I received this great question from a Patron recently:

Hi FH, I am applying for a S$1.2m loan from DBS.

For fixed rate, I can get 2.75% flat for 2, 3, 4 or 5 years.

Floating is minimum 2 year lock in at 3M SORA + 0.75%.

If I want to be conservative I would lock in a 5 year fixed for the shortest tenor of 9 years.

I also have the option to stump up the full amount in cash, i.e. no loan at all.

Not sure which way to go? Any advice??

Quite a few of you have been writing in about taking fixed interest rate vs floating interest rate vs paying off mortgages in 2022.

So I wanted to write this article to share my thoughts.

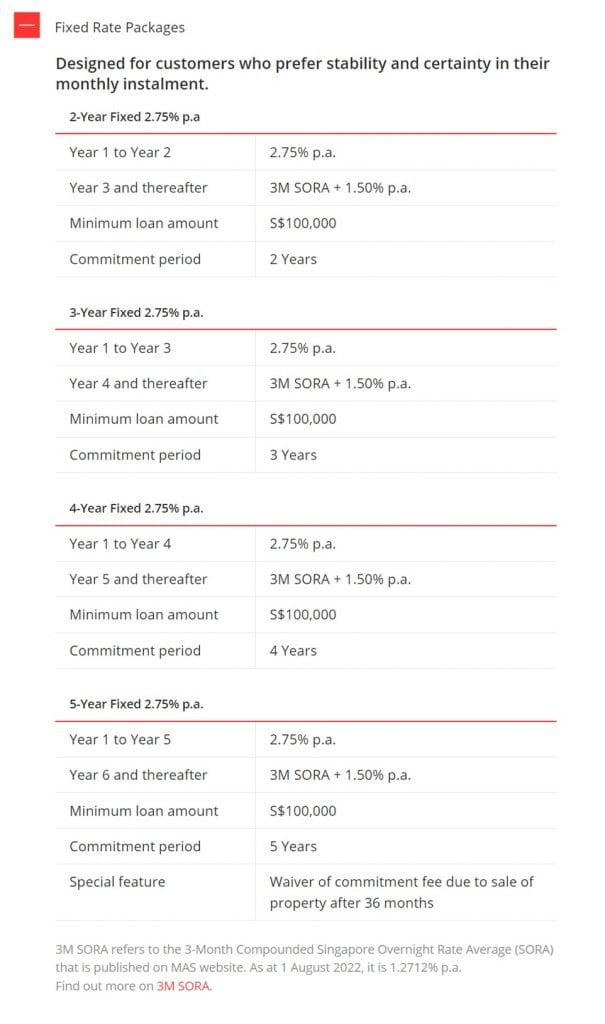

Latest DBS Fixed Interest Rate Mortgage Loans

First off – here are the latest DBS Fixed Interest Rates Mortgage Loans.

Basically, it is 2.75% for 2, 3, 4 or 5 years.

For the record, I know that you can get more attractive mortgage rates at other banks. But let’s just use DBS mortgage rates in this article for ease of reference. The thought process is the same in any case.

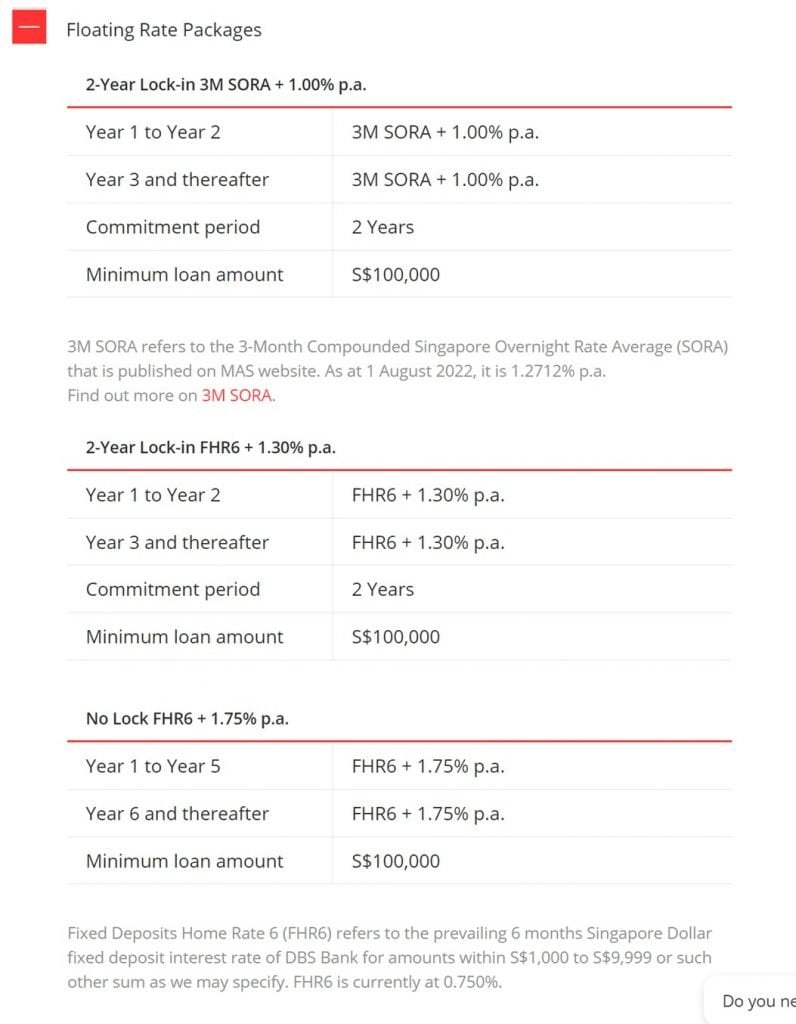

Latest DBS Floating Interest Rate Mortgage Loans

Here are the latest DBS Floating Interest Rates Mortgage Loans.

Basically, there are 3 options:

- 2 year lock in 3M SORA + 1.00% (now 2.25%)

- 2 year lock in FHR6 + 1.3% (now 2.05%)

- No lock FHR6 + 1.75% (now 2.5%)

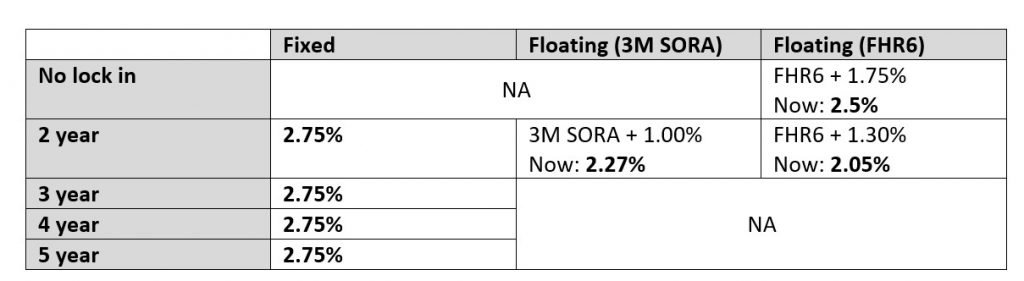

Fixed vs Floating Interest Rate Home Loan Mortgages

So to sum up, these are the options available from DBS today, if you are looking to take up or refinance your mortgage:

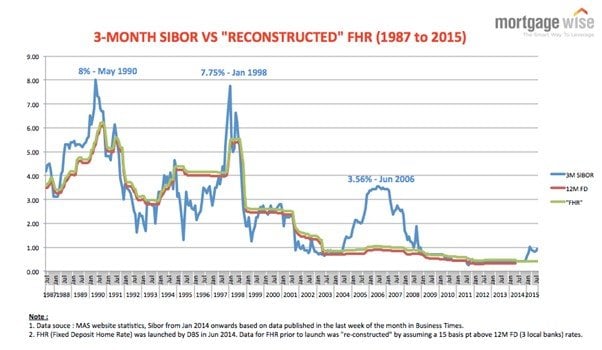

Picking between SORA vs FHR6 floating rate mortgages (SIBOR phased out)

I get a lot of questions about picking between Singapore Overnight Rate Average (SORA) and FHR6 (DBS 6 month Fixed Deposit Rate).

The difference between SORA and FHR6, very simply, is that:

SORA interest rates are determined by the market, FHR6 interest rates are determined by DBS.

So it ultimately comes down to a question of whether you could be rather be at the mercy of the market, or at mercy of DBS.

SORA being market determined will track US interest rates very closely.

FHR6 being determined by DBS, will tend to be more stable, and move with a slight lag to the market (both to the upside and downside).

The chart below gives you a good idea of how FHR6 will look like vs SORA (SORA wasn’t around back then but will look like SIBOR).

My Personal View on SORA vs FHR6?

My personal view is that I would *probably* pick a FHR6 pegged mortgage when interest rates are going up (like right now).

Because FHR6 will not go up as quickly as SORA.

Whereas when interest rates are going down (probably in 2023 / 2024), I would probably use SORA, which should theoretically go down faster than FHR6.

Should you take a Fixed or Floating interest rate mortgage in 2022? (as a Singapore Investor)

To answer this question, there are 2 key points you need to look at:

- Interest Rate Outlook

- Your personal risk appetite

Interest Rate Outlook

The logic goes like this.

If you think the Feds are going to cut interest rates in 2023 to below 2.75%, then you probably want to take floating.

If you think the Feds are going to raise interest rates to 3.75% in 2023 and keep them there for a while, then you probably want to take fixed.

That said, knowing the theory, and actually trying to predict where interest rates will go, are 2 completely different matters!

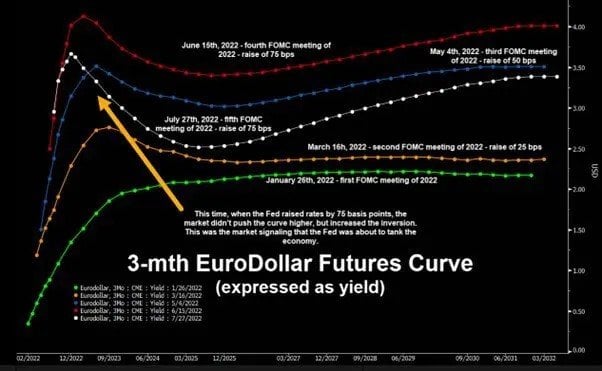

Understanding where Interest Rates may go

I shared a bit of the theory around interest rate curves in the recent article on Singapore Savings Bond / Singapore Government Security yields, so do check it out if you want more background.

The long and short is that:

- Singapore interest rates track US interest rates very closely because of the impossible trinity

- Short term interest rates are driven by Fed Funds Rate, which is controlled by the US Federal Reserve (US Central Bank)

- Long term interest rates are driven by the market, and reflect supply/demand dynamics, and market expectations as to future inflation / pricing

- The Eurodollar futures curve gives you some idea where the market sees the path of interest rates going. This changes over the time as new information comes to light, and you can see latest market probabilities here.

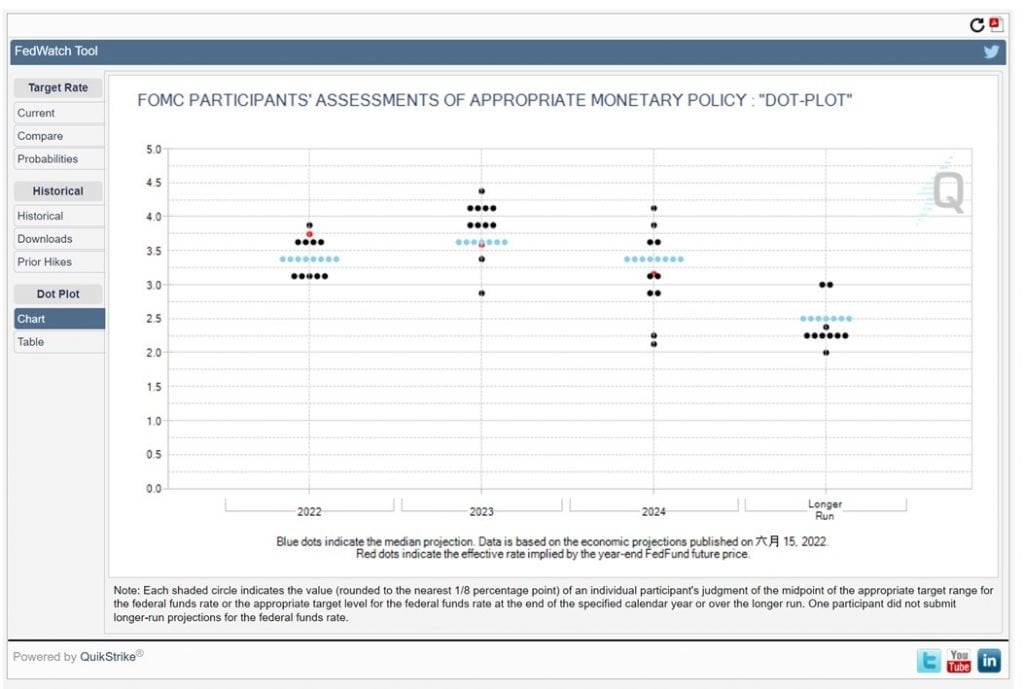

My personal view on where interest rates may go in the next 12 – 24 months?

The exact path of interest rates is always tricky to predict, so I suggest you take this with a pinch of salt.

My personal view though, is that a lot of truth lies in the Fed dot plot.

I think we’ll go to 3.5%+ by early 2023, and stay there for a while, before rate cuts in late 2023 or 2024.

The potential wildcards of course, is if (1) the economy / stock market melts down, or (2) inflation stays sticky.

If the economy or stock market starts falling apart by early 2023, then all bets are off.

In such an event, yeah I see the Feds pivoting and cutting interest rates.

Alternatively, if inflation stays sticky and refuses to go away, for example if oil prices keep going up.

Then I think there’s a risk the Feds may even hike beyond 3.5% – 3.75%, even into 4% territory.

So… Fixed Interest Rate Mortgage?

This actually means the 2.75% fixed for 2 years might not be a bad idea, because it shields you from another short-term rate hikes, while also being short enough that you benefit from rate cuts in 2024.

The downside of course, means that if I am wrong on the path of interest rates and the Fed does indeed cut in early 2023, then you do lose out on the lower interest rates.

BTW – we share commentary on Singapore Investments every week, so do join our Telegram Channel (or Telegram Group), Facebook and Instagram to stay up to date!

I also share great nuggets of wisdom on Twitter.

Don’t forget to sign up for our free weekly newsletter too!

[mc4wp_form id=”173″]

Your personal risk appetite

As you can see, when trying to predict where interest rates can go, it’s all about probabilities.

There are no certainties.

Because of this, I think the decision of whether to take a fixed vs floating interest rate mortgage loan, will also need to factor in individual risk appetite.

Think about it this way.

Are you okay to take the risk of having to pay more on your mortgage, in exchange for the potential of paying less?

Or do you want something that is fixed and predictable, that does not change for the next 2 years and allows you to plan your finances clearly.

This is a very personal decision, that only you yourself can answer.

I know some investors who cannot stand the thought of being locked in at 2.75% when the interest rates are at zero.

In which case floating may make sense.

Whereas some investors absolutely hate the uncertainty that comes with a floating interest rate mortgage, and they lose sleep at night worrying about mortgage rates going to 4.0%.

In which case just go with fixed and give yourself peace of mind.

Should you pay off your mortgage loan?

The final option the Patreon had, was to pay off his loan.

When deciding whether to pay off your mortgage loan, the key factor is:

What is the expected return on the money, if you don’t use it to pay off your mortgage?

So if the alternative is to chuck it all in REITs, and you think you can achieve a 5% return, then it doesn’t make sense to pay off a 2.75% mortgage.

But if your alternative is to place it all into the bank at 1.0% interest, then yeah I would say paying off the mortgage makes sense.

Basically – you pay off your mortgage loan, if you don’t think you can achieve a return on investment higher than the mortgage rates.

What mortgage loan would I take… in 2022?

I’m lucky in that I refinanced all my mortgages last year at ~1.1% for 2 – 3 years, so I don’t have to worry about refinancing until 2024.

But if I had to refinance today?

I think I would go for a 2 year fixed loan at 2.75%.

I know that by locking in at 2.75% I’m going to look like a fool if the Feds cut to zero in early 2023.

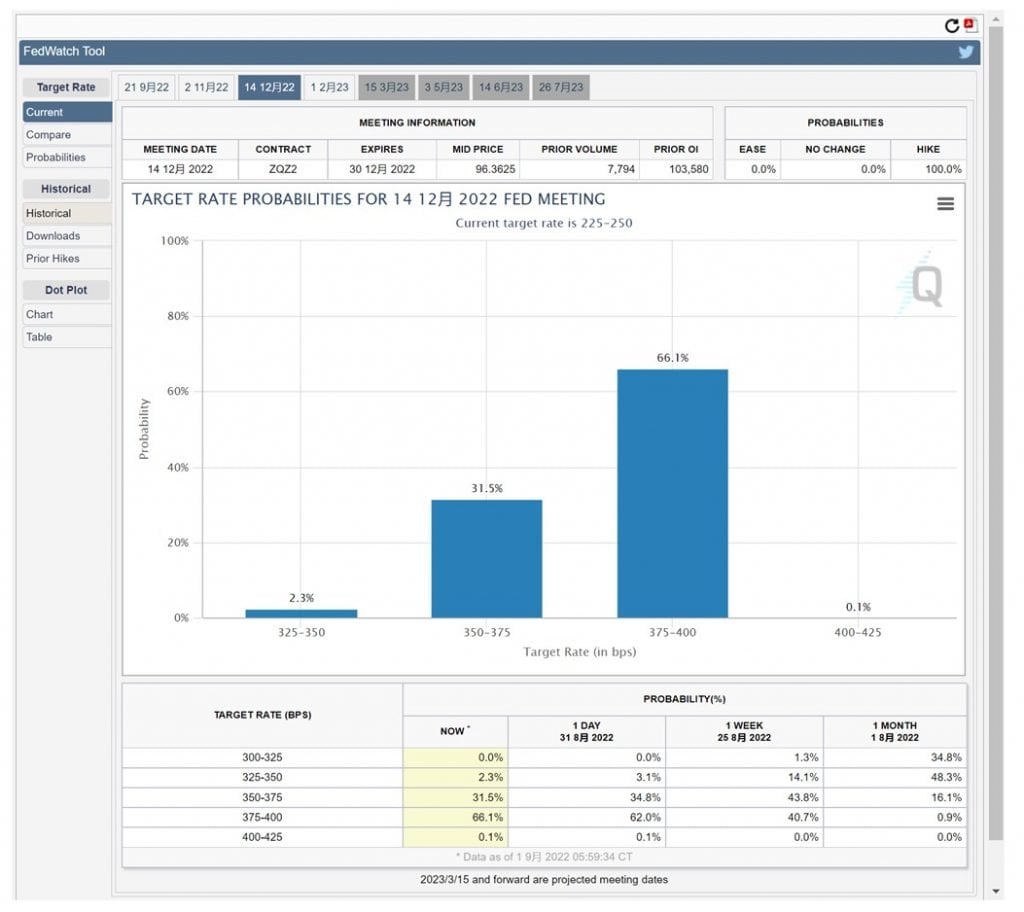

But the way I see it, by end of the year we’re going to be at 3.75% on the Fed Funds Rate:

And I just think this economy is more resilient than people are expecting.

The rate cuts will come, but not as soon as people are expecting.

I would say late 2023 or early 2024.

With a fixed rate mortgage, at least I’m enjoying the lower interest rates until the Feds start cutting.

And if I’m wrong, at least it’s just a 2 year lock-in, so I just refinance in 2024.

And I think I should be able to deliver returns better than 2.75% in the long term, so I wouldn’t pay off the mortgage.

You can view my personal portfolio and my stock / REIT watchlist on what I’m keen to buy on Patreon.

What if I’m wrong?

Of course, I admit I could be wrong on my interest rate outlook here.

If I wanted to go with floating interest rates, I think I would take the 2 year FHR6 + 1.30%.

At least that shouldn’t go up as fast as a SORA mortgage in the short term.

Use a Mortgage Broker… they provide real value add…

Now I hate to say this.

But frankly, if you are looking to take up a new mortgage or refinance your mortgage – use a mortgage broker.

In my experience, a mortgage broker provides real value add.

Okay maybe they can’t give you an in depth break down on the Eurodollars futures curve and where interest rates are headed over the next 12 months.

But they can compare all the mortgages available on the market available, and let you know which bank offers the best rates.

This alone is a huge time saver.

And if you run into problems, a mortgage broker can provide advice on how to solve it.

It’s completely free too, because their commissions are paid for by the bank

In any case – Property Guru has a if you’re taking up a mortgage or refinancing.

I’ve used it for my loans and found them pretty useful – you can give it a try .

They help you compare all the mortgage loans on the market to find the lowest rates, and a mortgage broker can reach out to offer more advice.

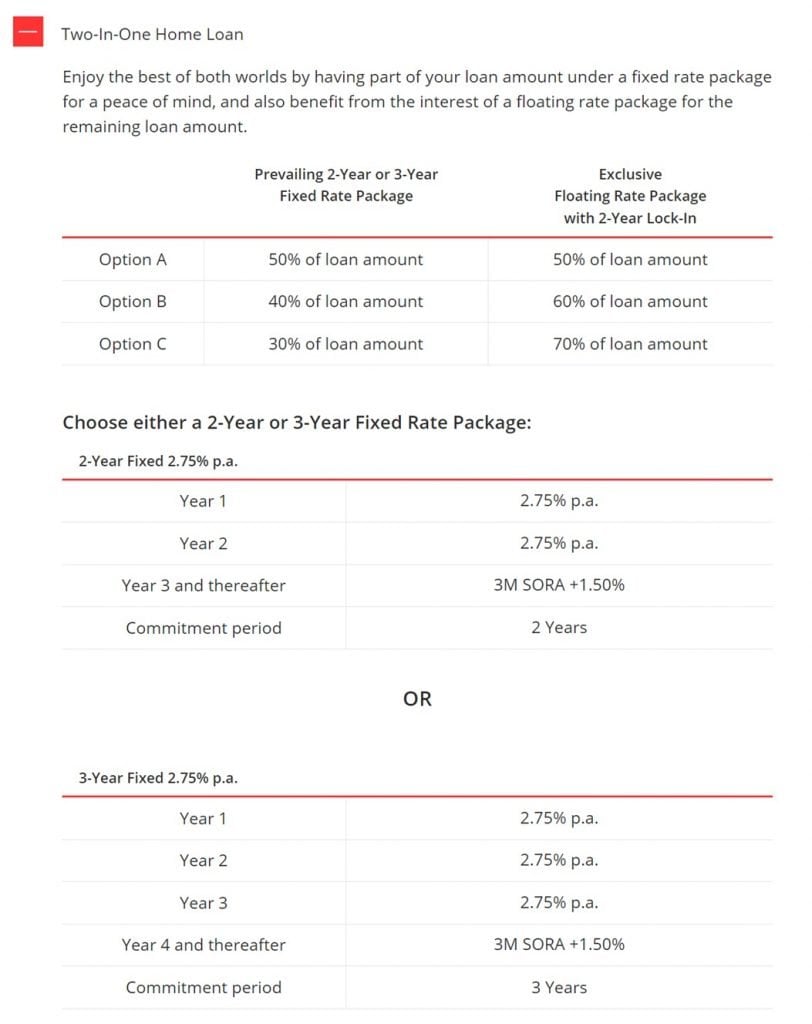

Fixed + Floating Interest Rates Mortgage Loan

Just FYI that there is a third option available.

A mix of fixed and floating loan.

For example, a 50% fixed rate, and 50% floating rate mortgage.

So if you’re the kiasu kind that cannot decide between fixed or floating interest rates, this might be for you.

Closing Thoughts: Update from the Patron

Interestingly, the Patron dropped me an update:

HI FH, just to let you know, I’ve decided against the loan option.

The way I see it, I will most likely get the ‘important’ decision (fixed/floating, & tenor) wrong at some point and end up kicking myself.

The market is shifting, and I may do something I regret with the funds I have available, like going long the S&P500 or QQQ at the wrong time. . .

So while I have the funds, I decided to pay in full cash, and rent out the property with a net yield over 3% which isn’t bad.

Hope its some insight into at least what I am doing.

For what it’s worth – I actually thought this was a great decision, by someone who understands his own strengths and weaknesses well.

Okay, from a pure investment perspective I get that if you take the $1.2 million loan and invest it like George Soros you could have $10 million by end of this decade.

But hey – not all of us are George Soros.

And if you don’t invest well, you could easily lose money over the next few years, in what I expect to be quite a treacherous macro environment.

So kudos to the Patron for understanding himself well, and making a bold decision like this.

Remember in life – there is no right or wrong decision. And you don’t have to answer to anyone but yourself.

Decide whatever works best for you, and move on.

Use a Mortgage Broker… they provide real value add…

Now I hate to say this.

But frankly, if you are looking to take up a new mortgage or refinance your mortgage – use a mortgage broker.

In my experience, a mortgage broker provides real value add.

Okay maybe they can’t give you an in depth break down on the Eurodollars futures curve and where interest rates are headed over the next 12 months.

But they can compare all the mortgages available on the market available, and let you know which bank offers the best rates.

This alone is a huge time saver.

And if you run into problems, a mortgage broker can provide advice on how to solve it.

It’s completely free too, because their commissions are paid for by the bank

In any case – Property Guru has a if you’re taking up a mortgage or refinancing.

I’ve used it for my loans and found them pretty useful – you can give it a try .

They help you compare all the mortgage loans on the market to find the lowest rates, and a mortgage broker can reach out to offer more advice.

As always, this article is written on 2 Sep 2022 and will not be updated going forward.

If you are keen, my full REIT and stock watchlist (with price targets) is available on Patreon. You can access my full personal portfolio to check out how I am positioned for the coming downturn too.

Looking for a low cost broker to buy US, China or Singapore stocks?

Get 100 USD in Apple Shares with , a zero commission broker.

Get a free stock and commission free trading with .

Get a free stock and commission free trading with .

Special account opening bonus for Saxo Brokers too (drop email to [email protected] for full steps).

Or for competitive FX and commissions.

Looking to buy Bitcoin, Ethereum, or Crypto?

Check out our guide to the best Crypto Exchange here.

Do like and follow our Facebook and Instagram, or join the Telegram Channel. Never miss another post from Financial Horse!

Looking for a comprehensive guide to investing that covers stocks, REITs, bonds, CPF and asset allocation? Check out the FH Complete Guide to Investing.

Or if you’re a more advanced investor, check out the REITs Investing Masterclass, which goes in-depth into REITs investing – everything from how much REITs to own, which economic conditions to buy REITs, how to pick REITs etc.

Want to learn everything there is to know about stocks? Check out our Stocks Masterclass – learn how to pick growth and dividend stocks, how to position size, when to buy stocks, how to use options to supercharge returns, and more!

All are THE best quality investment courses available to Singapore investors out there!

FYI – We just launched the FH Property Series. Everything you need to know to buy a property in Singapore, completely free of charge.