I’m still getting quite a few questions on buying T-Bills with CPF-OA, so I wanted to pen this piece to get the information out there.

The general thinking here, is that CPF-OA pays 2.50% interest rates.

Whereas you’re looking at close to 4.00% on the T-Bills.

T-Bills are backed by the Singapore Government and pretty much risk free, so buying T-Bills with CPF-OA is a no brainer?

Where the catch you say?

There’s no free lunch in this world?

What are the risks with buying T-Bills with CPF-OA?

The 2 key risks are:

- Will CPF-OA interest rates go up?

- Not losing more CPF-OA interest than you need to

Will CPF-OA interest rates go up?

If you buy 4.00% T-Bills, and CPF-OA interest rates get increased to 4.5%, you will for obvious reasons look very silly.

Throw in the 1 month lost CPF-OA and you could lose quite a bit.

How likely is this?

Manpower Minister Tan See Leng was asked in parliament recently on whether CPF-OA interest rates will be increased moving forward.

This was his response:

“On Tuesday, Manpower Minister Tan See Leng responded to a parliamentary question on whether there are plans to incentivise CPF members with high OA savings to tap alternative options for higher interest earnings.

He said they could put their CPF funds into short-term Singapore Government Securities (SGS) products like T-bills.

He added that OCBC and UOB customers will be able to use their CPF savings to apply for T-bills online by the first quarter of 2023, after DBS Bank first allowed customers to do so in late January.

OCBC confirmed to The Straits Times on Tuesday evening that its customers will be able to use their mobile apps and Internet banking accounts to invest their OA and Special Account (SA) funds in T-bills from March.”

So… read into that what you will on whether CPF-OA interest rates will go up.

Although sometimes, a bird in hand is worth two in the bush… if you know what I mean ????

Not losing more CPF-OA interest than you need to

The way that CPF works, is that if you take money out of CPF-OA – you will lose CPF-OA interest for that entire month.

Regardless of whether you deduct the money on the 1st of the month, or the last day of the month.

So generally speaking, to avoid losing more CPF-OA interest than you need to, you want to buy T-Bills towards the start of the month.

The 16 March 2023 T-Bills are only issued on 21 March 2023, and mature on 19 Sep 2023.

This means you’ll lose the CPF-OA interest for the whole month of March, and only get the moneys back on 19 Sep 2023.

That’s not a lot of time to roll over the CPFIS money into new investments, whether its new T-Bills or back to CPF-OA.

So timing wise, this may not be ideal.

More kiasu CPF-OA investors may want to opt for the 30 March 2023 Auction instead – where the issue date is 4th April.

I’ve also been getting some questions on this.

So just to clarify the timings of the fund flow (based on my personal experience with DBS):

- CPF-OA Fund are deducted from your CPF-OA 1 day after the T-Bills issue date

- Funds are redeposited into your CPFIS Account at 6pm on the maturity date

- It takes 3 working days to transfer funds from CPFIS to CPF-OA (if done online)

Do note the above may be subject to change, and may differ from bank to bank.

So do confirm with your agent bank to be sure.

Is it worth it to buy T-Bills with CPF-OA?

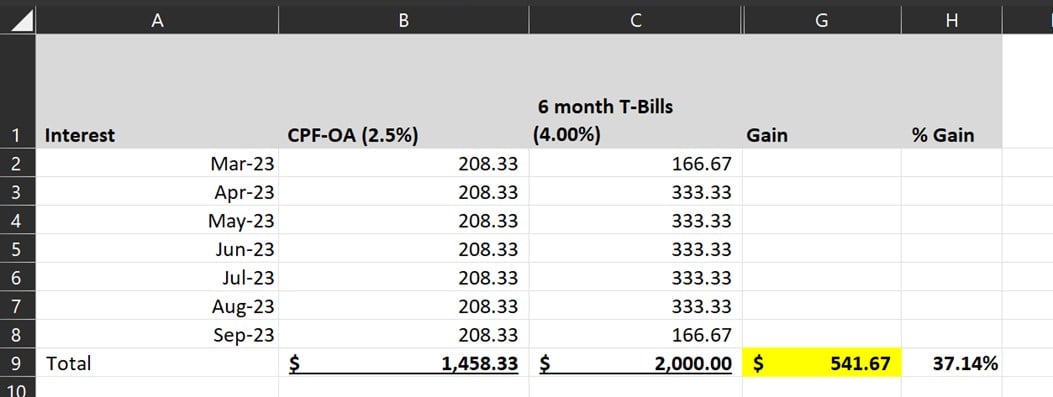

Assuming:

- You buy $100,000 of T-Bills with CPF-OA

- T-Bills are issued at 4.00%

Then you make an extra $541.67 by buying the T-Bills, instead of leaving the money in CPF-OA.

This is just for 6 months, so over a 12 month period the amount will close to double (subject to where interest rates are in 6 months).

Is this worth it?

I mean only you can decide for yourself.

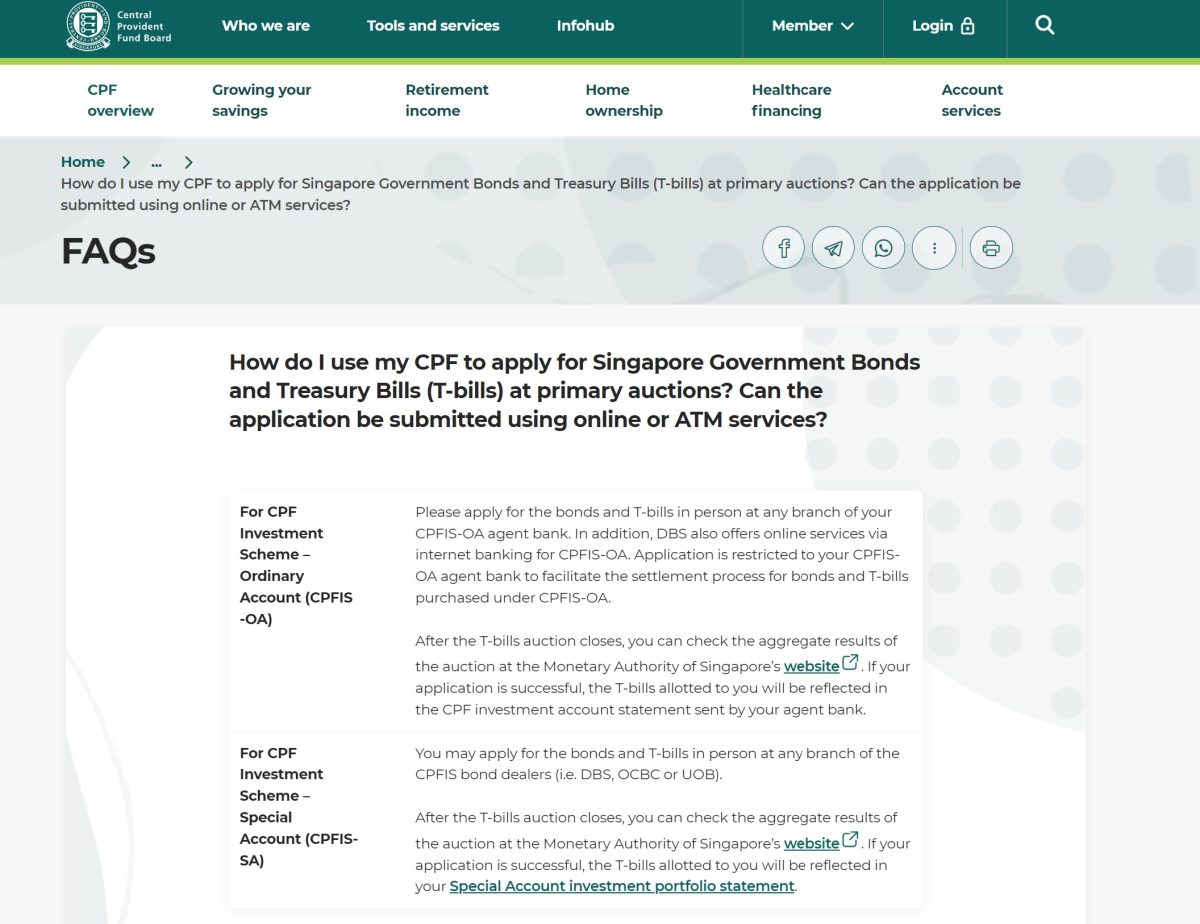

But if your CPFIS account is with DBS, you can apply for T-Bills online, which takes no more than a couple of minutes if you know what you’re doing.

Pretty much a no brainer once you can do it online in my view, and I got it done for my own CPF-OA once online applications were available.

OCBC, UOB customers can tap CPF funds to buy T-bills online from Mar 31 and Apr 22 respectively

Unfortunately, if your CPFIS account is held with OCBC or UOB, you cannot buy T-Bills online just yet.

You still have to go down physically to a bank branch for now.

However, per the Business Times, OCBC and UOB customers will be able to do so from 31 March (OCBC) and 22 April (UOB).

Great news for those with your CPFIS account at OCBC or UOB.

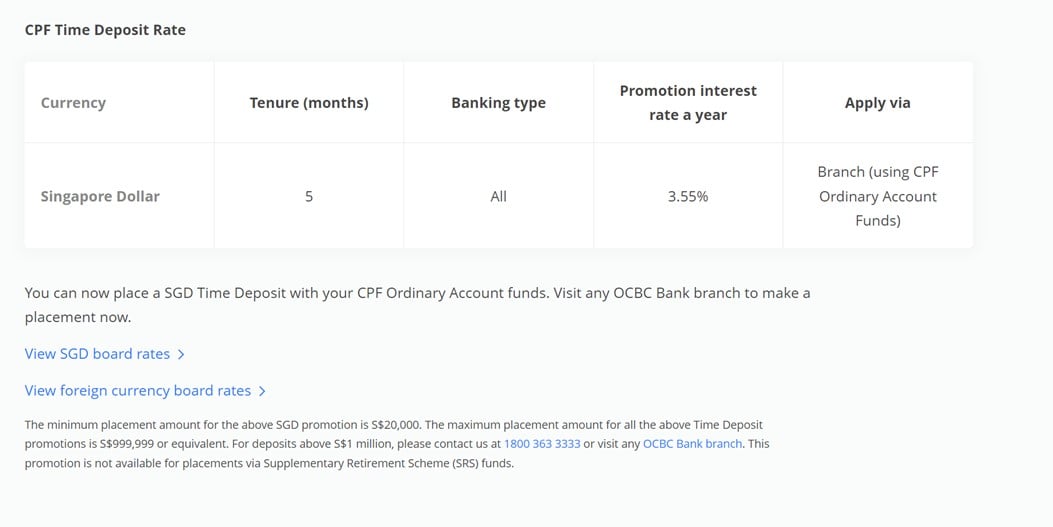

OCBC Fixed Deposit interest rate for CPF-OA plunges to 3.55%

Just a note that you can also buy Fixed Deposit using CPF-OA Funds.

This used to be at 3.88% from OCBC, but it has now been revised down sharply to 3.55%:

With this change, T-Bills are probably your best bet for CPF-OA funds.

Timeline to apply for 16 March 2023 T-Bills – Buying with CPF-OA

For CPF-OA applications, you’ll want to get your applications done by 12pm on 14 March 2023.

Rule of thumb is 12pm, 2 working days before the Auction date.

Should you bid competitive or non-competitive?

Bidding wise, I know there are some who advocate just putting in a non-competitive bid or bidding a low yield to guarantee allocations.

I’m not a fan of that as I do think it opens you up to the possibility of a freak result.

Better to just spend a few minutes thinking about the minimum yield you’re prepared to accept and cutting off this possibility.

So let’s discuss a bit about what is the expected range of yields we will see for the 16 March 2023 T-Bills.

BTW – we share commentary on Singapore Investments every week, so do join our Telegram Channel (or Telegram Group), Facebook and Instagram to stay up to date!

I also share great tips on Twitter.

Don’t forget to sign up for our free weekly newsletter too!

[mc4wp_form id=”173″]

What is the expected yield on the 16 March 2023 6 month T-Bills?

SGS Yields – 3.94%

The 6 month T-Bills trade at 3.94% on the open market.

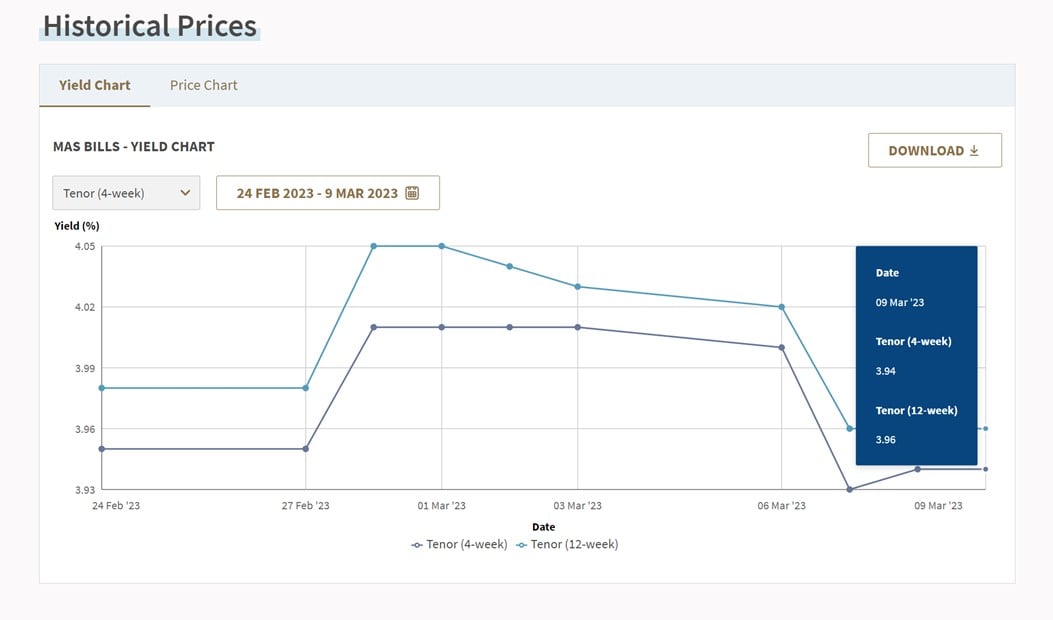

MAS Bills – 3.96%

The latest 12 week MAS Bills trade at 3.96%.

These are institutional only products, which give you a good idea of market pricing.

Jerome Powell reaccelerating the pace of interest rate hikes?

In case you missed it, at Jerome Powell’s testimony to the Senate this week, this was what he said:

Powell told the Senate banking committee that “the ultimate level of interest rates is likely to be higher than previously anticipated” and said recent economic data was “stronger than expected”.

He added: “If the totality of the data were to indicate that faster tightening is warranted, we would be prepared to increase the pace of rate hikes.”

In my January macro posts, I said the Feds made a big mistake in failing to push back on easing financial conditions.

The step down in interest rate hikes from 0.5% to 0.25% was too quick, as evidenced by reaccelerating economic growth and inflation.

Metaphorically speaking – they got cocky, and took their foot off the pedal too quickly.

Well, the Feds have awoken to this reality, per Jerome Powell’s comments this week.

The market is now pricing is a good chance (65%) of a 0.50% interest rate hike at the next FOMC meeting (up from 0.25%).

Market is now pricing in a peak of 5.50 – 5.75% interest rates this cycle.

My base case is for 6.00% terminal interest rates, so we are getting very, very close to the end game here.

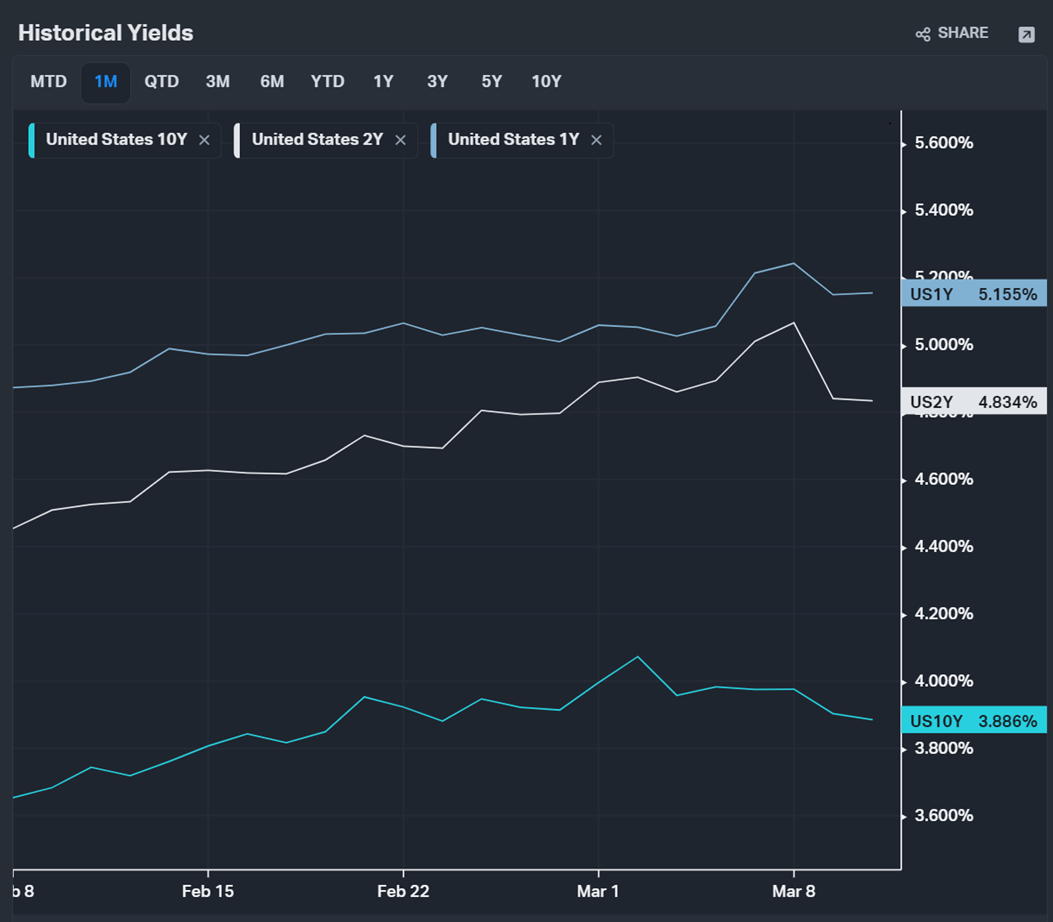

What was the market reaction?

The market reaction was very interesting though.

After the news from Powell on 8 March, you can see that the interest rates from the 1 year all the way out to the 10 year actually dipped.

If you look at the 12 week MAS Bills, you see a similar trend:

Why exactly this happened is not a simple answer.

You could argue it’s due to positioning, due to a flight to safety, due to the increased possibility of a recession due to more aggressive interest rate hikes.

You can also point towards the fear over the failure of US banks Silvergate bank and Silicon Valley bank.

Whatever the case, this is important to note.

Is this a green light to start buying short term bonds?

When interest rates are low, investors expect them to stay low forever.

When interest rates go up, investors expect interest rates to go up forever.

If there’s something I’ve learned from my time investing, it’s that – whatever the market expects with 100% certainty, you really want to start thinking about the possibility that it is wrong.

With the US 2 year breaking 5.00% this week.

And with market pricing in 5.75% terminal interest rates.

I do want to stress again – we are getting very close to the interest rate end game here.

Sure, there’s probably 25 bps to 50 bps more tightening that could get priced in.

But at these kind of levels, I think the risk for interest rates is to the downside, rather than to the upside.

Or in plain English – it’s probably not a bad idea to lock in current levels of interest rates (at the short end).

Just to be clear, this is only the short end.

The long end (10 year interest rates for example), is a completely different story.

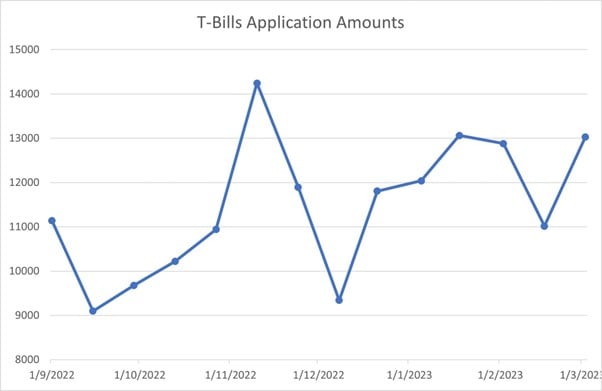

6 month T-Bills – Demand has been increasing steadily

If you look at the T-Bill application amounts, you’ll find that they remain very elevated.

Given the sharp drop in bank fixed deposit interest rates, you could see demand for T-Bills stay high.

Not to mention the evergreen demand from CPF-OA applications.

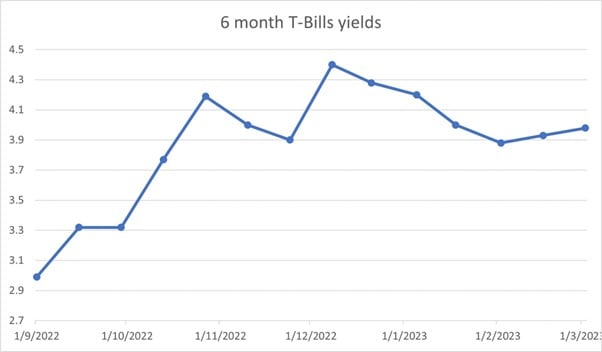

Will interest rates on the 6 month T-Bills cross 4.00%?

For some reason, many investors are fixated on the 4.00% mark.

Which frankly speaking, is more psychological rather than anything.

Interest rates have been on an uptrend since early Feb, so there is definitely a possibility that we break 4.00% on the T-Bills this time around.

But looking at all the data above, I don’t think that’s going to be my base case.

I think my expected yield for the next round of T-Bills will be 3.90% – 4.00%.

The Fed actions of this week have increased the possibility of a recession in the near term, which could have pretty big implications on fund flows into risk free assets like T-Bills.

But at the end of the day, it all comes down to supply demand at the individual auction.

So let’s see.

As always, this article is written on 11 March 2023 and will not be updated going forward.

If you are keen, my full REIT and stock watchlist (with price targets) is available on Patreon, together with weekly premium macro updates. You can access my full personal portfolio to check out how I am positioned as well.

Trust Bank Account (Partnership between Standard Chartered and NTUC)

Sign up for a Trust Bank Account and get:

- $35 NTUC voucher

- 1.5% base interest on your first $75,000 (up to 2.5%)

- Whole bunch of freebies

Fully SDIC insured as well.

It’s worth it in my view, a lot of freebies for very little effort.

Full review here, or use Promo Code N0D61KGY when you sign up to get the vouchers!

– Get up to USD 500 worth of fractional shares

I did a review on WeBull and I really like this brokerage – Free US Stock, Options and ETF trading, in a very easy to use platform.

I use it for my own trades in fact.

They’re running a promo now with up to USD 500 free fractional shares.

You just need to:

- and fund any amount

- Maintain for 30 days

Looking for a low cost broker to buy US, China or Singapore stocks?

Get a free stock and commission free trading .

Get a free stock and commission free trading with .

Get a free stock and commission free trading with .

Special account opening bonus for Saxo Brokers too (drop email to [email protected] for full steps).

Or for competitive FX and commissions.

Do like and follow our Facebook and Instagram, or join the Telegram Channel. Never miss another post from Financial Horse!

Looking for a comprehensive guide to investing that covers stocks, REITs, bonds, CPF and asset allocation? Check out the FH Complete Guide to Investing.

Or if you’re a more advanced investor, check out the REITs Investing Masterclass, which goes in-depth into REITs investing – everything from how much REITs to own, which economic conditions to buy REITs, how to pick REITs etc.

Want to learn everything there is to know about stocks? Check out our Stocks Masterclass – learn how to pick growth and dividend stocks, how to position size, when to buy stocks, how to use options to supercharge returns, and more!

All are THE best quality investment courses available to Singapore investors out there!