So the latest allotment for the Singapore Savings Bonds are out.

And I mean we all knew this round would be unpopular because the yields are a fair bit lower than the market yields.

But wow, are they unpopular indeed.

Each person who applied can get up to $42,500.

As compared to last month’s Singapore Savings Bonds where each person gets only $13,500.

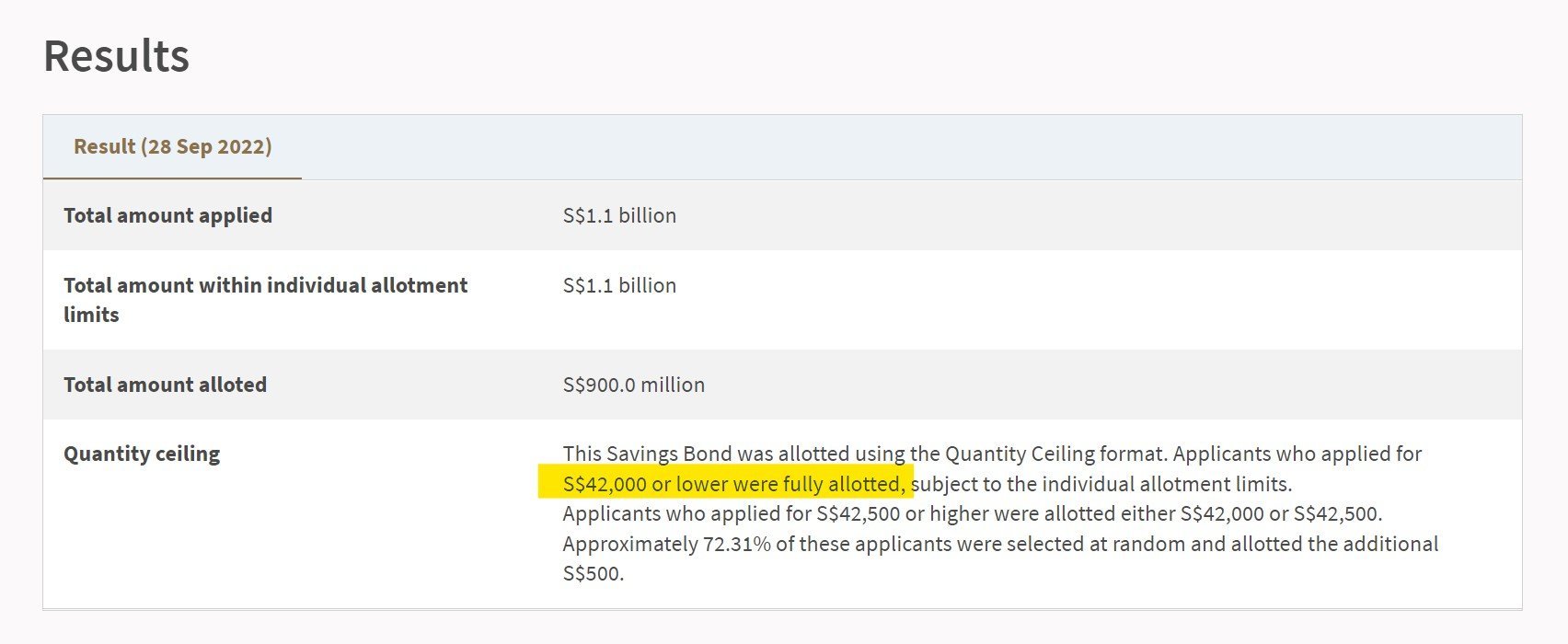

October 2022 Singapore Savings Bonds – Allotment Results

Diving deeper into the numbers.

The October Singapore Savings Bonds received $1.1 billion worth of applications, which is a fair bit lower than the September Singapore Savings Bonds at $1.9 billion.

Issue size is exactly the same at $900 million.

Each person has a chance of getting either $42,000 or $42,500, with a 71% chance of getting $42,500.

Why are October Singapore Savings Bonds less popular than September / August?

I don’t think it takes a rocket scientist to figure this one out.

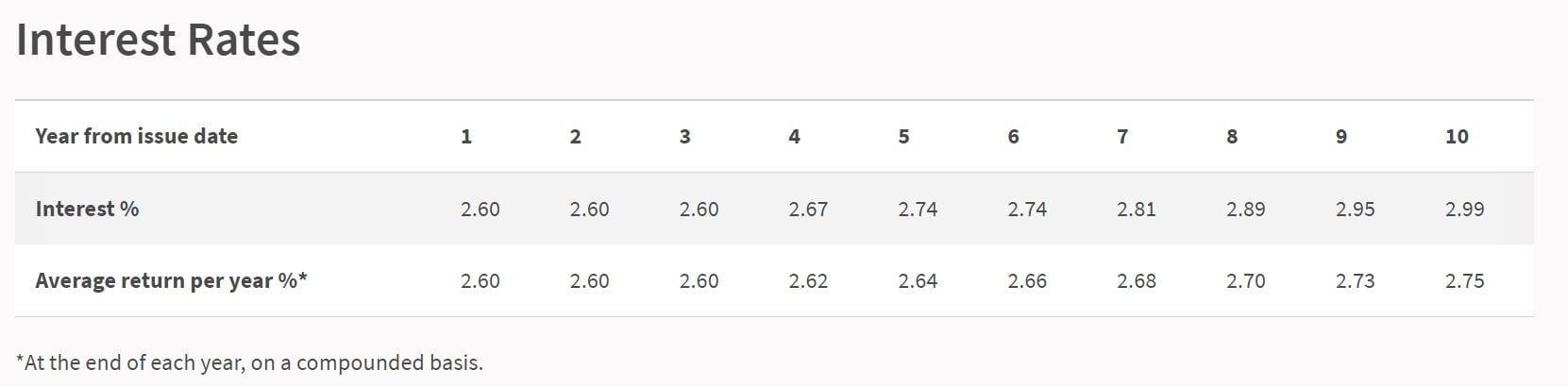

The October Singapore Savings Bonds yield:

- 2.6% for the first year

- 2.75% for 10 years

Whatever way you spin it, those yields are terrible compared to what the market is offering now.

Latest T-Bills yield 3.32%, which are likely to go up even higher after the Fed Rate Hikes.

Whereas the latest 10 year SGS yields 3.36%, a fair bit higher than the October Singapore Savings Bonds (2.75%).

What am I doing with my Singapore Savings Bonds?

I increased my application for the October Singapore Savings Bonds by quite a bit because I expected them to be unpopular.

That seems to have paid off.

As shared previously, while the yields are lower than market yields, I still like Singapore Savings Bonds for the liquidity they offer.

As long as you submit a redemption before the end of month deadline, you get all the money back (with accrued interest) at the start of the next month.

This liquidity is something that you don’t really get with T-Bills.

And with Singapore Savings Bonds, you’re also given the option to hold up to 10 years, in the event interest rates are cut down the road.

In any case – With this latest round of allotments, I am fully maxxed out on Singapore Savings Bonds.

Going forward, I will be redeeming my 2019 Singapore Savings Bonds, and refreshing them into the latest market yields.

Some of the 2019 Singapore Savings Bonds yield 1.7% even in their 4th year, so it’s a no brainer to redeem and refresh them.

As always, love to hear what you think!

Refinancing tool

With rapidly rising interest rates – it might pay off to look into refinancing if your loan is coming due.

There’s a by Property Guru.

Do give it a try if you’re close to refinancing.

It’s completely free – you just input your mortgage details, and the tool lets you know whether you’ll save money by refinancing.

If the answer is yes, they’ll give you recommendations on what loan to take.

If the answer is no, you can set up a reminder for the tool to remind you when its time to refinance.

I did the same for my own mortgages and found it pretty useful.

Do give it a try .

Can you redeem old ssb and buy new ones same time? Esp when you have hit yr max limit?

Yes, that’s possible.

If I am not wrong…

Redemption applications can only be lodged during the 1st four business days of the month.

Redemption amount along with any accrued interest, will be credited to the linked CDP account on the 2nd business day of the following month.

Ooooops….

Pl ignore my earlier post on redemption, my interpretation was wrong.

Np! Yes you have the whole month until the last few business days of the month to put in a redemption notice 🙂

Dear FH,

T-Bill yields have been high recently in spite of its relatively poorer liquidity compared to SSB. But SSB rates are comparatively lower even though it has better liquidity that T-Bill.

Since both products are govt-guaranteed and somewhat similarly positioned in terms of tenor, ie 6 mths for T-Bill and 1 mth (minimum) for SSB, one would expect the yield/interest rate to rise (or fall) in tandem. But that is not happening. Why? Tks.

Hi VS,

Yes I explained the mechanics in this article: https://financialhorse.com/latest-singapore-savings-bonds-yield-2-75-why-are-interest-rates-going-down/

It is due to how the SSB yields are calculated, which tracks the average SGS yields over the past month, and are smoothed out so that short term yields will not be higher than long term yields.

Long story short – SSB yields should get better the next few months.