXI). Both offer exposure to the largest China companies listed on the Hong Kong Exchange, which for foreign investors, is probably the best way to play this trade. If you want some Hong Kong exposure (and lower fees) go with the Hang Seng. If you want pure China exposure, go with the FXI. There’s no right or wrong answer here, it really depends on your portfolio allocation, because some people may already have existing HK exposure so they prefer something that’s all-in on China.

The bigger question though, is where are China stocks going to go in the next 2 years, and the next 10 years. In investing, the journey matters as much as the outcome. Just because an investment will have 500% returns in 10 years, does not mean it cannot drop 80% over the next 2 years. And in such a situation, most investors are going to sell. Personally for me, I don’t think this is the right time yet, I want to see how the trade war plays out a bit more before committing to this investment.

But as always, don’t just follow my advice blindly, think about the arguments I presented, think about whether you agree with them, and arrive at your own reasoned conclusion. You’ll be a better investor for it.

Till next time, Financial Horse, signing out!

Financial Horse has a set of 7 Commandments for Successful Investing, that I ask myself before making every investment, and that I will never break regardless of the situation. Enter your email below to receive a copy in your inbox!

[mc4wp_form id=”173″]

Enjoyed this article? Like our Facebook Page for more great articles, or join the Facebook Group to continue the discussion!

Not all china big companies list in HK especially those domestically-facing ones like kweichou moutai, Midea grp, China minsheng bank..

But they can be accessed via etf that gives pire exposure to China A50 Index and CSI 300 index:

iShares FTSE A50 China Index ETF (HKEX:2823)

iShares Core CSI 300 Index ETF (HKEX:2846)

That’s a great point, thanks for pointing this out. I’ll update the post accordingly. Cheers.

Both 2823 and 2846 are synthetic ETF which do not invest directly in the component stocks. They were popular long time ago before foreign exchange investors were allowed to invest in China stock markets. Nowadays with the hongkong shanghai stock connect, there are better options i.e. physical ETFs such as 2822 and 3188.

That’s for pointing this out! You are absolutely right, my apologies for missing this out. Have updated the article accordingly.

FH? What are your thoughts on KWEB? I find that it has lots of potential for big capital gains goiung forward too

Hi James!

I had a quick look, KWEB looks like a very specialised bet on China software companies listed overseas. If you are bullish on that sector, by all means go ahead. Personally I think something like that would be very volatile going forwrad (ie. you’re either going to make 20% capital gains, or 20% capital loss). I prefer something more diversified like the FXI, but really, that’s just my investing style 🙂

FH, congrats as Hang Seng has gone up by 30+ % since Oct 2018. I am new to ETF and keen to find out more. How is this different from investing directly on HS indices ? Are we allowed to have Stop Loss on ETF like Indices ? Also, I like to know how would the China tech fund impact on both HSI and China A50 ?https://www.channelnewsasia.com/news/technology/china-fund-managers-rush-to-capitalise-on-shanghai-s-new-tech-board-11308856

Hi there! It’s actually just a different way to invest in the HS indices. For example if you’re investing in Singapore, you can just buy the STI ETF to gain broad exposure to all 30 of the STI constituents, or you can just buy individual counters. I find ETFs a helpful way to get broad exposure to an index.

Absolutely, you can use stop losses on ETFs, but the exact mechanics depends on your stock broker.

The last question is a tricky one, and it’s impossible to know the impact for certain. In the short term anything can happen, but if you’re investing in the long term, the only thing that really matters is earnings and economic growth, and you can tune out the short term noise.

hi FH

like to know how to buy this tracker fund ? My broker advised not to use CFD to trade if i want to hold it for long term. What special broker are you using ? thanks

Hi! It’s an ETF listed on the Hang Seng, you can just buy their shares directly if you have access to HK shares. You can check out the link here for more info: https://en.wikipedia.org/wiki/Tracker_Fund_of_Hong_Kong

https://www.trahk.com.hk/eng/

What are yr thoughts about investing in China companies in Africa?

there was a surge of 2-3% for china index including HSI yesterday although HK was not closed for trading. I was trading HSI futures and made some profits. I expect this tracker fund to gap up today when it opens and likely to close the gap as it does yesterday with the future. Am I right to say that there is a time gap in the price action between futures and this ETF ? And if so, how can we take advantage of this time difference ? Your enlightment is much appreciated.

Hi FH, may I check if I buy HK:2800 via DBS Vickers, is the dividend paid out in HKD less a 1% fee? Thanks

Yes it is less the dividend handling fee and FX spread. I can’t seem to find how much they charge for dividend handline though.