As you guys know, T-Bills yields have been on a steady downtrend.

So in this article, I wanted to discuss a couple of points:

- Why do T-Bills yields keep falling?

- What is the estimated yield on the next T-Bills auction on 3 July? Any chance that yields go back up?

- What are the alternatives to T-Bills in today’s market?

I’m trialing a slightly different format for today’s T-Bills article (as compared to previous version).

Love to hear what you think on which style you like more!

Executive Summary (for the busy horse‑riders)

- Six‑month Singapore T‑bill yields have nosedived from 3 % in January to just 2 % in the latest 19 June auction.

- The main culprits are cheaper short‑term funding (SORA, SGD swaps), flat issuance, and an army of retail bidders parking spare CPF‑OA cash.

- Barring a curve‑ball from the Fed or MAS, I think the next auction settles around 1.95 % ± 0.05 %. If you need the liquidity, go non‑competitive and move on; otherwise, decent fixed‑deposit promos might give you more juice.

So… why are T‑bill yields falling off a cliff?

Let’s keep it simple – yields move because of demand, supply, and the broader interest‑rate backdrop. Here’s how each leg looks right now:

- Funding is dirt‑cheap. Six‑month compounded SORA has dropped nearly 100 bp since February, landing around 2.05 %. When banks can fund at 2 %, they are not going to pay you 3 % on a government bill.

- MAS is happily neutral. The central bank left the SGD NEER slope alone in April and has not drained liquidity. Result: the banking system is swimming in deposits.

- Supply is steady as a rock. Auction size has been stuck at S$7–7.5 bn for almost a year. No squeeze, no spike.

- Retail money keeps turning up. Every fortnight, investors throw >S$15 bn at the T-Bills auction despite the sharp drop in interest rates. Liquidity clearly matters more than a few basis points.

- Fixed‑deposit promos lost their shine. In January you could lock in 2.8 % for six months; today most banks are dangling 2.15–2.25 %. That makes a 2 % T‑bill look… tolerable.

Put those five ingredients together and that has led to the collapse in T-Bills yield:

Where are we on the chart?

I plotted every six‑month auction this year above.

It’s basically a ski‑slope: 3.04 % in late‑Jan → 2.00 % now, with one lonely bounce in late‑March.

The line of best fit is dropping about 11 bp every auction – painful if you’re chasing yield, lovely if you bought early and can brag.

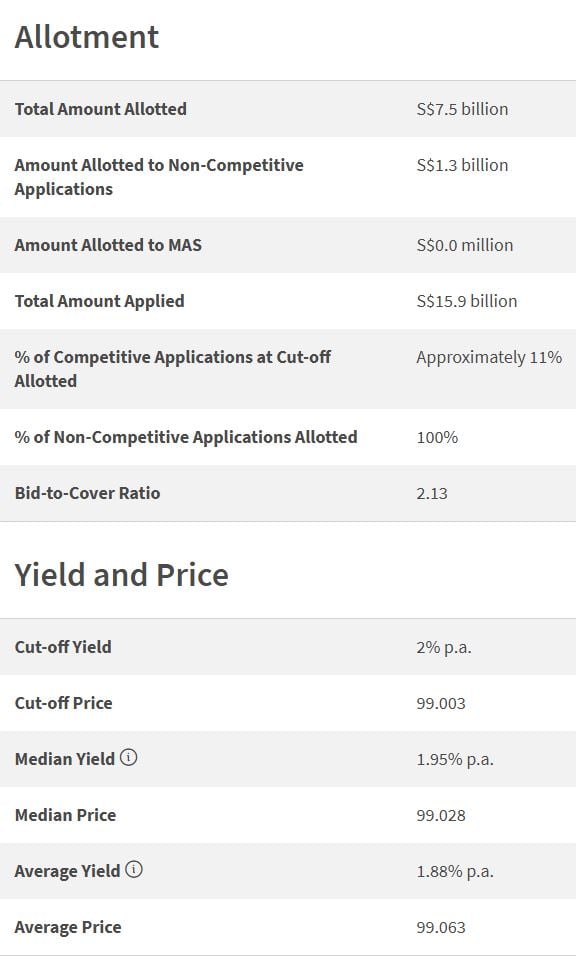

Key stats from the 19 June auction (code BS25112X):

- Cut‑off yield: 2.00 % (‑5 bp vs 5 Jun)

- Bid‑to‑cover: 2.13× (S$15.9 bn bids for S$7.5 bn supply)

- Median bid: 1.95 % Translation: the crowd is already happy to lend the government money at a ‘1‑handle’.

Follow Financial Horse to avoid missing any post!

Crunching the numbers for 3 July T-Bills Auction

I know some of you enjoy the quant side, so here’s the quick‑and‑dirty model I run each fortnight:

| Method | Fair yield |

| Trend line (last 6 auctions) | 1.94 % |

| Secondary‑market price (20 Jun close) | 2.00 % |

| SG‑US regression (beta 0.35 vs 6‑m US bill) | 1.95 % |

Weight them 40/40/20 and you get 1.97 %. Sprinkle a ±5 bp error bar and you have my base case: 1.90 –2.05 %.

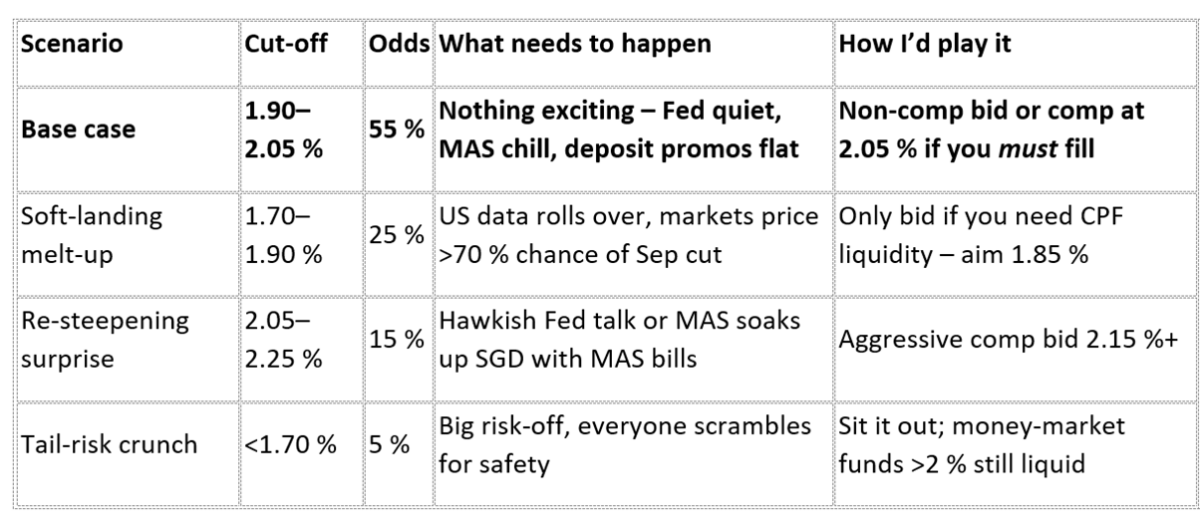

Scenario grid for T-Bills Auction (because life is messy)

In picture form:

And the same in text form:

| Scenario | Cut‑off | Odds | What needs to happen | How I’d play it |

| Base case | 1.90–2.05 % | 55 % | Nothing exciting – Fed quiet, MAS chill, deposit promos flat | Non‑comp bid or comp at 2.05 % if you must fill |

| Soft‑landing melt‑up | 1.70–1.90 % | 25 % | US data rolls over, markets price >70 % chance of Sep cut | Only bid if you need CPF liquidity – aim 1.85 % |

| Re‑steepening surprise | 2.05–2.25 % | 15 % | Hawkish Fed talk or MAS soaks up SGD with MAS bills | Aggressive comp bid 2.15 %+ |

| Tail‑risk crunch | <1.70 % | 5 % | Big risk‑off, everyone scrambles for safety | Sit it out; money‑market funds >2 % still liquid |

Should you even bother?

CPF‑OA money

Break‑even vs CPF’s guaranteed 2.5 % is about 2.83 % after adjusting for the lost interest. At a 2 % T‑bill you’re losing roughly 0.8 % annualised.

Bottom line – don’t buy T-Bills with CPF.

Plain‑vanilla cash

Compare against fixed deposits. If a bank hands you 2.25 % for six months with SDIC insurance up to S$100k, that’s already better. T‑bills only win on credit quality or if you need a short settlement cycle.

Building an income barbell

Sub‑2 % on the front end drags your blended yield unless you pair it with 3–4 % corporate notes or REIT perpetuals. Think of the T‑bill as the cash buffer, not the return driver.

What could surprise?

- Fed surprises hawkish. Pushes USD bills to 4.6 %, drags SGD swaps +20 bp, T‑bill clears 2.3–2.4 %.

- MAS recentres the NEER in October. Liquidity tightens, auction size maybe rises to S$9 bn. Yields pop 20‑30 bp.

- Banks crank up deposit promos. A 2.5 % six‑month promo forces competitive bids higher.

- Global risk‑off. Everyone hides in bills; yields print a 1.6 handle.

Keep one eye on Fed funds futures and the MAS auction calendar; those two lines will telegraph most surprises.

My game plan (not financial advice!)

- CPF‑OA: Skip unless cut‑off >2.4 %. The negative carry isn’t worth it.

- Cash float: If you really want, use a competitive bid. Otherwise, chase the best fixed deposit board rate.

- Income portfolio: Stick to a barbell – short T‑bills for safety, overweight quality SGD corporates (or US investment grade SGD hedged) for yield.

Alternatives to T‑Bills: where to park idle cash?

Table in picture form:

And text form:

| Instrument | Gross yield (6‑m equivalent) | Liquidity | Credit risk | My quick take |

| Bank fixed deposit (promo) | ~2.25 % | Break‑early penalty | SDIC‑insured ≤ S$75k per bank | Best balance if you can lock funds and promo ≥2.25 % |

| High‑yield savings account (multiplier) | 2.0–3.5 % (if conditions met) | Daily | Bank credit | Great if you already hit spend/salary triggers; hoops may be annoying |

| Money‑market fund (unit trust) | ~2.1 % net | T+1 redemption | Diversified ST paper | Seamless liquidity; watch expense ratio |

| Singapore Savings Bond (latest issue) | 2.49 % first‑year, avg 2.80 % ten‑yr | Monthly redemption (1‑mo interest forfeit) | AAA sovereign | Better for >1‑yr horizon; not ideal for 6‑m parking |

| Short‑term corp note (AAA/AA) | 3.0–3.3 % | OTC secondary, bid‑ask spread | Corporate | Adds yield but less liquid; min size S$250k |

My pick right now:

If you can spare six months, an SDIC‑insured promo FD at ≥2.25 % edges out the T‑bill without extra risk.

Need daily liquidity? A low‑fee money‑market fund around 2.1 % beats the bill with T+1 liquidity.

Alternatively a high yield savings account works if you can fulfil the requirements without too much hassle.

Final thoughts on T-Bills

T‑bill yields are falling because the system is flush and nobody has a burning need for the cash.

Until MAS or the Fed turns off the liquidity tap, don’t expect miracles. Park your cash smartly, keep an eye on promos, and remember – sometimes the best trade is keeping powder dry.

Enjoy the rest of your weekend, and may your kopi stay hot and your yields stay juicy.

Horse out.

This post is written on 25 June 2025 and will not be updated going forward. My latest views on markets, my Stock watchlist and full Personal Portfolio, are shared on FH Premium.

That last comment “…sometimes the best trade is keeping powder dry…” says it all. The stockmarkets look relatively expensive right now.

Fair enough!

Hi FH,

SDIC insurance had been increased from up to S$75k to S$100k per customer since 1 April 2004. Please update your article above.

My bad – updated!