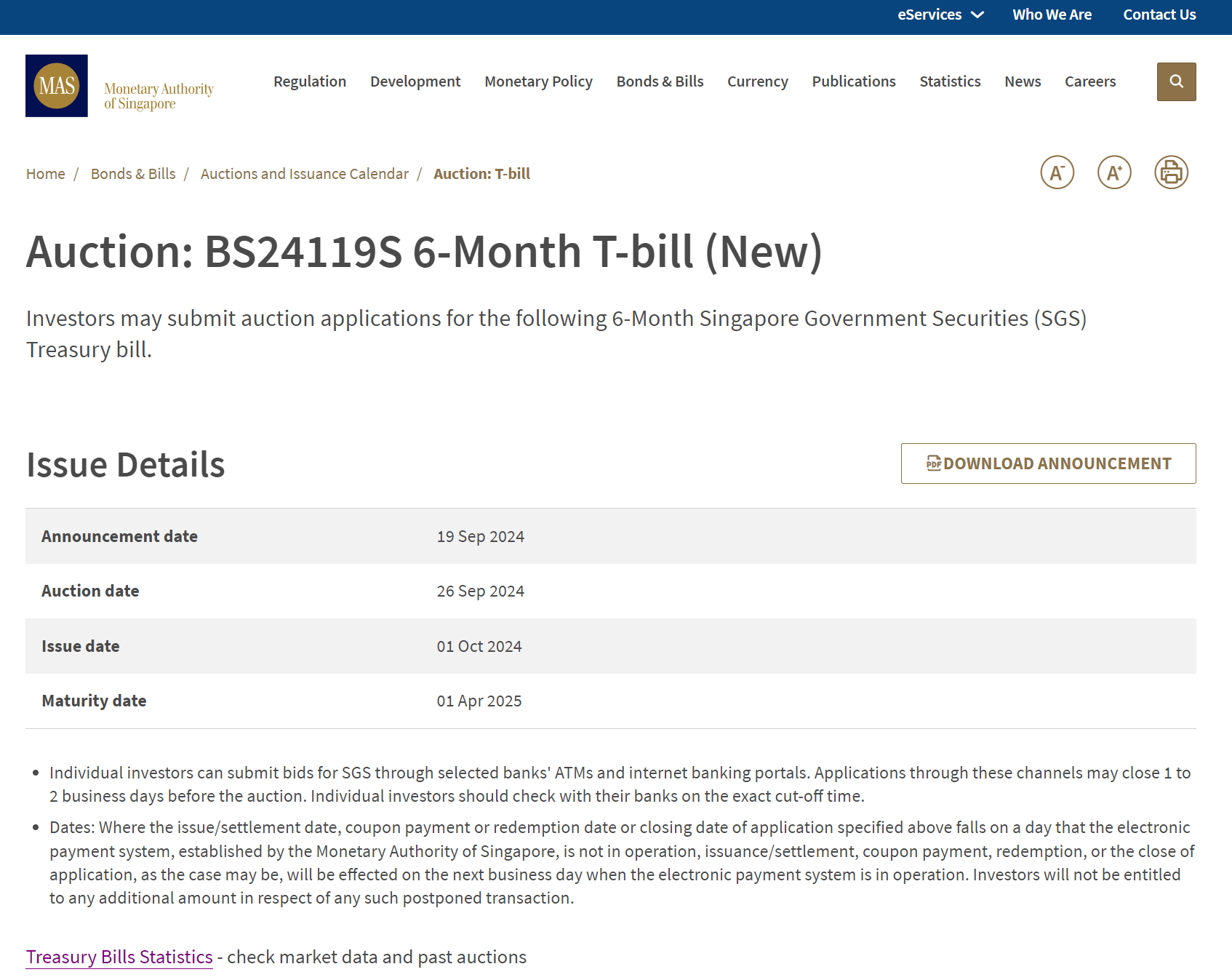

The next 6-month T-Bills auction is on Thursday 26 Sep 2024.

Given that the Feds just did a jumbo 0.50% rate cut this week.

Quite a few of you have been asking whether we’ll see a further drop in T-Bills yields at next week’s auction.

The last T-Bills auction had a 3.10% cut-off yield, so if it falls further then T-Bills really aren’t that attractive any more.

Reflecting this, we saw demand for T-Bills fall quite sharply in the most recent auction, and spreads indicating tighter bids – indicating that most investors have caught on to this fact (that T-Bills are no longer a must buy).

2 points I wanted to discuss.

- Will T-Bills yields drop further after Fed rate cuts?

- Will I still buy the 6-month T-Bills despite falling interest rates?

Will T-Bills yields drop further after Fed rate cuts? What is the expected yield on the next 6-month T-Bills Auction?

Jerome Powell’s Fed cut interest rates by 0.50% this week

In case you missed it, Jerome Powell’s Fed cut interest rates by 0.50% this week.

You can see the full transcript here, where Powell tries to paint an optimistic picture of the US labour market and insist that the Feds are not behind the curve here.

But if you ask me, I would say that as Fed Chair, he really couldn’t have said anything else.

My personal take is that recent US data paints a picture of a slowing labour market, and between inflation and unemployment, I think the risk has now tilted towards the latter.

So the Fed was slightly behind the curve here, and they had to “catch up” so to speak.

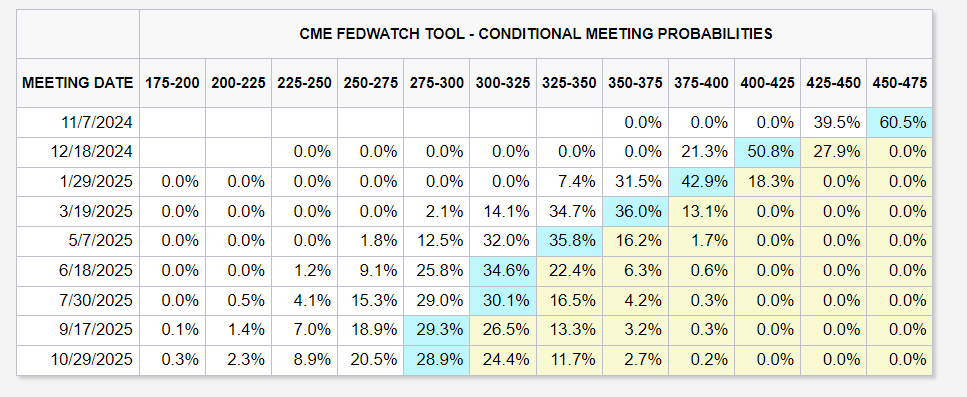

The market today is pricing in another 2.0% in interest rate cuts in the next 12 months.

I know a lot of you have commented that that’s a lot of cuts, and given how strong the US economy today is that may not be justified.

Personally I’m not so sure about that given latest data showing a weakening labour market, but we’ll see.

The key now is whether the Fed rate cuts will be enough to stimulate the economy, or whether unemployment starts to pick up steam going forward.

Assuming this path of rate cuts plays out – what is the final T-Bill yield?

Historically the SGD 6-month yield trades at about 0.5 – 1.5% lower than Fed Funds.

So if you assume the terminal Fed Funds Rate will be 2.75% – 3.00% in mid 2025 (which is what the market is pricing in).

That give us a ballpark of 1.5% – 2.5% for the SGD 6 month T-Bill in mid 2025.

Will this play out?

Again, much will depend on the path for the US labour market going forward, so let’s see.

6-month T-Bills yields dropped to 3.10% at the most recent auction (3.13% at the previous auction)

In the most recent T-Bills auction, cut-off yields dropped to 3.10% (was 3.13% the previous auction).

This is the lowest yields we’ve seen over the past 18 months.

6-month T-Bills yields slide on the open market – trading at 3.07%

On the open market – 6-month T-Bills continue their slide.

Trading at 3.07%.

That being said – trading liquidity on the T-Bills is so thin that actually the market pricing is not that useful.

So I would caution against placing too much reliance on market pricing on T-Bills.

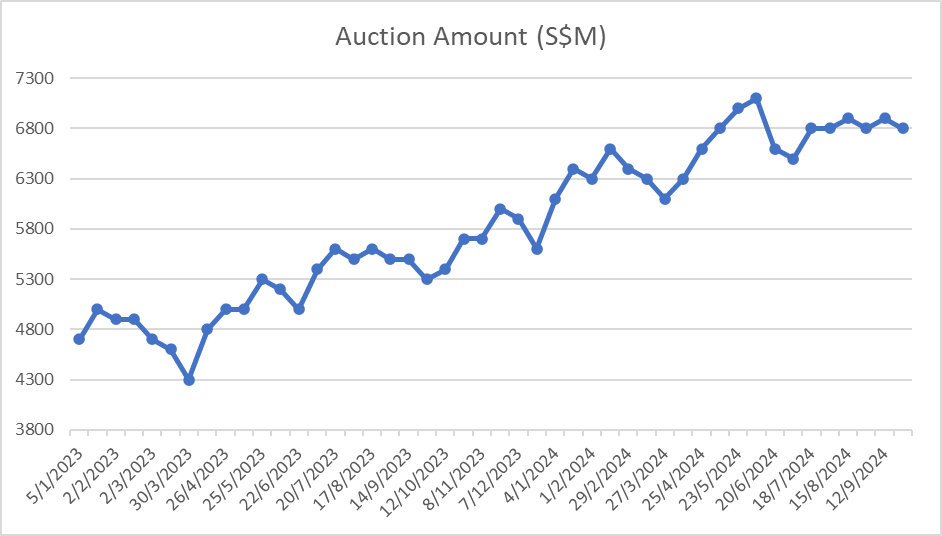

T-Bills application amount plunges to $13.4 billion (vs $16.0 billion previously)

The good news, is that with the sharp drop in yields, T-Bills application amounts also fell sharply.

This makes sense, given that with the lower yields T-Bills are no longer a must buy.

We’re seeing $13.4 billion in demand, a huge 16.25% drop in application amount vs the previous auction.

Spreads for T-Bills dropped – indicating tighter bidding

At the same time, we’re seeing a sharp drop in spreads between the median and average yield for bids submitted.

This is a good sign, as it suggests that investors are starting to be more rational in their bidding (less low-ball bids so to speak).

T-Bills Supply is flat at $6.8 billion (vs $6.9 billion at previous auction)

The bad news – is that we’re not getting much reprieve in the form of higher supply.

T-Bills auction amount is $6.8 billion, which is almost flat vs the $6.9 billion we saw in the previous auction.

Estimated yield of 3.00% – 3.15% on the 6-month T-Bills auction?

I could be wrong, but I think we’ll see T-Bills yields stabilize around the levels its trading at on the open market (3.07%).

Yes the Feds did a larger than expected rate cut this week, but much of this had already been priced in by the market even before that (marked priced in at least 1 50bps rate cut in 2024).

The wildcard is demand.

If investor demand for T-Bills continue to fall, and bidding spread continues to narrow, we could well see an uptick in yields.

I would probably go with an estimated yield of 3.00% – 3.15% on the next T-Bills auction.

That said, I do encourage investors to submit a competitive bid, so if there is a surprise on the downside you are not forced to buy.

Will I still buy 6-month T-Bills with lower interest rates?

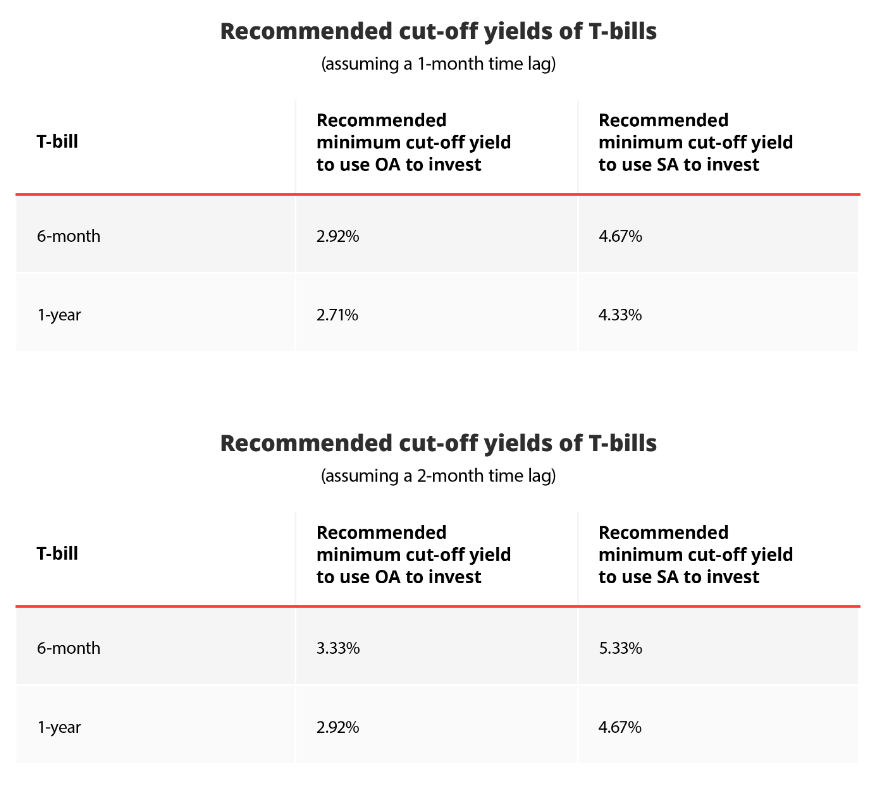

For CPF-OA – Breakeven is 2.92%

Note that if you’re buying T-Bills with CPF-OA, the “breakeven” rate is 2.92% because of lost interest.

Here’s the explanation from DBS below:

It is not as straightforward as you will need to work out the “breakeven” yields of T-bills for using CPF savings to ensure that you will not be in a worse off position.

This is partly because the interest computation of CPF balances is affected by the transactions in your CPF account. Contributions received this month start earning interest next month and withdrawals/deductions in this month will not earn interest from this month onwards.

Depending on when the deduction is done from your CPF account, you might lose up to 2 months of CPF interest. Taking that into account, these are the cut-off yields for T-bills that will result in a higher return than that of CPF-OA and SA yields.

Still worth buying T-Bills with CPF-OA?

At 3.10%, the profit you are making isn’t really that big.

Unless you have a large amount of cash in your CPF-OA, it may not really be worth the time and effort to continue applying anymore.

Once my current batch of CPF-OA T-Bills expire, I don’t really see myself rolling them over into T-Bills anymore unless yields pick up.

Alternative to T-Bills for Cash?

For cash, these are the other options available:

| Yield (indicative) | Liquidity | Level of Risk? | |

| Bond Funds | 4%+ | Average | Moderate |

| Chocolate Finance | Good (4.2% on first $20,000) | Good | Low – Moderate |

| High Yield Savings Account (Eg. UOB One) | Good (4%) | Good | Risk free if below SDIC limit ($100,000) |

| Money Market Funds (Eg. MariInvest, Fullerton SGD Cash Fund) | Good (3.5 – 3.6%) | Good | Low – Moderate |

| T-Bills (6-months) | Average (3.10%) | Low (cannot exit before maturity) | Risk Free |

| Fixed Deposit | Average (3.1 – 3.35%) | Average | Risk Free if below SDIC limit ($100,000) |

| Singapore Savings Bonds | Low (2.59%) | Good | Risk Free |

Some readers have commented that with declining interest rates, it’s better to buy REITs or stocks instead.

Just to be clear, the purpose of this article isn’t to discuss that.

I myself am buying REITs / stocks, and you can see what I am buying on FH Premium.

The purpose of this article is mainly to discuss where I am parking my cash that is not invested in the markets.

Where am I parking my cash?

In the past the big chunk of them was in T-Bills, but with the sharp drop in yields it has definitely opened up alternatives.

For the recent maturing T-Bills, I have generally parked them:

- Money Market Funds (eg. MariInvest)

- Bond Funds (eg. Endowus Income)

Will I still apply for the T-Bills?

I have a pretty big chunk of T-Bills maturing soon, and if the money comes back before 25 Sep, I might just submit a competitive bid for the T-Bills.

I’ve skipped most of the auctions the past month or two, so I already have plenty of cash in alternative like Money Market Funds and Fintech plays.

So for the sake of diversification, I might pop some of them into T-Bills.

But again that’s just me, and theres no right or wrong here.

Actually with the sharp drop in T-Bills yields I find some of the Fintech options pretty attractive, that I discuss further below.

Follow Financial Horse to avoid missing any post!

I also send out a newsletter at 10am every Sunday – rounding up the posts from Financial Horse for the week. Sign up below!

4.20% on first $20,000 if you deposit to Chocolate Finance

I wrote a detailed review on Chocolate Finance, so do check if out if you are keen.

Long story short is that Chocolate finance pays 4.2% on the first $20,000, withdrawable instantly.

The funds are invested in a selection of bond and money market funds, and Chocolate Finance will top up any returns if they are lower than 4.2%.

With the sharp drop in interest rates across the board, suddenly Chocolate Finance’s 4.2% looks a lot more attractive.

That said I don’t expect this 4.2% to last forever, Chocolate Finance will likely reduce it at some point.

Until then at least, you can enjoy the higher yields.

Personally I have some cash in Chocolate Finance, but I do want to stress that this is not SDIC insured and not risk free.

I leave it for investors to decide if you are comfortable with the risks (see my full review here).

Chocolate Finance is invite only, but you can use the FH invite link below if you are keen to try it out:

https://share.chocolate.app/nxW9/ep4q7wxp

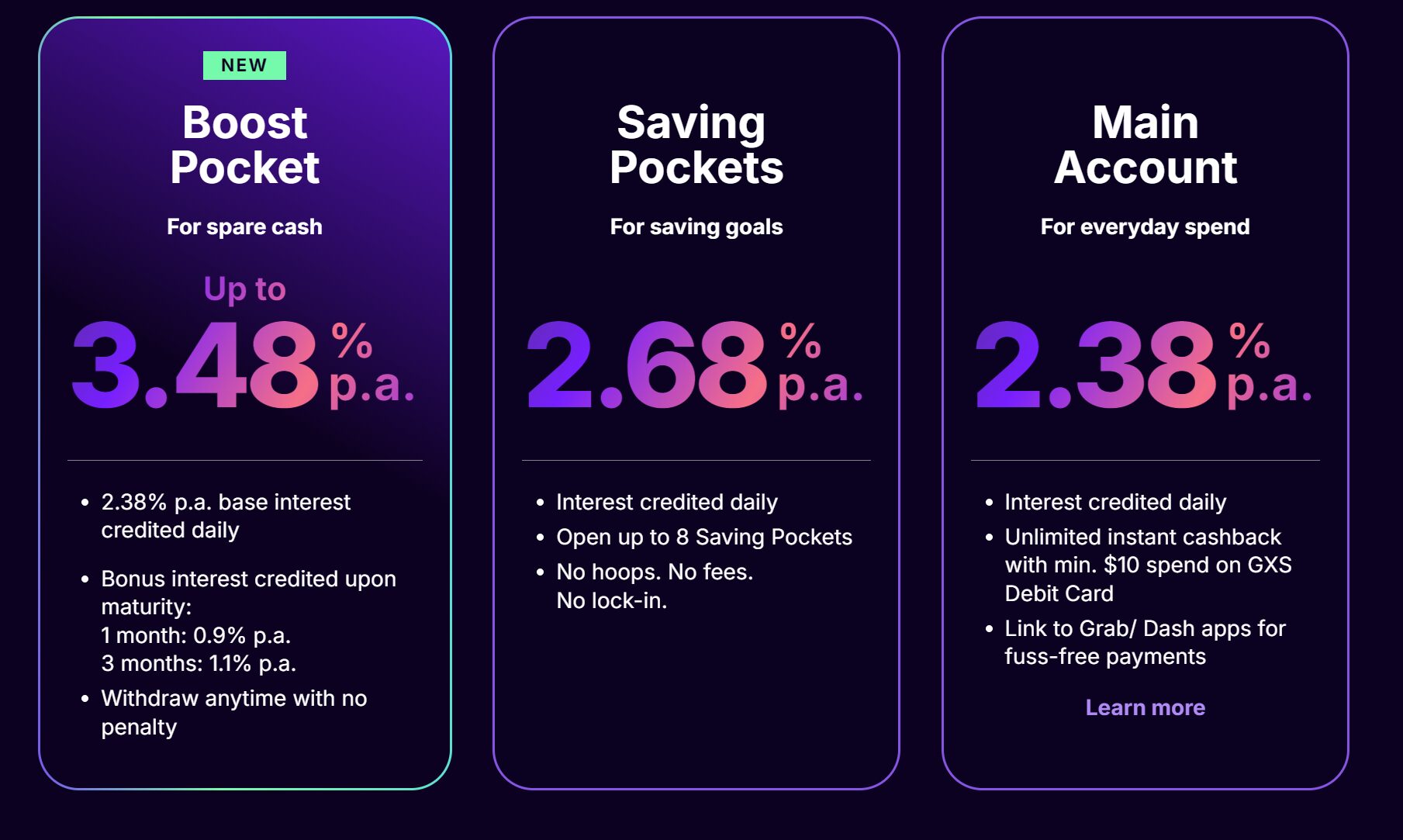

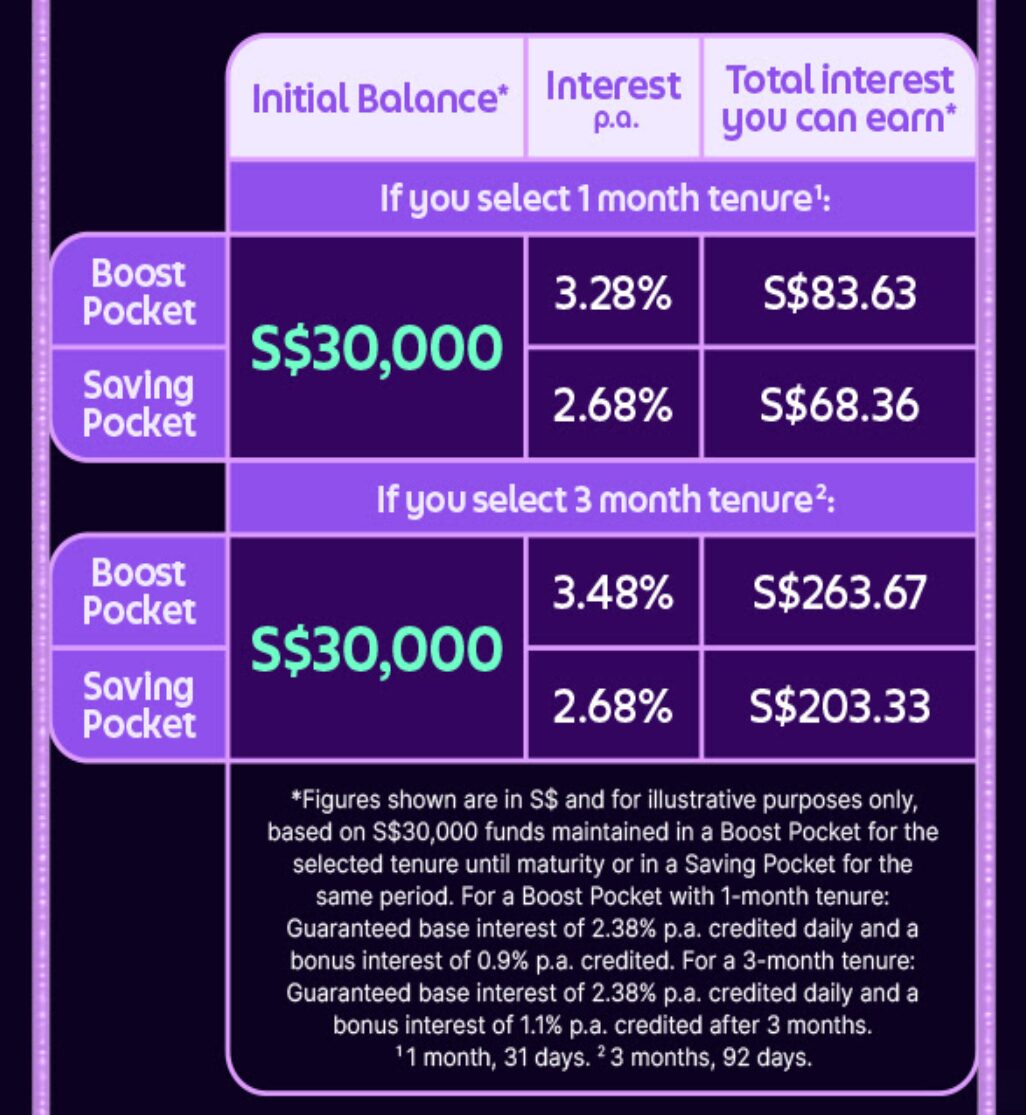

GXS Bank – Pays 3.48% yield for 3 months

Alternatively GXS Bank is running a promotion now.

If you deposit $30,000 for 3 months, you’ll get an effective yield of 3.48%.

GXS Bank being a digital bank means this is SDIC insured, so it’s a pretty good deal and in line with the best institutional fixed deposit rates available.

I myself topped up the full $30,000 to enjoy this promo rate.

Syfe Cash+ Guaranteed pays 3.20% yield for 3 months tenure

You can also consider Syfe Cash+ Guaranteed (who then deposits the cash into an institutional fixed deposit deposit).

This allows you access to institutional fixed deposit rates:

- 3.20% for 3 months

- 2.90% for 6 months

Rates are not amazing though, and if T-Bills stay at 3%+ they may be a better choice.

Do note that Syfe Cash+ Guaranteed is NOT SDIC insured though.

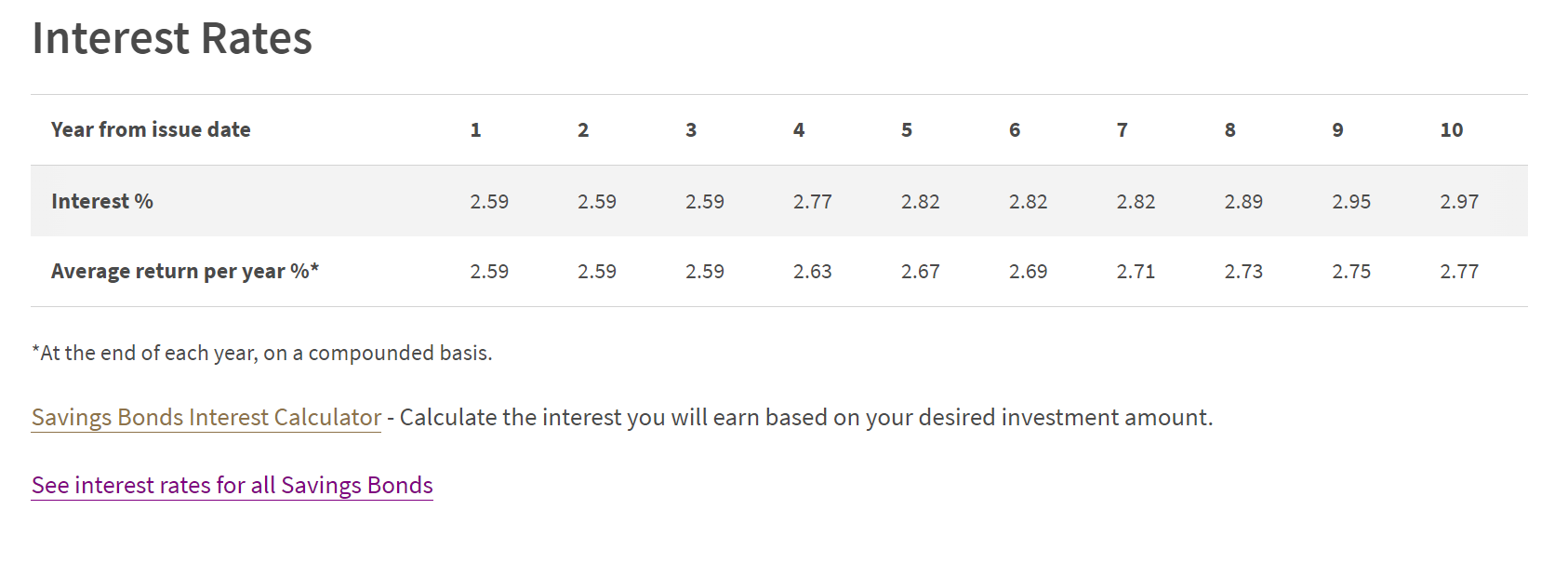

Singapore Savings Bonds are not that attractive

I bought quite a big of last month’s Singapore Savings Bonds as I thought the 3.06% first year yield was attractive given the sharply dropping interest rates.

With T-Bills yields falling to 3.10%, that did turn out to be a good move.

In any case this month’s Singapore Savings Bonds have much lower yields at 2.59%, and I don’t find them attractive at this level.

Deadline to apply for the T-Bills auction on 26 Sep (Thurs)

Next 6 months T-Bills auction is on 26 Sep (Thurs).

Deadline to apply is therefore:

- 9pm on 25 Sep (Wed) for cash applications (and CPF-OA applications via DBS or OCBC internet banking)

- 9pm on 24 Sep (Tues) for UOB CPF-OA applications

This post is written on 20 Sep 2024 and will not be updated going forward. My latest views on markets, my Stock watchlist and full Personal Portfolio, are shared on FH Premium.

Follow Financial Horse to avoid missing any post!

I also send out a newsletter at 10am every Sunday – rounding up the posts from Financial Horse for the week. Sign up below!

Saxo Brokers – Trade the 100 most popular US stocks commission-free

Saxo is running a promotion where new account holders can trade the Top 100 US stocks commission free (more details).

Special account opening bonus for FH Readers:

- Sign up via the link: Saxo Brokers

Chocolate Finance- pays 4.2% yield on first $20,000

Chocolate finance pays 4.2% on the first $20,000, withdrawable instantly.

The funds are invested in a selection of bond and money market funds, and Chocolate Finance will top up any returns if they are lower than 4.2%.

I wrote a detailed review on Chocolate Finance (note not SDIC insured).

- FH invite link below:

https://share.chocolate.app/nxW9/ep4q7wxp

Stock Café – track your portfolio performance (including dividends)

I use StocksCafe to track my portfolio and dividend stocks (full review).

- FH x StocksCafe Referral Code:

https://stocks.cafe/user/tosignup?referral_code=financialhorse