To be honest, I actually wasn’t planning to do a review on Eagle Hospitality Trust. But then I realised it was a long weekend, so I figured what the heck.

Anyway after going through the prospectus, it turns out that Eagle Hospitality Trust is similar to ARA US Hospitality Trust in many ways. So a lot of my comments in the review on ARA Us Hospitality Trust will hold true here as well, such as:

- Poor alignment of interests between sponsor and unitholders – Sponsor only holds a 15% stake post listing.

- No big institutional cornerstones – this IPO is mainly taken up by private wealth, which doesn’t exactly inspire confidence.

- Small cap REIT means that future growth will be funded via equity offerings – If you buy into this REIT, you should be prepared to cough up capital for future equity offerings, as is likely to be the main way they will fund growth going forward (insufficient debt headroom for large acquisitions).

There are a couple of points I wanted to touch on in greater detail here:

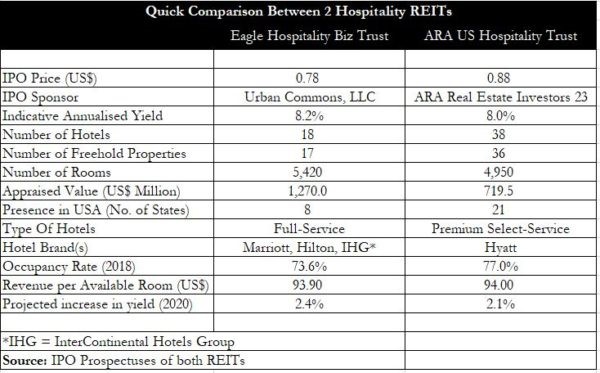

1. Assets – less diversified, more upscale, bigger asset size, lower occupancy and lower margins

Motley Fool has a pretty nice comparison between both REITs:

To sum it up, the difference between the two REITs is that Eagle Hospitality Trust is:

- Less diversified – Eagle Hospitality Trust only has 18 hotels across 8 states, while ARA US Hospitality Trust has 38 hotels across 21 states.

- More upscale – Eagle Hospitality Trust operates more upscale hotels as compared to ARA US Hospitality Trust which is more midscale. Eagle operates the Marriot, Hilton and IHG brands, while ARA operates the midscale Hyatt brands.

- Has a larger asset base – Eagle Hospitality Trust starts with an asset size of US$1.27 billion versus US$0.72 billion for ARA US Hospitality Trust

- Lower occupancy and lower margins – Eagle Hospitality Trust has a 73.6% occupancy and 39% gross operating margins, while ARA US Hospitality Trust has a 77.0% occupancy and a 50% margin. It’s hard to interpret this one conclusively, because while it seems that ARA US Hospitality Trust’s assets are more profitable, it could also mean that Eagle Hospitality Trust has more upside once they unlock the value of their assets. Then again this could be standard for the location and upscale nature of Eagle’s assets.

Ultimately though, it’s hard to pick between the two simply because I don’t have in-depth knowledge of the US hospitality industry. I’m just sitting here reading through the prospectus and having to take their word for it on how US hospitality will turn out in 2019, and how great the location of these assets are. It’s not like Ascott REIT where if they tell me how great Ascott Orchard is, I can just pop down to Orchard to check out whether this is indeed true, and I also have a pretty good idea of how Singapore’s tourism statistics and economic growth are like.

If you held a gun to my head and make me pick based on the numbers above, I’d probably go with Eagle Hospitality Trust, because I like that it has a larger asset base. Small cap REITs make me nervous, because the only way they grow is via a big dilutive equity fund raising, and Eagle Hospitality Trust is almost double the size of ARA US Hospitality Trust.

Note: A fellow blogger, Probutterfly has done some interesting research on the Queen Mary asset in Eagle Hospitality Trust. Do check out his take on it here, it’s well worth the read if you’re serious about this REIT.

2. Master Lease with Fixed Income

What I did like about Eagle Hospitality Trust though, is that its leases are structured as a master lease, with fixed rent accounting of about 66% of the rental income.

I didn’t like that ARA US Hospitality Trust is exposed to 100% variable rent, because I felt that the inherently cyclical nature of the hospitality industry would spell disaster for the REIT’s DPU when US hospitality inevitably suffers a down cycle.

With Eagle Hospitality Trust, the upside won’t be as big if US Hospitality does really well, but at least the yield should be more stable and predictable going forward.

3. Operational Data

Unlike ARA US Hospitality Trust, the operating statistics for Eagle Hospitality Trust do show a fairly decent uptrend from FY2016 to FY2018, which is pretty nice.

What is interesting though, is that both REITs are projecting a huge jump in revenues from FY2018 to FY2019. This leads me to 2 possible conclusions:

- They are right, and FY2019 is the year where US Hotels become great again – Perhaps we shouldn’t be so sceptical. Perhaps both REITs are right, and FY2019 is indeed the year that America becomes great again, where Americans travel in droves, and hotels experience a huge boost in revenue. Perhaps the year to date FY2019 data backs up this statement, which is why both REITs are so confident about their aggressive projections. If this is true, both REITs could actually a bargain at current prices, with a sustainable 8+% yield.

- They are both wrong, and FY2019 is not the year US Hotels become great again – Perhaps both REITs are similarly wrong about the direction of the US hospitality market in FY2019, and they fail to meet their aggressive forecasts. If so, I’ll be more comfortable holding Eagle Hospitality Trust become of the fixed component of their master lease. Then again, because DBS is the issue manager for both REITs, I find it hard to believe DBS would allow something like that to happen.

Personally though, I don’t see a need to make a bet either way just yet. The macro environment looks incredibly uncertain right now with the trade war set to escalate. And looking at how ARA US Hospitality Trust is trading since IPO (Spoiler Alert: It hasn’t been great), there also doesn’t seem to be a need to rush into this stock just yet.

I would probably give it a couple of months, let the trade war play out, let the post-IPO trading settle down, and wait for the first quarterly results from both REITs to see whether the actual operating performance is in line with the aggressive projections. If I like what I see then, I’ll open a position.

4. Valuations

| Yield | Price/NAV | |

| Keppel KBS US REIT | 8.0% | 0.955 |

| Manulife US REIT | 6.7% | 1.07 |

| Ascott Residence Trust | 5.92% | 0.861 |

| CDL Hospitality Trust | 5.75% | 1.05 |

| Eagle Hospitality Trust | 8.2% | 0.98 |

| ARA US Hospitality Trust (latest price of 0.865) | 8.14% | 1.00 |

I’ve also set out the valuation of Eagle Hospitality Trust above, benchmarked against the other US REITs.

It definitely seems that Eagle Hospitality Trust has used ARA US Hospitality Trust’s price action post listing as a benchmark for their pricing, which is not surprising given that DBS is the issue manager for both.

Anyway, Eagle Hospitality Trust is IPO-ing at an 8.2% forecast yield, and 0.98 times book value, which is highly similar to ARA US Hospitality Trust.

Just because it’s in line with ARA US Hospitality Trust though, doesn’t necessarily mean it’s a great buy. With a small cap REIT like this, with exposure to primarily US hospitality assets, and a high likelihood of big equity offerings going forward, I would probably want something in the range of a 9 – 10% yield, and a 10 – 15% discount to book before I consider picking it up.

Closing Thoughts: Eagle Hospitality Trust vs ARA US Hospitality Trust

Given that Eagle Hospitality Trust came so shortly after ARA US Hospitality Trust, I guess it was natural for investors to compare the two.

And there’s not much to pick between the two really, both are highly similar, small cap REITs with exposure to US hospitality, at book value and an 8.2% forecast yield.

Personally I like Eagle Hospitality Trust more because of the fact that 66% of its rent is fixed rent, which provides more stability going forward. I also like that it’s slightly bigger in market cap, and the operating statistics look more consistent.

Ultimately though, it suffer from many of the same problems as ARA US Hospitality Trust, being the lack of big cornerstones, poor alignment of interests between sponsor and unitholders, and the high likelihood of equity offerings to fund future acquisitions.

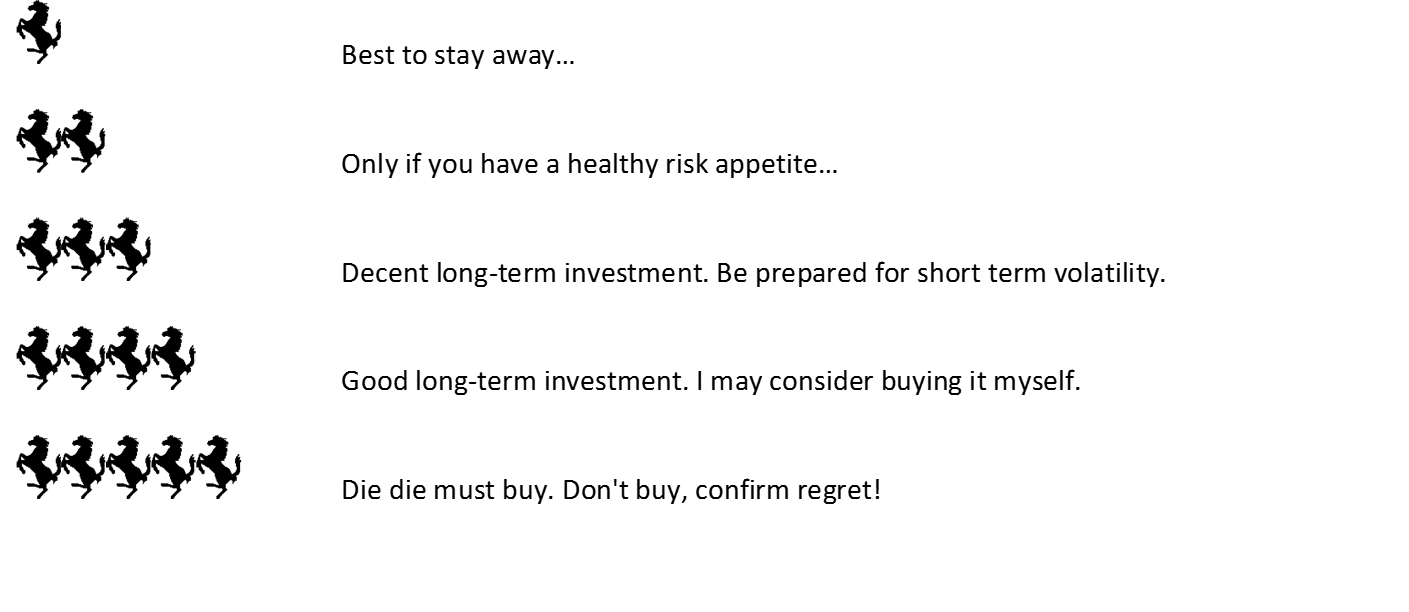

I’ll give Eagle Hospitality Trust a 2.5 Horse rating, compared with ARA US Hospitality Trust’s 2 Horse rating.

Share your thoughts in the comments section below! I respond personally to all comments!

Financial Horse Rating – Eagle Hospitality Trust

![]()

Financial Horse Rating Scale

Enjoyed this article? Do consider supporting the site as a Patron and receive exclusive content. Big shoutout to all Patrons for their generous support, and for helping to keep this site going!

Like our Facebook Page and join the Facebook Group to continue the discussion! Do also join our private Telegram Group for a friendly chat on any investing related!

Did you read about queen mary’s potential maintenance cost? This reit could go very wrong

Yep I saw them. But because this point didn’t feature heavily in the prospectus, it seems to me that it might not be as big an issue as it’s made out to be. Because if it really were, no lawyer / underwriting bank would want to sign off on the prospectus knowing this was a material point. Especially given that DBS was the issue manager.

[…] In a simplistic sense, we can view Eagle’s IPO from the lens of a typical REIT investor looking at Yields, P/B Ratio and Gearing. Our friends over at Financial Horse as a more detailed look at the numbers behind Eagle and I won’t repeat it here… […]

Very interesting comparison. I agree that Eagle has an edge over ARA. It seems EHT has more upside potential once income is stabilised in its properties and profit and occupancy go up. The slight ‘discount’ in pricing on the IPO is also enticing as is the resulting bump in yield. Comparing the two, EHT appears to have more creative potential, with options like the $250M ‘Queen Mary Island’ that may provide a potential future boost in revenue and value. According to the prospectus there’s a future acquisition potential for a large upscale property in NYC – the former Ritz Carlton. The pipeline looks to be more ambitious and diversified than ARA.

I think the bet is really on the future outlook of the US hospitality market. Do we think the US economy continues to grow, encourage more destination travel and hotel usage. Do corporate tax rate cuts implemented by their president drive more business travel and growth, leading to more hotel usage? And finally, does EHT trade at a large enough discount to comparable peers, that buying in the IPO is better than waiting it out, even if just a few bps difference?

It seems as far as yield goes, for exposure to the US market at a $1b+ valuation, the options are limited. EHT appears to be the most attractive option, currently. With yield so hard to obtain these days, the stability of RE assets seems to be appealing, US-based or not.

Great comment! Yes I agree with you on this. Ultimately though, it’s really about the US hospitality market as you mentioned. If the US economy holds up and the REITs meets its forecast distribution (or beats), this could be a pretty interesting counter.

Hi FH, what is your take on the post-IPO closing price of .73? Looking at the strengths of the REIT, particularly the 66% fixed income and long master leases, .73 seems like quite an attractive valuation, return and P/NAV wise. Worth dipping your hooves into?

Hi! I just wrote an article on this earlier, you can check out my thoughts there. Hope it helps!

https://financialhorse.com/eagle-hospitality-trust-balloting-results/

[…] Interestingly enough, the general consensus among Singapore finance bloggers for Eagle Hospitality Trust was overwhelmingly poor. Just about every one said they didn’t like it or would be skipping it (my own take here). […]