So I got a question from a Patron that really got me thinking:

Hi FH, Good morning, Two days ago when there was news that a US company (Moderna) has good news of Covid19 vaccine, DOW went up 900 pts and STI 45 points.

Then the news last night (19 May) says that the Moderna Vaccine news was not accurate, DOW came down 300 points.

Pls advise your view on how you read the market when eventually Covid 19 Vaccine is found…. will it be too late to BUY into the market at that time? Or economy and companies are in such extreme mad shape and trouble that it cause further downward pressure?

Thanks

Seems simple right?

But the more I thought about it, the more I realized how complex this question actually was, and how many issues had to tie in to fully answer it.

I just couldn’t shake this question from my head, so I knew I had to write a full article on it.

FYI we’ll share commentary on the 2020 crisis every weekend going forward, so for those of you who haven’t signed up for our mailing list, please do – its absolutely free.

It’s a weekly newsletter that goes out at noon every Sunday, and rounds up the week’s posts so you never miss anything. Sign up below (you get a free guide when you sign up):

And as always – this article is written on 22 May 2020. Updated thoughts are on Patron.

A framework to understand how stocks work

To answer this question, I wanted to first share my own personal framework on how stocks work. I don’t think it’s perfect, but it’s the best framework I have for understanding what’s been happening so far.

If you disagree with it, or you have refinements to the framework, please please share your comments below. I am actively looking for people who disagree with this model– so we can refine it.

And very simply, this framework is based on the idea that in the short to mid term, stocks are driven by liquidity, and in the long term they are driven by earnings.

Short to mid term – Liquidity driven

The world is driven by supply and demand.

Supply v Demand is the central concept in all of business, economics, and pricing, which is why it’s the first thing they teach you in economics. I never understood it back then, but as I got older I gradually became to appreciate how important supply and demand is.

So in the short term, the supply of stocks typically doesn’t increase by much. You may get an odd IPO here and there, but unless it’s a big one, it really doesn’t move the needle (although when there are a number of big ones – you see liquidity being affected and stock prices weaken).

Which means that short term, it is demand that truly drives prices. And this is what the liquidity concept aims to capture. It looks at the amount of cash flowing into stocks, versus the amount of cash flowing out.

And liquidity itself, is driven by a number of factors, such as M2 money supply, investor sentiment on stocks, QE, etc.

The most important one for current purposes is QE, because the magnitude of QE dwarfs all the others.

Understanding the Impact of QE

So let’s use the liquidity framework to understand Quantitative Easing (QE).

In QE – The Fed basically buys Treasuries.

And the Fed buys more Treasuries than the increase in supply, so this has 2 effects: (1) The price of Treasuries goes up – because demand > supply, and (2) This crowds out the market for Treasuries – because the Feds buy treasuries, so that’s less treasury for private money to buy.

QE drives liquidity into stocks

So coming back to (2), there’s now money that cannot go into Treasuries. Where does that money go?

Remember most of this is institutional money, and when you’re a big hedge fund or pension fund with $100 billion, the money needs to go somewhere, and you can’t just park it at a bank or buy a few penny stocks.

So if you’re an intuitional investor in such a scenario – there are 2 things you want in an investment. You want (1) good returns, and (2) good liquidity.

Gold is out because gold doesn’t generate cash flows and performs poorly when the economy is good. Commercial Real Estate has good returns but poor liquidity. Corporate debt has okay returns, but liquidity is not amazing.

So the only asset class that has sufficient liquidity and returns for the big institutional players, is stocks. So the excess cash flows into all risk assets classes (which is why CRE and corporate debt all benefit), but stocks benefit the most.

QE is bearish for Bonds

But now is the part where it gets a bit more tricky.

When the Feds buy bonds, they crowd out the market, and drive up the price of bonds. When the price of bonds goes up, the expected future return goes down.

Because of this, the more the Feds buy, the poorer the investment bonds are.

And therefore the net effect of this – is that QE is bearish for bonds. Investors sell bonds, and they use the cash to buy shares. Sounds counter intuitive I know, but that’s my theory, and its generally backed up by the price action.

If you disagree, just let me know below.

QT is the opposite

Now I’ve simplified the above analysis for obvious reasons, but the net effect here, is that QE is bearish for bonds, and its bullish for stocks.

And on the flip side, Quantitative Tightening (QT) is the same logic in reverse. It is bullish for bonds, and bearish for stocks.

We saw this in 2011, 2015, and 2018

Why March 23rd marked the short-term bottom?

With this framework in mind, let’s go back to March 23 which marked the short-term bottom in this COVID19.

For the record – I did write in my post back then that I started buying stocks on March 23, so I guess that gives me some street cred to write this post ? .

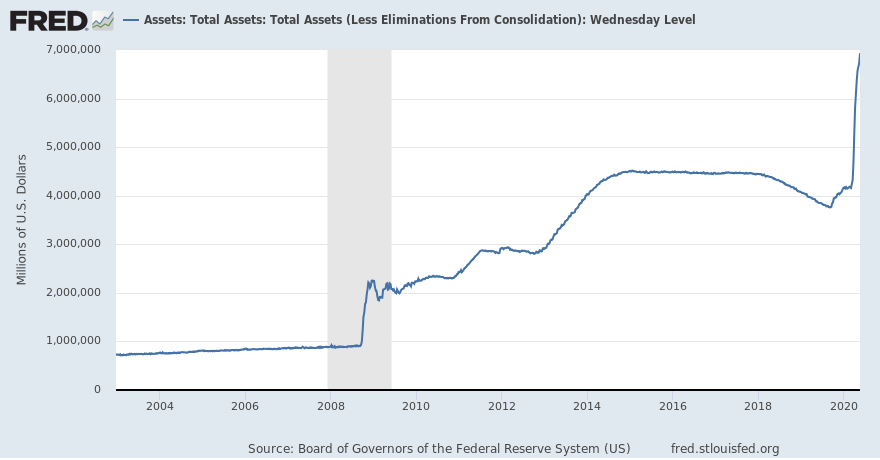

On March 23, the Feds committed to unlimited QE.

This was similar to QE1 – 3, the only difference was the size. Absolutely crazy because it makes QE 1 – 3 look like nothing in comparison.

But that’s the thing about debt right. Debt is like drugs, the more you use it, the more the economy builds up a resistance, and the marginal value of debt drops. It’s what the Chinese have discovered, and why they’re so reluctant to stimulate with debt now.

So QE infinity works the same was as QE 1 – 3. Bond prices drop, and stock prices go up. Which is exactly what we’ve seen since March 23.

What happens next?

And now the million dollar question – what happens next.

Short to Mid term

So in the short to mid term – it’s all about liquidity. For as long as the Feds buy bonds, prices of stocks will go up, and prices of treasuries will drop.

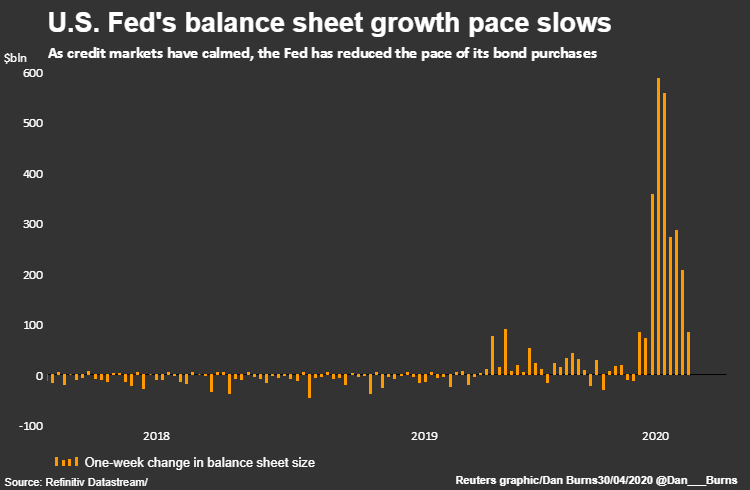

The problem though is that the rate of purchase by the Feds have slowed. It was strongest in late March and April, which is why we saw the biggest moves then.

After that, the pace of buying slowed, removing a powerful tailwind for stocks, and we’ve seen stocks generally rangebound after that.

So in the absence of Fed buying, we need another party to come in in a strong way to drive liquidity.

What party could that be?

There’s still a lot of institutional and retail money on the sidelines, so if that money comes in we could get another leg higher – so that’s important to watch. Moves like what happened this Monday are important.

Corporate buybacks are recovering in a small way, but I think it’s mostly out for this year.

So I think that short term, unless sentiment changes materially (eg. Reopen goes smoother than expected – driving all the money on the sidelines back into the market), the Fed Balance sheet is the key to watch.

And to sum it up:

If the Feds buy, stocks go up.

If they slow their buying (like what they’ve done), stocks stay range bound.

If they tighten, stocks sell off, but let’s be realistic, Feds are never tightening again for a few years.

King Dollar

Another theory I talked about back in March was about the King Dollar.

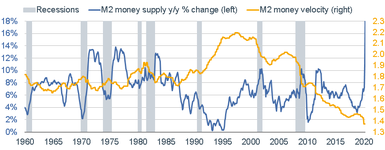

The US economy is 20% of global GDP, but 70% of world trade is denominated in USD. USD dries up because global trade stops (velocity of money drops), so the whole world is short USD.

The chart below illustrates this well. Money supply goes up as the Feds print more USD, but money velocity drops because everybody just hoards the dollars, so there is still a shortage.

At the same time, there is also big capital outflows from emerging markets – driven by a strengthening USD, commodities bust, COVID19 handling etc.

So all that money flows out from the world and back to the US, and where does that money go? If you guess stocks, you guess same as me.

So in a way, US stocks have this additional tailwind of USD’s reserve currency. It’s a similar dynamic to what played out in 1997, when Asian economies were going through their worst recession ever, and in the US – we had the Dot Com boom. All liquidity fuelled.

Unfortunately this point is unique to US, so the same analysis will not hold for European and Singapore stocks. US stocks have this additional tailwind that global equities do not.

Long term – earnings driven

So that’s the short to mid term. But longer term, it’s almost exclusively earnings driven.

All the liquidity in the world isn’t going to help if companies don’t make money, so longer term we look at earnings.

This is the more traditional analysis of looking at corporate margins, profitability, etc. Stuff out of a corporate finance textbook.

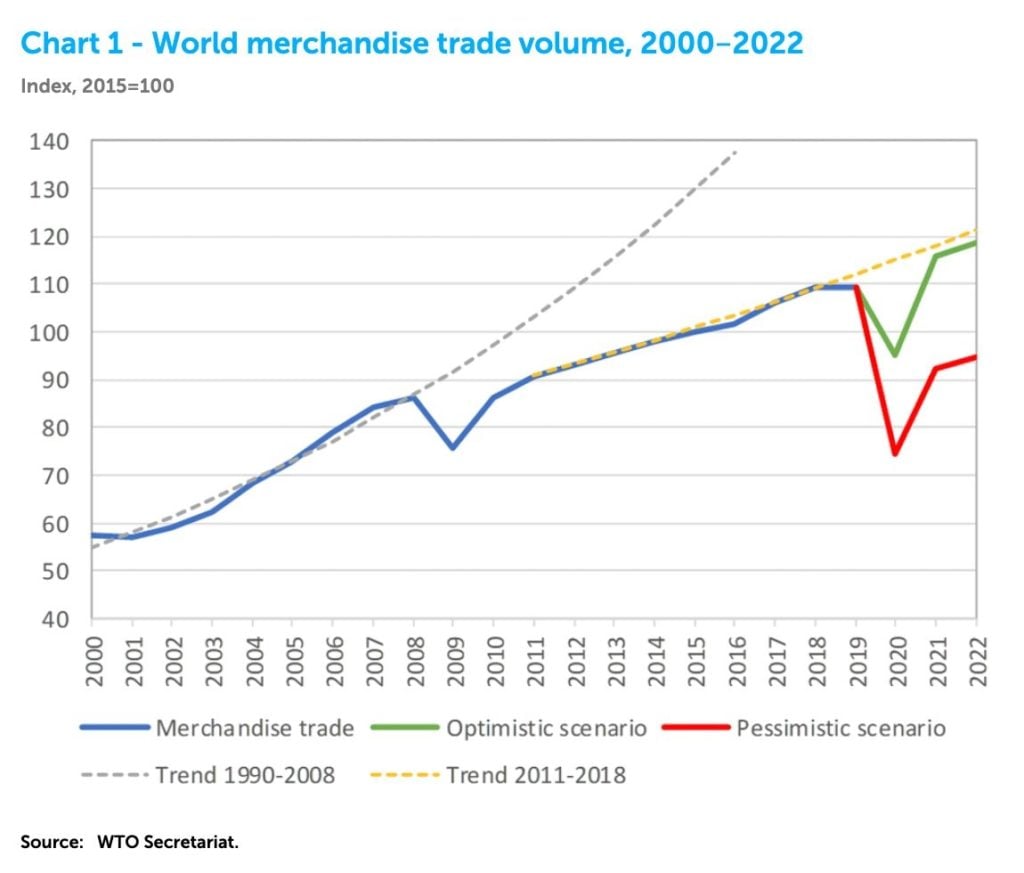

What do earnings look like?

And the key question for earnings, is whether we are going to be on the red line, or on the green line.

The market now looks to be pricing in a green line scenario, so if the reality turns out to be different, we may see another selloff in the absence of Fed intervention.

What do I think personally?

Okay so no one knows the answer to this question, and your guess is as good as mine. We’ll only know for certain in Q3 once everybody starts to reopen and we get to look at earnings impact.

And personally, I still think the reopen is going to be harder than we imagine. Frankly I just don’t see the world going back to where it was in Dec 2019 for the whole of this year.

China’s a good example. They locked down the whole country for almost 2 months, barred international visitors, got new case count almost to zero, and they’re still grappling with a second wave now and had to lockdown Jilin.

You can say what you want about China, but they’ve been the poster child in this fight so far. So if China is having such problems with a second wave, what about the other countries in Europe or the US that are reopening even before case count drops to zero?

So while I get the liquidity dynamics in play, and I will buy in line with liquidity dynamics, I’m a lot more cautious on the earnings front.

Impact of Vaccine

So going back to the question from the original Patron:

Pls advise your view on how you read the market when eventually Covid 19 Vaccine is found…. will it be too late to BUY into the market at that time? Or economy and companies are in such extreme mad shape and trouble that it cause further downward pressure?

Impact of the vaccine news is that:

On liquidity – positive news of the vaccine drove some money on the sidelines into the market, driving up prices.

On earnings – too early to say for certain because we’ve not cleared clinical trials and mass production is not clear. But assuming those are settled (and those are big ifs), then once mass production is available, they will improve earnings.

So the short term liquidity impact has already been baked in once the news was released, and futher impact will come from more news (eg. clearing clinical trials, easy mass production etc).

And longer term earnings impact will come only when the vaccine has been mass produced and deployed, because only then will social distancing measures be reduced and consumer sentiment improve.

But don’t miss the forest for the trees here. News like this will come out every other week from here on out, and a lot of this is just noise. Go back to basics, and go back to the framework set out here. Look at the bigger picture.

Closing Thoughts: There is no liquidity outside of capital markets

The other thing that is unique about this crisis, is that because everyone in lockdown mode, we actually haven’t seen any real liquidity outside of capital markets.

We haven’t seen deals actually done in commercial real estate of M&A in a big way post COVID19, so it’s also interesting to watch if private valuations will keep up to the lofty public valuations.

I would truly be amazed if the world manages to hit pause for 2 to 3 months, and then we reopen perfectly, without anything breaking in the global economy.

I hope that we can do so, because that’s the ideal outcome for the world, but somehow I’m quite wary that there’s something brewing under the surface, that we’ll only see come to light in 2H2020.

After all, you don’t know what you don’t know.

Share your comments below!

Support the site as a Patron and get market and stock watch updates.

Do like and follow our Facebook Page. We share great links and infographics there.

Join our Facebook Group to continue the discussion, we have a great community of investors who want to help each other become better investors. Everyone is welcome!

Looking for a comprehensive guide to investing that covers stocks, REITs, bonds, CPF and asset allocation? Check out the FH Complete Guide to Investing.

Or if you’re a more advanced investor, check out the REITs Investing Masterclass, which goes in-depth into REITs investing – everything from how much REITs to own, which economic conditions to buy REITs, how to pick REITs etc.

Both are THE best quality investment courses available to Singapore investors out there!

Great article. Frankly, one of your best. Completely agree with you that we should be monitoring fed balance sheet now.

How do you thin real estate will hold under this crisis. I forsee a short and long term slow down in commercial rental reversions simply due to recessionary effects and a move to encourage greater WFH (Mastercard and most of silicon valley). Could this be the new normal? How about air travel? Business travel accounts for more than 50% of airline revenue and about 70-80% of their margins. Would business travel reduce? Or would we continue seeing them maintain on the basis that most companies already travel on necessity since the 08 crisis.

These 2 specific industries – aviation and real estate have the potential to send ripples through the entire market given the size of their ecosystems, their dependence on debt and their general lower margins.

Thanks! Glad you enjoyed it. This one was a bit more dry and technical, so I wasn’t sure what the reception would be like.

I think CRE will have a tough year or two. CRE isn’t like stocks which are very liquidity / QE driven, the moves from the Fed don’t flow through to CRE as well. I dont think we’ve seen the full impact yet because real estate tends to lag capital markets, so we’ll probably only see the real impact in 2H2020 and onwards.

But yes – I do think CRE and aviation will have a tough year or two.

The advice to filter out vaccine news is sound. The Moderna rally unwound within a few days, the CEO having sold a significant amount of stock at the highs after doing rounds of TV interviews with a flimsy, data-lite, press release. Beware pump and dump.

Anything short of an effective vaccine, or the virus disappearing like SARS, and current stock valuations have a problem. Whilst not quite priced for perfection, stocks are priced for the most optimistic outcomes with very little room for bad news. There is a greater downside risk than upside potential in my view. At the end of March prices were attractive, today, not so much. Arguably it’s already too late to buy into this market, there’s very little value.

The GFC caused a 6% reduction in GDP in most developed economies. The reduction in GDP from COVID is far larger. Even a recovery to 90% of 2019 output would be utterly catastrophic for long term investment prospects. Without a vaccine entire industries are going to be devastated, travel, tourism, hospitality, commercial real estate, retail.

Vast liquidity injections are keeping zombie companies afloat, preventing the creative destruction required to fuel a strong recovery. Major economies drowning in debt, increasing inequality, accelerating de-globalisation, supply chain reshoring and demographic challenges and the outlook next for the 10 to 20 years is highly uncertain. It hasn’t fully impacted people yet, but I wouldn’t be surprised if we see very serious social unrest in the next few years.

This isn’t to say there won’t be a recovery, humans are ingenious and life goes on, but I am certainly cautious. The next bull market has not begun we’re still looking at a bear market rally. If you look at fund flows, most of the ‘smart money’ has not participated in this rally, it’s been driven by retail, short squeezes and very low liquidity.

Thanks! Really enjoyed your sharing.

Pretty similar views on my end – I started buying late March and again in April, but with the recent run up I’ve dialled back purchases quite significantly. I think the risk-reward for equities at this stage no longer looks compelling.

I also agree on the social unrest and political uncertainty point. I think this will play a far bigger role over the next few years than most people are expecting.

Too cautious u would have miss the rally of a life time, The so call “smart money” now look stupid.. April was the best month for stock in decade( google). I know, because i buy in beginning April, amazingly, some of my stock are at all time high and some at 52 week high. Don’t try to time the market, Buy some and when crash come, just sell and capture your profit, simple as that. Data and study show that staying in the market throughout the crises make more money.( google) .

Don’t need to try to out think the market. Financial horse is right, supply and demand apply to stock market,

U have likely miss the rally and i still think it is not too late as Fed can provide more liquidity if need a rise. The rally got more leg to go. And there might not be a bottom again for a long time though it appear there might be one, We don’t know

Financial horse already said,, ” After all, you don’t know what you don’t know. ”

But one thing we know is that there is a rally in the market,right now and there is money to make,,

Make hay while the sun shine. By the time the sun go down, i would be out with handsome profit, to buy back cheaper at one of the bottom to ride the next wave up to make even more profit.

Market are always 6 months ahead of the real economy, and are forward looking.( google)

Good luck to you all and me too, cause i risk less profit if market crash tomorrow.

Thanks for sharing your thoughts, I did enjoy reading this.

I think stay till rally over will make more profit that selling now. Like you said we don’t know what we don’t know. I think use trailing stop is the best way to get out of the market with maximun profit., Keep our portfolio trim so can sell fast in a crash.

Wrote a big comment but lost it all.

TLDR: There is a supply of t-bonds.and people are still buying them (see 20Y bonds issue)

People are buying AAA t-bonds at negative yields.

There is an impedance mismatch in risks for switching from t-bonds/cash to stocks. Those investors can’t be the same group of people.

c-bonds/t-bonds market tells a different story – there is a disagreement between two crowds of investors.

Oh dear, sorry to hear that.

Really interesting point you raised, I wish we were able to read the full original version. What’s you conclusion from this though? That bond market is pricing in material risks to the downside, that equity is missing?

I would have thought QE buying from the fed split investors into 2 – those who had to go further out on the risk curve for yield, and those who cannot afford to take on any risk at all, and are buying treasuries at whatever price. The latter group together with QE is driving up bond prices short term, just like in QE 1 to 3, but it will reverse in the mid term assuming things play out the same way. I do think things are different here though because the Feds will be forced to do yield curve control to keep borrowing costs down (if they haven’t already).

I guess the TLDR version is that QE / yield curve control has distorted the Treasury market’s price signals. But would love to hear your take.

Maybe I am overly bearish, but if the recovery takes longer than is currently being priced in by the markets – and I think it will – there will be good opportunities to invest over the coming years. Watching the rally from the sidelines hurts if you didn’t buy in March and April, but the economic COVID fallout has barely begun. I think you have been saying similar in recent articles – have patience!

Agree that fallout has barely begun. Hertz filed last night – and it’s going to be bad news for used car prices. CRE hasn’t even started its collapse.

Liquidity phase is over, we’ll shift into insolvency phase soon.

Regarding the modena vaccine, a good read is here.

https://edition.cnn.com/2020/05/22/investing/moderna-coronavirus-vaccine-stock-sales/index.html

Regarding the FED, in the latests fed meeting with all the state governors, the FED chairman Powell mentioned,

” The fed role only aids in liquidity issues, but not insolvency”

That statement alone, says alot and is very sobering.

Thanks for the share! Agreed on liquidity =/= solvency, it’s something we’ve been talking about on this site for a while.

I too, think that this will come to prominence in 2H2020 when companies start to run out of cash.

I feel that at the end of the day, retail investors need to understand two things: (1) prices of securities are based on markets’ EXPECTATIONS, and (2) the markets’ expected outcomes are PROBABILISTIC.

There are billions of dollars circulating every day in the market trying to price risk and information. The prices that you see reflect the probabilities that the market assign to every possible outcome they can think of, and these probabilities can change drastically in an instance. To make matters worse, the market is made up of all sorts of people – they range from the full-time portfolio manager/analyst who is modelling out every single item in the income statement/balance sheet of a particular company, to a 16yo kid who executes his trade based on reddit’s recommendations. However, at the end of the day, the markets collectively agree on a single price.

Prices move only when new information arrives, causing each market participant to shift their expectations and the probabilities they assign to each outcome. That is why it is not uncommon for prices to rise when economic growth is weak (perhaps they are pricing in easier monetary policy?), or prices to fall when economic growth is strong (perhaps it is inflation or monetary tightening they are pricing in this time). Likewise, I will not be surprised to see prices fall when a vaccine is truly found (inability to distribute vaccine? wars over vaccine supply?) nor will I be surprised to see prices rise under a prolonged lockdown.

Comments such as “the market will definitely fall because of high unemployment and upcoming wave of corporate bankruptcies”, or “the market will eventually recover when a vaccine is found”, or “this is a dead cat bounce/bear market rally” are just silly. Unless you go out there and gather information from the Buyside (hedge funds, asset managers, insurance companies), the Sellside (bank trading desks, research analysts), the flow of funds among investors, it is practically impossible for a retail investor to understand what the markets are currently pricing. And on what basis does a retail investor have to claim that the current market price is the wrong price?

With that said, the only recommendation I can give to retail investors is just to Buy and Hold a globally diversified equity ETF to reap the equity risk premium over the long run. He or she can choose to have an allocation to a fixed income ETF (government or quasi-government only, definitely not credit) depending on his/her volatility or maximum drawdown tolerance.

That’s an interesting view. I’m not so much a believer in the random walk theory actually, I believe that markets can be inefficient in the short term – and they do frequently.

I think my view advanced in this article was more than liquidity and QE has distorted price signals from the market – so price isn’t what is used to be (if it even used to be anything at all). So it’s got to a point where you keep an eye on earnings in the longer term, but short term you just buy when the Fed buys, and sell when the Feds tighten, and you’ll make money doing so.

Nothing much to add to the discussion, just wanted to say that you really do produce one of the better and well thought out articles among the sea of financial bloggers out there. thumbs up

Thank you J! Appreciate the support. 🙂

Hi FH

On Mar 14, I wrote a short comment after reading many cries of a bear market. I said I didn’t think – because I believed the cause was not directly economic. That being so, a lot depends on whether Trump shed or even moderate his then headstrong attitude towards dealing with the pandemic – it was all about C19 and one man’s stubbornness? I said I believed it was a bull straying into bear territory altho I also thought the DJI would not get near its record of around 29,500.

Just as the crash was C19 centric I believe that the rebound is not solely the result of the FED’s ‘bailout’ plans but also based on the progress towards containing the pandemic and hopes of finding a cure and/or vaccine. So this is what the markets rock and roll to now, more so than economics.

Sooner or later, and I believe quite soon, economic reality will hit. The big difference between now and 14 Mar when I posted my comment is that 38.6 million people in US had lost their jobs and with 2.48 in the latest reported week it looks like the number will continue to a few more weeks at least. Based on inituition, I had said that 40 million is a critical mark and if the number grows too far above that we may have a castratrophe on our hands. More so as with summer upon them it should be peak season. Also, it is likely that many of the employers that laid off workers may no longer be around. And supply chains may take time to be fully restored as lockdowns among countries were not coordinated due to the spread out infections between countries and the response of the respective gov.

So I think the stock market will soon revert its focus to more normal fundamental factors.

By the way, an aspect of the FED buying treasury bonds that I am not sure about and hope you can enlighten me. The FED balance sheet grows as it ‘prints’ money to fund the ‘assets’ purchases. I not sure what happens when the bonds mature? The US Treasury, under normal circumstances, will redeem and cancel them, most likely funded from issuing new bonds as the US budget has been growing. As the FED is buying, reversing from selling pre C19, its balance sheet continues to grow. On the other hand, at the other arm of the gov, the US Treasury, liabilities are growing and since it’s left and right hand, will these expired bonds remain unresolved and left to be dealt with in some distant future years? So will it be simply ‘contraed’ which will reduce the size of the FED balance sheet, allowing it to buy even more ‘assets’ while wiping off a some liabilites of the US gov. Net effect being more USD in ‘circulation’ whether in physical form or as computerised digits. Will is result in a ‘climate change’ for the USD?

Interesting, thanks for the share.

I may actually have the opposite view of you here. In early March I shared my view at the time that a big global recession is coming. But once the Feds flipped to unlimited QE, the liquidity crisis went away. So the next phase is a solvency phase, that has the potential to play out horribly in credit markets and with big losers – but the winners could stand to gain if the Feds and Govts furiously plug credit holes as they appear. It’s never been done in history though, so if they manage to do so, this would be the first.

On your question, we need to split by phases. Originally, Feds would continually roll over the debt to keep its balance sheet constant, so they bought more treasuries when the existing holdings expire. Then they switched to QT – where they allowed it to roll off for good. As we discussed above, QT led to Treasuries going up and stocks going down, so they promptly stopped it. And then we have where we are now, where the Feds haven’t said how they’re going to handle the rolling off yet because we’re still in crisis mode – so we’ll only know in due course.

My personal belief is that yield curve control is inevitable going forward. Just google it for more info – was last done during WWII.

Hello,

A question not related to this article. Etoro platform during the week announced that Singapore customer are now allow to buy stock from USA stock market at no fee at all. What is your take on Etoro platform as well as their offer? Are there there horrible fine print we should be mindful of.

Thank you.

Haven’t looked at Etoro in detail yet, but lots of reviews out there saying the platform is very poor.

Yes,, i believe u are trying to say that market is always forward looking and and the market is always months ahead of the real economy.. am i right?? My apology if i got the wrong meaning of your post..

I guess what I’m trying to say is that a lot of investors read into price signals of the market as telling a narrative, but their read is shaped by their own bias. It’s like reading tea leaves right – you see only what you want to see. At its core, the market is about supply demand, and there’s been a flood of liquidity recently, which drove prices up. Reading too much into it may not be wise.

Could the relatively high level of the stock market be a reflection of hyper inflation which had already started? In other terms the market is early in pricing that stocks don’t hold much value but currencies even less. Therefore the current real value of everything on capital market has already crashed big time, but the face value appear just marginally slower

It’s possible to argue that investors are frontrunning the coming inflation wave, but personally I dont think this is the case. I think it’s just liquidity.

We’ll see though.

I had trouble understanding this article, a bit too technical – where can I find more information about all these terms you threw around in the post?

Hm that’s a tough one. I would probably start with Google.

I will try to explain the terms more in future posts. For this one I mainly wanted to unload my stream of thoughts, so I didn’t dwell too much on the presentation. My apologies.

So QE infinity works the same was as QE 1 – 3. Bond prices drop, and stock prices go up. Which is exactly what we’ve seen since March 23 -> did you mean bond yield and not bond prices? When the fed buys treasury bonds, the price goes up and the yield drops.

Sorry I mean Treasuries and not Bonds.

And no, there is no typo haha. I get that it’s a controversial point, but it seems to be backed up by price action. Once QE starts, bond prices go up (yields drop) in the short term, then after a while it reverses (prices go down, yields go up). My theory is set out above – Investors sell them and move into risk assets, but as some have pointed out, correlation =/= causation. It’s really up to you what you believe though, no one can prove these things for certain.

Hey FH,

Been following you (free version… or euphemism for cheapo who doesn’t want to pay for anything) for awhile now, and thoroughly enjoy your insights because it’s not that technical (finance people can relate) and frankly they mirror my thoughts too.

I think at this point, the most sophisticated investor at the retail level can only conclude that it is a wait and see game. We are not bounded by contracts nor obligations to make investors a la hedge funds / institutional monies. Blue chips / stay home themes are at ATHs, biotech is a punt, traditional income companies are slowing down and some may even go out of biz (banks, aviation, reits). So really to squeeze any upside out of the market at the moment involves sound capital management (or again, euphemistically, how much you are willing to bet on greater fool’s theory for a certain % upside).

Above not applicable to SG market, but we will be surprised at the amount of stupidity that resides in the US market, the amount of hype and marketing that will drive retailers to make their first purchases at ATH, especially with that stimulus paycheck and 0% trading fee Robinhood.

It really is a massive game of musical chairs that is hard to unravel. Maybe intentionally so. Even our Big Short wonder Scion Capital is fishing boots right now – we expect the dude who dived into so much junk mortgage + rating information previously to be able to process an insane amount of info to take action on. And to no avail this time.

At the end of it all, it is more important that we consider our roles as little gears of a bloody f*cking huge corporate machine and the implications of all these fiscal/monetary policies being forced down our throats. I do not promote Marxism, but incidents of late really put his “ideologies” in the spotlight, eh?

Hi Ray,

Thanks for sharing your thoughts. Always glad to hear from a reader (don’t worry if you decide to stick with the free content, you’re still more than welcome here 🙂

I do agree that the main advantage retail investors have vs institutional investors is that we are not constrained by quarterly performance. We have the option to just sit around and do nothing, and wait for things to play out. That’s probably the biggest advantage of retail money, and we should rely on it.

Haha, agreed on the last point too. The strange thing about this crisis is the the response will likely exacerbate the inequalities in society. I do think political uncertainty and conflicts will go up if we continue to progress down this path.

great reviews. enjoy your articles. seems like professional traders are mostly trading the US markets. I am thinking the best trade to set up now is simply to buy a US index and sell a Sgp index. What is your thoughts

Haha I disagree with that. I think there are good opportunities to be had in every market, it’s just about looking for them. 🙂

Thanks for the great article. Would like to get your views on the unprecedented levels of government aid (achieved in days, what took months to achieve during the GFC – probably good timing due to upcoming elections) globally and if there will be a meaningful impact on LT earnings. While the key aim is to keep companies and workers afloat, it seems likely that these low-interest government loans and/or equity injections may lead to an extended period of earnings growth and a bull run, similar to what we’ve seen in the past decade

Higher equity prices have enabled companies to efficiently raise larger amounts of equity, which adds to the above

Current valuation multiples are almost back to pre-Covid-19 levels (after assuming perhaps a 10% hit to earnings), which are a result of years of multiple expansions for most sectors at least. From current prices, do you see more multiple expansion upside, or will earnings growth be the main driver of prices?

Thanks for the great article. Would like to get your views on the unprecedented levels of government aid (achieved in days, what took months to achieve during the GFC – probably good timing due to upcoming elections) globally and if there will be a meaningful impact on LT earnings. While the key aim is to keep companies and workers afloat, it seems likely that these low-interest government loans and/or equity injections may lead to an extended period of earnings growth and a bull run, similar to what we’ve seen in the past decade

Higher equity prices have enabled companies to efficiently raise larger amounts of equity, which adds to the above

Current valuation multiples are almost back to pre-Covid-19 levels (after assuming perhaps a 10% hit to earnings), which are a result of years of multiple expansions for most sectors at least. From current prices, do you see more multiple expansion upside, or will earnings growth be the main driver of prices?

That’s a good question. Will reply you via this weekend’s article!