The latest results for the OCBC Financial Wellness Index are out!

The OCBC Financial Wellness Index comes from an annual survey of 2000 working adults (between 21 and 65), with 10 questions to judge participants’ financial health.

The biggest takeaway from the results?

Singaporeans are not prepared for retirement.

And the biggest culprit?

Millennials.

As a millennial myself – this really got me thinking. What are we (as an age group) doing wrong here?

Are you ready for retirement?

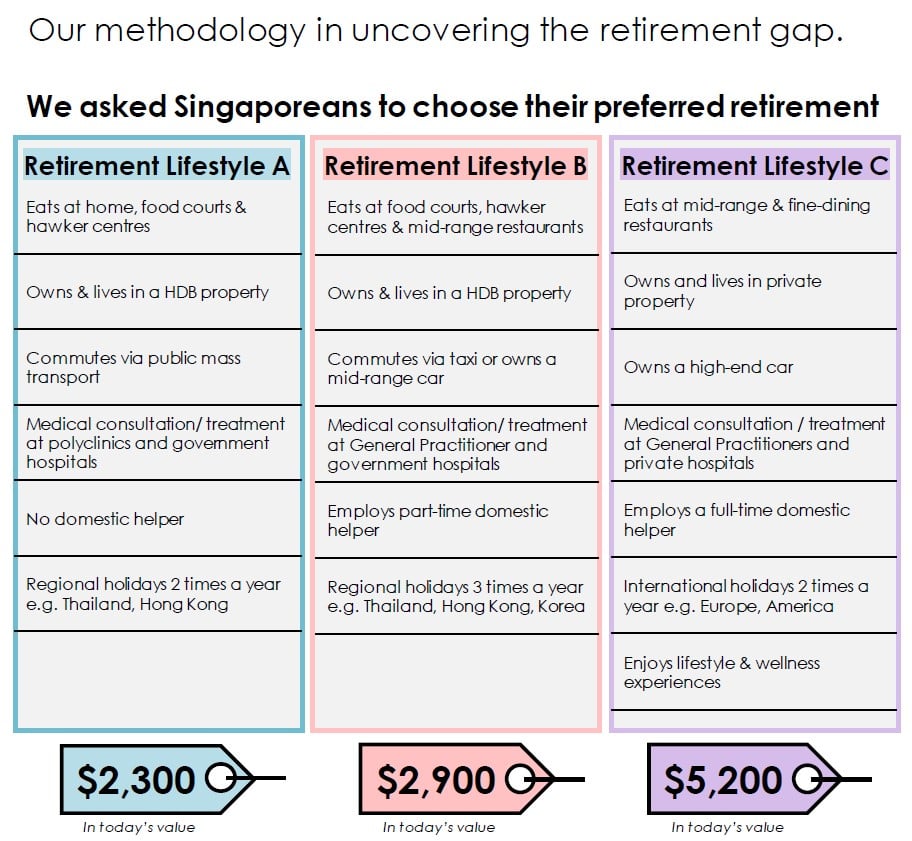

The methodology that OCBC used is really interesting.

There are 3 retirement lifestyles set out below:

- Lifestyle A – Frugal

- Eats primarily at home, hawker centers/food courts, takes public transport, resides in HDB with no helper, government medical care, and holidays to nearby countries 2x a year

- Lifestyle B – Medium Expenditure

- Eats at a mix of food court and restaurants, commutes via taxi/car, resides in HDB with part time helper, government medical care, and regional holidays 3x a year

- Lifestyle C – YOLO Retirement

- Eats at fine dining restaurants, drives a high-end car, resides in private property with full time helper, private medical care, and international holidays to Europe/US 2x a year

Pick the retirement lifestyle you want and note down the amount you need per month in retirement. From this rate, work out how much you need in retirement, assuming you retire at 65 and budget for 20 – 25 years.

Based on your current savings, savings rate, and your investment rate, would you have enough?

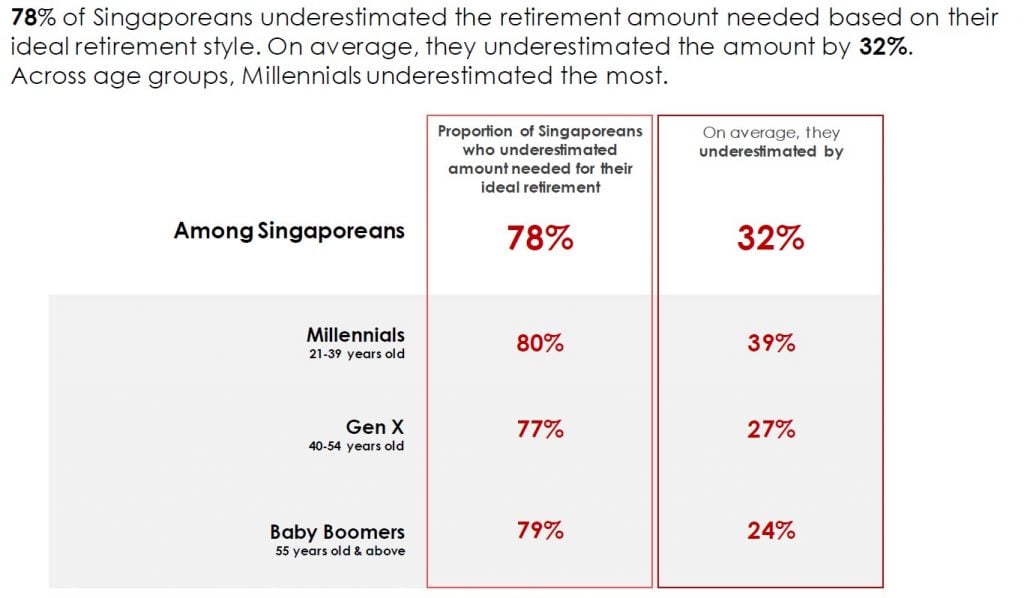

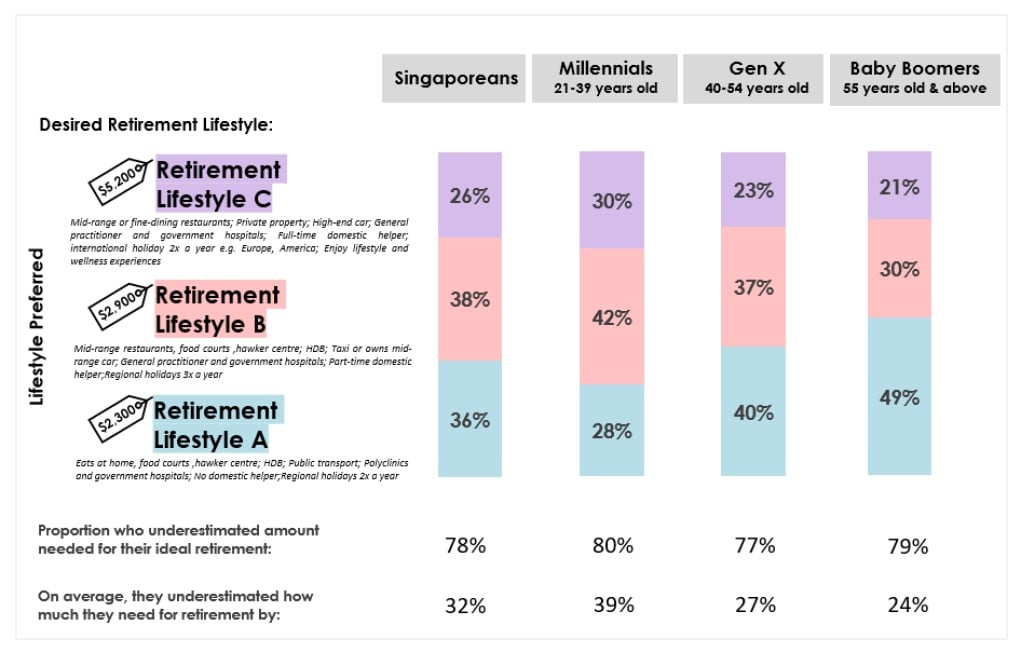

The conclusion across all age groups?

Almost all age groups underestimate the amount they need for retirement (78%), and they underestimate by about 32% on average.

Here at Financial Horse we’re dedicated to improving financial literacy and investment competency for Singaporean investors, so it was something that we really wanted to help address.

Successful wealth management always involves 2 steps:

- Making money (increasing your income and decreasing expenses)

- Investing money

Many Singaporeans work hard on step 1, while neglecting step 2.

And over time, the value of your purchasing power just gets eroded away by inflation.

The past 20 years are a fantastic example.

Compare a person in 2000 who kept all his savings in cash, versus another who bought private property and stocks.

Who do you think would come out ahead?

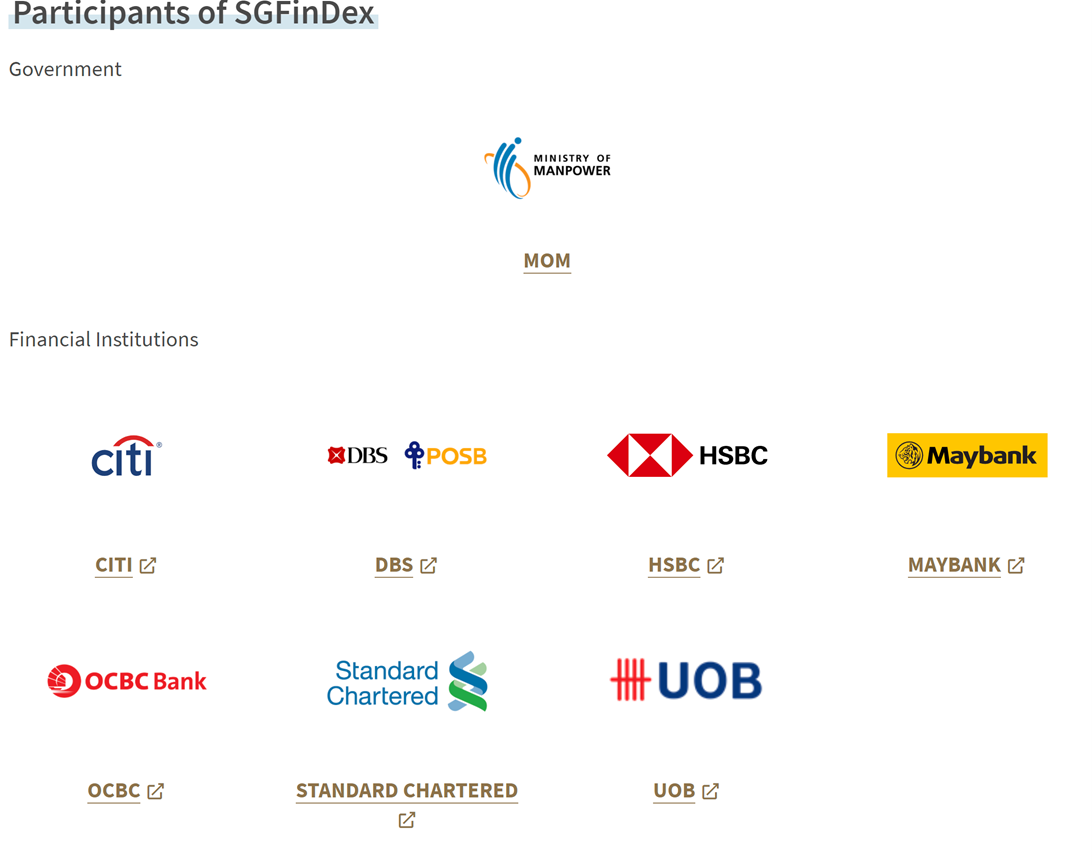

SGFinDex Platform

To help with this, the government stepped in with the Singapore Financial Data Exchange (SGFinDex). This allows you to connect all your bank accounts, so that you can view your finances in one place. The participating banks are set out below.

SGFinDex is just the underlying architecture. To actually use it to generate meaningful results, you will need to view it from a bank’s App.

Word on the street is that OCBC’s is pretty well done, so I tried it out myself.

To access it, you need to:

- Login to the (or )

- Go to Your Financial Oneview

- Authorise OCBC to access SGFinDex

You can then see all your bank accounts consolidated in the including:

- Savings accounts

- CPF

- IRAS

- Credit Card

- Loans

There are some limitations in SGFinDex though, that doesn’t allow the following to be captured:

- Shares held in CDP

- Shares held in custodian

- Amex credit cards

- CIMB accounts

But without a doubt, SGFinDex is way better than the previous solution (which was basically Excel and manual work).

Being able to see all your savings accounts, CPF, credit card, and loans from a single bank’s app, is great stuff.

OCBC Life Goals – Achieve your financial goals

The also includes OCBC Life Goals.

This helps you run the retirement calculation we talked about at the start of this article (based on the OCBC Financial Wellness Index).

The steps are:

- Decide how much you will spend each month in retirement

- Simulate how much you will have based on:

- How much you have now (this is auto populated once you’ve consolidated your financial data on OCBC’s Your Financial OneView)

- How much you will save each month

- How you invest (expected returns)

All your bank accounts, expenses, and credit cards are linked to SGFinDex, so it saves a lot of time if you’re the kind that has bank accounts and credit cards everywhere.

Really great stuff.

Even if you don’t plan to invest with OCBC, it’s worth logging into the app to play around with Financial OneView and OCBC Life Goals.

It really forces you to think about your retirement strategy, and whether you’re on track or need to do more.

I highly recommend it – it’s a great way to kickstart 2021, right before Chinese New Year.

What next?

Once you do the retirement planning, it’s your call entirely on what to do next.

If you’re on track, then congratulations and no action required.

If you’re not on track, then you probably need to do something about it. That’s the whole mission of Financial Horse after all – to help investors plan their finances and invest for their future.

What the can do is (1) help manage your finances, and (2) offer Investment options.

(1) Manage your finances

The helps you manage your finances by making it easy to track:

- How much you save – you can set savings goals and the App will offer personalized insights and nudges to keep you on track

- How much you spend – to manage your expenses

- How much debt you have – to consider paying down some or reducing new debt

(2) Investment Options

You can also invest within the . Options include:

- OCBC RoboInvest

- Shares (via OCBC’s Blue Chip Investment Plan – with either cash or SRS)

- Unit Trusts

Closing Thoughts: Worth a try?

From the OCBC Financial Wellness Index, it’s clear that most Singaporeans are not well prepared for retirement.

And with the rate at which prices keep going up, it’s not hard to see why.

However, not thinking about it, and pretending it isn’t there, doesn’t make the problem go away.

With the consolidation of your financial informaton on , enabled by SGFinDex and OCBC Life Goals, it really has become much easier to keep track of all your finances in one place, and calculate if you’re on track for retirement.

If you’re one of those with your accounts all over the place, and you’ve been avoiding strategizing your finances, I think the can really help.

Depending on the results, you can then decide whether you’re on track, or more action is required.

It’s completely free too, so it doesn’t hurt to login and give it a try.

Who knows, it may just change your financial life. ????

Note: This post was sponsored by OCBC Bank. All views and opinions expressed in this post are from Financial Horse.

Check out our FREE Guide to Investing, and join our Telegram Group for weekly updates!

2021 Stock Watch: Support the site as a Patron member and get premium content & stock watch across 3 markets!

May I ask what HDB (property) stands for? I tried to find an explanation, but this shorty is the meaning it seems.

We (as a couple) have now exactly 5220 SGD monthly. We count to 92years with zero interest/gains. We can live of 15% of income. Our secret is work in tranquil concentration – we do not own smartphones or anything which peeps us out. OCBC would not want us as clients. 🙂

Thank you very much for your kind answer.

HDB stands for Housing Development Board – it’s basically public housing in Singapore. 🙂

That’s an amazing story, and I must congratulate you on this. Really happy for you and your retirement planning. Literally the holy grail of these apps.

Personally I can’t imagine living without a smartphone anymore these days though, so the fact that you can is really impressive!