In response to the recent Temasek Bonds offered at 1.8%, many of you commented that the interest rate was too low.

So when OCBC approached us with Allianz SGD Income Plus II, which features a monthly dividend pay-out of 3.5% – 4.5% p.a.* at 0% sales charge, I was pretty keen to check it out. (FYI – This 2nd Tranche II is a follow up from Tranche I that sold out earlier this year.)

In this yield-starved environment we are living in, how do they achieve such a high dividend pay-out?

Is it worth investing in?

Note: This post was sponsored by OCBC and this fund’s tranche II is available exclusively to OCBC customers and for a limited time only. All views and opinions expressed in this post are from Financial Horse.

Basics: Allianz SGD Income Plus II – Monthly dividend pay-out of 3.5% – 4.5% p.a.* at 0% sales charge

The main features of Allianz SGD Income Plus II are:

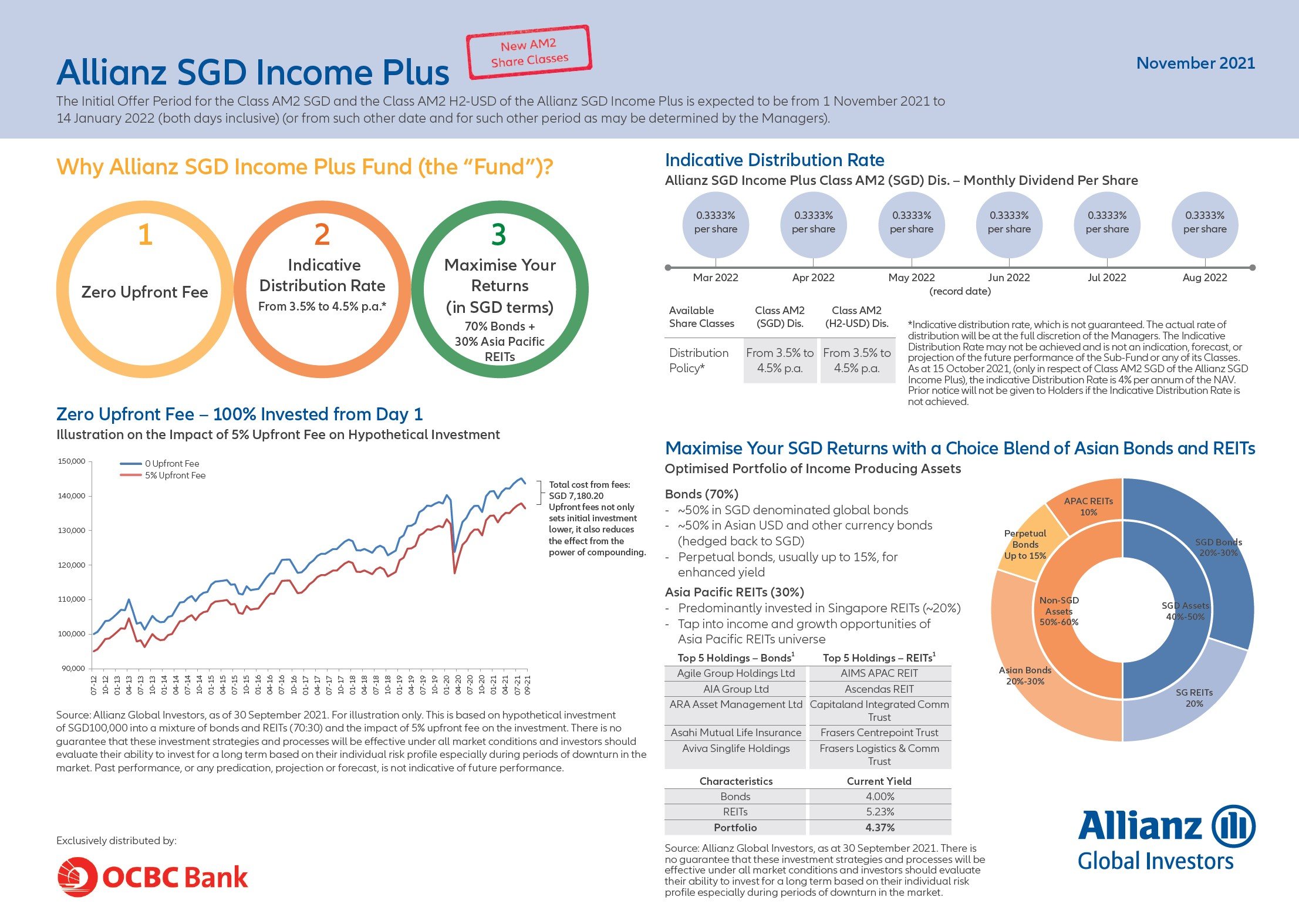

- Asset allocation (70% bonds, 30% REITs)

- Indicative dividend of 3.5% to 4.5% per annum, SGD denominated

- Actively managed by professional and experienced fund managers

- Monthly dividend pay-out

Fees are set out below:

Notable points are

- No sales charge (zero upfront fee)

- Lock up for 2 years – 2% of redemption proceeds if redeemed within 2 years. No charge from third year onwards

Minimum subscription amount is $1,000 (if you apply online).

It’s quite a lot to digest, so let’s run through each of that in greater detail.

Why Allianz SGD Income Plus Fund II?

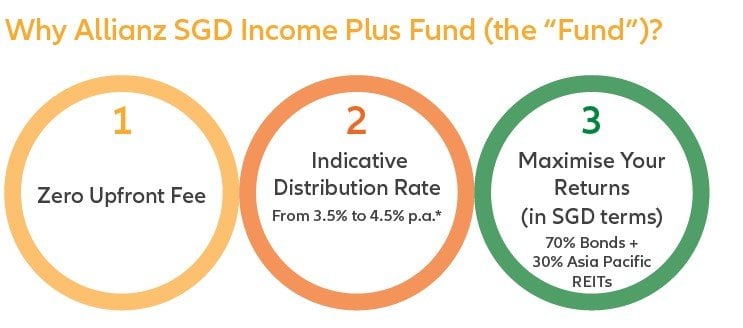

Asset Allocation of Allianz SGD Income Plus II

The fund is actively managed, and the broad asset allocation is 70% bonds, 30% REITs.

Bond Component (70%)

The Bond component is made up of approximately:

- 50% SGD denominated global bonds

- 50% Asian USD and other currency bonds

All non-SGD bonds are hedged back to SGD.

Based on the indicative model portfolio as of 28 September 2021, the top 5 holdings for the Bond component are:

- Agile Group (property developer)

- AIA Group (insurance)

- ARA Asset Management (property manager)

- Asahi Mutual Life (insurance)

- Aviva Singlife (insurance).

Note that this is indicative and may deviate depending on market conditions on inception.

Insurance and real estate seem to feature quite heavily in the bond segment.

The average yield of this 70% bond component is 4.0%.

As a retail investor, this is probably the main highlight because none of us can cost effectively assemble a bond portfolio that pays an average coupon of 4.0%.

You need to be an accredited investor subscribing for $250,000 minimum per bond.

REITs Component (30%)

To further juice up the yield, Allianz SGD Income Plus II will have a 30% allocation to REITs.

This is primarily Singapore REITs and should form approximately 20% of the overall portfolio.

Based on the indicative model portfolio as of 28 September 2021, the top 5 holdings for the REITs component are:

- AIMS APAC REIT

- Ascendas REIT

- CapitaLand Integrated Commercial Trust

- Frasers Centrepoint Trust

- Frasers Logistics & Commercial Trust

Average yield on this REIT segment is 5.23%.

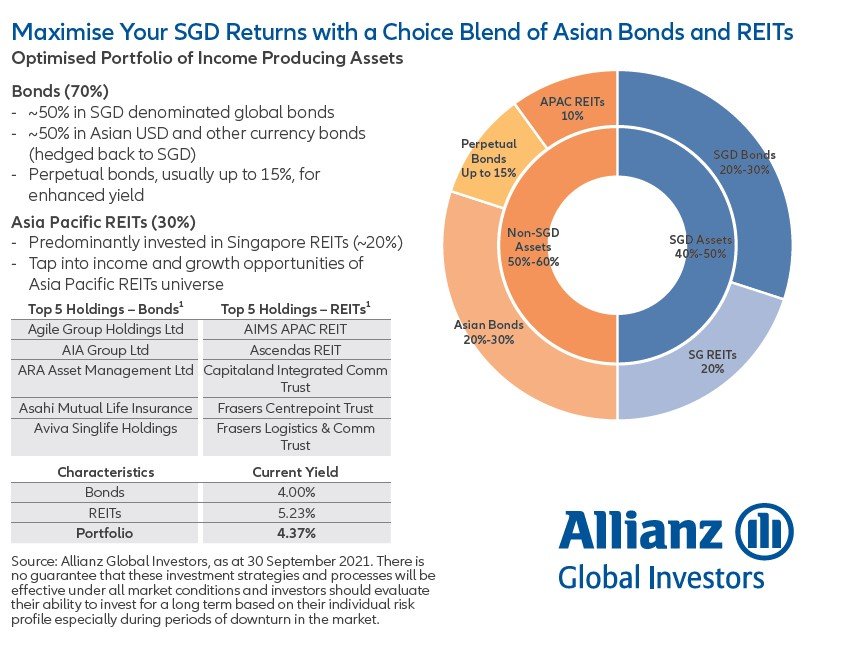

Dividend Yield of Allianz SGD Income Plus II – Monthly Dividend Pay-out

The current indicative blended yield on this portfolio is 4.32%.

This excludes capital gains, but is before fees (1% p.a.), so after you net off all those the forecast of 3.5% – 4.5% looks fair.

What’s interesting is that the fund will aim to pay a monthly dividend, forecast to be about 0.33333% per share (works out to 4% a year).

Of course, the actual amount paid out will depend on market conditions, but this monthly pay-out could be pretty useful for investors (e.g. retirees) who want the monthly income.

Actively Managed Fund

It’s important to note that Allianz SGD Income Plus II is an actively managed fund, and not a passive indexing strategy.

So we do need to take a look at the quality of the portfolio managers and their track record.

The key Portfolio Managers are a Mr Albert Tan, and a Mr Wayne Chew:

Allianz SGD Income Plus II will be managed by the Asian Fixed Income team headed by David Tan, CIO Fixed Income Asia Pacific, who has over 28 years of industry experience. The responsible portfolio managers of Allianz SGD Income Plus would be Wayne Chew, of the bond sleeve and Albert Tan for the REITs sleeve.

Their descriptions from the prospectus below:

NOT Capital Guaranteed

Now onto the million-dollar question – is this capital guaranteed? Is the 3.5% – 4.5% yield guaranteed?

The simple answer is no, the returns and capital are not guaranteed.

If you want risk free (or low risk), go with the Temasek Bonds with 1.8% yield.

A 10-year Singapore savings bond yields 1.71% now.

If you want yield above that you need to take on some risk – after all, there’s no free lunch in this world.

While Allianz SGD Income Plus II is actively managed, the returns are not guaranteed.

Update: A couple of you have reached out to ask if this is a low risk product comparable to the Temasek Bonds. To be very clear, the Temasek Bonds are best in class for that risk profile, and there is unlikely to be a superior product at that risk level.

A low risk product in this climate would be something like the SSB/Temasek Bonds with a sub 2% yield. A product like this Allianz SGD Income Plus II would be higher risk than the Temasek Bonds, where you accept to take on more risk in search for a higher yield.

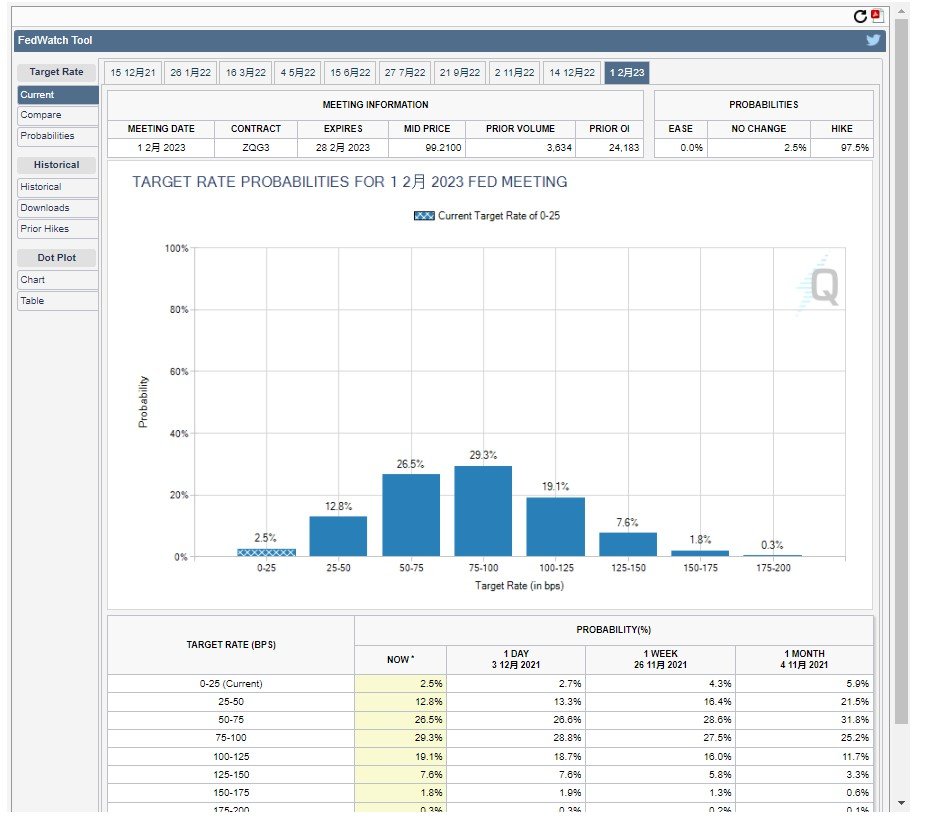

Rising interest rates a potential headwind

With a bond and REIT heavy portfolio like this, you do need to be cautious about interest rate increases.

The past few years had a powerful tailwind of interest rate decreases, but this new Allianz SGD Income Plus II is going to be facing rising interest rates over the next few years.

Market is forecasting an average of 3 rate hikes by early 2023, which could be a drag on performance.

Source: https://www.cmegroup.com/trading/interest-rates/countdown-to-fomc.html# as at 6 Dec 2021

If inflation is a big problem in 2022 and Jerome Powell hikes us into a market crash, this will definitely affect performance of this fund.

Fees

Fees are set out above.

Notable points are:

- No Sales charge

- Realisation charge of 2%, waived from third year onwards

- Minimum subscription amount is $1,000 (if you sign up online)

Take note of the realisation charge, which is a form of soft “lock-up”.

If you redeem your stake within 2 years of the subscription, you need to pay a realisation charge of 2% of the amount redeemed.

To illustrate – if you subscribe for $10,000, and you redeem in year 1, you pay a realisation charge of 2% which is $200, and you get back $9,800 plus whatever investment returns you made.

From year 3 onwards you can redeem anytime with no fees.

So it’s important to think about whether you would need to use the funds in the next 2 years before you go with Allianz SGD Income Plus II. Frankly a 2% withdrawal fee isn’t the end of the world if you have to pay it, but it’s still best to avoid it if you can.

What is my take on Allianz SGD Income Plus II?

The way I see it, the main advantage of Allianz SGD Income Plus II is the exposure to the investment grade bonds.

With the 70% bond component yielding 4.0% and of investment grade quality, this is not something you’ll be able to get exposure to yourself as a retail investor (you need to be an accredited investor investing $250,000 per lot).

The closest proxy would probably be to find an actively managed bond fund on Endowus, and then either DIY or buy a REIT ETF for the rest to juice the yield. But that’s a fair bit of work and hassle, and the actively managed bond fund on Endowus will carry its own set of fees as well.

For investors who:

(1) want monthly income,

(2) want yields higher than 2% but not too high risk, and

(3) don’t want to manage their own money

the Allianz SGD Income Plus II is a pretty good option.

You get pretty decent yields of 3.5% – 4.5%, a fund manager to look after your money, monthly dividends, and a medium risk profile.

Ultimately, it depends on your individual circumstances.

If you’re ok to take on more risk and volatility, and you don’t mind managing your own money, you could go with a 100% stock-REIT portfolio for a higher 5% – 6% yield, but with significantly more volatility.

It depends on your investing style and risk profile.

How to sign up for Allianz SGD Income Plus II?

The Initial Offer Period for the Allianz SGD Income Plus II is expected to be from 1 November 2021 to 14 January 2022 (both days inclusive).

Do note that:

- Subscription quota is limited and exclusively distributed by OCBC only

- The tranche will close once the quota is fully subscribed

Steps to sign up:

- For existing OCBC customers – simply click on this and it will prompt you to login before taking you directly to the Fund page within OCBC Digital App or Internet Banking to purchase these Allianz Income Plus fund units.

- For new OCBC customers – simply click on this (in desktop mode) and click on sign up for Online Banking. You will be able to open your OCBC account instantly and then proceed to purchase these Allianz Income Plus fund units.

|

Important Information This advertisement has not been reviewed by the Monetary Authority of Singapore. *The indicative distribution rate may not be achieved and is not an indication, forecast, or projection of the future performance of the Fund.

*Distribution payments of the Fund, where applicable, may at the sole discretion of the Manager, be made out of either income and/or net capital gains or capital of the Fund. As a result of the payment, the Fund’s net asset value is expected to be immediately reduced. The dividend yields and pay-outs are not guaranteed and might change depending on the market conditions or at the Manager’s discretion; past pay-out yields and payments do not represent future pay-out yields and payments. Past pay-out yields do not represent future pay-out yields and payments. Historical payments may comprise of distributable income or capital, or both (for further details, please refer to AllianzGI SG’s website).

|

||||||||||||||||||||||||||||

|

||||||||||||||||||||||||||||

|

|

||||||||||||||||||||||||||||

|

||||||||||||||||||||||||||||

|

|

Buying STI ETF will already be around 3% yield and with better capital upside.

May be better deal to go with STI ETF since for this SGD Income, its current 4.32% – 1% fee = 3.32% is similar and may not have so much upside due to its bonds.

But the risk profile is different though. STI is very heavy on financials and real estate. Whereas this is more of fixed income + REIT exposure.

what is the total expense ratio? i would assume 1% is probably jus the management fee?

I believe the 1% is all in.

So far nothing good besides off-loading to Premier clients.

Why need another own reit to buy other reits to pay half the returns but appreciate twice more than those that pay actual?

Any better plans for fixed income?

I think the main benefit for this plan is the Fixed Income exposure which is hard to replicate by yourself. And the REITs portion to juice the yield, for investors who dont want to manage their own money.

No frankly there are very few good options for fixed income today, thanks to the Fed and a decade of QE.

For investors who can stomach the risk and happy to manage their own money, I would think the better option is to just hold enough cash to tide through the volatility (or long vol/tail risk hedge for the more sophisticated investors), skip the fixed income portion (maybe CPF depending on personal circumstances), and put the rest into stocks/REITs/risk on.

If we take moneyowl wise income vs this fund, which will be better?

Moneyowl looks to mix in a lot more equities, so it should be a higher risk profile for potentially higher returns. Depends on how much risk you’re looking for.

I believe the Endowus Income Portfolios will be a better choice for most investors, since the payout is higher and has a greater fixed income weightage. What do you think FH?

Haven’t looked into Endowus Income yet, will see if I can do a review. 🙂