I received this question recently on the Financial Horse Forums:

Hi Financialhorse. My investment property is going enbloc. I do not intend to buy back another property because of the ABSD. Can you advise me how to do a safe investment to generate income? I am in my 60’s and my risk appetite is not high. Thanks.

This really caught my eye because after my previous 10 Stocks to buy in the next market crash article, a reader also reached out saying that he planned to invest his en-bloc proceeds based off the suggestions in that article. Financial Horse doesn’t believe in coincidences (I am a huge conspiracy theory nut), and the fact that in the span of less than 7 days, 2 separate readers had similar en-bloc questions points to something deeper.

Over the next 12 months, a lot of Singaporeans are going to be receiving their en-bloc proceeds. Assuming this house wasn’t their primary residence, that is going to translate into a lot of spare liquidity to be reinvested.

In this article, I will describe what I will do if I were in such a situation, and readers can decide if this is relevant to them.

Assumptions

Let’s flesh out this reader’s profile a bit more. I will change her name to June for privacy reasons, as I do not know if her forum name is her real name.

June is in her 60s. She has a primary residence where she stays with her family. She also has a private condo that is an investment property, and that she uses to generate income. The market value of the property is S$1.5 million and generating S$4,000 in rental a month. This translates to a 3.2% NPI yield, which is fairly market standard. The property has now been sold at S$2 million in an en-bloc.

June’s financial knowledge is not high. Being in her 60s, she mainly just wants to enjoy her golden years rather than track the stock market on a day to day basis (which is not good for the heart, even for younger persons). Her risk appetite is not high, and the primary consideration is wealth preservation rather than wealth creation. Given that her investment property was generating income, she needs to invest in alternatives to replace the lost income.

Basics: Why not buy another property

The first and most obvious question of course, is why not buy a replacement property? There are two big problems with this, being:

Replacement costs – The way the property market is priced these days, if you sell your condo in an en-bloc, you will not be able to buy back a similar profile condo in the same locale with the proceeds. This means that investors will need to purchase either a smaller condo in that location, or move to alternative locations. Neither of which may be attractive options to the seller.

ABSD – But perhaps the most glaring reason is Additional Buyer’s Stamp Duty (ABSD). ABSD rates are set out below, and coupled with traditional stamp duty, can really add up to transaction costs. For example, on a S$2 million dollar replacement property, you are looking at:

S$140,000 (ABSD) + S$64,600 (BSD) = S$204,600

That’s S$200,000 worth of taxes alone! If June owns 2 existing properties, that number jumps to S$260,000. This means that June is paying 10% of the purchase price in taxes, and without tapping into her savings to cover stamp duty, the amount she can spend on her replacement property is reduced by S$200,000 immediately. I can definitely see why June does not want to buy another property.

| Profile of Buyer | ABSD Rates from 12 Jan 2013 |

| Singapore Citizens (SC)1 buying first residential property | Not applicable |

| SC1 buying second residential property | 7% |

| SC1 buying third and subsequent residential property | 10% |

| Singapore Permanent Residents (SPR)1 buying first residential property | 5% |

| SPR1 buying second and subsequent residential property | 10% |

| Foreigners (FR) and entities2 buying any residential property | 15% |

| Purchase Price or Market Value of the Property | BSD Rates for residential properties |

| First $180,000 | 1% |

| Next $180,000 | 2% |

| Next $640,000 | 3% |

| Remaining Amount | 4% |

Source: IRAS

Yourself (5%)

Let’s look at an alternative way of spending that S$2 million. Firstly, June should take 5% of that proceeds and treat herself to a holiday, a fancy handbag, a nice spa, whatever she wanted her whole life but never got the chance to do. She’s worked hard her entire life, and now that she’s had a large liquidity injection, its time to take some of that hard earned money and enjoy. Seriously. You’re not going to miss that S$100,000 from your investments.

For the remaining 95%, I would advise putting 60% in high yielding savings accounts or bonds, and 35% into equities and REITs. This would allow June to maintain a large cash buffer to meet any emergency expenses and reduce the volatility that comes with equities investments, but at the same time enjoying higher dividends from equities and REITs.

Bonds (60%)

The 60%, or S$1.2 million, should go into the highest yielding fixed deposit accounts or bonds.

In terms of priority, this should be: (1) CPF, (2) Singapore Savings Bonds, (3) Bond ETF, (4) Fixed Deposit.

CPF

There is no product in the market that will beat CPF’s risk adjusted returns. CPF members aged 55 and above will also earn an additional 1% extra interest on the first $30,000 of their combined balances (with up to $20,000 from the OA). As a result, CPF members aged 55 and above will earn up to 6% interest per year on their retirement balances. And these returns are guaranteed by the Singapore government.

However, there are many limitations with CPF, one of which is that it cannot be freely withdrawn, as citizens need to maintain a minimum Retirement Sum in CPF. You can take a look here for more information, and decide if topping-up CPF is an appropriate choice for you. If it is appropriate, definitely do it, as none of the other products in this article can match CPF in terms of yield and safety.

Singapore Savings Bonds

The next best choice is Singapore Savings Bonds. It’s a great investment for the following reasons:

Decent interest rates – This month’s SSB’s interest rates are set out below, which are actually very decent and far higher than any fixed deposit out there. By holding to maturity, one would enjoy a 2.43% return a year.

Risk Free – It is backed by the Singapore government, and completely risk free

Redeemable at any time – SSBs can be redeemed at any time (you will even earn pro-rata interest up till the date of redemption). This makes it a highly liquid investment.

| Year from issue date | 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | 10 |

| Interest, % | 1.68 | 2.14 | 2.21 | 2.21 | 2.30 | 2.52 | 2.67 | 2.81 | 2.96 | 3.12 |

| Average return per year, %* | 1.68 | 1.91 | 2.01 | 2.06 | 2.10 | 2.17 | 2.24 | 2.30 | 2.37 | 2.43 |

Source: SSB

The only problem is that each person can only subscribe for S$100,000 worth of SSBs. If June has 2 kids and 1 husband, she can subscribe in each of their names, totalling S$400,000. But beyond that, she will still need to search for an alternative.

Bond ETF

June can buy Singapore Government Securities direct if she so chooses (see more here). However, there is no liquid market for SGS, and apart from holding to maturity, there is no easy way of exiting the bonds at fair value.

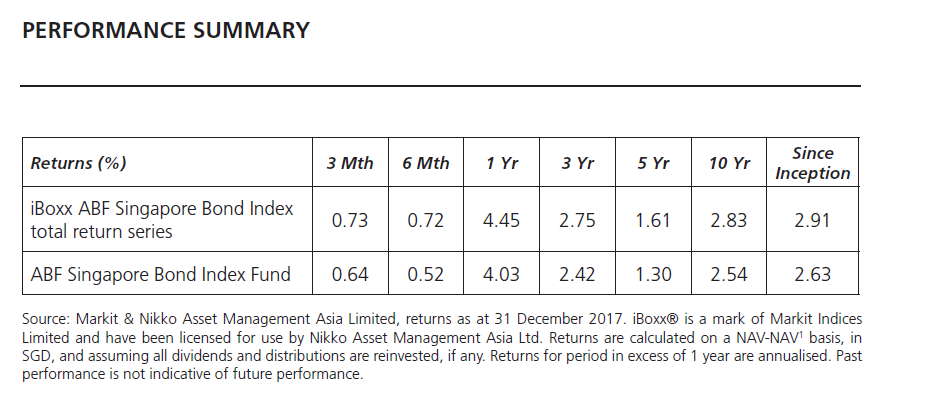

The alternative I would propose, is to buy a bond ETF. The forward yield of the ABF Singapore Bond Index Fund is approximately 2.5%, and less the management fees of 0.2%, works out to approximately 2.3% a year. The historical returns of 2.54% over the past 10 years are pretty decent as well.

Source: Annual Report

However, there’s not much liquidity on the bond ETF. Average trading volume is about 265,400, so to accumulate a S$800,000 position without moving the market, she would need to buy in over a number of days. Exiting the ETF should be alright for small amounts, as she can just sell directly on the SGX. To exit the investment all at once may be problematic if the quoted price is trading way below NAV. If so, the best alternative may be to redeem directly through a participating broker.

Fixed Deposit

Fixed deposit is always an alternative, but the current yields are not that attractive. One way to do it is to keep S$100,000 to S$200,000 in fixed deposit, as it may be more liquid than the Bond ETF.

Forex Risk

A US Treasury ETF, such as the TLT, would be highly liquid and meet almost all the objectives we want from a bond ETF. Unfortunately, for Singaporeans, that would require taking on Forex risk. While this may be fine for 20 or 30 year olds who have multi-decade investment periods, this is a lot more risky for a 60 year old. If there is a large depreciation in the USD, and she needs the money urgently, she may be forced to sell at a loss, which can really hurt her nest egg.

Don’t forget, there is 30% withholding tax payable on US bonds for Singaporeans, so a 3% yielding bond will be reduced to 2.1% after tax, which makes it very hard for US bonds to match up to local alternatives.

Bond Yields

Assuming a 2.4% return on this 60% bond component, it works out to approximately S$28,800 income a year.

Stocks/REITs (40%)

The remaining 35%, or S$700,000, should go into blue chip dividend stocks or REITs, which are intended to make up for the lost income. In my previous article, I had assumed a market crash scenario where the valuations are a lot more attractive. The analysis is different at current price levels. For example, CCT is currently yielding about 4.5%, and I would not be comfortable buying it at such prices.

Unfortunately, the en-bloc portfolio has to take the market as it is, and cannot wait for a crash (that would be market timing, and can be disastrous if the timing is wrong). Accordingly, the stocks I would suggest are:

DBS Bank

I wrote a long article on DBS previously on why I like this bank, but there is no getting around the fact that DBS is a risky investment. It’s near its all time highs, and banks are highly prone to large declines when a recession hits. However, I do like this stock because of its 4.2% yield, and theoretically, it should go even higher once the economy, and interest rates, pick up. Given the risks in this counter, I will only put in 5%, or S$100,000.

Mapletree Commercial Trust (MCT)

I view MCT as a hybrid between CMT and CCT. It is a blue chip REIT with solid properties located in Singapore and I really like the Sponsor. In addition, MCT is currently trading at a 5.6% yield, while CMT and CCT are trading 5.3% and 4.5% yields respectively. For that reason I would prefer MCT based on current prices.

I will add in 20%, or S$400,000 to MCT. This serves as a Singapore retail and commercial play.

Mapletree Greater China Commercial Trust (MGCCT)

Given that June has almost S$1.2 million in bonds, we can afford to take slightly higher risks in the equity portion of her portfolio. Don’t forget, all this is excluding her other assets, and she almost certainly has her primary residence and other savings that contribute to her net worth.

MGCCT is trading at a nice 6.5% yield, it has very decent properties in Hong Kong and China, and I really like the latest acquisition of its Japan portfolio, which was DPU accretive while diversifying the asset base. However, I acknowledge that this is riskier than MCT, and for that reason, I will add only 7.5%, or S$150,000 of MGCCT.

Ascott Residence Trust

Following on the thread above, I also wanted to diversify the portfolio away from Singapore, and into a different class of real estate. Ascott Residence trust is a good fit. It is a hospitality REIT backed by the CapitaLand Group (another Sponsor I really like), and is currently trading at a nice 6.2% yield. I will add 7.5%, or S$150,000, as well.

Equity Yields

The equity component of the portfolio will generate an average 5.7% yield, which is about S$40,000 annually. Together with the bond component, that is about S$70,000 annually.

Assuming the house was originally trading at a 3.2% yield originally, it would have yielded about S$48,000 a year, which after property tax, maintenance, agent fee, expenses etc, would be about S$40,000. Accordingly, this portfolio yields about S$30,000 (more than 50%) more than the original investment property, and is far more liquid as it allows June to sell certain components to raise cash as required.

Decision points

As readers may note, there is a very heavy allocation to real estate, with almost 35% of the portfolio coming from REITs. I view this as an acceptable risk, considering that originally, 100% of this money was invested in real estate anyway. By diversifying the en bloc proceeds into bonds and REITs, June actually diversified her portfolio significantly, while at the same time increasing her yield.

Don’t forget, in a recession, the house would lose 20-30% of its value, and its rental income would fall significantly. By moving 60% of the allocation into bonds, this actually drastically reduces the impact of a recession/fall in real estate prices on the portfolio.

A key question would be how should June react in a recession? What she should do, is to never sell the equity component. Look at the equity component as if she bought a house instead. If there is a recession and the S$2 million house is now worth S$1 million, would you sell? The heavy allocation to REITs means that the analysis here is largely the same. Vivocity’s valuation may fall 30% in a recession, but as long as you keep holding it, its property value, and rental yield, will eventually pick up. Of course, any spending needs in the meantime will come from cash savings or dividend income first. If this is insufficient, she should sell small amounts from the bond component.

The next question is whether to sell the bonds to buy a property on the cheap in a recession? In the next recession, I think there is a possibility that the government will remove ABSD, so buying a property actually becomes an option again. This can be a high risk high reward move, and whether it works would depend on your profile as an investor. If you have children to support you, or a large pool of existing savings, this can actually be a great solution. You can sell S$1 million worth of bonds, use that to cover 50% of the purchase price of a new property, and take up a mortgage for the remaining 50% (secured on your primary dwelling). The rental income can be used to meet the monthly mortgage repayments (with small top-ups from existing assets or children). As the recession passes, you stand to make massive capital gains, and your rental income will pick up as well.

Closing Thoughts

A lot of Singaporeans believe that the only way to be rich is to buy a property, rent it out, and watch it appreciate in price. This is largely based on the astounding growth in Singapore property prices over the past 50 years. However, don’t forget that the past 50 years saw Singapore grow from a backwater port into a global financial centre. For property prices to keep up the pace of growth requires this remarkable growth story to continue in the future. Not only that, but property prices require favourable long term supply and demand dynamics, in the form of a growing population, and slow pace of new supply.

Whether this is the case, is anyone’s guess. However, with interest rates on the rise, the global economy on a 10 year bull run, and the current en-bloc craze driving property prices up, I would be somewhat wary of plonking 2 million dollars worth of en-bloc proceeds into the property market right now. The portfolio I have set out above serves as an alternative. It is broadly diversified, generates decent yield, and allows one to adopt a wait and see approach. If I am wrong and the markets pick up, at least the equity/REIT component of the portfolio will appreciate. If I am right and property prices fall, the equity/REIT component may drop, but the massive bond component will stay intact, and allow me to deploy the money at a far more reasonable valuation.

What are your thoughts on this? Is there a better solution to June’s problem? Share your thoughts in the comments below, or better still, respond directly to June here.

Financial Horse has a set of 7 Commandments for Successful Investing, that I ask myself before making every investment, and that I will never break regardless of the situation. Enter your email below to receive a copy in your inbox!

[mc4wp_form id=”173″]

Enjoyed this article? Like our Facebook Page for more great articles!

Excellent article. Will definitely work on it. Thanks again.

No problem, glad you like it!

How does the the kids subscribe to SSB? Don’t they need a CDP account etc ?

Hi SY,

Welcome to Financial Horse! Yes you are right, a CDP account is required.

However, as June is in her 60s, I assumed her kids are above 18 and able to subscribe for SSBs. If this is not the case, a higher amount can be allocated into the bond etf.

Excellent suggestions!

Considering the late economic cycle, high valuations, and the fact that her prev rental income was $40+K … Maybe can reduce equity allocation to 25% to generate similar income.

The larger bond portion can be used to top up the equities to 40% or even 50% allocation in the event of 20+% or 30+% bear market.

Ok ok i know is market timing … But unless she really needs higher income now…

Great point Sinkie! Yes actually you are right, a 20% to 30% equity allocation will still make up for the same amount of loss income, and this can be used to buy a new property or equities in the event of a bear market. I guess the ultimate allocation will depend on her risk appetite and desired income.

Great point Sinkie! Yes actually you are right, a 20% to 30% equity allocation will still make up for the same amount of loss income, and this can be used to buy a new property or equities in the event of a bear market. I guess the ultimate allocation will depend on her risk appetite and desired income.

Excellent article. Well balanced!

Cheers. Welcome to Financial Horse!

Should stock market decline in the future with higher interest rate, won’t bond price decrease in value as well ?

If true, then one would own a much reduced bond and equity/Reit asset value in the next recession ?

A stock market decline usually results in lower interest rates, and correspondingly higher bond prices. Under traditional investment theory, bonds and equities are inversely correlated, hence the 60:40 equity bond portfolio, as the bond component will smooth out losses in the equity component.

Further, these are Singapore government bonds, which are far less volatile than corporate or EM bonds.

https://imgur.com/cjn1HnT.jpg, Hyflux piece of land that ESR holding is a goldmine

Interesting, I’ll have a closer look at this, but would you care to share your thoughts on why its a goldmine? My concerns with ESR were mainly because I am not sure if the manager can provide sufficient value add.

hi there FH,

thanks for your blog. I do enjoy reading it and it’s good food for thought.

I have a question: considering your article on Netlink Trust a few weeks after this article, would you add that stock to the portfolio instead?

Hi there!

Yes that’s a good point. I really like Netlink trust, and I think it can definitely form a key part of this portfolio.

Cheers!