Remember when Shopee (Sea) stock used to be the hottest thing since sliced bread?

Yeah… this horse is old enough to remember that… when Sea was worth more than double DBS’s market cap.

Since it’s high of $372 in October 2021, Sea stock has fallen a whopping 81%.

After reporting a poor set of 2Q 2022 financial results this week – Sea’s stock price fell another 17%.

So… is Sea stock finally a good buy at this price?

What was my conclusion in January 2022 – with the share price at $154?

I last looked at Shopee (Sea) stock back in January 2022, when the share price was at $154.

My conclusion then was that I like the execution and the growth, but I hate the global macro.

I thought it was too early to open a long term position in Sea, given that the Feds would be aggressively tightening monetary policy going forward.

That’s not the kind of climate you want to go long on loss making tech stocks.

8 months on, I’m pretty excited to refresh my view on Shopee (Sea) actually.

Shopee (Sea)’s Second Quarter Earnings

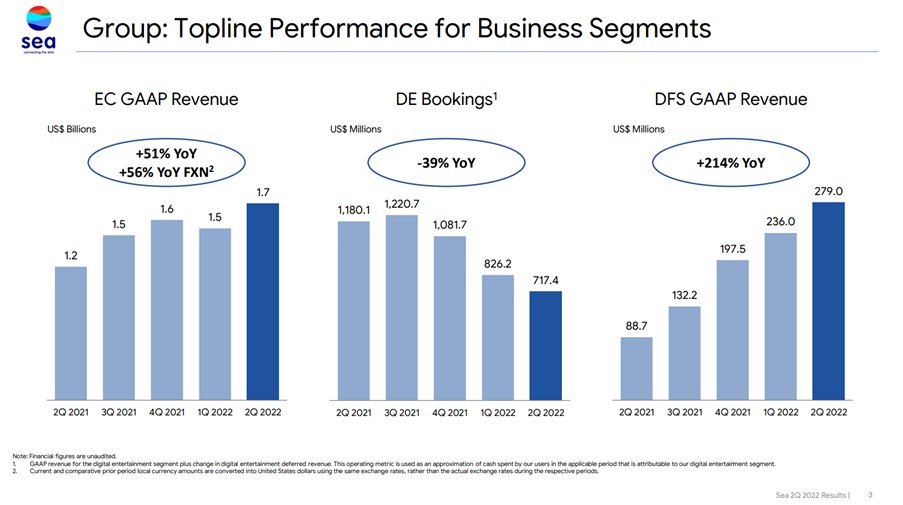

Here is Sea’s latest earnings split by business segment.

To sum up:

- E-Commerce (Shopee) is still growing revenue, but growth is slowing. ECommerce is still bleeding cash and losing a ton of money

- Gaming (Garena) is still the big money maker, but the revenues are declining at a pretty scary pace – down 39% year on year.

- Fintech (Sea Money) is growing well, but is too small to contribute meaningfully to the bottom line. And it’s still bleeding cash.

So basically, you have a company where the gaming business is the cash cow, but where the profits are declining rapidly.

Which means e-Commerce needs to step up and contribute to the bottom line, because Fintech is not going to do it anytime soon.

Key Takeaway from the Shopee (Sea)’s Earnings Call – Profitability over Growth

In case it wasn’t already clear, Shopee (Sea)’s focus is on profitability over growth these days.

Here’s Forest Li making it crystal clear (emphasis mine):

During the pandemic lockdown, we rapidly scaled our businesses to answer to the fast-rising market demand for online consumption and services.

As a result, we significantly expanded our businesses and the total addressable market and strengthening our market leadership while improving growth efficiency. We were able to achieve these results by focusing on doing the right thing at the right time in setting our direction and being agile and adaptable in our execution. Now we are in an environment of increased macro uncertainty with rising inflation, rising interest rates, local currency depreciation against the U.S. dollar, and ongoing reopening trends.

In this environment, being agile and adaptable is even more crucial to the long-term success of our business. We believe the right thing to do at this unprecedented time is to focus even more on self-sufficiency, long-term profitability, and the defensibility in our business operations. Our results for the second quarter demonstrate the early success of this effort. Because of our strong execution in the quarter, Shopee’s unique economics improved significantly, driven by efficiency gains across our markets.

You see in an era where interest rates are zero and the Feds are pumping in $120 billion a month – money is cheap.

So you focus on growth at all costs.

With inflation at 8.5% and the Feds raising interest rates at 0.75% per meeting – money is no longer cheap.

You need to shift to stuff that investors care about, like profitability.

Forest Li was one of the first to spot this trend

To give credit where credit is due – Forest Li was one of the first Tech CEOs to spot this trend.

Earlier this year when other tech companies were still on a hiring spree, Sea already made the decision to refocus on profitability, and exit non-core market like France and Spain.

Later in the year they also started retrenching staff within their fintech arm SeaMoney, in a bid to cut costs.

They’ve also tried to monetise Shopee more – less vouchers and giveaways, and more charging sellers for ads.

But… Monetisation takes time

The problem though, is that you don’t go from burning cash to printing cash overnight.

It takes time.

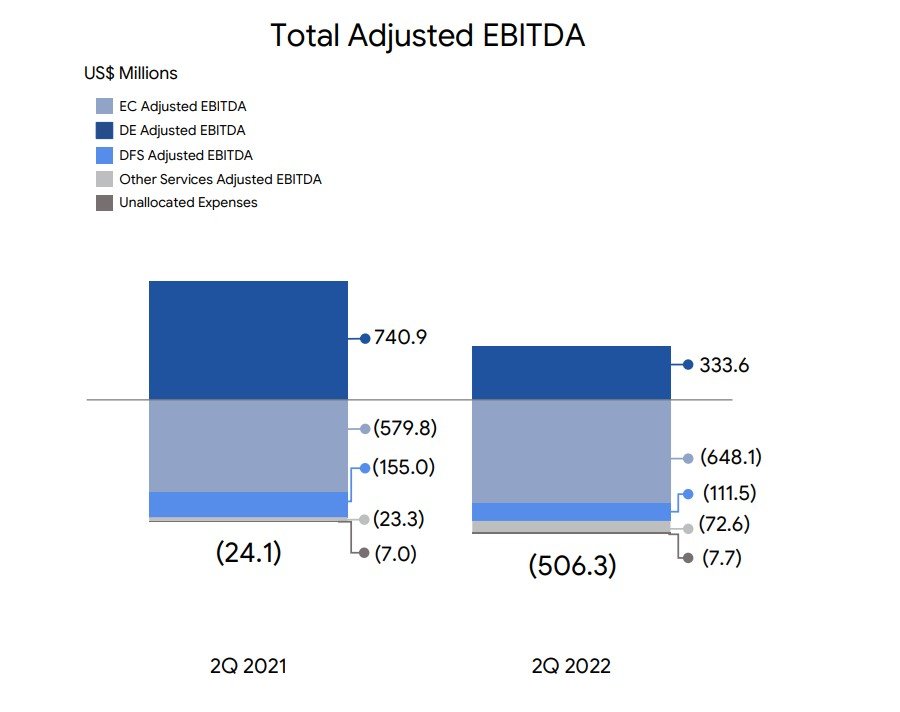

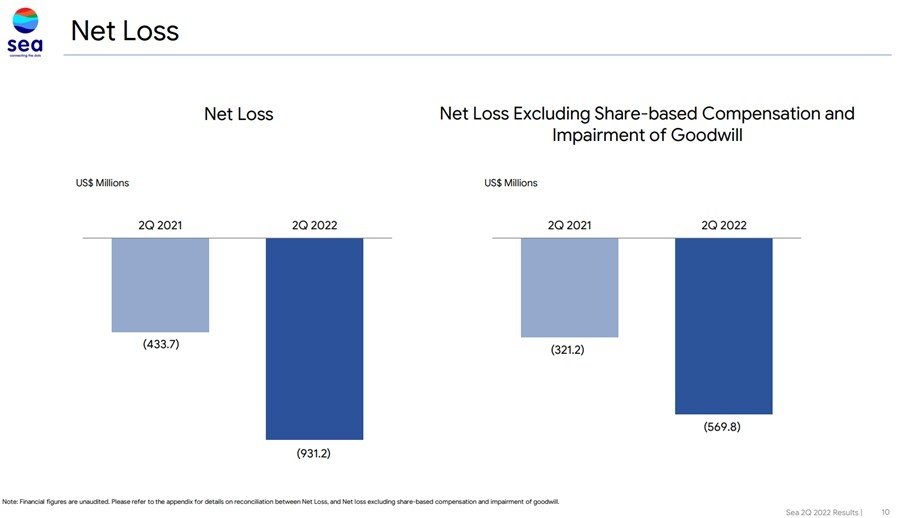

As at Q2 2022, Sea is still bleeding cash – losing $931 million a quarter:

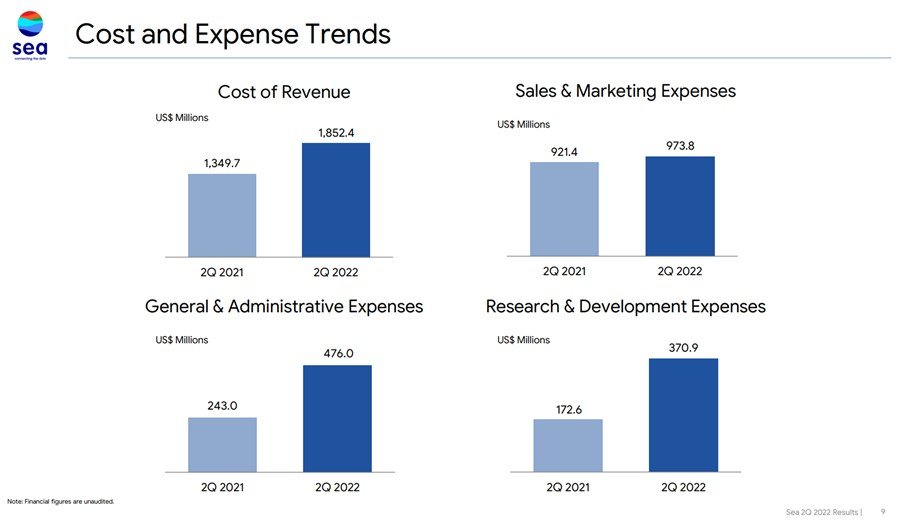

According to the earnings call they’re taking steps to cut down expenses, but when I look at the P&L it’s not so clear to me.

Yes, Sales & Marketing expenses has slowed, but the growth in R&D, General & Administrative, is still worrying.

For Sea stock to rally meaningfully in a year with poor macro, it has to come from fundamental drivers.

Either (1) the core business needs to grow strongly, or (2) Sea must succeed in monetising their core business (more).

So it’s worth discussing a bit more on each of the 2 core businesses – Gaming and Ecommerce.

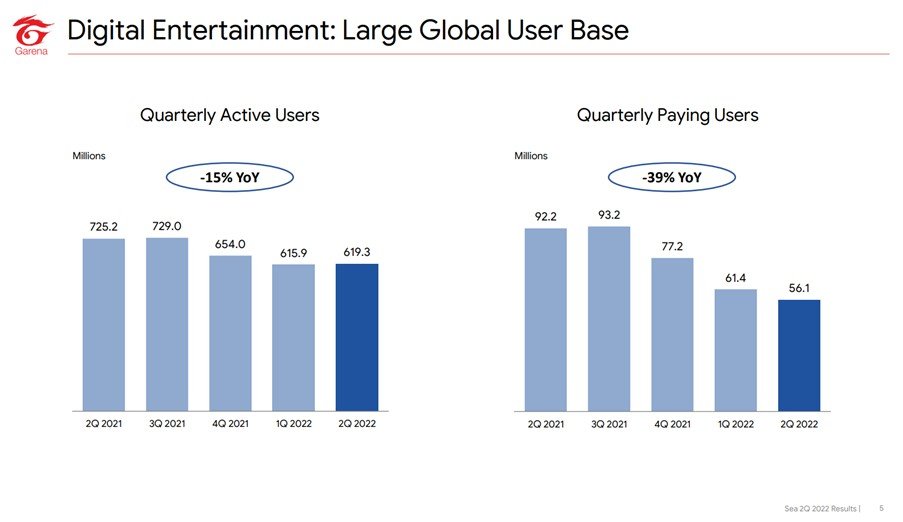

Sea’s Gaming Business (Garena) – Still bleeding Users

If you take away the gaming business from Sea, all you’re left with is eCommerce and Fintech arms that are bleeding cash.

So the vitality of the gaming business – Garena, is vital.

And within Garena, much of the earnings comes from one game – Free Fire.

The numbers are not pretty.

Quarterly active users down 15% year on year, quarterly paying users down 39% year on year.

That’s 4 consecutive quarters of declines in paying users, which is worrying.

Sure, you can put some of that down to Free Fire’s ban in India earlier this year.

But this is still a worrying sign.

And just like Tencent, Garena is overly reliant on their one hit game.

Whether they can come up with new hit games to replace Free Fire, is not so clear for now.

There are mega games publishers like Activision Blizzard, EA Games, Take Two etc that can churn out hit games after hit games. I wouldn’t really count Sea (Garena) in that camp for now. They’re more like a Tencent Gaming / Netease gaming in my view, which means the gaming business needs to be valued appropriately (less).

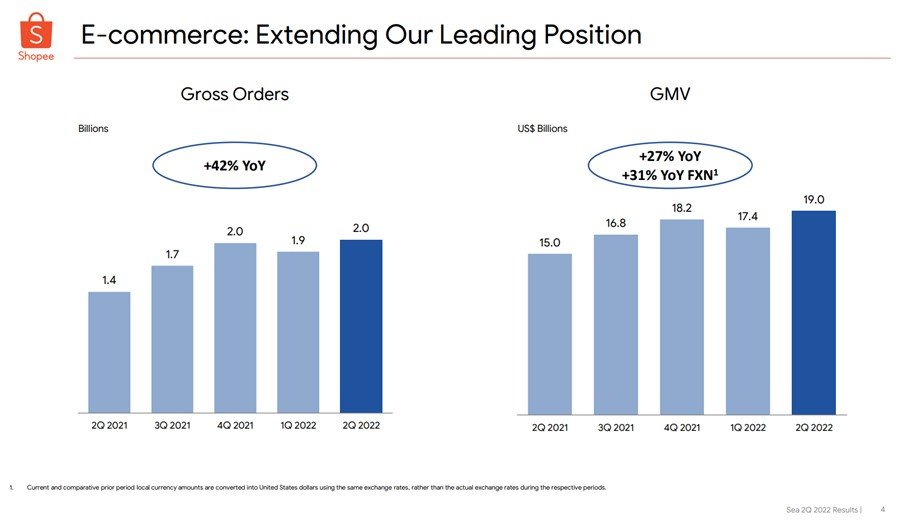

E-Commerce (Shopee) – Growth is slowing

At the same time, e-Commerce growth is slowing noticeably.

The days of 80% growth in GMV are long over.

We’re looking at 27% growth in GMV these days.

What is interesting though, is that growth is slowing more quickly for the smaller merchants.

Whereas the bigger brands are doing comparatively better.

I suppose one way of reading this is that branding still matters a lot.

This could have implications on how Shopee monetises.

Sea has done a lot more to monetise the core Shopee business, including cutting back on giveaways, and charging sellers for ads (to have their search results appear at the top of each search).

But E-Commerce is still bleeding cash, and there is a lot more Shopee will need to do on monetisation to turn that around.

As of now Shopee is still comfortably in the lead vs Lazada (3 – 4 times Lazada’s GMV), but as they start to monetise the platform more and start charging sellers, one can’t help but wonder if the competitors like Lazada or Amazon may start to catch up.

Sidenote – Refinancing tool

With rapidly rising interest rates – it might pay off to look into refinancing if your loan is coming due.

I know a lot of you have been writing in for my views on fixed vs floating loans, and I plan to write a full article for this.

But in this market – I think you’re pretty much forced into taking floating. The banks themselves know interest rates are going up quick, so the fixed rate loans are priced in such a way that they aren’t sufficiently attractive (in my view).

In the meantime, there’s a by Property Guru.

Do give it a try if you’re close to refinancing.

It’s completely free – you just input your mortgage details, and the tool lets you know whether you’ll save money by refinancing.

If the answer is yes, they’ll give you recommendations on what loan to take.

If the answer is no, you can set up a reminder for the tool to remind you when its time to refinance.

Do give it a try .

What is a fair valuation for Shopee (Sea) stock?

With a business changing this rapidly, I’m not even going to bother trying something like a Discounted Cash Flow analysis.

I’m just going to be super broad brush here.

Optimistic Scenario for Shopee (Sea)

Shopee’s core markets of SEA, Brazil and Taiwan have a combined GDP of $4.2 tillion.

Shopee is basically an eCommerce and gaming company rolled into one, so let’s compare against the equivalent China juggernauts – Alibaba and Tencent.

Tencent at their prime was valued at US$660 billion, Alibaba at $800 billion – and China’s GDP is $14.7 tillion.

If we adjust that by GDP, that gives a potential peak valuation of $200 billion if Sea can ever achieve Tencent / Alibaba’s dominance.

Let’s say we cut that by half because of poor macro conditions, and because investors will never value South East Asia as highly as they valued China.

That works out to a $100 billion optimistic, best care scenario if Shopee (Sea) executes flawlessly.

Which is not too shabby, implies a potential 130% upside from current prices.

Pessimistic Scenario for Shopee (Sea)

In a more pessimistic scenario, let’s use Alibaba and Tencent’s current valuations.

Alibaba and Tencent’s share price have a lot of pessimism around the core business built in, and a hefty geopolitical premium for being a China stock.

Adjusted for GDP that would imply a $70-105b market cap for Sea, still a 100% upside from here.

This is interesting – it tells you that either Shopee (Sea) stock is cheap, or Tencent/Alibaba is still too expensive.

Alternatively let’s use Coupang, Korea’s dominant ecommerce player.

At a $31 billion market cap, with Korea’s GDP of $1.6 trillion, that implies an equivalent $70+ billion market cap for Sea.

Almost an 80% upside.

Okay, you can argue Coupang is in a more dominant ecommerce position, but I suppose Sea’s gaming business could make up for it.

This was very interesting for me, it indicates the market may be undervaluing Sea stock, at least relative to other tech names.

Macro Conditions – Still not favourable

My primary gripe with Shopee stock back in Jan 2022 was the poor macro conditions.

I just felt it was a year to respect the macro, and not get too cute with fundamental stock picking.

8 months on – has anything changed?

We’re now at 2.5% on the Fed Funds Rate, and we’ll be at 3.5% by end of the year.

That means the bulk of the Fed tightening is probably behind us, although higher rates and QT do lie in the future.

I wrote a more detailed macro update for Patrons this week, so do check it out for fuller views.

I’m definitely less bearish than I was back in Jan.

But I don’t think we’re at the all-clear point where I would go all-in on risk just yet.

I still want the clarity from the Feds before I do that.

Remember – the priority for me this year is capital preservation, and not necessarily capital growth. I think there will be time to switch to all-in risk when the Feds flip dovish.

But of course, this ultimately has to be a personal decision, and other investors may want to take more risk.

BTW – we share commentary on Singapore Investments every week, so do join our Telegram Channel (or Telegram Group), Facebook and Instagram to stay up to date!

I also share great nuggets of wisdom on Twitter.

Don’t forget to sign up for our free weekly newsletter too!

[mc4wp_form id=”173″]

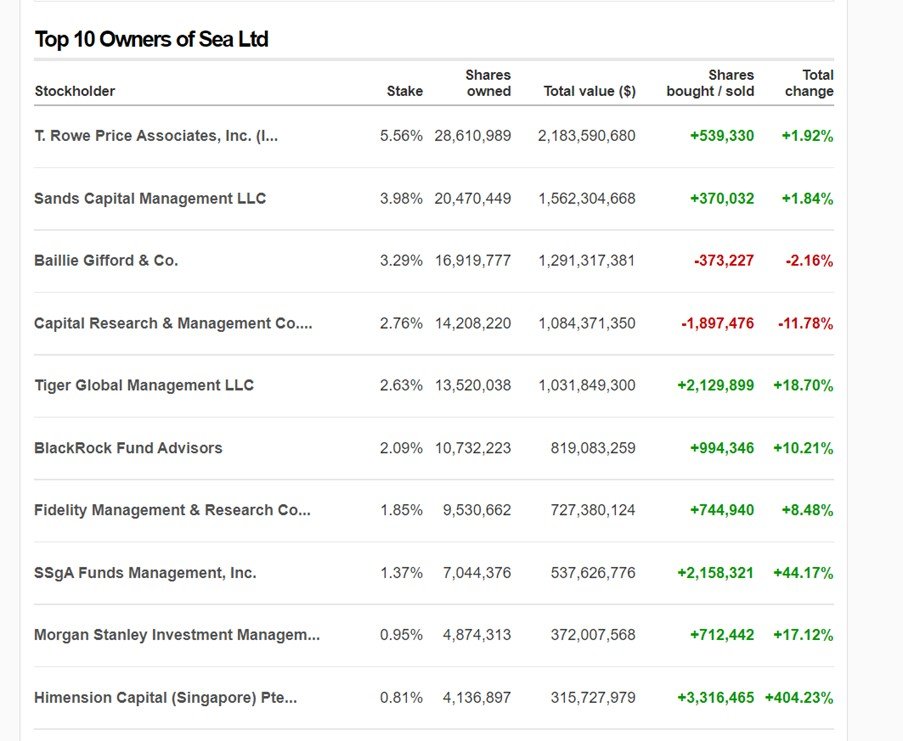

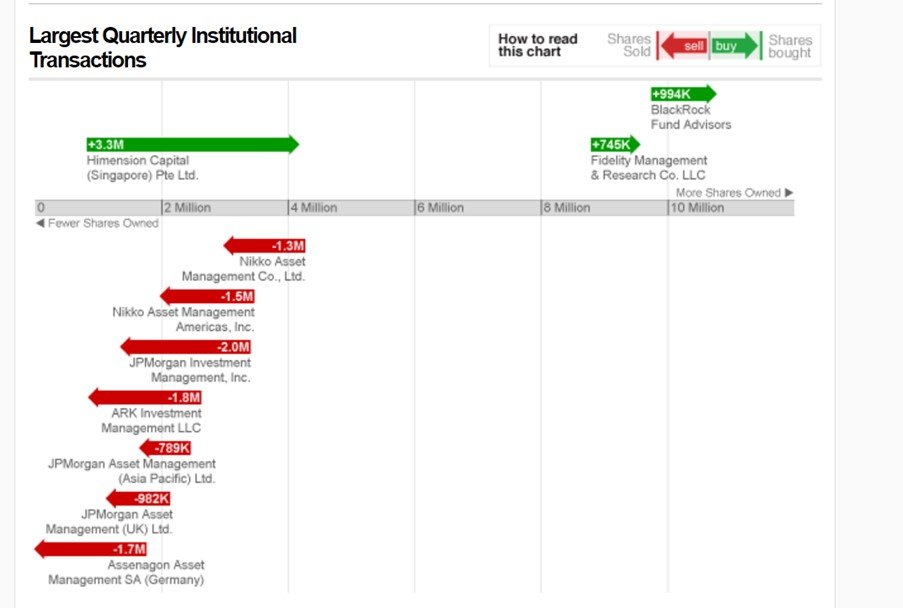

Shareholders of Sea Ltd (Shopee)

Lots of big name shareholders of Sea, including T Rowe and Blackrock (I’m not sure you count Tiger Global as a big name anymore after their fiasco).

Himension Capital (Singapore) opened a big position in Sea this quarter.

I did some digging around but there’s not much information on them available, although the founders are Chinese which is interesting.

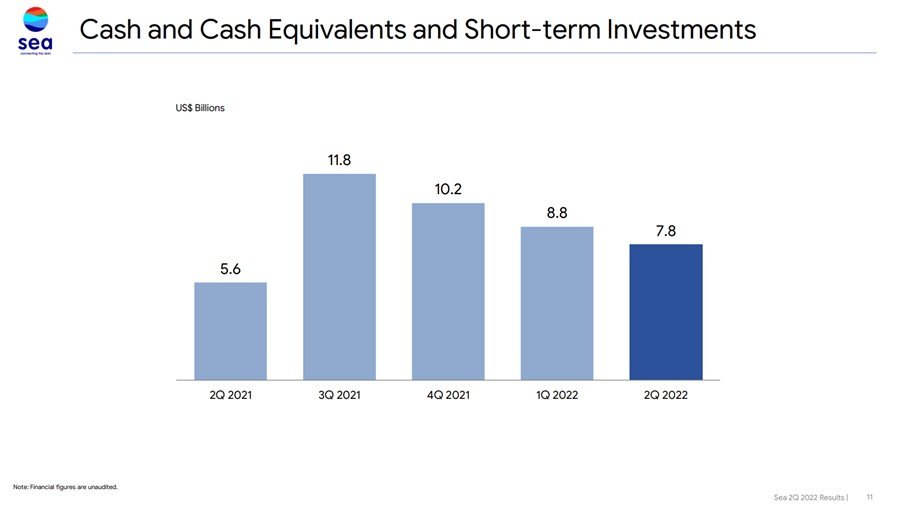

Balance Sheet of Shopee (Sea)

For what it’s worth, balance sheet is rock solid with US$7.8 billion in cash at quarter end.

Will I buy Shopee (Sea) stock at $67?

Full disclosure that I do not currently hold any position in Sea Ltd stock.

What I like about Shopee (Sea)?

I actually like Shopee (Sea Ltd) a lot more at this price today than I did back in Jan 2022.

I think in Forest Li you’re getting a determined and scrappy founder who wants to make a name for himself.

I think in Shopee you’re getting the dominant e-Commerce platform in South East Asia, Taiwan, and Brazil (for now).

I think in Garena you’re getting the existing Free Fire Cash cow, and a regional games distribution platform.

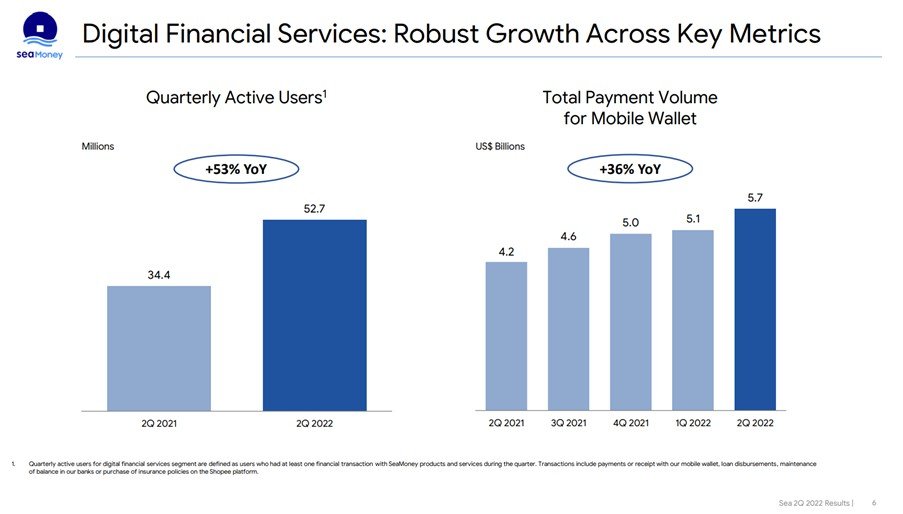

Sea Money is a big wildcard, but I think you can think of it as a long dated OTM call option on Forest Li somehow being able to pull it off.

Total Payment Volume for Sea Money is at $5.7 billion for Q2 which is not too shabby.

And valuations wise – if you compare with other eCommerce players like Alibaba and Coupang, the stock does look cheap here.

What I don’t like about Shopee (Sea)?

The problem remains the global macro conditions.

As a long-term investor, investing through multiple business cycles – you need to know when it is time to swing for the fences, and when it is time to just preserve capital.

We’re definitely getting closer to the point where I would want to swing for the fences, but I don’t think we’re there just yet.

You can get 3.5% yield on cash by end of the year, absolutely risk free.

That’s not really the kind of climate I want to load up on risk.

I probably still want to be flat on risk, until macro conditions improve.

And fundamentals wise – Shopee will need to execute a tricky transition from growth to profitability, in a year with unfavourable macro. All while cutting headcount and operation costs.

Whether they can do it remains to be seen.

Although you could probably argue that at current prices, quite a lot of pessimism is already baked into the stock.

Technicals wise – Shopee (Sea) stock bottomed at 54 in June, so if you are looking to build long term positions that would be a crucial price to watch.

Closing Thoughts: I like Shopee (Sea) stock

For what it’s worth – I do like Shopee (Sea) stock.

It’s going to be a 3 horse rating for me (out of 5).

Depending on how macro conditions and share price play out the next 3 – 6 months, I may very well open a position.

I will share my updated views on Patreon as and when I decide to do so, so do sign up if you are keen.

You can also see my full stock / REIT watchlist on Patreon. Will be updating the watchlist this weekend given the big changes in share prices the past few weeks.

Refinancing tool

With rapidly rising interest rates – it might pay off to look into refinancing if your loan is coming due.

I know a lot of you have been writing in for my views on fixed vs floating loans, and I plan to write a full article for this.

But in this market – I think you’re pretty much forced into taking floating. The banks themselves know interest rates are going up quick, so the fixed rate loans are priced in such a way that they aren’t sufficiently attractive (in my view).

In the meantime, there’s a by Property Guru.

Do give it a try if you’re close to refinancing.

It’s completely free – you just input your mortgage details, and the tool lets you know whether you’ll save money by refinancing.

If the answer is yes, they’ll give you recommendations on what loan to take.

If the answer is no, you can set up a reminder for the tool to remind you when its time to refinance.

Do give it a try .

As always, this article is written on 19 Aug 2022 and will not be updated going forward.

If you are keen, my full REIT and stock watchlist (with price targets) is available on Patreon. You can access my full personal portfolio to check out how I am positioned for the coming downturn too.

Looking for a low cost broker to buy US, China or Singapore stocks?

Get 100 USD in Apple Shares with , a zero commission broker.

Get a free stock and commission free trading with .

Get a free stock and commission free trading with .

Special account opening bonus for Saxo Brokers too (drop email to [email protected] for full steps).

Or for competitive FX and commissions.

Looking to buy Bitcoin, Ethereum, or Crypto?

Check out our guide to the best Crypto Exchange here.

Do like and follow our Facebook and Instagram, or join the Telegram Channel. Never miss another post from Financial Horse!

Looking for a comprehensive guide to investing that covers stocks, REITs, bonds, CPF and asset allocation? Check out the FH Complete Guide to Investing.

Or if you’re a more advanced investor, check out the REITs Investing Masterclass, which goes in-depth into REITs investing – everything from how much REITs to own, which economic conditions to buy REITs, how to pick REITs etc.

Want to learn everything there is to know about stocks? Check out our Stocks Masterclass – learn how to pick growth and dividend stocks, how to position size, when to buy stocks, how to use options to supercharge returns, and more!

All are THE best quality investment courses available to Singapore investors out there!

FYI – We just launched the FH Property Series. Everything you need to know to buy a property in Singapore, completely free of charge.

Shopee vs Lazada….one is bleeding and the other is still profitable. In the inflationary world, I don’t see how Shopee can turn around the situation, there is only so much you can cut, fix cost and headcounts are required to keep the company running, someday later, Shopee will go into the same path like paypal or ebay…a brand that live on former glory but nobody care nowadays because there is a better and stronger alternative available :p

Haha, agree that this is a real concern. I suppose the question is that if this plays out – what is the fair valuation for Shopee (Sea) stock?

Interesting analysis, FH!

After reading, I am convinced to stay away. If upside in best case scenario is only 100-130% when comparing to Alibaba and Tencent when these are and have been highly profitable companies while SEA is a highly unprofitable company with only a one trick tired pony driving profit, then the risk return ratio is way out of whack.

At current burn rates, their cash will run out in 2 years, not a lot of time. Unless they show real signs of turning profitable at half their current valuations, it is hard to make a case to buy.

That’s an interesting takeaway! It is true that the former leaders sometimes never regain their former glory, so the same could happen with SEA. Will be an interesting stock to watch.

For those not inclined to hold on fundamentals, it’s a pretty decent stock to trade too. From the lows of 50s it’s rallied almost 60% to the 80s, could be used to trade as this market plays out.

The difference between SEA and an online retailer like amazon is that the latter has a subscription model and operates in the USA where the gdp is high. Shoppee operates in asia and south east asia where gdp (barring Singapore) are much much lower. There are also national, cultural, logistical differences and difficulties which make south east asia (though large), a poorer and more fragmented market. Shoppee is stuck selling low value items to their different customers. Garena is subject to the whims of the ccp – if the ccp should ban gaming and the monetisation of which on political grounds, there is no recourse for Garena. And this is reflected in the down trend as this has already happened once. Even their parent Tencent is subject to the whims of the ccp. Shopee money suffers from the same challenges as shopee. Large, fragmented and large poor customers with a lot of administrative and cultural barriers. SEA stock only went that high because it was in a fed fueled qe bubble as people thought it was a amazon/shopify proxy for south east asia and asia. But it isnt really. Not saying it couldn’t go back up to those valuations but if based on real business matrices, itll be a long time coming. Perhaps never.

Agree on the amazon point. Amazon also does logistics and is very vertically integrated, which is why I did not use Amazon’s valuations as a benchmark for SEA (they are different businesses like you said).

Also agree on the value of the SEA market vs USA, although what SEA has going for it is growth potential. You may argue the growth potential will never be realised, which is a valid point too.

Didn’t quite get the Garena point though. Most of their revenue comes outside China, so why are they vulnerable to CCP? It’s stuff like the India ban that is tricky.

SEA Money – Absolutely agreed on challenges. Which is why I view this more as a long dated OTM call option. Any upside is just a bonus.

I actually agree SEA went as high as it did because of the easy money. All that is over now. Whether it can go back up will depend on whether they can execute on the business. Jury is still out on that one. 🙂

rubbish co