I’ve actually been very keen to do a deep dive into Singtel for a while now.

Because this is what Singtel’s share price looks like.

Since the recent earnings on 23 May, the stock price has been on a tear.

Singtel’s share price has gone from 2.4 to 3.07 in 2 months – a 28% increase.

In fact if you look at the charts, Singtel’s share price has been going up for 9 weeks in a row, and broken out of its post-COVID range.

A 28% jump in what used to be a hated dividend stock, now paying a 5% dividend yield even after the jump.

Never thought I would say this – but is Singtel stock a good buy?

Why are Singtel’s shares up 30% in 2 months?

Singtel’s management has been working on a strategic reset of the company for a few years now, but it was only until the recent earnings result that the market rewarded them for their efforts.

Any what was the reason for this?

In my view – the catalyst was their change to the dividend policy.

52% increase in dividend yield? What is Singtel’s dividend yield at this price?

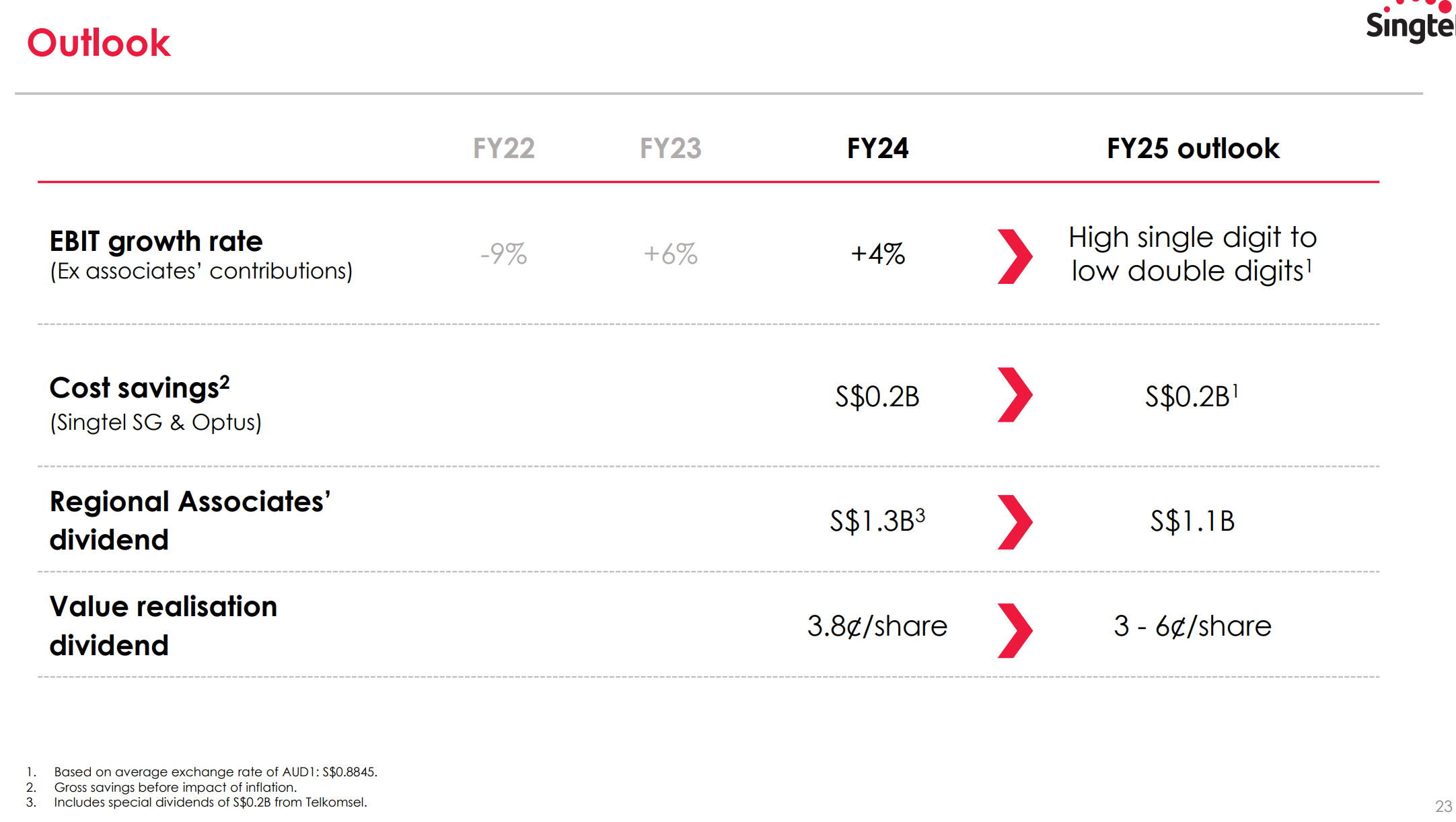

Singtel announced a huge 52% increase in dividend yield for FY 24.

From 9.9 cents last year, to 15 cents this year.

At latest share price of 3.07 that works out to a close to 5% dividend yield.

Dividend Policy for Singtel going forward

But why did dividend jump so much?

It is largely due to this new “Programmatic Value Realisation Dividend”.

According to Singtel, this new dividend will be:

“Funded from current excess capital, as well as future excess capital from identified asset recycling pipeline of ~S$6B, after investing in growth”

Basically from capital recyclying, after selling assets.

But crucially though – Singtel said that this new Value Realisation Dividend is “embedded into the dividend policy, and not a one-off”.

In other words – investors can expect a structurally higher dividend yield from Singtel going forward, and the 52% increase in dividend yield is not a one-off.

So you can kind of see why the market liked this.

At the $2.4 that Singtel was trading at pre-earnings in May, it would have been a 6.25% dividend yield and on par with bank stocks like DBS / OCBC / UOB Bank – without the interest rate risk if the Feds were to cut interest rates.

The jump in share price makes sense when you look at it this way.

In fact here is Singtel’s outlook for the Value Realisation Dividend in FY25.

They’re projecting 3 – 6 cents, which is generally in line with (potentially better than) the 3.8 cents VRD in FY24.

Singtel has been executing well on their strategic transformation

So while the change in the dividend policy was the catalyst that sparked off the rally.

To give credit where credit is due.

Singtel’s management has been executing well on the strategic transformation plan for a few years now.

There are 2 key factors I want to single out that have contributed to Singtel’s recent outperformance:

- Successful capital recycling – at attractive valuations

- Underlying Business is doing well – both the core business and associates

Successful capital recycling – at attractive valuations

This slide from Singtel below sets out the 2 key deals that frankly this horse was very impressed with.

Let’s talk a bit about both deals.

Singtel’s Data Centre Business – 20% sale to KKR at $1.1 billion

Per reporting from Retuers:

New York-based KKR bought a 20% stake in SingTel’s regional data centre business last year for S$1.1 billion ($816 million).

Now Singtel’s data centre business is still in growth phase and not a mature business.

A 20% stake at $1.1 billion would value the full data centre business at $5.5 billion.

That’s pretty generous, which indicates a lot of the valuation was “brought forward” from future revenues.

So this is a good move by Singtel to realise value for shareholders, in that it (a) brings forward future revenues, and (b) signals to the market that an established player like KKR is willing to value Singtel’s nascent data centre business at a $5.5 billion valuation.

Very well done.

49% Comcentre stake sale to Lendlease (Singtel Headquarters)

In 2022, Singtel also announced the sale of 49% of their headquarters to Lendlease.

Here’s the reporting:

Singapore, 1 June 2022 –Singtel today announced that it is partnering with global real estate group Lendlease to redevelop its Comcentre headquarters into a S$3 billion world class sustainable workplace featuring the latest smart building and digital technologies.

…

Singtel and Lendlease have agreed to enter into a joint venture for the redevelopment, where Lendlease will subscribe to 49% of the shares of the joint venture company in 2024 and Singtel will hold 51%. The joint venture company will pay S$1.63 billion to Singtel for the land cost of the development, in or around 2024. Singtel will be responsible for the differential premium payable on the redevelopment.

Again, I like this deal.

SingTel is not a real estate company, there’s really no reason to have so much of their balance sheet tied up in real estate.

With this move they freed up almost $1.6 billion on their balance sheet for other investments.

They brought in a specialist real estate player with expertise to handle the real estate work.

And yet they retain a majority stake in the headquarters.

Divestment of loss-making assets – Amobee and Trustwave

Apart from the 2 deals above, Singtel has also been divesting loss-making assets like Amobee and Trustwave.

To me this was a no brainer.

Amobee and Trustwave are US advertising and cybersecurity companies.

The previous time I looked at Singtel shares a few years back, it struck me as mind boggling that Singtel would want to compete in US advertising and cybersecurity, both of which are highly competitive and technologically advanced industries.

Both Amobee and Trustwave have been loss-making for years, and the only crime here is that Singtel held onto these companies for so long.

You can now follow Financial Horse on Google Chrome to avoid missing any posts!

Just:

- Click the 3 dots on the top right of Google Chrome

- Click Follow!

- And Financial Horse posts will now appear on your home page, under Following:

You can also follow Financial Horse on:

I also send out a newsletter at 10am every Sunday – rounding up the posts from Financial Horse for the week. Sign up below!

Singtel is executing well on the capital recycling – selling old world assets, buying new world assets

So Singtel has freed up a lot of their balance sheet from the moves above.

What are they doing with all the money?

Here’s reporting from Reuters:

A consortium of U.S. investment firm KKR (KKR.N), and Singapore Telecommunications (SingTel) (STEL.SI), has emerged as the frontrunner to buy a minority stake worth $1 billion in one of Asia’s biggest data centre providers, two sources said.

Of course, there are no guarantees this deal will materialise.

But the fact is that Singtel is selling stuff that is loss making and doesn’t synergise with their core business.

And looking to buy sexy new assets like data centres to drive future growth.

That’s a story I can get on board with.

Underlying Business is doing well – both the core business and associates

The icing on the cake – the underlying business is doing well too.

Okay maybe “doing well” is too strong a word, but rather it is doing okayish, and no longer in terminal decline like it was a few years back.

Singtel’s core businesses are:

- Optus – Australian Telco

- Singtel – Singapore Telco

- NCS – Provides technology services to corporates across APAC

- Digital Infra – Nxera, the data centre business

I’ve extracted their performance below, and generally all are doing okay / flattish.

Compared to a few years back when all were in the red, this looks a lot better.

The regional associates like Bharti Airtel and Telkomsel are also doing better.

Across the board – pre-tax profits are up 3% on a year basis.

What is the growth strategy for Singtel going forward?

Now what is Singtel’s growth strategy going forward?

You can see the slides below, but it’s really as simple as – optimising the core, while scaling growth engines meaningfully.

Again, I love it.

Strategy does not need to be too complex sometimes, you just need to nail the execution.

And sometimes turning a company around is really as simple as focussing on extracting profits from your core business, and using all that profits to invest in new growth engines.

From Singtel’s perspective, the Telco business in Singtel, Optus and the regional associates are the core business to be optimised profit wise:

While the growth businesses are NCS (Tech services to corproates) and Digital Infrastucture (Nxera – data centres).

Singtel’s Balance Sheet is strong – buying management plenty of runway to execute on the strategic transformation

On top of that, Singtel’s balance sheet is actually really strong.

$4.6b in cash, and $7.8b in net debt.

1.3x debt to EBITDA/Assoc PBT ratio.

And a ridiculous 17.8x interest rate cover ratio.

With a balance sheet like that, it buys management a lot of runway to execute on their strategic vision.

$2 billion impairment of goodwill on Optus – a bad acquisition can haunt you for a long time

It’s not all bright sunshine though.

Singtel recognised a $2 billion impariment of goodwill on their Optus acquisition (the Australian Telco which Singtel acquired in 2001):

As part of the Singtel Group’s review of its investments, the recovery value of Optus Group was assessed to be below its carrying value as at 31 March 2024. This reflected a range of factors including weaker prospects in the enterprise market, increased cost of capital and the softer macroeconomic outlook in Australia partly offset by the benefit from the regional MultiOperator Core Network (MOCN) agreement which Optus has entered into with TPG Telecom. Consequently, the Group recorded a non-cash impairment provision of S$2.0 billion on the goodwill of Optus. The Group also recorded a non-cash impairment provision for goodwill of S$340 million for the Asia Pacific Cyber Security Business mainly from general business weakness on lower corporate spending. In addition, a non-cash impairment provision of S$280 million (A$320 million) was recorded for goodwill of NCS (Australia) due mainly to higher cost of capital.

And even after that $2 billion impairment, there is still another $5.9 billion of goodwill on Singtel’s balance sheet:

In the current year, the Group recorded an impairment charge of S$2.0 billion in relation to Optus. At 31 March 2024, the carrying value of Optus includes S$5.9 billion of goodwill.

This just goes to show you that how a bad acquisition can really haunt you for a long time.

Will I buy Singtel stock?

I never thought I would say this – but I actually really like what Singtel’s management has been doing with the company.

Management is making all the right moves with the company that should have been taken years ago, but better late than never.

And with the increase to the dividend in May, that was the catalyst that sparked the market rerating in Singtel shares.

That being said, the share has run up a lot, in a very short time.

We’ve had 9 weeks of the stock going up, which makes me somewhat wary of buying a position here.

Are the forward valuations cheap – if Singtel can execute?

At current prices, Singtel trades at a:

- Forward PE of 19x

- EV/EBITDA of 15x

Whether that is cheap really depends how you think of Singtel.

If you think of Singtel as a traditional telco business, I would say those valuations are exorbitant.

If you think of Singtel as a tech company investing in data centres, those valuations may be cheap.

So put it all together – I suppose it goes back to execution.

Singtel looks about fairly valued today, and continued share price upside would depend very much on management’s ability to execute on their strategic transformation – to optimise the core businesses, while scaling growth engines meaningfully.

In the bigger scheme of things – if Singtel can execute, does more upside lie in store?

Here is the longer term share price since IPO.

Singtel shares have gone as high as 4.4 at one point.

So if you think that this is the bottom for Singtel, and management can meaningfully execute on the transformation.

It’s not impossible to think that there could be future upside in play.

So… will I buy Singtel shares or not?

Again, I like what Management has done, and is doing with the company.

My concern is that the stock has had a monster of a move the past 9 months, and valuations today have brought forward a lot of future growth.

I’m not sure if I am keen to buy a big position today.

But again, I definitely like what management is doing, and this is definitely going to be a stock on my watchlist going forward.

At the right price, or if management continues to execute well.

You know I could actually see myself buying a position.

As always – I will share updates on FH Premium if and when I decide to buy a Singtel position.

You can also see my full stock and REIT watchlist on FH Premium, and my full portfolio today.

There have been huge moves in stock prices the past 2 weeks, with lots of opportunity in markets.

I will be updating my stock and REIT watchlist this weekend on the names that I am keen to buy, do sign up for FH Premium if you are keen.

Never miss another post from Financial Horse!

Follow Financial Horse on:

I also send out a newsletter at 10am every Sunday – rounding up the posts from Financial Horse for the week. Sign up below!

so, they did a huge impairment on Optus, which is arguably their core biz.

Written off 2 other non profitable ventures.

Core biz is flat, while attempts at diversification is mediocre.

The only reason it’s up is because it’s opening its coffers to ramp up dividend. But if you’re buying for dividend, lots of better choices.

Unless they hit a winner on diversification, they’ll end up like SPH in a couple of years.

Yes fair enough – it will ultimately come down to execution.

Can management execute on their vision to transform the company beyond the core telco business, or not.

Wow. I held it in CPF and Cash @ $1.9 since 1991 IPO. Lol.

That is amazing. 30+ years!