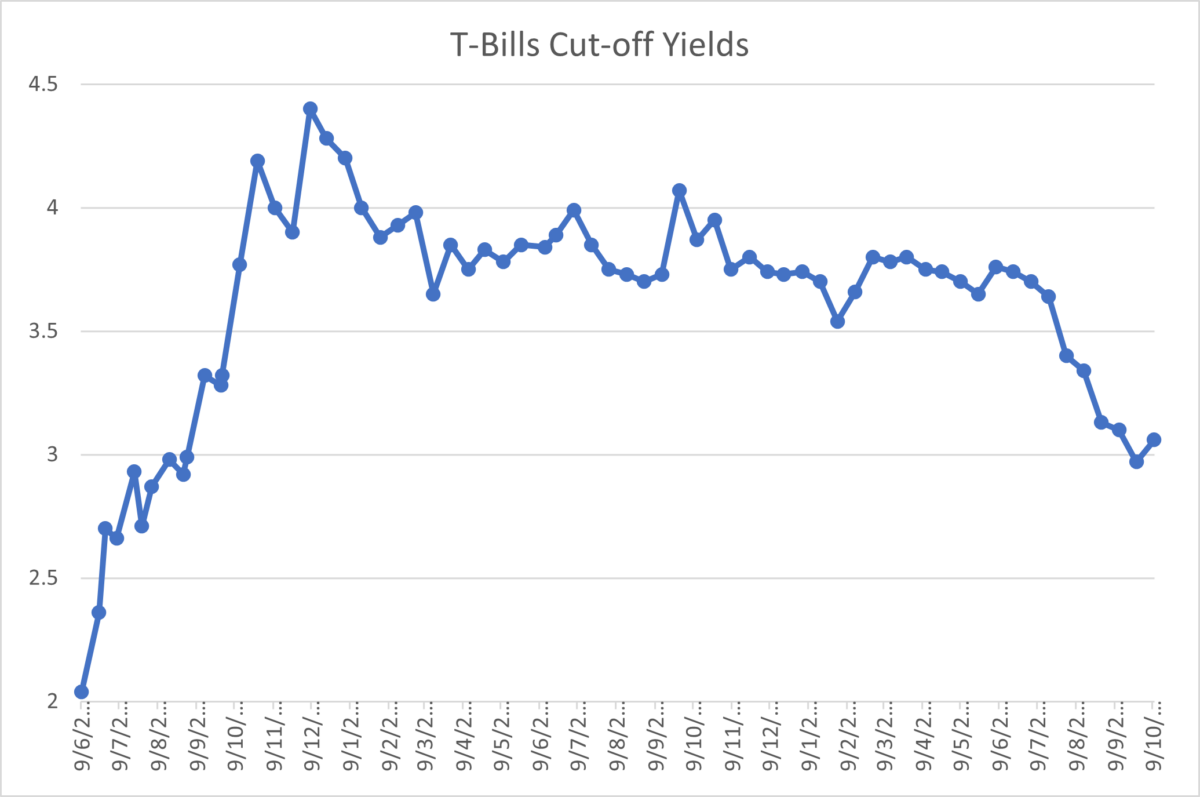

As you would all have observed – T-Bills yields are falling.

The latest T-Bills yields closed at 3.06%, which is the lowest it has been since late 2022 (more than 24 months ago).

For Singapore investors, we have been enjoying high interest rates risk free just “chilling in T-Bills”.

But with falling interest rates – how to earn attractive yields on cash in today’s climate?

One option is fixed income (bonds).

Why are short duration fixed income (bonds) attractive in today’s climate?

Short duration fixed income (1 – 3 year duration) is an attractive option in today’s climate.

Reason being that in a rate cut cycle, short duration fixed income allows you to “lock in” interest rates, such that you continue to enjoy attractive yields even after Fed rate cuts.

And yet you don’t take on too much duration, that you suffer huge capital losses if interest rates go up (compared to a 10-year bond for example).

In my view, a 1 – 3 year duration forms the sweet spot in allowing you to lock in rates for a longer duration (compared to T-Bills), and yet not too much duration that you can suffer big capital losses if rates go up.

So it was of great interest to me to learn that POSB is offering several short duration fixed income solutions.

One solution that investors may wish to consider is the SaveUp Portfolio:

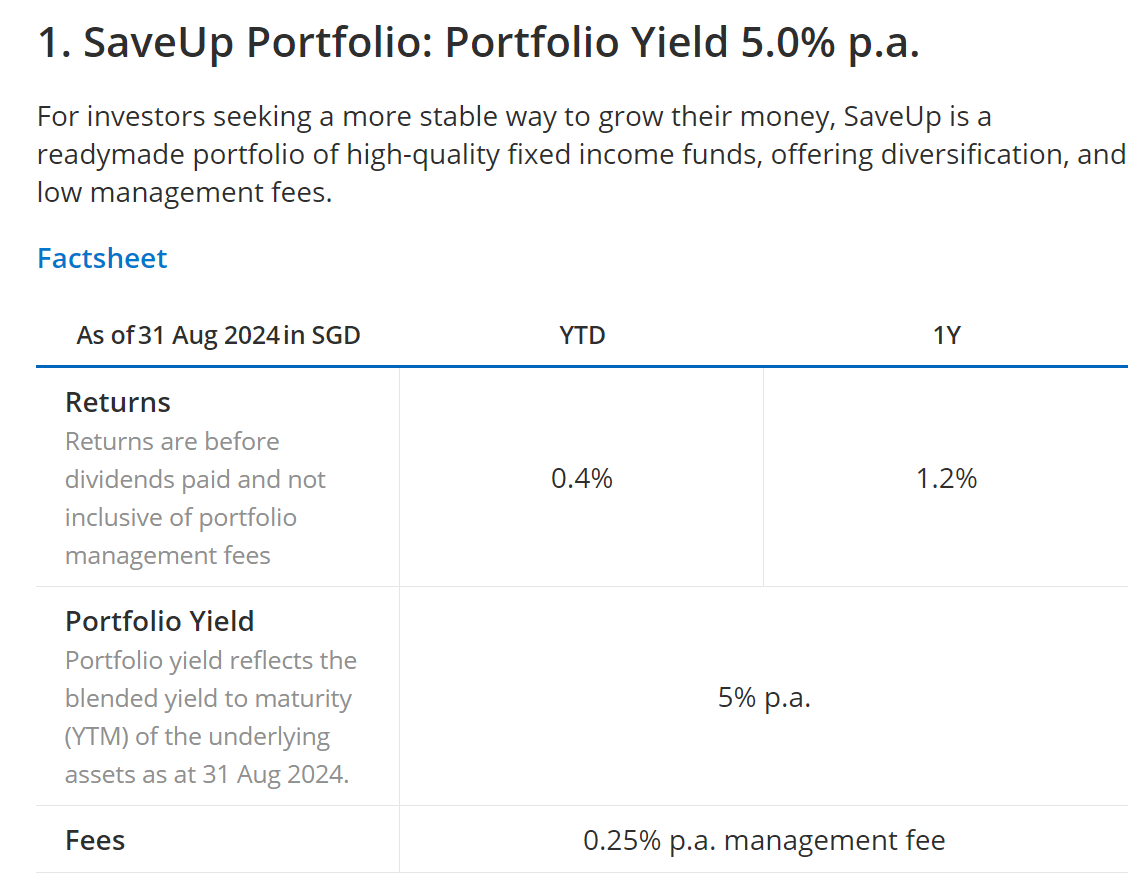

“As of end Aug 2024, the portfolio’s model characteristics were as follows: yield-to-maturity stood at 5.0%, with a duration of about 2.0 years. It has an average credit rating of A with high yield allocation below 10%.”

A portfolio with an average duration of 2.0 years, relatively decent credit rating, 5.0% yield to maturity and invested via DBS/POSB Bank.

Sounds very attractive, so let’s take a closer look.

Disclosure: This post is sponsored by POSB. All views and opinions expressed in this post are from Financial Horse.

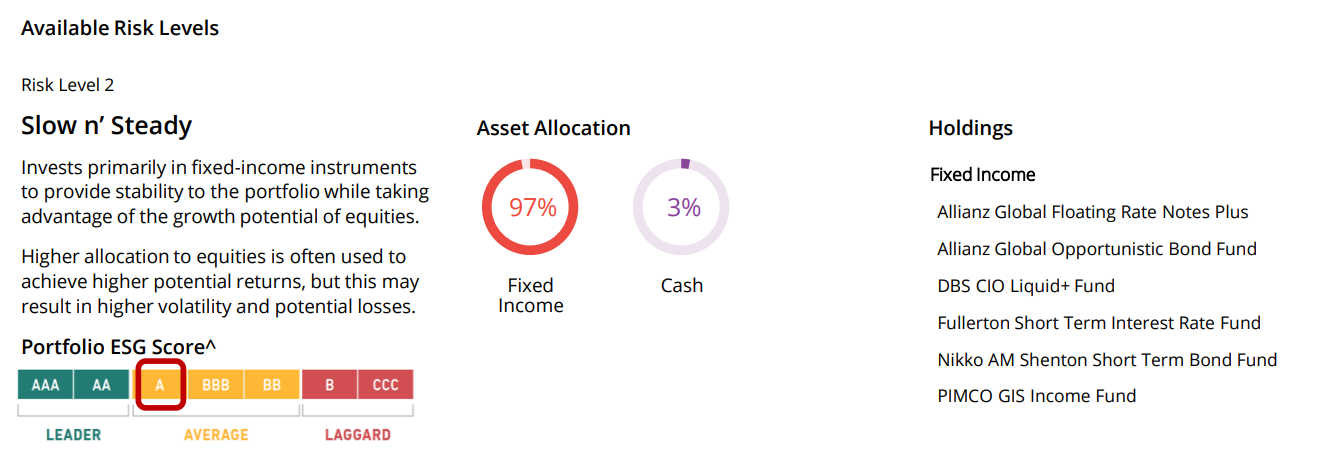

What is DBS/POSB SaveUp digiPortfolio?

The POSB SaveUp digiPortfolio is actively managed by DBS, and made up of 6 different bond funds:

- Allianz Global Floating Rate Notes Plus

- Allianz Global Opportunistic Bond Fund

- DBS CIO Liquid+ Fund (can be invested standalone – see more below)

- Fullerton Short Term Interest Rate Fund

- Nikko AM Shenton Short Term Bond Fund

- PIMCO GIS Income Fund

Just looking at this mix of funds suggest a nice mix between short-medium term bond funds.

The ideal target audience is “investors seeking a more stable way to grow their money”.

On top of this, there is also the DBS CIO Liquid+ Fund (4.90% portfolio yield) and Nikko Short Term Bond Fund (4.55% portfolio yield), which I’ll touch on below as well.

What I like about DBS/POSB SaveUp digiPortfolio

Let me start with what I like about the DBS SaveUp digiPortfolio.

Short duration, decent yield, relatively low risk

Per DBS:

As of end Aug 2024, the portfolio’s model characteristics were as follows: blended portfolio yield stood at 5.0% p.a, with a duration of about 2.0 years. It has an average credit rating of A with high yield allocation below 10%.

Sounds attractive to me.

Most cash instruments today are either split between the short-term bond funds (<12-month duration), or mid-term bond funds (4-5 years duration).

A portfolio with an average duration of 2.0 years, relatively decent credit rating, and 5.0% yield to maturity is pretty unique in the market, and there are not many similar products to my knowledge.

The portfolio yield is 5.0% (as at 31 August 2024).

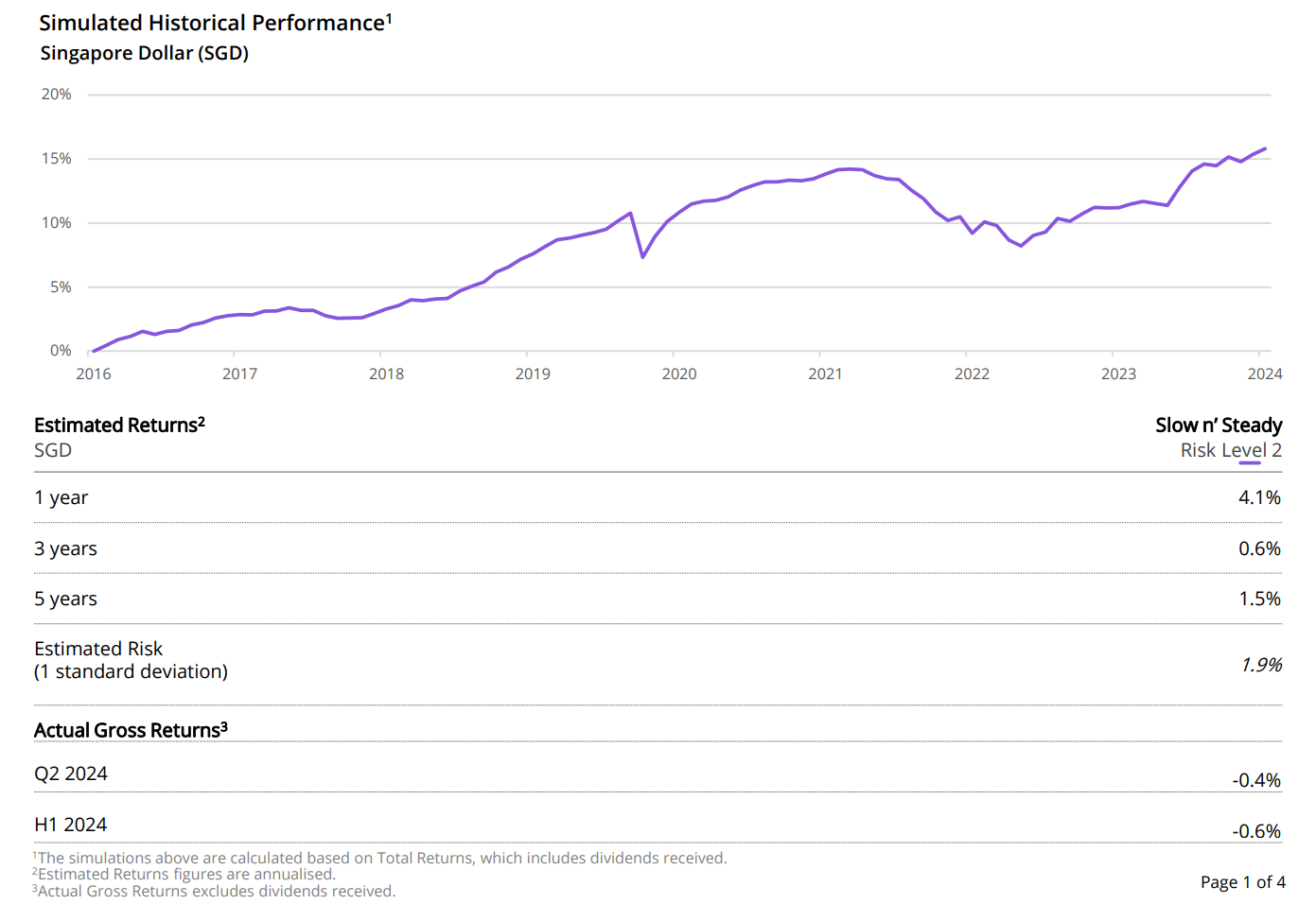

Annualised 1-year returns (inclusive of dividends) is about 4.1%, which is pretty decent.

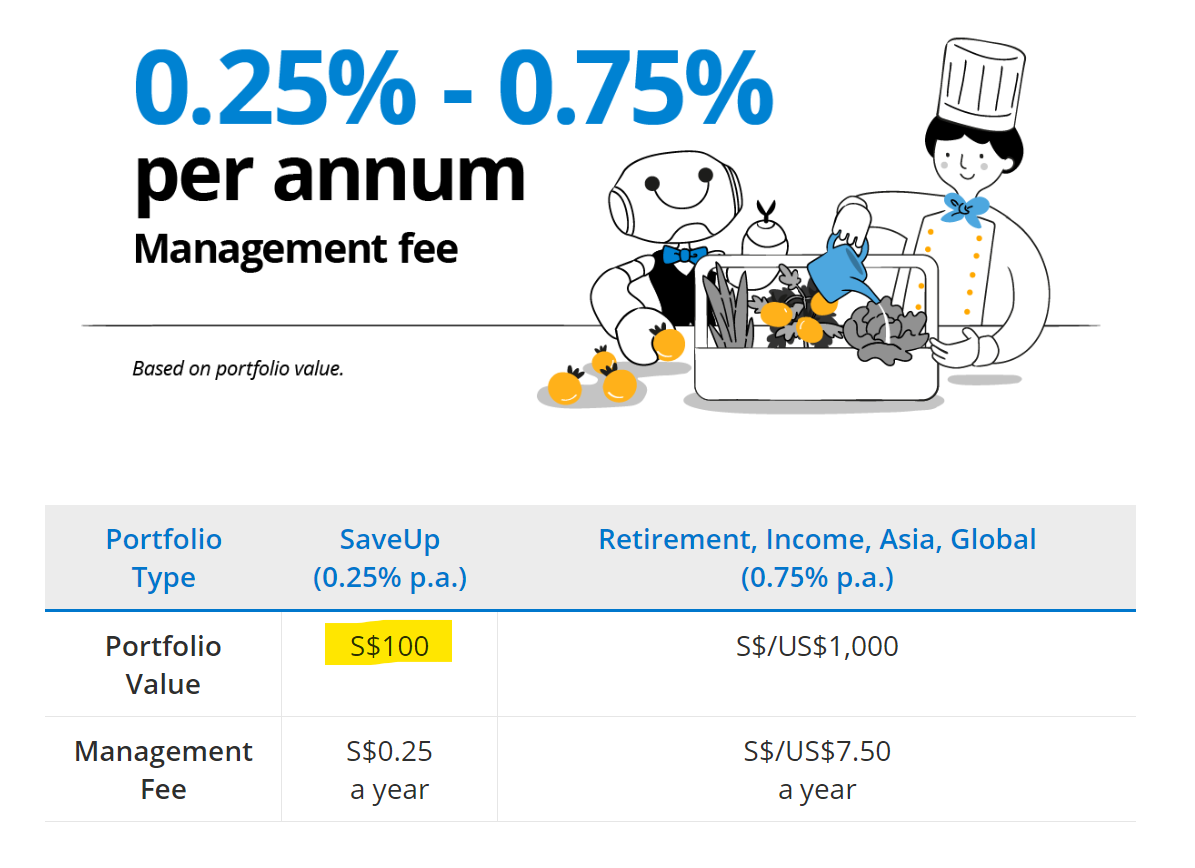

Fees are low (0.25% p.a.)

Fees are decent too.

Unlike the other digiPortfolios which have a 0.75% fee, for the SaveUp digiPortfolio it’s only a 0.25% p.a. management fee.

Note that investors will invest in the “best available share class” for each fund.

So for example for the core of the portfolio like PIMCO Income, DBS CIO Liquid+, Allianz Global Opportunistic bond, Fullerton Short Term Interest Rate, investors will be buying the funds with the cheapest available total expense ratio (TER).

Based on the Q3’24 portfolio composition, the TER of underlying funds (excluding the 0.25% DBS fee) would be in the range of 0.35-0.45% p.a., more than a third cheaper of what the retail share classes would have cost.

I like this a lot, this is in line with the best in class practices (and cheapest fees) available in the market today.

DBS/POSB is a household name + Invest as low as $100, and counts towards DBS Multiplier

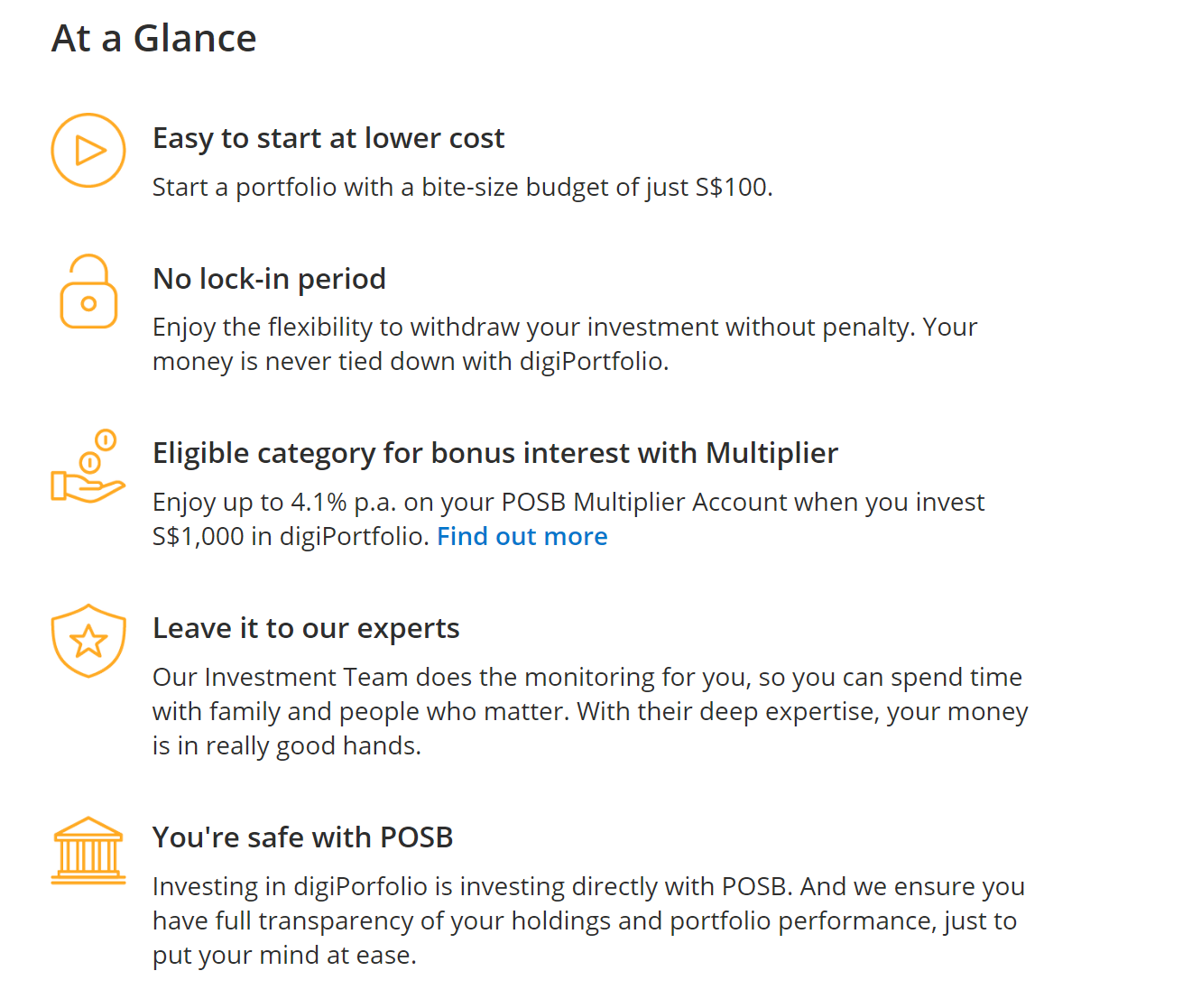

It is easy to start a portfolio, as you can invest as little as $100 each time.

There is also no lock-in period.

And of course, this is DBS/POSB Bank you are investing with.

For many investors, the fact that it’s DBS/POSB comes with a peace of mind that is invaluable.

In addition, you may also use your new investment into digiPortfolio to fulfil the “Investments” category for your DBS Multiplier account (with a minimum qualifying amount of $1,000 per transaction).

Note that the units of the underlying funds are pooled, but given that this is DBS/POSB, I do not see this as a material concern.

You can login to SaveUp and you will be able to see the full portfolio composition, what date the transactions were made, and full P&L breakdowns.

Risks of DBS/POSB SaveUp digiPortfolio

What about potential risks of DBS SaveUp digiportfolio?

Note that DBS/POSB SaveUp digiportfolio is not risk free

To be absolutely clear – unlike T-bills (which are guaranteed by the Singapore government), the underlying bond funds are NOT risk free.

While the bond funds selected are generally low risk, they are not zero risk.

If there is a global depression and investment grade credit starts to default in size, this portfolio may not be immune.

Case in point – you can see how actual gross returns (before dividends) for 1H 2024 was -0.6%.

To be fair though, 1H 2024 was a period of rising interest rates which would have pressured bond prices (bond prices trade inversely to interest rates).

Now that we are on a rate cut cycle, bond funds should theoretically benefit.

Annualised 1 year return (including dividends) is about 4.1%, but as to what are the future returns, only time will tell.

Note that SaveUp Portfolio does not distribute the dividends, but rather all dividends will be reinvested into the portfolio during quarterly rebalancing.

Actively Managed by DBS/POSB

This portfolio is actively managed by DBS/POSB, in that they may shift the asset allocation depending on market conditions.

As with any active management, this can play out both ways – get it right and this is a positive, get it wrong this is a negative.

Here’s some colour from DBS/POSB (on how they adjusted the portfolio in 2024):

In 1H24, global bonds (represented by the Bloomberg Global Aggregate Bond Index) detracted by -3.2% (in USD terms) as investors recalibrated their rate cut expectations for the year on the back of resilient economic data.

The SaveUp Portfolio, that is invested in bonds, delivered a price return (excluding fund dividends received) of -0.6% in 1H24 despite the weakness in bond markets. The portfolio’s short duration stance and focus on quality helped mitigate the drag from the broader bond market.

Our exposure to floating rate notes fund (Allianz Global Floating Rate Notes Plus), SGD short-duration bonds (Nikko AM Short Term Bond) and global diversified funds (PIMCO GIS Income and DBS CIO Liquid+) were the top contributors to the portfolio.

Through the quarter, we have kept the portfolio allocations unchanged as we believe that the portfolio is in a good position to generate positive returns going forward. The mix of strategies provides a holistic allocation despite our tight risk targets for this portfolio. As of end-May 2024, the portfolio’s model characteristics were as follows: yield-to-maturity stood at 5.6%, with a duration of about 2.1 years. It has an average credit rating of A with high yield allocation below 10%.

Going forward, we expect bond performance to be driven by easing monetary policies. With rate cuts expected in 2H24, it remains a tailwind for bonds, offering an attractive risk-reward for this asset class.

The key risk to bonds is sticky inflation, however, it would be mitigated by the portfolio’s short duration stance and high-quality positioning. At current attractive yields, the portfolio is in a good position to generate positive returns that will exceed fixed deposits or SG T-bills over the longer term, barring unforeseen adverse events.

Generally speaking, I do agree with DBS.

With the tailwind of Fed interest rate cuts coming.

There’s really no need to make big changes to allocation.

You just want to hold a broad portfolio of high-quality bond exposure, and let the rate cuts do the rest.

Comparison of DBS/POSB SaveUp digiPortfolio with other options

I know some of you will ask – what are the alternatives to DBS/POSB SaveUp digiportfolio?

As of end Aug 2024, the portfolio’s model characteristics were as follows: yield-to-maturity stood at 5.0%, with a duration of about 2.0 years. It has an average credit rating of A with high yield allocation below 10%.

The way I see it is that DBS/POSB SaveUp digiPortfolio is quite unique in the market for its 2.0 year duration.

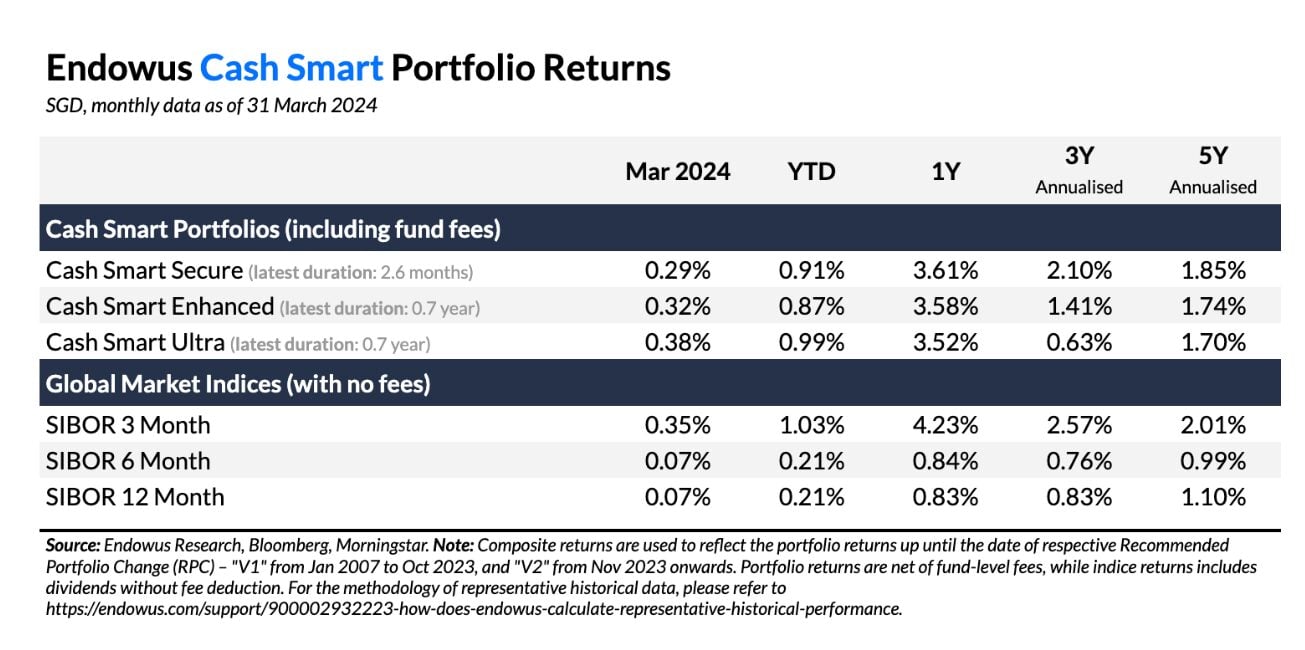

Let’s say you buy a bond fund from Endowus Income or Syfe Income, you’re looking at about 4 – 5 years duration.

Whereas if you buy a money market fund, even the highest duration money market fund is typically less than 12 months.

For eg. Endowus Cash Smart which is the most aggressive money market fund option – the duration is only 0.7 years.

And let’s say you decide to park cash in T-Bills or Fixed Deposit, typically you’re only locking in for 6 – 12 months at a time.

So the average duration of 2.0 years for the DBS/POSB SaveUp digiPortfolio is pretty unique in my view.

I don’t know of many other similar products out there, but please feel free to correct me if I’m wrong.

Who might consider DBS/POSB SaveUp digiPortfolio?

Per DBS/POSB, POSB SaveUp digiPortfolio is:

- “Ideal for seeking a stable way to grow their money with short duration bonds

- Offers diversification, and low management fees”

I think that’s about spot on.

What I would add is that you do need to recognise that there is no free lunch in investing.

If you want risk free, you can buy a Singapore government bond (the 2 year pays 2.4% today).

If you want a higher yield, you have to accept a certain level of risk.

The question then is what level of risk you as an investor are prepared to accept.

For investors comfortable taking some risk for a higher yield than cash fixed deposit rates, while not wanting to take on too much risk, I think the DBS/POSB SaveUp digiPortfolio is a good option to consider.

I funded a small amount into SaveUp Portfolio for the purposes of this article, and after this review, I’m actually minded to invest more into SaveUp myself.

I like that SaveUp portfolio offers:

- 5.0% portfolio yield

- Relatively cheap 0.25% management fee

- 2.0 years average duration (long enough to lock in yields, and not long enough to take on duration risk)

The icing on the cake is that this can be invested via DBS / POSB Bank, all within the comfort of your DBS / POSB digital banking app (and it counts as an investment for DBS Multiplier).

Other options: DBS CIO Liquid+ Fund and Nikko Short Term Bond Fund

The DBS SaveUp Portfolio is a multi-fund portfolio.

Alternatively if you want a single fund option, -there is also the DBS CIO Liquid+ Fund and Nikko Short Term Bond Fund for investors to consider.

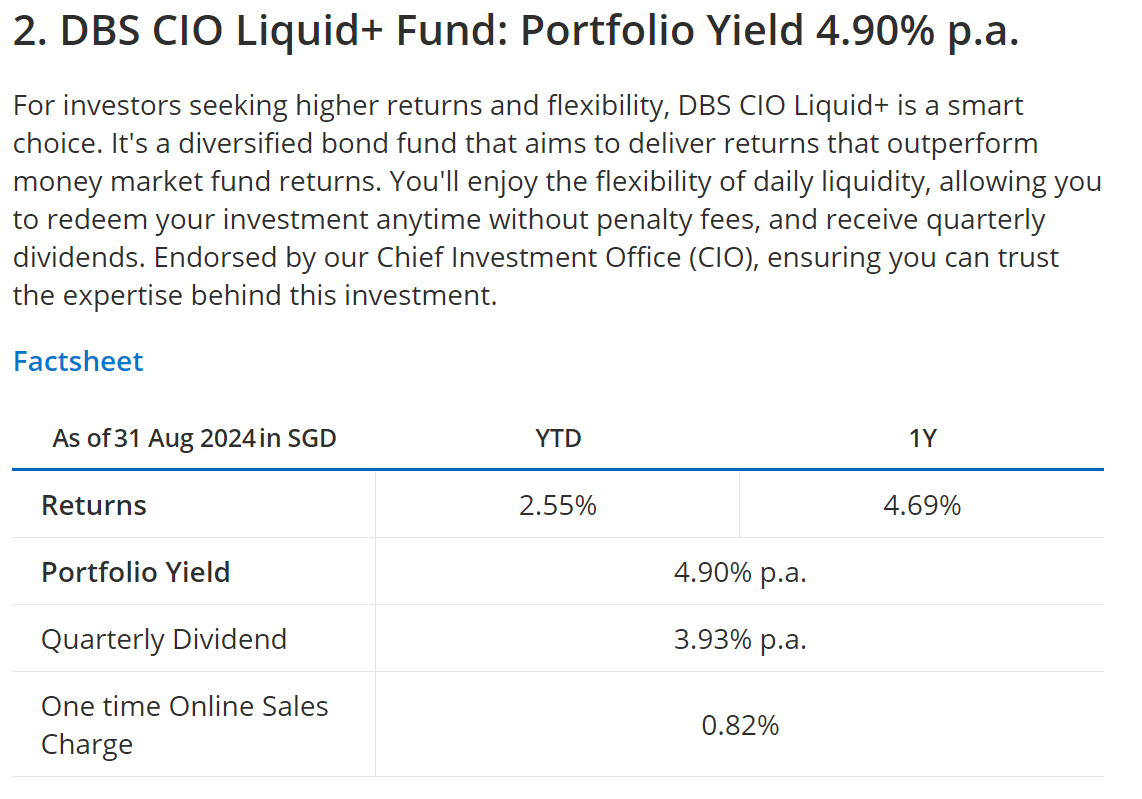

The DBS CIO Liquid+ Fund with portfolio yield of 4.90%:

Average duration is 2.02 years, and you can see the fund exposure below:

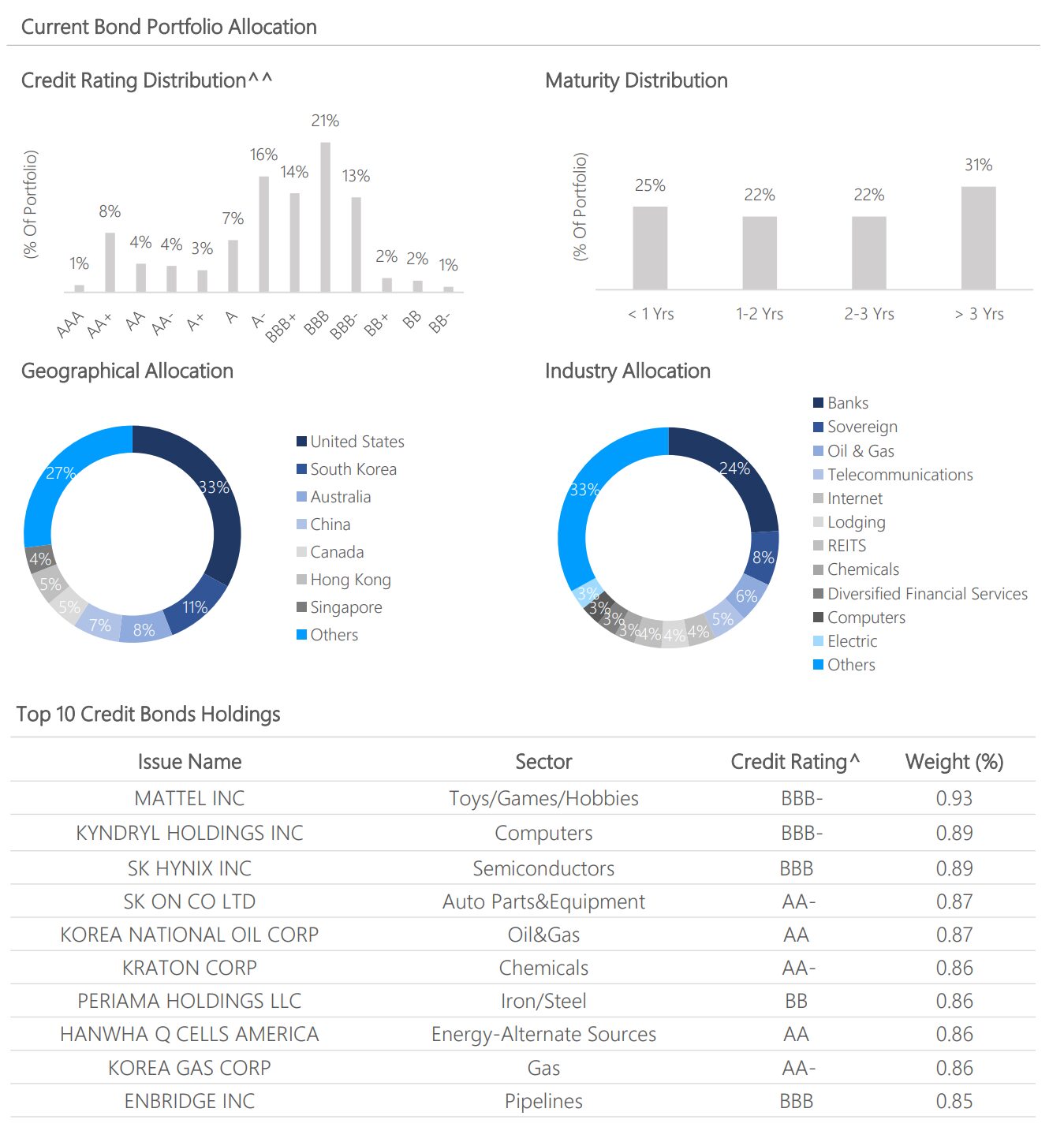

And for those who want to invest their CPF or SRS Savings, you can use the Nikko Short Term Bond Fund, with a portfolio yield of 4.55%:

Average duration is shorter at 1.37 years, and you can see the full breakdown below:

In any case I leave it for investors to decide if these products are appropriate for you.

You can get more information on each of the funds at the link below.

Find out more here: https://go.posb.com.sg/tbills-fh

Disclaimers

All investments come with risks and you can lose money on your investment.

This information is for general information only and should not be relied upon as financial advice. This publication may not be reproduced, or communicated to any other person without prior written permission.

This information does not take into account the specific investment objectives, financial situation or needs of any particular person. Before entering into any transaction involving any product mentioned in this publication, where applicable, you should seek advice from a financial adviser regarding its suitability for your own objectives and circumstances. If you choose not to do so, you should make an independent assessment and do your own due diligence on the product. This information does not constitute or form part of any offer, recommendation, invitation or solicitation to subscribe to or to enter into any transaction. It is not intended to provide, and should not be relied upon for accounting, legal or tax advice.

All investments come with risks and you can lose money on your investment. Invest only if you understand and can monitor your investment. Diversify your investments and avoid investing a large portion of your money in a single product issuer.

This advertisement has not been reviewed by the Monetary Authority of Singapore.

The information herein is not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution or use would be contrary to law or regulation.

DBS Bank (Company Registration. No. 196800306E) is an Exempt Financial Adviser as defined in the Financial Advisers Act and regulated by the Monetary Authority of Singapore.

The content here is for informational purposes only and should NOT be taken as legal, business, tax, or investment advice. It does NOT constitute an offer or solicitation to purchase any investment or a recommendation to buy or sell a security. In fact, the content is not directed to any investor or potential investor and may not be used to evaluate or make any investment. Do note that this is not financial advice. If you are in doubt as to the action you should take, please consult your stock broker or financial advisor.

Disclosure: This post is sponsored by POSB. All views and opinions expressed in this post are from Financial Horse.

Hi. I don’t see the 5% yield indicated in the DBS website. They indicated between 1.5-2% yield. Am I seeing the wrong SaveUp?

Yes if you look at the latest fact sheet, it will show the latest yield which is 5.6% as of end May, and 5.0% as of end Aug: https://www.dbs.com.sg/ibanking/pdf/factsheet-saveup.pdf?pid=sg-dbs-pweb-other-investments-alt-tbills-textlink-factsheet

What about considering PIMCO Income Fund SGD-H with forward rates of 6.3% ?

That’s another option I’m planning to write on.

The biggest difference I would say is duration – PIMCO has about 4 years duration, while this SaveUp is about 2 years.

So if interest rates go up, the PIMCO fund would see bigger mark to market losses. And of course underlying bonds are also different in terms of geographical/industry exposure.

Hi FH,

Pls correct me if I understand it wrongly.

There is no dividends distribution so the yield doesn’t matter much.

We can only profit from capital gains in the bond price.

YTD capital gain is 0.4%

12mths is 1.2%

The returns seems to be lesser while the risk seems to be similar when compared against money market fund?

Thank you.

No that’s not correct.

The underlying bonds do pay a yield, and portfolio yield is about 5.0%. Just that all the yields will be automatically reinvested into the portfolio (instead of paid out to the investor).

And historical 12 months return is about 4%+ (once you factor in the reinvested dividends).

Hope this clarifies. 🙂

Hi how can we sell it if we need the funds?

You can sell via DBS/POSB mobile app or internet banking. Exactly the same process as the way you buy.

Unlike Endowus, DBS offers no trailer fee rebates, so might need to check if the TER on the underlying funds is indeed the cheapest. DBS also does not transparently declare the individual fund level TER, so difficult to guage that.

I asked DBS the same question, and this was what they told me:

“Note that investors will invest in the “best available share class” for each fund.

So for example for the core of the portfolio like PIMCO Income, DBS CIO Liquid+, Allianz Global Opportunistic bond, Fullerton Short Term Interest Rate, investors will be buying the funds with the cheapest available total expense ratio (TER).

Based on the Q3’24 portfolio composition, the TER of underlying funds (excluding the 0.25% DBS fee) would be in the range of 0.35-0.45% p.a., more than a third cheaper of what the retail share classes would have cost.”

Working backwards if TER is 0.35%-0.45%, that is actually very competitive.

Don’t forget if you use Endowus Income for example, there is a 0.60% management fee from Endowus on top of that (while DBS is charging 0.25% here).

Hi FH,

There is no need to invest via a wrap structure like Endowus Income. Just buy the retail tranche of the individual fund. It is still cheaper than a wrap structure.

Ok get what you mean, thanks!

Hi FH,

POSB SaveUp digiPortfolio is a fund of funds structure which means one incur two layers of fees. Although you can say that the underlying funds might incur lower TER than a normal retail tranche, if you add them together, it is still the same or even higher than similar funds.

For those who prefer distributions and also a CPF included fund, I would recommend LionGlobal Short Duration Bond Fund Class A SGD (Dist).

https://www.lionglobalinvestors.com/en/fund.html?officialNav=LDFA

Below are the details (Based on latest factsheet):

1. Quarterly distributions (can opt for auto reinvestment if you do not wish to receive the distributions).

2. Weighted Yield to Maturity 4.48%

3. Weighted Duration 1.48 years

4. Weighted Credit Rating BBB+

5. Currency Exposure (% of NAV) SGD 99.7%. – Means almost zero currency risk, important for risk adverse investors.

6. Annualised 1 year return (including dividends) is about 5.47%, much higher than POSB SaveUp digiPortfolio.

7. Management Fee: 0.5%pa. TER should be around 0.57%pa. It is still lower than POSB SaveUp digiPortfolio if you add 0.25%pa to 0.35-0.45% p.a.

The same fund has other classes as well, like A SGD(Acc) for non distribution and USD H tranches but these are not included for CPF investments.

Hi GH Chua,

Quick question – which platform do you use to buy LionGlobal Short Duration Bond Fund Class A SGD (Dist)? If you use something like Endowus, don’t they tack on a 0.30% management fee as well?

Genuine question, I’ve not been able to find a platform that has no fees.

Those who purport to have no fees actually do have hidden fees by giving you access to a more expensive share class (or no trailer fee rebate).

Hi FH,

I use FSM platform and invest into this fund directly using CPF OA monies. There is no fees for CPF Investment using FSM. Only a one off transaction fee from CPF agent bank.

However, if you are using cash to invest, there is a platform fee on FSM. The management fee and TER listed is for the retail tranche and it includes trailer fee.

Hope that the above clarifies.

Just to comment on this, I’ve been used PIMCO GIS Income Fund, SGD Hedged, about 4 years duration, and 6%+ yield to maturity.

But because of the duration its quite a different instrument vs the one you are using.

And it has to be via Endowus because otherwise the retail tranche is 1.5% fees (vs about 0.55% for insti share class).

Hi FH,

I think it is because you have invested into a bond fund that is not included for CPF Investments. CPF Board do engage consultants to look at the fee structure of those funds. To be included for CPF Investments, there is a cap for TER as most (if not all) of the funds available for CPF Investments are retail tranches. So, my first cut-off for looking at funds is to look at those that are in the CPF-included list only. This is effectively cap the expenses that the funds have to incur, otherwise they will be restricted from getting any more new funds from CPF.

Hi FH,

The average duration will change when DBS rebalances the composition of DBS Saveup?

DBS can change to bond portfolio that is totally different from the 6 in your article?

Thks

It’s actively managed by DBS, so yes the duration has the potential to change if DBS changes the composition of the bunds.

I dont think DBS can change to a bond fund outside of these 6, but let me confirm with DBS.

Hi FH, There’s no front end sales charge on this product?

Yes no sales charge. You can see this on their fact sheet: https://www.dbs.com.sg/ibanking/pdf/factsheet-saveup.pdf?pid=sg-dbs-pweb-other-investments-digiportfolio-saveup-pdf-textlink-factsheet

If DBS SaveUp digiPortfolio loses money cos yields start to keep rising again, can I choose to keep my portfolio to maturity and reap the 5% returns at maturity instead of watching the capital of the bonds drop due to rising yield? As long as these bonds don’t default, I will get 5% at maturity and I have holding power, right ?

Yes, you will keep the portfolio until you choose to sell.

Hi FH,

I can’t find the TER of the fund. Can you provide the link showing the TER of the fund?

I dont think they computed the TER: https://www.dbs.com.sg/ibanking/pdf/factsheet-saveup.pdf?pid=sg-dbs-pweb-other-investments-alt-tbills-textlink-factsheet

But working backwards should be about 60 – 70 bps ish.