So the latest allotment for the September Singapore Savings Bonds are out.

I was pretty surprised by the results actually.

Each person who applied can get up to $13,500.

As opposed to last month’s Singapore Savings Bonds where each person only got up to $9,500.

That’s a pretty nice increase in allotment, especially considering the 1st year interest rate jumps from 2.0% (last month) to 2.63% (this month).

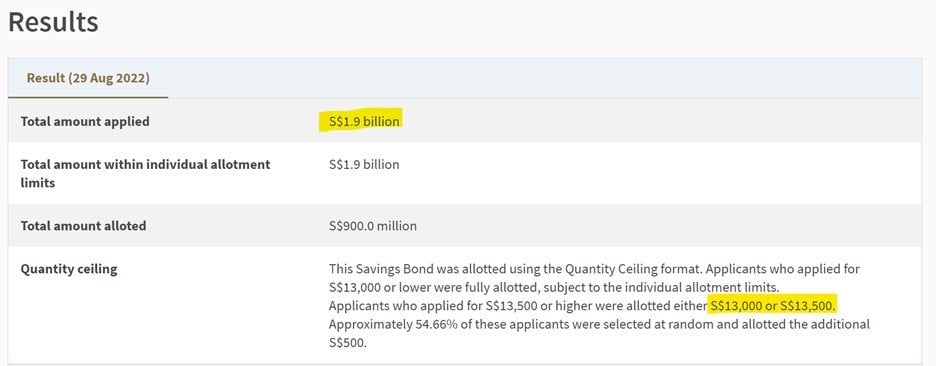

September 2022 Singapore Savings Bonds – Allotment Results

Diving deeper into the allotment numbers.

The September Singapore Savings Bonds received $1.9 billion worth of applications, which is a fair bit lower than the August Singapore Savings Bonds at $2.4 billion.

The issue size this time around is larger at $900 million ($700 million for August).

Each person has a chance of getting either $13,000 or $13,500, with a 54% chance of getting $13,500.

Frankly speaking, that’s a much better allotment than I was expecting, so I was pretty pleased with the result.

Why are September Singapore Savings Bonds less popular than August’s?

What puzzled me was why the demand for the September Singapore Savings Bonds was so much lower than August’s Singapore Savings Bonds.

I might be missing something here (and if I do please let me know).

But the way I see it, there’s 2 possible reasons:

- Investors are attracted by long end interest rates

- Investors have no more money

1. Investors are attracted by long end interest rates

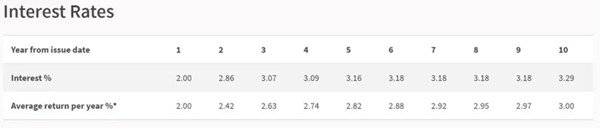

For reference, here’s the interest rates for the latest (September) Singapore Savings Bonds:

And here’s last month’s (August) Singapore Savings Bonds:

The key difference, is that:

- 1-year interest rates have gone up dramatically– 2.0% to 2.63%

- 10 year interest rates have gone down slightly – 3.0% to 2.8%

I suppose one way to see it is that investors are drawn by the headline 10 year yield.

Last month’s was 3.0%, this month’s was 2.8%, so they preferred last month’s.

Perhaps a lot of investors are looking to hold these Singapore Savings Bonds for the full 10 years, so they care more about the 10 year return rather than the 1 year return.

2. Investors have no more money (for Singapore Savings Bonds)

Another way of seeing it is that investor liquidity is drying up.

Perhaps the money has gone into last month’s Singapore Savings Bonds, perhaps it’s gone into stocks/REITs after the recent rally, or perhaps its gone into paying for the higher cost of living.

To the point where they don’t want to park their money in Singapore Savings Bonds anymore.

Who knows.

I would love to hear what you guys think on this.

BTW – we share commentary on Singapore Investments every week, so do join our Telegram Channel (or Telegram Group), Facebook and Instagram to stay up to date!

I also share great nuggets of wisdom on Twitter.

Don’t forget to sign up for our free weekly newsletter too!

[mc4wp_form id=”173″]

What am I doing – Singapore Savings Bonds vs T-Bills vs Singapore Government Securities?

Whatever the case, this is a welcome development for me.

I still have a whole bunch of Singapore Savings Bonds from 2018 that I want to redeem and refresh at the latest (higher) interest rates, so a higher allotment is a good thing in my books.

In fact I was actually considering plonking a whole chunk of my liquidity into 6 month T-Bills yielding 2.98% p.a. before this.

But as I covered in a previous article, with T-Bills you’re really sacrificing the liquidity, as it’s not easy (read: close to impossible) to get the money back before maturity.

Singapore Savings Bonds are a far superior product in my view, which allows you to get the money back any month (with accrued interest), while also allowing you to hold onto them for the full 10 years if you have no need for the money.

Personally I do see myself redeeming a good chunk of these Singapore Savings Bonds in the next 1 – 2 years to deploy into markets, so frankly I care much more about the short term interest rates than the long term interest rates here.

In any case, no change to my plans for now.

Will continue applying for Singapore Savings Bonds every month, and using it to refresh my 2018 Singapore Savings Bonds once my $200,000 is hit.

At this rate, it would still take about a year or more to fill up the full $200,000 limit!

Refinancing tool

With rapidly rising interest rates – it might pay off to look into refinancing if your loan is coming due.

I know a lot of you have been writing in for my views on fixed vs floating loans, and I plan to write a full article for this.

In the meantime, there’s a by Property Guru.

Do give it a try if you’re close to refinancing.

It’s completely free – you just input your mortgage details, and the tool lets you know whether you’ll save money by refinancing.

If the answer is yes, they’ll give you recommendations on what loan to take.

If the answer is no, you can set up a reminder for the tool to remind you when its time to refinance.

Do give it a try .

Another possible reason is people simply gave up. With such low allocations last month, they didn’t bother to apply.

True… good point.

Maybe they’re waiting for interest rates to go up further

True… possible too. Although with allocations this tight, could just apply first and redeem later if rates indeed go up significantly.

But agree this is possible. Another reason I thought could be that investors have put their money into T-Bills at the juicy 2.98% yield.

the pot of money offered (issue) grew larger as noted by you. I find that the likely reason why the allotment went up (assuming the same group of ssb lovers applied). and yes, agree on those who are waiting for rates to go up further!

True! Appreciate the sharing!