I received a really interesting question over Christmas (names and details amended for privacy reasons):

Dear FH,

Firstly, a Merry Christmas and Happy New Year to you and your family. Thank you for your wonderful posts and selfless sharing.

The question I have for you today is regarding ILPs or more specifically, AXA Wealth Treasure.

The 2 main selling points are as follows:

- 100% startup bonus.

- Access to accredited investors funds which was explained to me as funds with generally better performance.

https://markets.ft.com/data/funds/tearsheet/performance?s=LU0372178672:USD

https://markets.ft.com/data/funds/tearsheet/performance?s=LU0690374615:EUR

What is your view on such an investment plan? Seeing that the returns are quite substantial (>10%). I understand that there are annual management fees as well as fund sales charges which generally amount to 5%. But based off the portfolio that a certain AXA adviser shown me, the returns are still ~8%.

Compared to the funds which you suggested, there are few which shows capital appreciation and/or dividends which amounts to 8% or I might have probably missed it out.

…

I would like to add a few pointers.

- Compounded interest after effect of deductions for the 4% and 8% is definitely lower. We are looking at (for year30/40 and 4%/8%), 1.4/1.9 and 5.3/5.8% respectively. Although given the portfolio shown to me, the returns are still ~8% which I suppose could only be attributed to the higher returns which brings the net returns higher.

- Perhaps you can share with us your view on insurance and investment. Whether to keep one clear of the other and what plans and why are you on them if it’s not too private for you.

I have to confess, it took me quite a while to understand AXA Wealth Treasure. A lot of information was only located in the formal product summary rather than the easier to read fact sheet, and it was drafted in a legal manner with lots of definitions and cross referencing. Because of that, I can’t be absolutely certain that I didn’t miss anything out, so do note the disclaimer below:

The information contained in this article has not been independently verified. No representation or warranty expressed or implied is made as to, and no reliance should be placed on, the fairness, accuracy, completeness or correctness of the information or opinions contained in this article. Neither Financial Horse or any of its affiliates, advisers or representatives shall have any liability whatsoever (in negligence or otherwise) for any loss howsoever arising, whether directly or indirectly, from any use, reliance or distribution of this article or its contents or otherwise arising in connection with this presentation. Past performance is not indicative of future performance. If you are in doubt as to the action you should take, please contact your financial advisor, stock broker, or legal advisor.

Basics: AXA Wealth Treasure

Very simply, AXA Wealth Treasure is an insurance / investment product.

When you buy AXA Wealth Treasure, you get to pick:

- Your monthly premiums (ie. how much you want to contribute each month, subject to a minimum of S$300 a month) and

- Your premium payment term (ie. how long you want to contribute for, which can be anywhere from 5 to 30 years. After the term is up, you get to withdraw the money).

AXA takes the money and invests it in investment funds (basically Hedge Funds), and you get to pick the funds you want.

There’s a terminal illness insurance and health insurance component, so you’ll get a payout if you get a terminal illness or pass away (additional charge if you want a bigger payout).

At the end of your premium payment term, you get to withdraw the money. How much money is left will depend on how well the funds you chose have performed.

There are a few other interesting features:

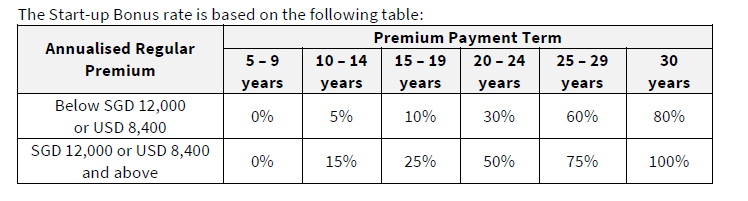

- Startup bonus – Depending on your premium payment term, AXA will give you a startup bonus. So for this reader who wanted the 30 year premium payment term, if he invested SGD12,000 or above a year, AXA would match 100% of his first year premium.

- Loyalty bonus – Starting from the 6th year of the plan, AXA also pays a loyalty bonus of 1% a year of the prevailing account value. So if you have S$60,000 after 5 years, they’ll give you S$600 for the 6th This money goes into your investment sum with AXA.

Please note that this summary is massively simplified. I only went through the most critical features here, so if you’re thinking of actually investing, do get your financial advisor to walk you through the terms and conditions. This product is serious stuff.

Fees

My main gripe with AXA Wealth Treasure, is very simply, the fees. There are a lot of fees. I’ve summarised the main ones below:

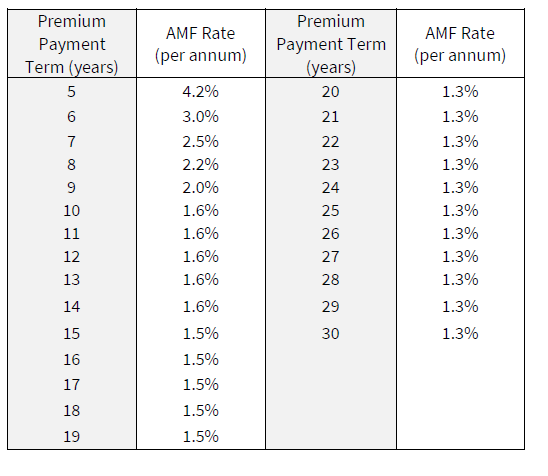

- Account Maintenance Fees – This is a fee that you pay AXA to maintain your account, which is set out in the table below. As you can see, if you pick a 5 year plan, the rate is an out of this world 4.2% per annum, which makes me think that you’re just not supposed to pick a 5 or 6 year plan. Anyway, the reader here wanted a 30 year plan, which would drop the fee to a 1.3% per annum.

- Investment Management Fees – There’s also a Monthly Investment Management Fee of 0.9% per annum.

- Fund Management Fee – There’s also a Fund Management Fee. This isn’t paid to AXA, but is paid to fund manager for the fund you chose. So for example if you pick the Amundi Fund that the reader was interested in, it has an expense ratio of 1.67% per annum, so you’ll pay the fund manager 1.67% per annum.

- Fund Sales Charges – This last charge depends on the funds that you pick. Some funds have a fund sales charge, which is basically a one-time fee you pay the fund, each time you want to invest new moneys with them. It typically ranges from 1% – 2%, and you’ll need to check with your financial advisor or the fund manager for the final number.

Just totalling that up, for a 30 year plan, you’re looking at about 3.87% in fees a year before Fund Sales Charges. With Fund Sales Charges, you could be looking at anywhere from 4% to 5% in fees.

You do get the startup bonus and loyalty bonus to lessen the pain (which probably work out to about 1+% a year worth of fees). After taking that into account, the net fees you pay, is probably around 3% to 4%.

I hate paying fees. The way I see it is this. Investment returns are inherently unpredictable. Nobody knows for certain what the stock market will return on a year to year basis. However, what is perfectly predictable, are fees. Regardless of how the stock market performs, you’re guaranteed to have to pay AXA and the Fund Manager a net total of about 3% to 4% a year, even if you lose money in the market that year.

Just to illustrate this dynamic. The long term return for stocks is about 7%, which is basically inflation plus economic growth. You can outperform his number in the short term, but over longer, multi decade periods, this is the number that almost all investors will trend towards unless you’re Warren Buffet. If you assume 7% returns a year, and invest S$1000 monthly, you’re left with $1,227,087 after 30 years. If you add on 4% fees on top of that, your returns drop to 3%, and you’re left with $584,193. That’s more than a halving of investment returns.

Lock-up

The other thing to note about AXA Wealth Treasure, is the lock up period. If you’re committing to a 30 year plan, your money is basically locked up for 30 years. If you want your money back earlier, you have to pay extra fees:

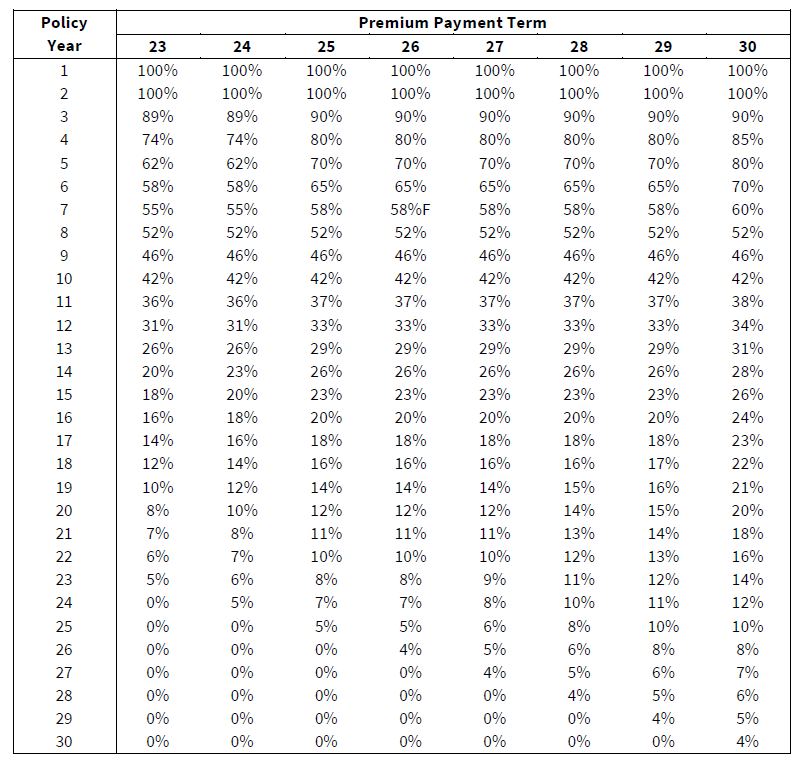

- Fees to terminate the plan early (Early Encashment Fee): If you want to terminate the plan early, the fee table are set out below. To take a simple example, if you sign up for a 30 plan, and you want to terminate the plan after 20 years (which is a heck of a long time in my book), you have to pay a fee of 20% of your account balance. Even if you terminate it at the final year, you’re still paying 4% of the account balance.

- Fee to withdraw a portion of money prematurely (Partial Withdrawal Charge) – If you wanted to withdraw the money but not terminate the plan (ie. you want to take money out, but you’re fine to continue contributing money every month), the fees are 5% from Year 6 to Year 25, and no charge from Year 26 onwards.

I don’t speak for anyone else on this, but the idea of locking up my money for 30 years, and having to pay a fee to access my own money, just blows my mind. I already have CPF-OA, CPF-SA, Medisave and SRS, which all have great lock-up periods, why would I want another way to lock up my money until my 60s?

Investment returns

At the end of the day, your contributions to AXA are passed on to a fund manager to invest on your behalf. Accordingly, your investment returns at the end of the 30 year period will depend on the performance of the funds you selected.

I’ve set out the returns for the 2 funds selected by the reader below, and benchmarked it against a simple S&P500 ETF. As you can see, the Amundi fund returned 14.10% annualised over 5 years, the Fundsmith one returned 17.88%, and the S&P500 returned 15.35% (do note these are GBP denominated numbers, which was all I could find).

Amundi SICAV II – Pioneer U.S. Fundamental Growth A USD ND

| Annual Returns (GBP) | 31/12/2018 | ||||||||||

| 2011* | 2012* | 2013 | 2014 | 2015 | 2016 | 2017 | 31/12 | ||||

| Price Return | 5.65 | 8.15 | 29.45 | 19.36 | 11.16 | 22.15 | 11.22 | 4.52 | |||

| +/- Category | 8.63 | -0.37 | -1.11 | 2.81 | 2.47 | -0.12 | -4.71 | 2.17 | |||

| +/- Category Index | 2.24 | -2.05 | -1.55 | -0.72 | -0.63 | -5.57 | -7.72 | -0.09 | |||

| % Rank in Category | 4 | 52 | 65 | 24 | 36 | 53 | 74 | 39 | |||

| Trailing Returns (GBP) | 17/01/2019 | ||||||||||

| Total Returns | +/- Category | +/- Category Index | |||||||||

| 1 Day | 0.49 | 0.54 | 0.07 | ||||||||

| 1 Week | 0.18 | -0.41 | -0.21 | ||||||||

| 1 Month | 0.47 | -0.39 | -1.76 | ||||||||

| 3 Months | -3.59 | 0.55 | 1.43 | ||||||||

| 6 Months | -2.57 | 2.65 | 2.76 | ||||||||

| YTD | 2.11 | -2.61 | -2.16 | ||||||||

| 1 Year | 3.62 | -0.99 | -1.96 | ||||||||

| 3 Years Annualised | 14.73 | -2.66 | -5.89 | ||||||||

| 5 Years Annualised | 14.10 | 0.44 | -3.12 | ||||||||

| 10 Years Annualised* | 16.22 | 1.23 | -1.65 | ||||||||

| Category: US Large-Cap Growth Equity | |||||||||||

| Category Index: Russell 1000 Growth TR USD | |||||||||||

Fundsmith Equity Feeder Class R EUR Acc

| Annual Returns (GBP) | 31/12/2018 | ||||||||||

| 2012 | 2013 | 2014 | 2015 | 2016 | 2017 | 31/12 | |||||

| Price Return | 10.51 | 24.71 | 22.18 | 15.53 | 26.11 | 21.80 | 1.53 | ||||

| +/- Category | 1.49 | 4.14 | 14.74 | 12.17 | 2.62 | 9.23 | 8.24 | ||||

| +/- Category Index | -0.23 | 0.39 | 10.72 | 10.66 | -2.13 | 9.99 | 4.57 | ||||

| % Rank in Category | 36 | 23 | 1 | 2 | 34 | 3 | 4 | ||||

| Trailing Returns (GBP) | 18/01/2019 | ||||||||||

| Total Returns | +/- Category | +/- Category Index | |||||||||

| 1 Day | 1.06 | 1.26 | 0.97 | ||||||||

| 1 Week | 0.72 | 1.14 | 0.82 | ||||||||

| 1 Month | 0.10 | 0.78 | -0.84 | ||||||||

| 3 Months | -1.20 | 2.05 | 2.23 | ||||||||

| 6 Months | -7.04 | -0.58 | -2.01 | ||||||||

| YTD | 2.97 | -0.28 | -0.55 | ||||||||

| 1 Year | 3.28 | 8.59 | 5.16 | ||||||||

| 3 Years Annualised | 18.94 | 6.68 | 3.78 | ||||||||

| 5 Years Annualised | 17.88 | 9.71 | 7.04 | ||||||||

| 10 Years Annualised | – | – | – | ||||||||

| Category: Global Large-Cap Blend Equity | |||||||||||

| Category Index: MSCI World NR USD | |||||||||||

| Annual Returns (GBP) | 31/12/2018 | ||||||||||

| 2011 | 2012 | 2013 | 2014 | 2015 | 2016 | 2017 | 31/12 | ||||

| Price Return | 2.65 | 10.90 | 29.85 | 20.52 | 7.12 | 33.60 | 11.16 | 1.38 | |||

| +/- Category | 3.18 | 0.98 | 0.79 | 2.66 | 2.46 | 1.95 | 1.15 | 1.82 | |||

| +/- Category Index | -0.23 | -0.01 | -0.08 | -0.24 | -0.14 | 0.05 | -0.12 | -0.18 | |||

| % Rank in Category | – | ||||||||||

| Trailing Returns (GBP) | 18/01/2019 | ||||||||||

| Total Returns | +/- Category | +/- Category Index | |||||||||

| 1 Day | 1.35 | 0.98 | 0.01 | ||||||||

| 1 Week | 2.22 | 1.81 | -0.01 | ||||||||

| 1 Month | 2.85 | 1.52 | 0.03 | ||||||||

| 3 Months | -1.76 | 2.09 | 0.01 | ||||||||

| 6 Months | -3.14 | 0.93 | -0.01 | ||||||||

| YTD | 5.21 | 1.40 | -0.01 | ||||||||

| 1 Year | 4.66 | 3.76 | -0.07 | ||||||||

| 3 Years Annualised | 18.53 | 1.92 | -0.13 | ||||||||

| 5 Years Annualised | 15.35 | 2.13 | -0.11 | ||||||||

| 10 Years Annualised | 16.02 | 1.27 | -0.12 | ||||||||

| Category: Large Blend | |||||||||||

| Category Index: S&P 500 TR USD | |||||||||||

So on face value, it looks like the Fundsmith fund did indeed outperform the index. But there are a couple of really crucial points you need to note:

1. Don’t be fooled by the 10 year performance – The past 10 years was an unbelievable bull run for global equities prices. An era of zero interest rates and record liquidity injection by central banks have inflated global asset prices, so the 10 year performance for just about every asset class looks ridiculous. Heck, if you gave a list of stocks to a monkey in January 2009 and let it pick, it would probably have delivered a decent return. If you’re expecting similar investment returns over the next 30 years, good luck.

2. How long can these Funds last? – Most of these funds have been around for less than 10 years. The Fund Management business is notoriously cutthroat, and in the next downturn, plenty of them will not survive. As we saw in December 2018 market turmoil, a lot of investors pulled money from active managers and redeployed them into passive ETFs. That’s a trend that I expect going forward. If you pick wrongly, you may just end up with a fund that closes after a few years, and you’ll need to pick a new one, and incur Fund Sales charges when making the switch. A 30 year timespan is a really long time, and it’s going to be hard to find one that will be around for 30 years.

3. How long can outperformance last? – The other problem with active management, is that funds that outperform for a few years, usually underperform the next few years, because long term performance tends to normalise towards the mean. And how do investors usually pick funds? By looking at historical performance. This places you in a funny situation where you’re more likely to pick a fund that did well in the past, and you buy into it just when it starts to underperform. There are some exceptions to this of course, there are the legends like Stan Drunkenmiller and Ray Dalio who are able to outperform consistently, but the challenge really is trying to find one of these guys. They don’t exactly grow on trees.

Don’t get me wrong, I’m not saying that active management is a bad thing. In fact there are some areas like fixed income and emerging markets where active management consistently outperforms passive investment because the markets are inefficient. The challenge though, is being able to pick the right fund manager. It’s a whole field in itself, with a ton of variables to consider (eg. will the fund manager leave, how good is his investment process, will he be able to outperform consistently, what markets are he invested in etc), and even I wouldn’t trust myself to be able to pick the right fund. A lot of these factors can only be determined by having a proper conversation with the fund manager to judge his personality and investment process, and when you’re investing anything less than S$10 million, you’re probably not going to have that opportunity.

Assuming you’re not able to find a Warren Buffet and you have to settle for a 7% annualised return over 30 years (that’s approximately the long term historical average), that return is about 3% to 4% after deducting fees, which is a heck of a lot less attractive.

If you do feel strongly in your fund manager picking prowess though, by all means go for it. You could well outperform us suckers who just invest in the S&P500 and STI ETFs ;).

Closing Thoughts – My thoughts on insurance and investing

Okay let’s recap. What AXA Wealth Treasure is, is an investment product that provides basic life and terminal insurance, at about a 3% – 4% annual fee. There is a lockup that effectively ties up your money for 30 years. The underlying performance is tied to the fund manager that you select, which is inherently uncertain.

I’m not going to issue any recommendations on AXA Wealth Treasure. Anyone being sold an AXA Wealth Treasure product will have a qualified financial advisor who is better placed to advise them based on their financial situation.

But what I will say, is that this is definitely not a product I personally would buy. There are 3 things I dislike in investing: (1) High Fees, (2) Liquidity (Inability to exit an investment), (3) Active Management for high fees. This product has all 3 of them.

How I handle insurance for myself is pretty straightforward. I have a health insurance plan, and a life insurance plan. And I have my investments. I would never mix the two, because mixing them creates a weird, complex hybrid product that makes it hard to evaluate each individually on their own merits.

When it comes to investments and insurance, simplicity is beauty. If you’re prepared to lock up your money for 30 years, you could really just take all that money and plonk it into the S&P500 on Dec 1 of every year. If you do it every year for the next 30 years, my bet is that you’ll probably outperform most hedge funds out there, net of fees.

Till next time, Financial Horse, signing out!

Financial Horse has a set of 7 Commandments for Successful Investing, that I ask myself before making every investment, and that I will never break regardless of the situation. Enter your email below to receive a copy!

[mc4wp_form id=”173″]

Enjoyed this article? Do consider supporting us and receiving additional exclusive content!

Like our Facebook Page for more great articles, or join the Facebook Group to continue the discussion!

The expression says it all LOL!

Learn the takeaway from Buffett’s 2008-2017 bet, and Bogle’s index fund. 😉

Hahah well said! Or rather… A picture speaks a thousand words!

There is a another product offered by AXA of similar nature namely AXA Wealth Pulsar. Any difference and comparison to the one you’d reviewed here (AXA Wealth Treasure)? Probably it would be good you do a similar review too to provide more awareness to the public. Thanks.

Sure, I’ll have a look. Cheers. 🙂

May I know what is the age of the writer and what similar product would you recommend then?

I would recommend just buying and holding a diversified equity portfolio. You can check out the all weather portfolio for a sample portfolio: https://financialhorse.com/all-weather-portfolio-for-singaporeans/

My fiancee just took up an ILP product called the AIA Pro Lifetime Protector Max. Any thoughts on it? I’m currently considerably afraid because of the negativity swirling about regarding ILPs and the poor long-term returns.

Okay I only took a quick look at the product so I may have missed some things. The broad structure of the products look similar, but the specific “features” vary (eg. things like the startup bonus, loyalty bonus etc are different for each product), but the general comments on high fees, investment returns etc, will continue to apply.

A lot would really depend on your financial situation, so it’s hard to advise in abstract. If you have a good financial advisor you trust, they would be better placed to advise for your specific personal situation.

my two cents: dun mix insurance with investments

you may get capital protection in case of death, but the money will come from somewhere, which is those ridiculously high fees.

for payouts in case of deaths, just get the pure vanilla term plans.

Agreed!

Any thoughts on the Tokio Marina Atlas Classic, which sounds pretty similar except that there is no penalty for early withdrawal of money so your money isn’t as locked-in as in this plan.

Hi there! I had a quick look at the brochure so I may not have caught everything, but the plan looks pretty similar to this. If you decide to terminate the plan early, there will be a termination fee. On top of that, the fees and fund fees are pretty high as well.

Cheers. 🙂

For someone whom has invested in this for about 3 months, do I terminate (getting a loss) or just hold it out for 30 years?

That can be tough to advise without knowing your financial circumstances and goals. I would suggest raising your concerns to your financial advisor, and they can walk you through them, as well as your options.

Cheers!

Etf like mutual funds all have fees. True that fund house fees can range around 1.5% and 0.75% for etf. But returns from fact sheets are after charges accounted for. So using your example of fundsmith which is currently performing at 19% annualised. What you are getting back from the fund say minus 2.2% from axa is still more than 15%. There are no charges for switching funds in awt currently.

Well, I guess the question is whether fundsmith can provide 19% returns going forward. If they can, then I agree this would be an absolutely amazing buy.