So I’ve been thinking a fair bit about markets of late.

And there are 3 asset classes in particular that I wanted to spend time discussing:

- REITs

- US Tech stocks (both semiconductors and software)

- Bitcoin (and Crypto)

US Tech in particular is a big one, because post-deepseek, it seems that investors are starting to rotate away from pure semiconductor / hardware names, into software names.

This provides very interesting opportunities for stock pickers – especially as not all the software stocks have rallied as much as the hardware stocks.

Whatever the case, US Tech requires a bit more time to do a deep dive, which I will probably cover next week.

I will discuss REITs in today’s article.

And crypto in tomorrow’s article.

This is an FH Premium post written in Feb 2025, that I am making available to all readers (as many of you have been asking for my views on REITs).

If you find content like this helpful, do consider subscribing for FH Premium.

You will also get access to my latest macro views, full stock / REIT watchlist, and personal portfolio (updated weekly).

REITs

How are the latest earnings results for REITs?

I’ve been looking at the recent REITs earnings reports with a lot of interest.

Feel free to pull up all the earnings reports if you like, but I’ll save you a whole load of trouble because I looked at almost all of them (at least the bigger name REITs).

By and large, the earnings have been generally ok.

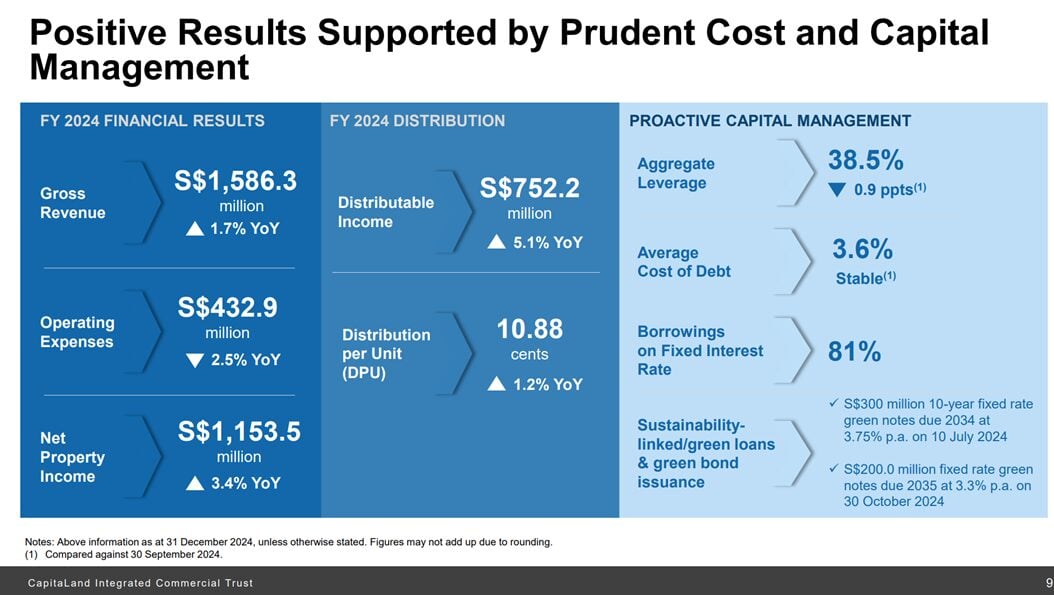

I’ve extracted CICT’s financial presentation below, and this is indicative of what we see from the other REITs, namely:

- Gross revenue flat / up single digits

- Operating expenses down slightly

- Net property income up slightly

- Cost of financing stable

- DPU up low single digits / flat

Think back to 12 – 24 months ago when REITs were reporting strong growth in gross revenue and net property income, yet 5 – 10% drop in DPU, because of higher financing costs, and things are very different today.

From a fundamental earnings perspective, I’ve been saying that probably the worst is over for REITs (for now), and we’ll see earnings start to stabilise going forward.

Exactly what we’re seeing.

But price action has not been pretty.

That said, price action has been terrible.

Here’s the REIT index as a whole – almost back to the 2024 lows.

Price is trending down and below key averages, so for now the downtrend is still intact.

But MACD and RSI suggest oversold conditions, so more aggressive investors *may* want to start thinking about whether this is a tradeable bottom.

Note that this price action comes despite the fact that Singapore 10 year yields have not actually hit the highs that we saw in 2024 (3.5%).

This means that on a comparative, yield spread basis (vs the 10 year), REITs today might actually be “cheaper” than they were in 2024.

Do REITs offer attractive yields today?

Some quick, indicative numbers:

| REIT | Yield |

| Starhill Global REIT | 7.5% |

| CICT | 5.5% |

| Ascendas REIT | 5.9% |

| Keppel DC REIT | 4.3% |

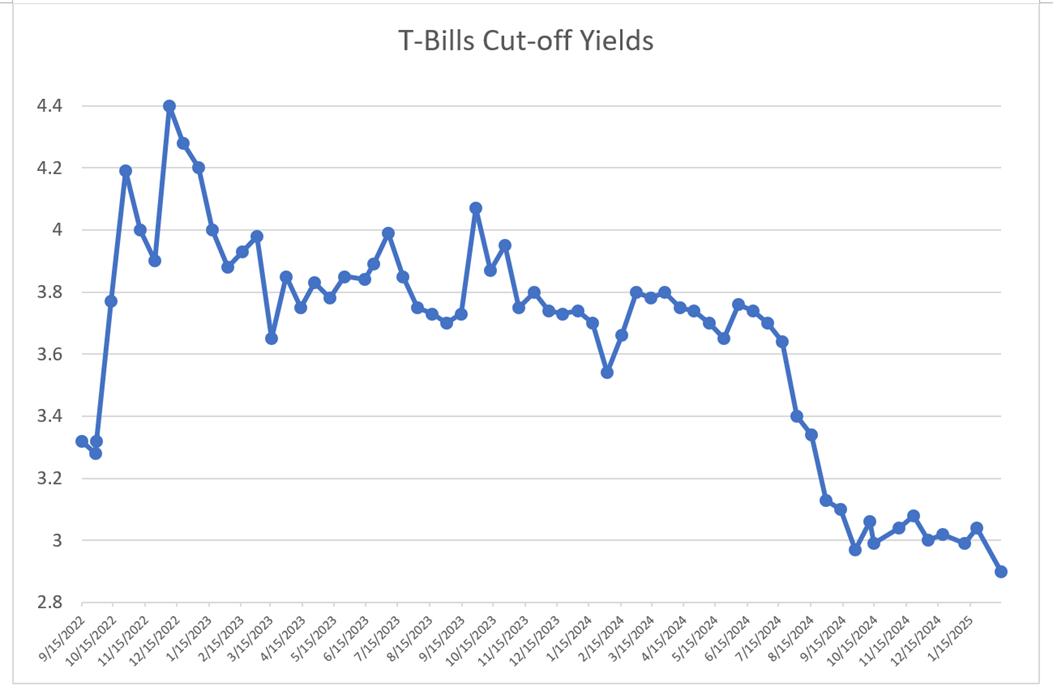

The latest 6-month T-Bills / 10 year government bond pays approximately a 3.0% yield.

This means that you’re looking at a yield spread of about:

| REIT | Yield | Yield spread |

| Starhill Global REIT | 7.5% | 4.5% |

| CICT | 5.5% | 2.5% |

| Ascendas REIT | 5.9% | 2.9% |

| Keppel DC REIT | 4.3% | 1.3% |

Is that worth it?

My Views on REITs?

You know what.

I actually think the risk-reward for REITs at today’s price is decent, but it’s all about how you view REITs in your portfolio, and how you size the position.

Follow Financial Horse to avoid missing any post!

Not really a capital gains style play?

What is fairly clear, is that I don’t think REITs are a capital gains style play today.

For really big meaningful capital gains from REITs – you need a large drop in interest rates.

And with Trump in office, I just don’t see that happening from a macro perspective.

You could argue that on a micro perspective there will be the occasional play like Keppel DC REIT (which sold off on the Guangzhou tenant bankruptcy fears) – that opened up a good opportunity to load up in the 1.6s.

Those will still come along.

But by and large if you look at REITs as an asset class today, I don’t see REITs as a capital gains style play today.

If not a capital gains play – how to view REITs?

The better way to see it, may be as a bond / fixed income style play.

If you really think about it, let’s say you buy a 3 – 5 year duration SGD hedged bond fund that pays a 5 – 6% yield.

As interest rates bounce around, the mark to market value of the bond fund will move daily, so it would make sense to add when interest rates are high, and redeem only when interest rates are low.

Conceptually, that’s kind of how I see REITs today.

You get a decent 2 – 4% yield spread vs the risk free rate.

If you diversify, stick to the blue chip REITs from strong sponsors with good balance sheet, and primarily Singapore properties, I would say the risk for the portfolio as a whole is low – moderate.

Of course, the market price will fluctuate over time, so you need to be okay with the money being locked up for a few months.

And on top of that – if you add opportunistically when prices are low (and trim when prices are high), you could further juice the returns as well.

And this could work pretty well as an alternative (or supplement) to a bond/cash portfolio.

How to think about it from a portfolio basis?

So let’s say hypothetically I have $1,000,000 cash that I want to set aside for yield.

Maybe I will keep $150,000 of that in liquid cash for the liquidity (in a high yield savings account).

Another $250,000 in 6-month T-Bills for risk free yield.

Of the remaining $600,000.

I might put $400,000 into REITs, and $200,000 into bonds.

That gives me something like the following:

| Asset | Amount | Yield | Amount per year |

| Cash | 150,000.00 | 3.0% | 4,500.00 |

| T-Bills | 250,000.00 | 3.0% | 7,500.00 |

| Bonds | 200,000.00 | 5.5% | 11,000.00 |

| REITs | 400,000.00 | 6.0% | 24,000.00 |

| 1,000,000.00 | 4.70% | 47,000.00 |

Now of course in practice you’ll want to tailor the numbers based on how much cash you have, risk appetite, how much liquidity you need and so on.

But the above gives you an illustration of how you can use a mixture of short term instruments (cash and T-Bills), and throw in some medium risk yield instruments like bonds and REITs to achieve a higher blended yield.

The key of course, being that bonds / REITs are not risk free, and the market price fluctuates, so if you do this you do need to keep enough cash on hand to meet liquidity needs (if interest rates surge and you’re sitting on mark to market capital losses on the bonds / REITs).

What will I do? Will I buy REITs in 2025?

Of course, some of you may ask whether this is worth it – taking on all that risk for an additional 1.7% yield uplift.

On 1 million, that’s an additional $17,000 a year.

Whereas you could just put it all into T-Bills, completely risk free, and only make $17,000 less a year ($30,000 a year).

Although that said – another way of seeing it is that a 47k yield a year, is a whopping 56% higher than a mere 30k a year.

What is the biggest risk with just putting all your cash in T-Bills?

A while back I would have said the biggest risk is lower interest rates upon refinancing.

T-Bills only last for 6 months, so a big question mark is where interest rates will be in 6 months.

But I would say this is a much smaller risk today, because of the Trump administration.

Interest rates may go down slightly from here, but I don’t think we’ll see a sharp drop in interest rates from here anymore – so this risk is largely reduced.

In which case – is that worth it?

To go through all that effort for the yield upside?

Ultimately – each investor needs to answer this for themselves.

If you’re young and can take a lot of risk, it may be that you just want a portion of your money in risk free cash / T-Bills, and the rest all in stocks for capital gains.

If you’re a retiree and you want the income, actually the above may make a lot of sense if you need recurring income to cover living expenses, and you’re okay to take on some risk beyond risk free.

My personal views? Will I buy REITs in 2025?

Personal view – I think it’s worth it.

I think we’re at a place today where interest rates are no longer stuck at rock bottom, which presents opportunities across the entire curve.

Assuming you have sufficient cash, splitting them up into various buckets based on the duration they can be locked up for, and the risk level, allows you to achieve a higher yield on the portfolio as a whole.

I wouldn’t want to take a lot of risk with this part of the portfolio though, so I would stick mainly to low – moderate risk names.

And of course on top of that, I would then layer on stocks / commodities / crypto exposure, for the real capital gains play (see full list of REITs and stocks I like on FH Premium).

| Asset | Amount | Yield | Amount per year |

| Cash | 150,000.00 | 3.0% | 4,500.00 |

| T-Bills | 250,000.00 | 3.0% | 7,500.00 |

| Bonds | 200,000.00 | 5.5% | 11,000.00 |

| REITs | 400,000.00 | 6.0% | 24,000.00 |

| 1,000,000.00 | 4.70% | 47,000.00 |

So that’s my views on REITs today, and you can see my follow up thoughts on Crypto, US Tech, and China stocks on FH Premium.

This is an FH Premium post written in Feb 2025, that I am making available to all readers (as many of you have been asking for my views on REITs).

If you find content like this helpful, do consider subscribing for FH Premium.

You will also get access to my latest macro views, full stock / REIT watchlist, and personal portfolio (updated weekly).