In case you missed it, Singapore unveiled a new set of property cooling measures last week.

I know a lot of you follow the Singapore residential market very closely, and quite a few are looking to make property decisions.

So I wanted to share my views on the cooling measures, and how they might affect the Singapore residential property market moving forward.

And if you only take away one thing from this article, let it be this excerpt from the MAS, MND, HDB joint statement:

“The Government remains committed to keep public housing inclusive, affordable and accessible to Singaporeans. We will continue to monitor the property market and adjust our policies to ensure that they remain relevant.

We urge households to exercise prudence before taking up any new loans, and be sure of their debt-servicing ability before making long-term financial commitments.”

What were the cooling measures rolled out?

The full announcement from MAS, MND and HDB is available here.

To sum up:

Private Property

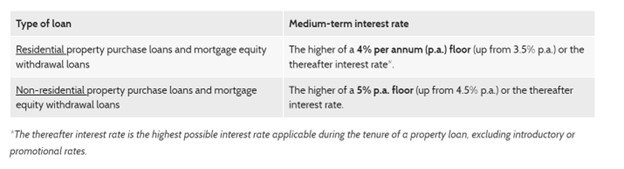

- Total Debt Servicing Ratio (TDSR) for private residential loans are now calculated using a floor of 4.0% interest rates (was 3.5% before this)

HDB

- Introduction of Floor Rate of 3.0% to calculate eligible loan amount

- Loan-to-Value (LTV) limit for HDB housing loans reduced from 85% to 80%

- 15 month wait out period to buy resale HDB after selling private property

Let’s talk a bit more about each of them.

1) TDSR for private residential loans are now calculated using a floor of 4.0% interest rates (was 3.5% before this)

Previously, the TDSR for private residential loans was calculated using the higher of (a) market interest rates, or (b) 3.5%.

This is now changed to the higher of (a) market interest rates, or (b) 4.0%.

Thinking behind this change?

As explained in the joint statement:

Mortgage interest rates pegged to the 3-Month Compounded Singapore Overnight Rate Average (SORA) have been rising in the past months. They are expected to rise further in 2023 along with US interest rates, before settling at a higher level compared to the lows during the period 2013 to 2021.

The revised medium-term rate floors ensure that households borrow prudently for their property purchases in a higher interest rate environment. This is necessary as property loans are long-term commitments and are often the households’ largest liability. Some borrowers may need to right-size their intended property loans but will be better able to service these loans when interest rates rise.

Impact of this change?

So the immediate impact of this change, is to reduce the maximum amount of mortgage loan a home buyer can take.

But to be very fair, the loan reduction amount is small.

And frankly, it is also a fairer reflection of the interest rate climate we are currently in, where mortgage rates are likely to go up to 4% soon.

So I don’t see this change so much as a cooling measure, and more as an update to reflect the current interest rate environment.

Government does not want buyers to take on too much debt, and run into financial difficulties when interest rates go up.

2) HDB Loans – Introduction of Floor Rate to calculate eligible loan amount

Previously, the interest rate used to compute the eligible loan amount for HDB loans is 0.1% above CPF-OA (ie. 2.5% + 0.1% = 2.6%).

This is now changed to the higher of (a) 3% p.a. or (b) 0.1%-point above CPF-OA.

There is no change to interest rates on the HDB loan which remains at 2.6%

Impact of this change?

This one is fairly straightforward, it is just an extension of the floor rate concept from private loans, into HDB loans.

As per above, I don’t see this as a cooling measure, and just as a way of ensuring those who take HDB loans don’t overextend.

Interest rates are going up, and may stay there for a while.

This set of changes makes sure buyers do not overextend, and can afford the loan even if interest rates go up.

That said, the fact that the HDB loan floor is 3.0% while the floor for private loans is 4.0% indicates that the government is likely to continue the preferential treatment for HDB loans moving forward.

And since HDB loans remain at 2.6% while private mortgages may hit 4% soon, this makes HDB loans much more attractive in the short term.

3) Loan-to-Value (LTV) limit for HDB housing loans from 85% to 80%

In the past you could borrow 85% of the HDB value in mortgage.

This is now reduced to 80% (private residential is 75%).

Thinking behind this change?

MAS/MND/HDB explains it quite clearly in their press release (emphasis mine):

This is not expected to affect first-timer and lower-income flat buyers significantly, as they may receive significant housing grants of up to $80,000 when buying a subsidised flat directly from HDB, or up to $160,000 when buying a resale flat. They can also tap on their CPF savings to pay for the flat purchase, thereby reducing the loan amount they may need to take.

This change is not intended to affect those buying their first HDB, and the lower income.

Which means… this is intended to affect those buying their second HDB (or more).

Impact of this change?

This is a fairly big change, as it increases the amount of cash required by buyers upfront (by 5% of the purchase price).

My view is that this is quite clearly intended as a cooling measure, by reducing demand.

The goal is to reduce the pool of potential buyers for resale HDBs, especially targeting those buying their second (or more) HDB.

I suppose the message here is that if you are low income or if you are a newly married couple buying your first home, that is fine.

If you are cashing out your existing HDB to buy a second one (or moving for some other reason), then you can wait. If you really want to move, you need to save up more cash upfront.

4) 15 month wait out period to buy resale HDB after selling private property (for sellers under 55)

This is the big one.

Sellers who sell a private property, need to wait 15 months before they can buy a resale HDB.

This will not apply to seniors aged 55 and above who are moving from their private property to a 4-room or smaller resale flat.

Thinking behind this change?

As HDB explains it:

This is a temporary measure to moderate demand for resale flats, which we will review depending on overall demand and market changes.

…

The Government remains committed to keep public housing inclusive, affordable and accessible to Singaporeans. We will continue to monitor the property market and adjust our policies to ensure that they remain relevant.

We urge households to exercise prudence before taking up any new loans, and be sure of their debt-servicing ability before making long-term financial commitments.

Impact of this change?

This is an interesting change that is designed to hit a very specific segment of buyers – those who are looking to cash out of their private property, and move into a resale HDB.

And to pocket the difference.

The message here is clear.

If you are 55 or older, you can cash out of your home, but you cannot move into a 5 room resale HDB (4 room and below only).

If you are below 55, you should not be doing this at all.

But – HDB also makes it clear that this is meant to be a temporary measure to bring down demand for resale HDBs. If supply picks up, or demand comes down, they may take it away.

Short term at least, this will reduce demand for resale HDBs.

What are the implications of this set of property cooling measures?

My views on the impact of this set of cooling measures in the short term:

- Good for the rental market – Those who want to cash out of their private property are now more inclined to rent

- Bad for resale HDB prices – Demand for resale HDB is now reduced

- Neutral for Private Residential prices – No major impact for private residential from this set of changes

Looking at the bigger picture – Residential Property still a good investment?

But we need to take a step back, and look at the overarching message the government is trying to send.

From this set of changes, my takeaway is that:

- Government is concerned that resale HDB prices are going up so quickly (and becoming unaffordable for Singaporeans)

- Government does not want households to overextend financially, especially with rising interest rates

Which brings us back to the MAS, MND, HDB joint statement:

“The Government remains committed to keep public housing inclusive, affordable and accessible to Singaporeans. We will continue to monitor the property market and adjust our policies to ensure that they remain relevant.

We urge households to exercise prudence before taking up any new loans, and be sure of their debt-servicing ability before making long-term financial commitments.”

Long term bullish?

The problem with Singapore housing, is the exact same problem we have globally with inflation.

After COVID, household incomes went up significantly.

Consumers have more money and they spend more.

But supply cannot keep up with the higher demand.

And therefore prices go up significantly.

There’s only 2 ways to solve this:

- Increase supply

- Decrease demand

Of course – you cannot increase housing supply overnight. It takes years to build a new HDB.

Which means you can only control demand.

Bringing Demand down

With this set of measures, that’s what government is trying to do, by bringing down demand for resale HDBs in the short term.

But just like with inflation, you cannot keep demand suppressed forever.

At some point in time, either these temporary measures will be removed, or the market will adjust to the reduced demand.

So for what it’s worth, I don’t think these set of cooling measures have a big impact on Singapore residential property prices in the longer term.

Nor are they designed to.

Closing Thoughts

I think the days of getting wildly rich from Singapore residential properties are over.

The days of levering up and buying 10 properties, and getting insanely rich as long as you can hold onto them all for a decade or two, that’s over.

But if you temper your expectations, and look for low single digit returns long term (nominal, before accounting for the debt).

I think that’s quite realistic, and is actually what the government is trying to gun for here.

Government doesn’t want residential real estate prices to crash because that would affect household balance sheets and financial stability. And frankly given the TDSR and ABSD measures in place households are not overleveraged, and should have significant holding power.

But too rapid price increases are not healthy either. They make housing unaffordable for buyers. And they encourage speculation, as buyers borrow and bid higher prices in the hopes of making even more down the road.

So Singapore residential real estate has become a very unique asset class where you in some ways have the government at your back, to ensure stability in this asset class.

Just don’t expect double digit annualized returns on residential real estate. Those days are over.

Will more property cooling measures come?

So while more property cooling measures may come, the more important thing is to understand the broader philosophy guiding the actions from the government:

The Government remains committed to keep public housing inclusive, affordable and accessible to Singaporeans. We will continue to monitor the property market and adjust our policies to ensure that they remain relevant.

We urge households to exercise prudence before taking up any new loans, and be sure of their debt-servicing ability before making long-term financial commitments.