I’ve been getting quite a few questions to continue the T-Bills series of articles, especially with T-Bills yields creeping back up again on reduced rate cut expectations.

So that’s exactly what we’ll do today.

3 questions I wanted to discuss today:

- Estimated yield on the next 6-month T-Bills auction?

- What are the alternatives to T-Bills in this market? Fixed Deposit, Money Market Funds, Bonds?

- Will I start buying T-Bills again?

Estimated yield on the next 6-month T-Bills auction?

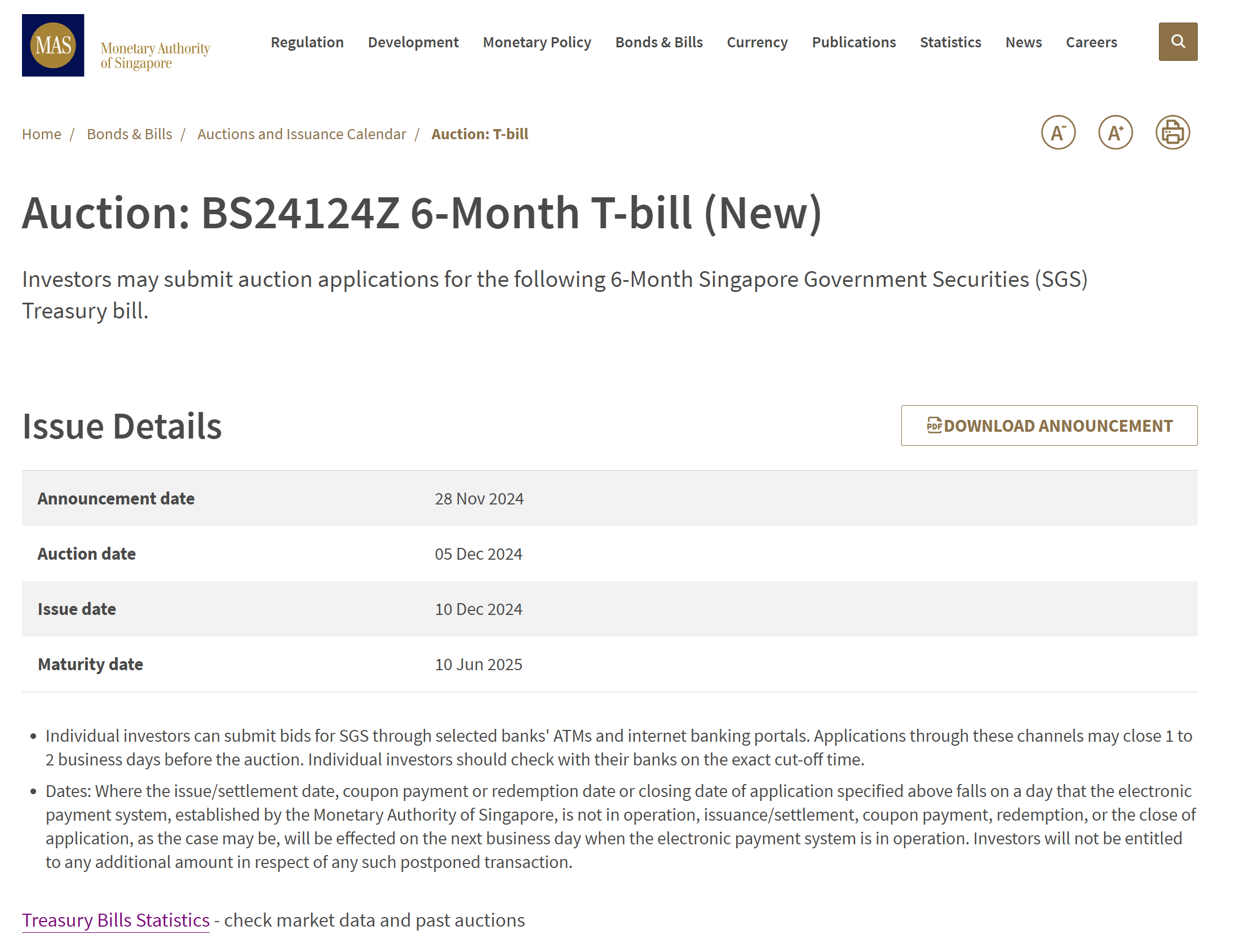

The next 6-month T-Bills auction is on 5 Dec (Thurs).

Deadline to apply is therefore:

- 9pm on 4 Dec (Wed) for cash applications (and CPF-OA applications via DBS or OCBC internet banking)

- 9pm on 3 Dec (Tues) for UOB CPF-OA applications

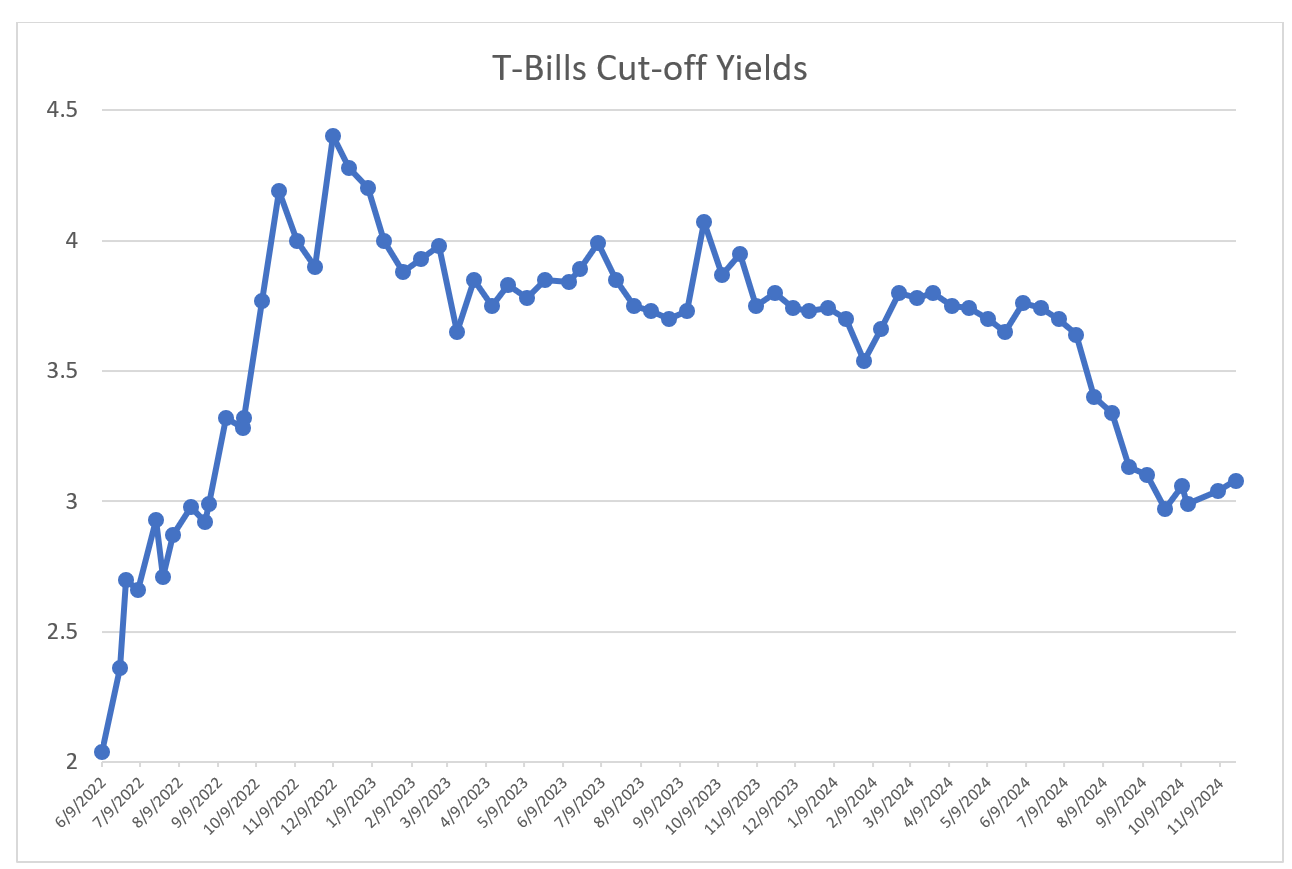

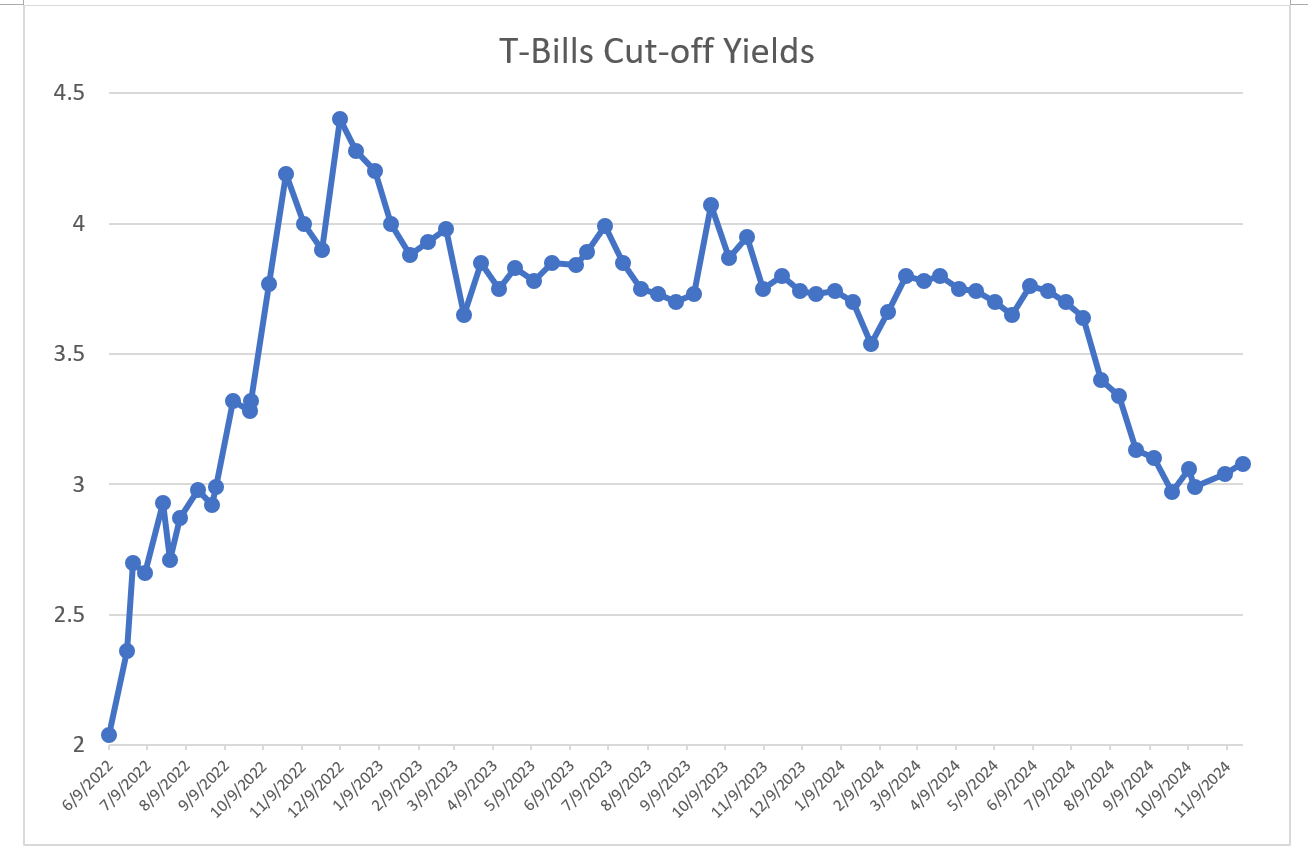

6-month T-Bills yields rose to 3.08% at the most recent auction

In the most recent 6-month T-Bills auction, cut-off yields went up slightly to 3.08% (was 3.04% the previous auction).

Charted below, you can see how this has crept up slightly the past few auctions, but big picture wise its still down a lot from 1 – 2 years ago.

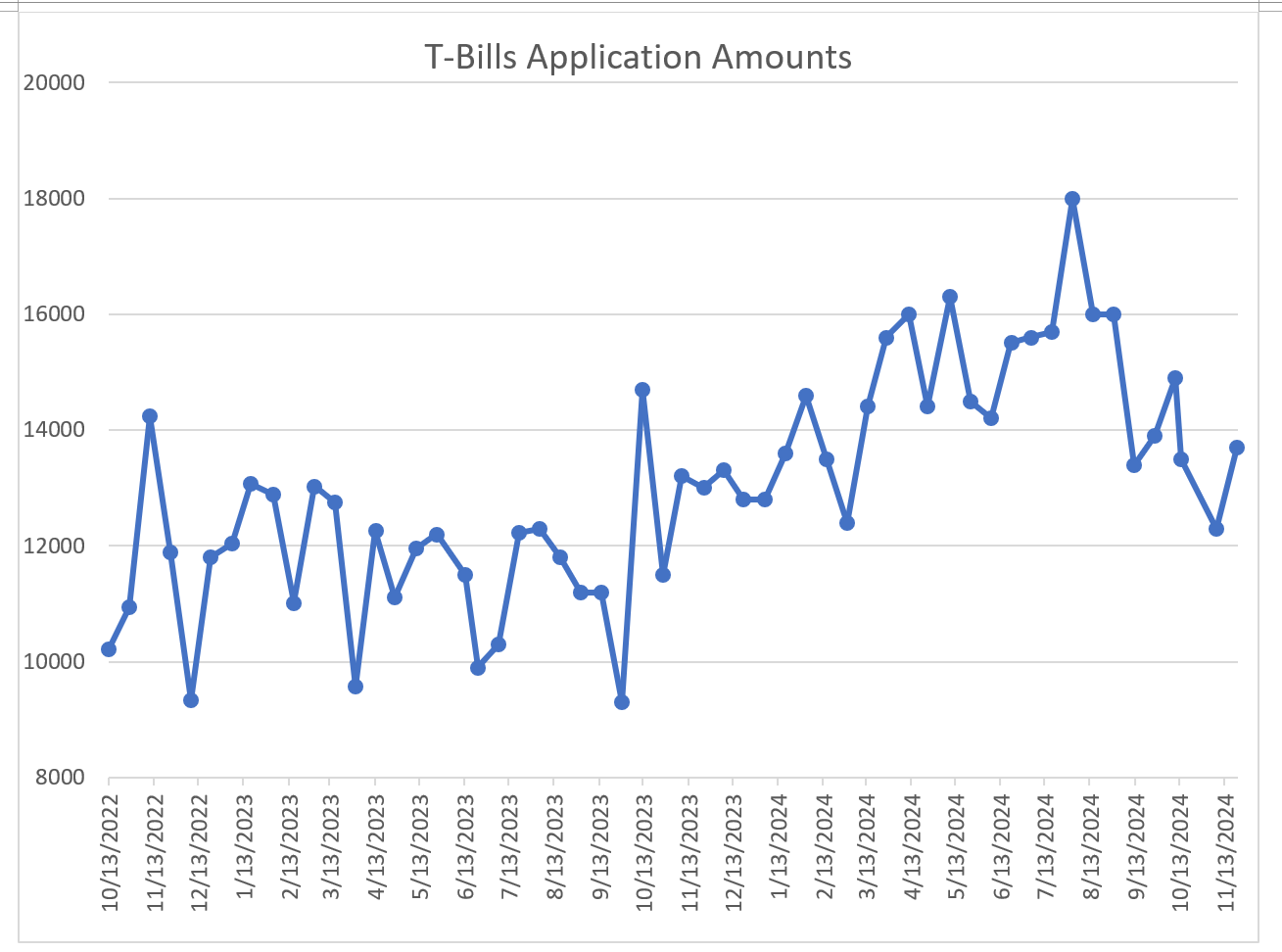

Despite the fall in T-Bills yields, demand remains very high.

At the most recent auction, demand actually increased 11% to $13.7 billion.

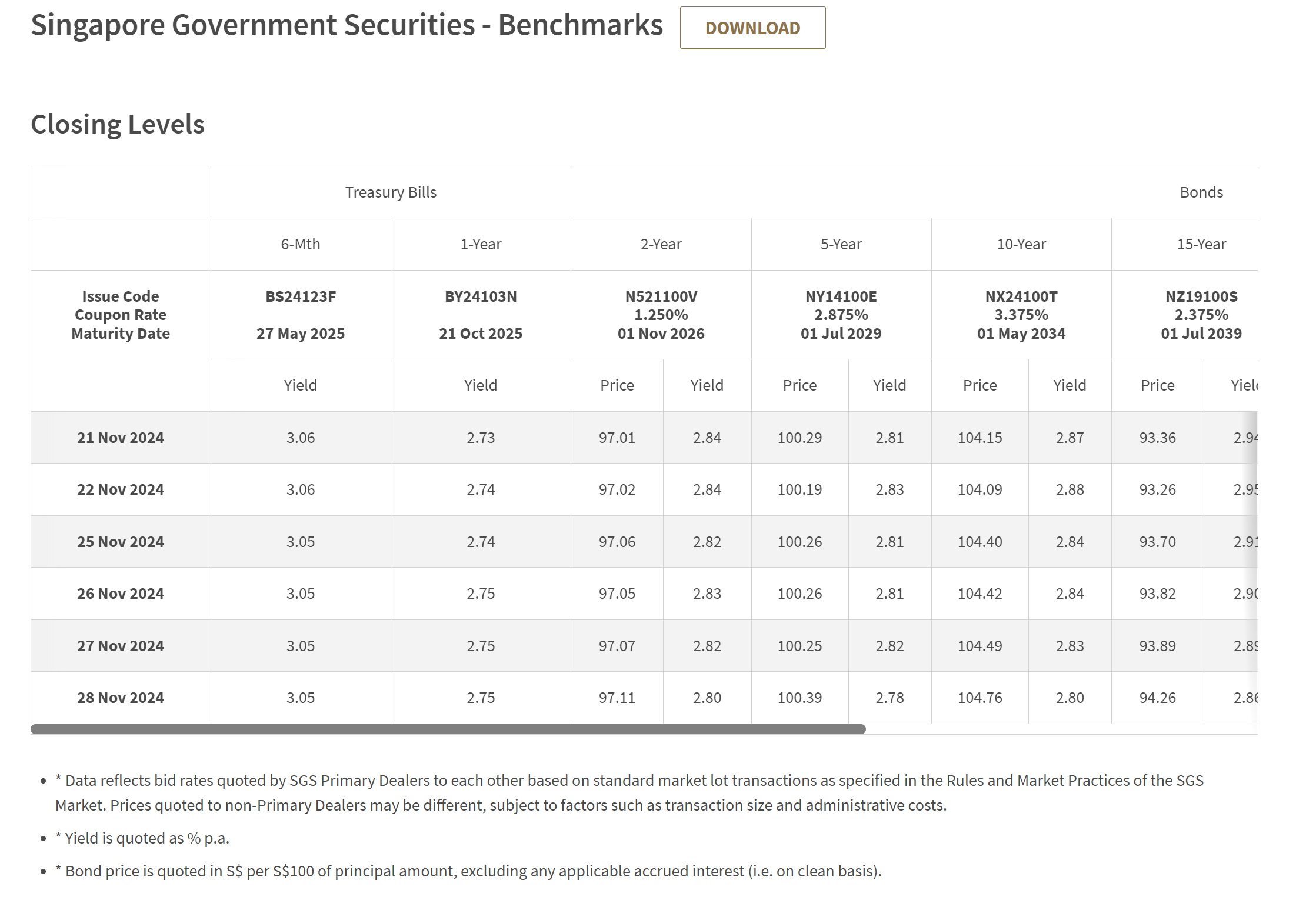

6-month T-Bills yields stable on the open market – trading at 3.05%

On the open market – 6-month T-Bills trade at 3.05%.

That being said – trading liquidity on the T-Bills is so thin that actually the market pricing is not that useful.

So I would caution against placing too much reliance on market pricing on T-Bills.

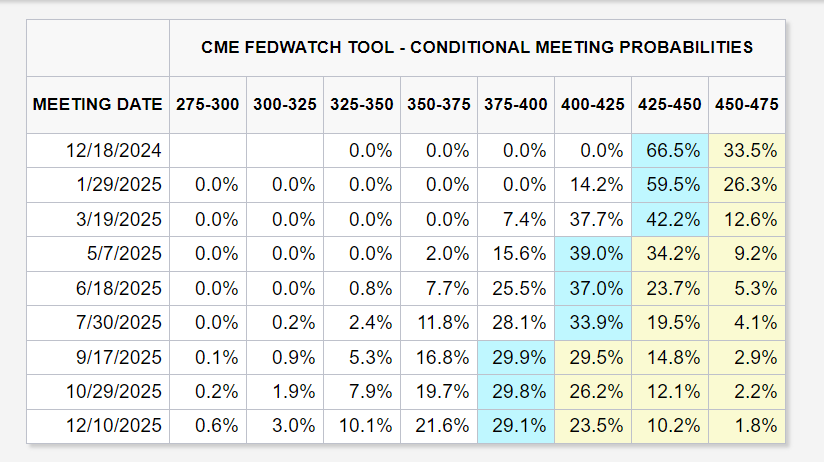

Market is only pricing in 3 more rate cuts the next 12 months

The bright side (for yields) is that the market is no longer pricing in as many rate cuts.

Because of Trump’s win, and expectations for a strong US economy – the market is only pricing in 3 more rate cuts the next 12 months.

That being said, this hasn’t changed materially the past few weeks, so I wouldn’t expect this to have a significant impact on the T-Bills auction yields.

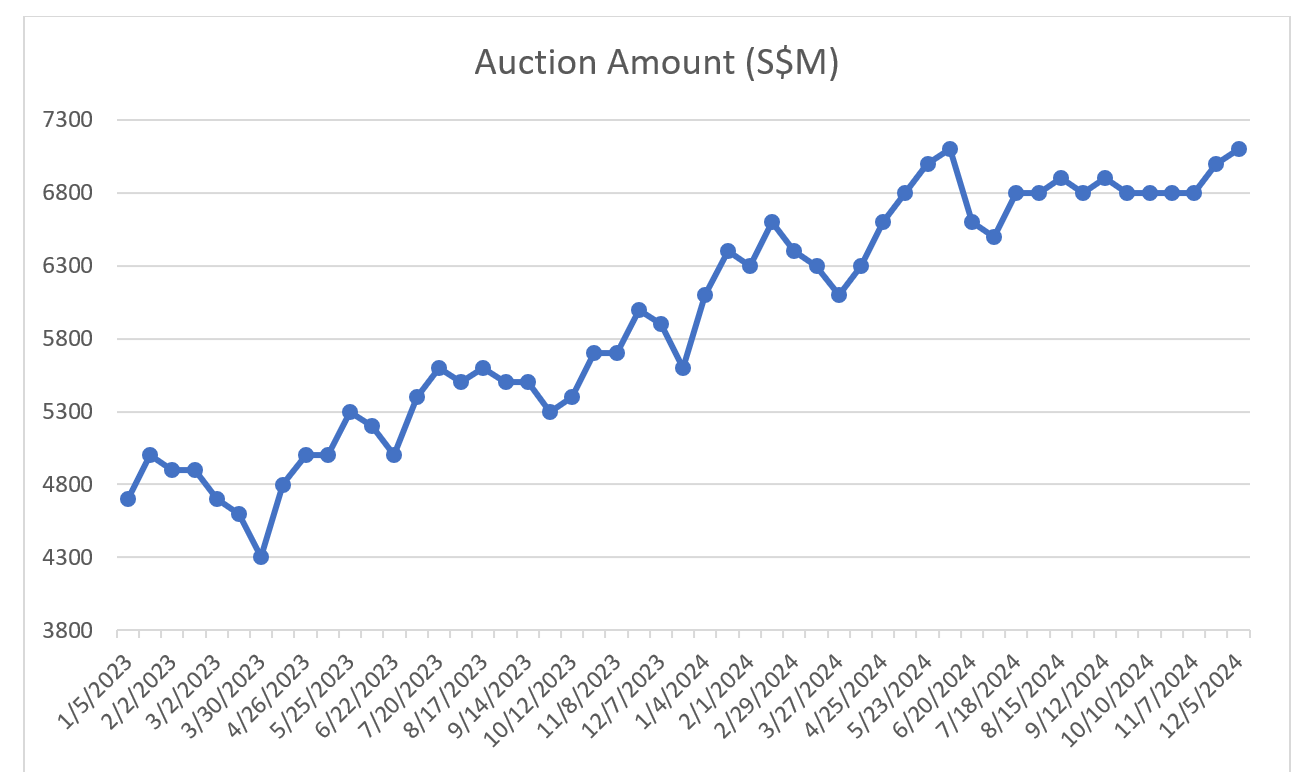

T-Bills Supply is up to $7.1 billion ($6.8 billion 2 auctions ago)

More good news is that on the supply side, auction amount is picking up to $7.1 billion.

You can see how the auction amount has picked up the past 2 auctions – which has coincided with the rise in yields (although its not so clear whether this is what caused the rise in yields).

Estimated yield of 3.00% – 3.15% on the 6-month T-Bills auction?

Market yields are 3.05%, but the rise in auction amounts, coupled with the recent trend of higher yields, suggest that there is a chance we could see a pickup in yields.

Putting everything together.

I’m going with an estimated yield of 3.00% – 3.15% for the next 6-month T-Bills auction.

What are the alternatives to T-Bills in this market? Fixed Deposit, Money Market Funds, Bonds?

Let’s discuss both ends of the barbell – the extremely short duration cash equivalents (<6 months), and the mid duration bonds (>1 year).

Money market fund instruments (like MariInvest) or fintech plays (like Chocolate Finance/GXS/FD) on the short end

MariInvest which is a money market fund pays about 3.29% over the past 30 days for me.

As a money market fund investing primarily in MAS Bills, it’s pretty low risk, with competitive yields, with very good liquidity (first $10,000 can be withdrawn instantly, rest is T+1 liquidity).

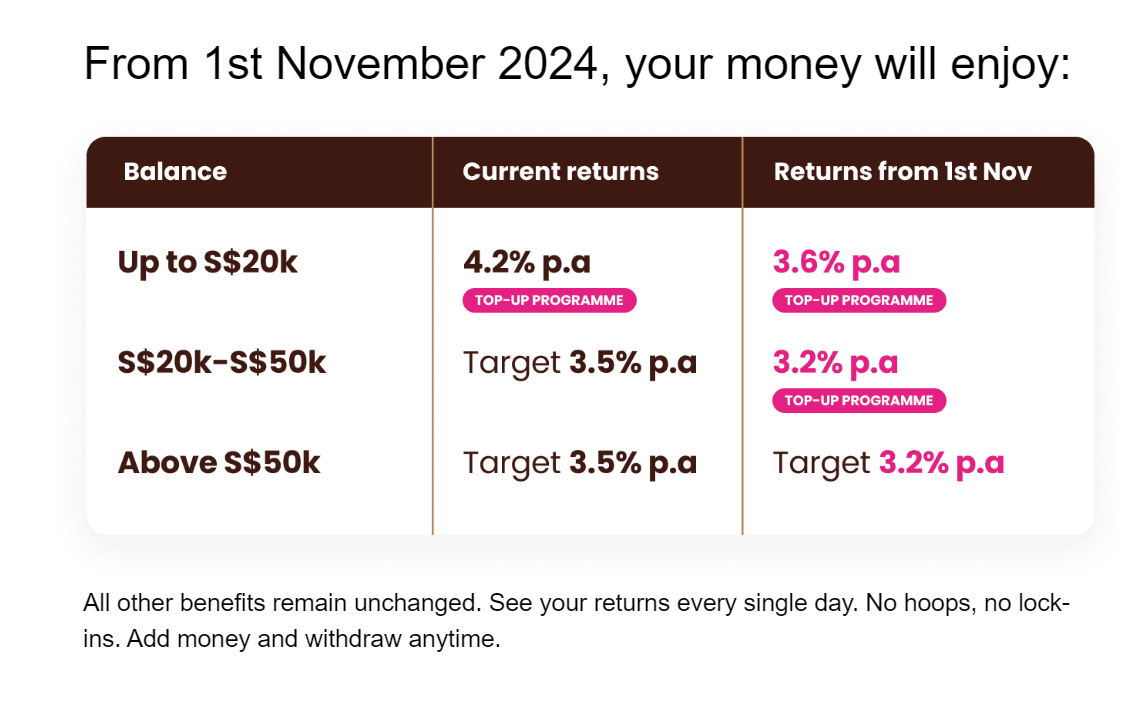

Alternatively, there’s stuff like Chocolate Finance that even after the drop in rates, will pay 3.6% on the first $20,000.

Follow Financial Horse to avoid missing any post!

Even stuff like a DBS Fixed Deposit is paying 3.20% for 12 months, higher than T-Bills (note this is up to $19,999 only, and it steps up to 3.3% if you are above 55):

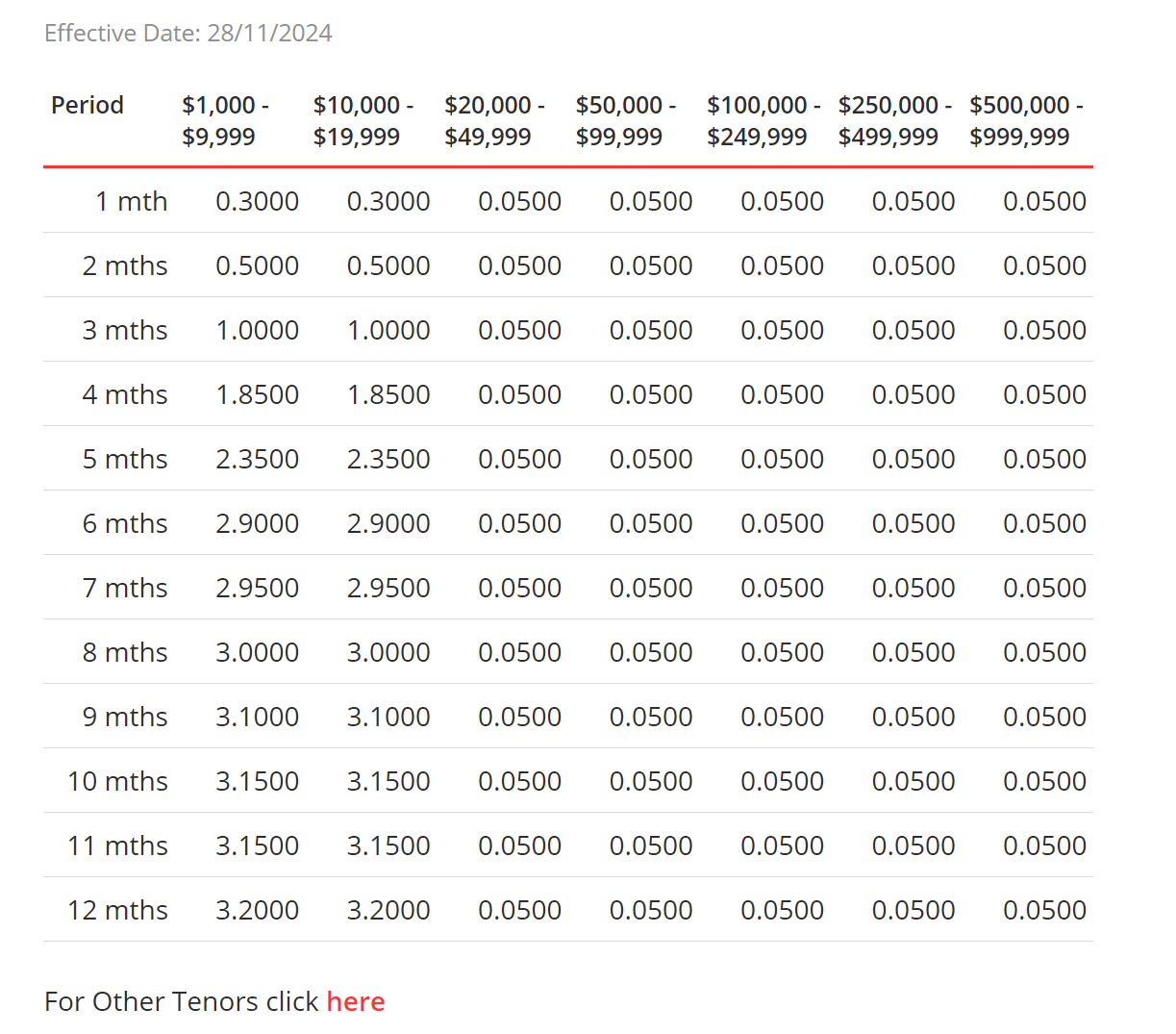

Syfe Cash+ Guaranteed allows you to access institutional fixed deposit rates.

You can see the latest rates below, and frankly they are not amazing and you’re probably better off with the other instruments on this list.

Short duration bond funds on the long(er) end

As shared in previous articles, I quite like short duration bond funds (2 year duration or so) given where we are.

I shared my thought process in a previous article, which I extract loosely below:

My personal view, is that it’s all about risk-reward.

It is for this exact reason that I advocate building exposure at the short duration bond space, and not the long duration bond space.

If I buy bonds with a 2 – 3 year duration.

If there is indeed a soft landing, default rates will be close to zero, so I collect my 5%+ yield the next few years.

Sure if interest rates go to 5.0% I may suffer capital losses, but given the short duration nature of the bonds those losses will be manageable, and go away the longer I hold the bond funds.

If there is a hard landing, interest rates will get slashed, and there is capital gains potential on these bonds.

The complexity is that in a recession there is default risk for the underlying bonds, but I would say if you’re playing in Investment Grade credit I *think* the defaults will be manageable barring a bad recession.

But of course there is risk, and there is no free lunch in this world.

From a portfolio perspective, the way I see it, with the Feds on a rate cut cycle, it makes sense to shift some funds out of cash and into short duration bond funds.

But I want a mix of both short term cash instruments (<6 month duration) and short term bonds, to cater for a wide range of outcomes.

The US 2 year yield trades at about 4.2% today, so even if you stick purely to investment grade credit you’re probably looking at a 5-6% yield, even after hedging back to SGD.

I think that’s a pretty decent option in today’s market.

Now to be clear I’m not saying to park all of your liquid cash into bonds – because there are still risks involved.

But it may make sense to put a certain percentage of your cash into bond funds, to lock in a longer duration and higher yield.

At least – that’s what I’ve been doing with my own cash.

Will I start buying T-Bills again?

Will the recent pickup in T-Bills yields.

I think T-Bills are back to being competitive as a cash management product again.

Main benefit being that T-Bills are risk free, and it’s a park and forget for 6 months kind of instrument.

SGD as well – so no FX risk.

The drawback is (and always has been) that you cannot get liquidity back on short notice.

Which is why you cannot park all of your cash in T-Bills, and you need to have some funds in other instruments like UOB One, Singapore Savings Bonds, and so on.

Personally I’ve been splitting my cash on both ends of the barbell – short term parked primarily in UOB One, SSBs, and Money Market Funds.

And mid term parked in bond funds / bonds.

I’ve generally been letting my T-Bills roll off and using the funds to invest into markets (increasing risk exposure in anticipation of and post Trump win).

But now my risk exposure is at a place where I am comfortable where it is again (see my full portfolio shared on FH Premium).

So who knows I may apply for T-Bills again the next couple of auctions.

Would love to hear what you think though!

Will you apply for T-Bills? Or park your cash elsewhere?

Deadline to apply for the T-Bills auction on 5 Dec (Thurs)

The next 6-month T-Bills auction is on 5 Dec (Thurs) for those keen to apply.

Deadline to apply is therefore:

- 9pm on 4 Dec (Wed) for cash applications (and CPF-OA applications via DBS or OCBC internet banking)

- 9pm on 3 Dec (Tues) for UOB CPF-OA applications

Follow Financial Horse to avoid missing any post!