The big news that came out this past week was Frasers Logistics and Industrial Trust (FLT) acquiring Frasers Commercial Trust (FCOT).

It’s the third big REIT merger in recent years (after Viva Industrial Trust and Ascendas Hospitality Trust), so I figured it was time to take a closer look at REIT mergers.

Basics: Merger of Frasers Commercial Trust and Frasers Logistics and Industrial Trust

The acquisition has been covered by other sites such as Seedly and Investment Moats, so I won’t cover it in too much detail.

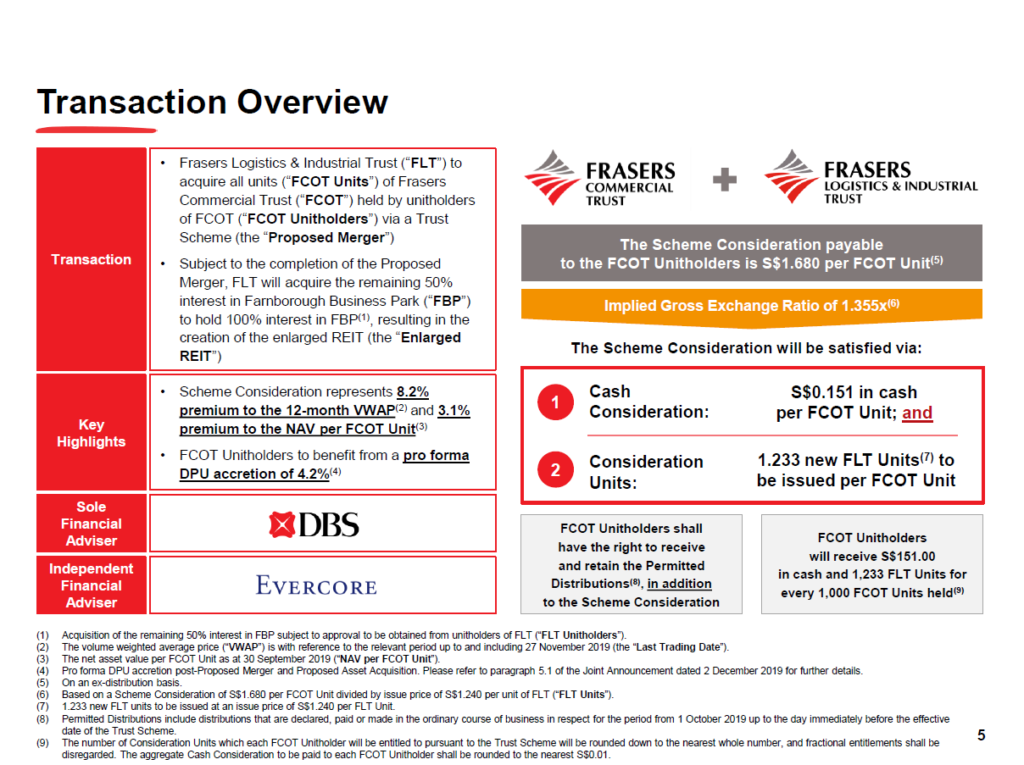

Basically, Frasers Logistics and Industrial Trust is acquiring all the units in Frasers Commercial Trust. The acquisition will be $0.151 in cash and 1.233 FLT units per FCOT unit. In plain English, for every 1000 FCOT units you hold, you get $151 in cash, and 1233 FLT units.

Frasers Logistics and Industrial Trust is an Australian and European Logistics/Industrial Trust with around $3 billion market cap, while Frasers Commercial Trust is a Singapore Industrial Trust, so the merger creates a Singapore/Australia/Europe logistics / industrial trust.

Why are Frasers Commercial Trust and Frasers Logistics and Industrial Trust merging?

Officially, there are a number of reasons listed for this acquisition, as set out below.

A quick note on Diversification

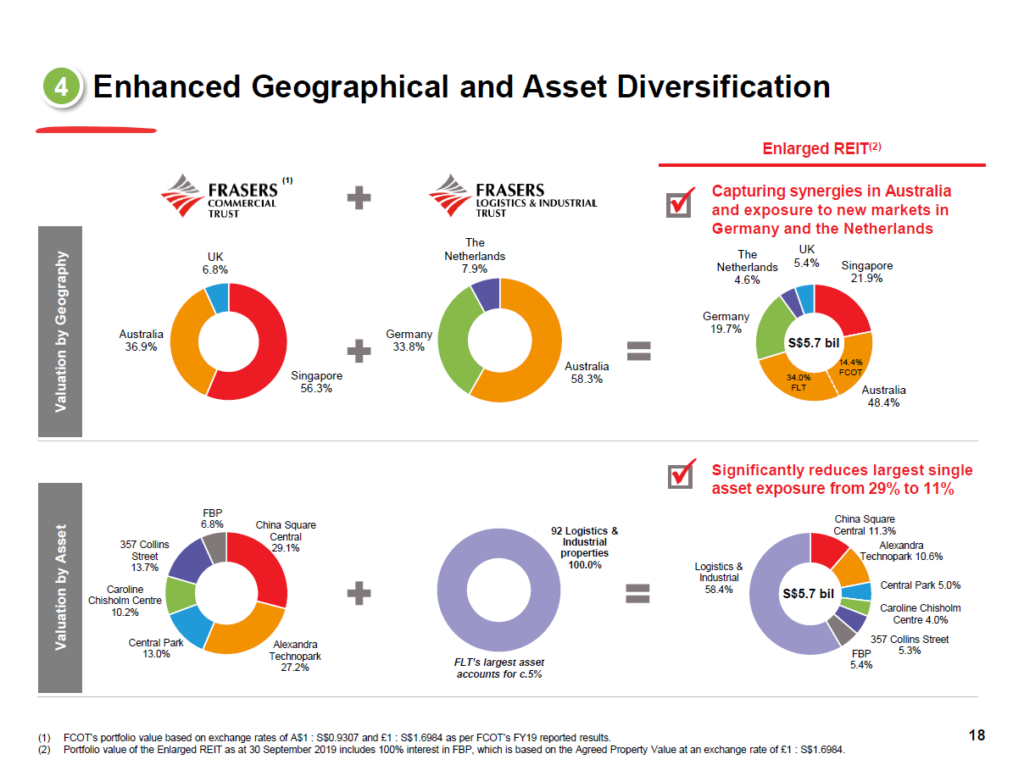

I noticed a number of other bloggers talking about how they love this transaction because of its diversification impact. I didn’t quite agree with that reasoning, so I just wanted to unpack it here quickly.

The argument from the other bloggers, is that before the merger, FCOT was mainly Singapore-Australia focussed, while FLT was mainly Australia-Europe. There was concentration risk for FCOT. Post merger, the combined REIT is far more diversified across properties and geographies.

Now I don’t deny that this is a feature of the current transaction, but I definitely don’t think this is the main rationale or advantage as other bloggers are alleging.

Don’t forget that as investors, the world is our oyster. There is technically no limit to the number of investments that we can buy to put into our portfolio.

Before this, if I wanted exposure to both Europe and Singapore / Australia, I could just buy both FCOT and FLT and be done with it. The current merger does nothing for me from a diversification perspective.

But before this, if I wanted to overweight Singapore exposure, I could buy more of FCOT. If I wanted more Australia I could buy more FLT. Post merger though, my only choice here is whether to buy the combined REIT, or to buy another REIT.

So from an investor point of view, diversification of the REIT is actually not a plus point, simply because I can achieve diversification on my own through proper portfolio construction (ie. buying other REITs).

Size is everything

So why are the two REITs combining, if it’s not for diversification purposes? Now no one knows for certain, but the way I see it, it all boils down to size.

Remember that saying about how size isn’t everything, it’s about how you use it (the REIT I mean..)? Yeah well, that was so 2005. These days, size really is everything.

Let’s jump back 15 years to 2004, around the time when the first Singapore REIT was IPO-ed (CapitaLand Mall Trust). It IPO-ed with one or two assets, Plaza Sing and another one that I can’t remember now.

Boy, those were the good old days for REITs. It was like the wild west back then. REITs were completely new to the Singapore market, there was little regulation or market practice to govern how things were done, and investors were all a bit green to this strange new structure called REIT.

How things have changed since. The 2 big events, were the Great Financial Crisis in 2008 (GFC), and the post GFC period. Okay so technically it was just the GFC.

The GFC was big in 2 ways:

1. Refinancing Risk – It was a huge wake up call to REITs on refinancing risk. It’s obvious now with the benefit of hindsight, but back in 2006 to 2007, real estate was on fire. Blue Chip REITs were trading at around 2 to 3% yields because investors viewed them as growth stocks, simply because real estate prices were going through the roof. Refinancing was not a problem at all. REITs could buy a property, then go out and arrange a financing package, without having to worry about being unable to finance.

And then Lehman hit. Nobody in real estate could get financing anymore. It was a huge shock to the system, and eventually resulted in the bankruptcy/takeover of some smaller REITs (Macarthur Cook Industrial REIT).

I don’t think the industry ever recovered from 2008. Sure, the scars have healed, but the memory is still fresh. These days, refinancing risk is big on the mind of all REITs, including all financing banks. Real estate financing is not as easy as it used to be pre-GFC. It’s definitely changing slowly the further we get from 2008, but there’s probably still some way to go before mindsets change completely.

2. Real Estate valuations have gone up – After Lehman, the Federal Reserve dropped interest rates to zero, and they injected over 4 trillion USD into the economy to prop up financial assets.

Interest rates are interesting. When rates go from 10% to 5%, companies around the world take up debt to finance capital investments to increase production. This is good.

But when rates go from say 5% to 0%, something seems to snap in the risk-taking behaviour. Because when rates are at 0%, the best thing to do no longer seems to be to invest in increasing production, it seems to be simply to invest.

The way I like to see it is this. Imagine I am a farmer planting sugarcane. When interest rates drop from 10% to 5%, boy am I going to take up a big loan to buy a bigger tractor and hire more farmers to grow sugarcane for me. But when interest rates go from 5% to 0%, am I still going to buy that tractor? No way sir, when interest rates are at 0% what I’m going to do is to take that money and buy my neighbour’s plot of land. Or if I’m a listed company, I’m going to buyback my own stock.

Obviously I have simplified the analogy a fair bit, but the key point here is that fixing interest rates at zero destroys the risk taking mentality. I don’t exactly know why, but I have a theory that it’s related to how 0% interest rates remove the whole concept of time value of money, which is central to all of corporate finance.

But that’s beyond the scope of this article. What is important for current purposes, is that most people took all that 0% interest rate money, and used it to invest in real estate around the world. So real estate prices soared through the roof. And 10 years after Lehman Brothers, we’re sitting on an epic real estate boom where high quality properties are now trading at 2 to 3% capitalisation rates.

So how does this tie back to Frasers Logistics and Industrial Trust buying Frasers Commercial Trust? The main problem is the inability to grow.

Imagine you’re a $1 billion market cap REIT. How do you grow from there? New properties are expensive, so to buy a new and good quality one it’s probably going to cost $500 million. That’s almost half your existing market cap. The maximum gearing is 45%, but nobody uses the max due to refinancing risk, so realistically you’re looking at around 40% gearing. This means the rest of around 30% of your market cap is pure equity financing. In this market, that’s going to be huge risk there.

Now imagine you’re a $10 billion market cap REIT. The same $500 million property is now 5% of your market cap. You can play around with your gearing a bit and do a small equity financing (small as a proportion of your market cap) to finance the deal. And because you’re bigger, you’re perceived as having lower credit risk, so banks are more eager to work with you.

By being bigger, you also get index inclusion, which boosts your trading valuation and liquidity, making it even easier to do further equity fundraisings down the road.

I do think there are some other minor reasons in play here, but by far the biggest one for me, is size. This biggest advantage behind this acquisition is creating a bigger REIT.

Implications for Singapore REITs

Don’t forget that this is the third REIT merger in recent years. The first to kickstart it all was Viva Industrial Trust (acquired by ESR REIT – the former Cambridge Industrial), and this was followed by Ascendas Hospitality Trust (acquired by Ascott REIT after CapitaLand’s acquisition of Ascendas).

There’s definitely a trend towards consolidation in REITs here, and I don’t see it stopping anytime soon.

The current market that we’re in will favour the bigger REITs, and that’s just an unfortunate consequence of this post GFC world.

1 + 1 = 3?

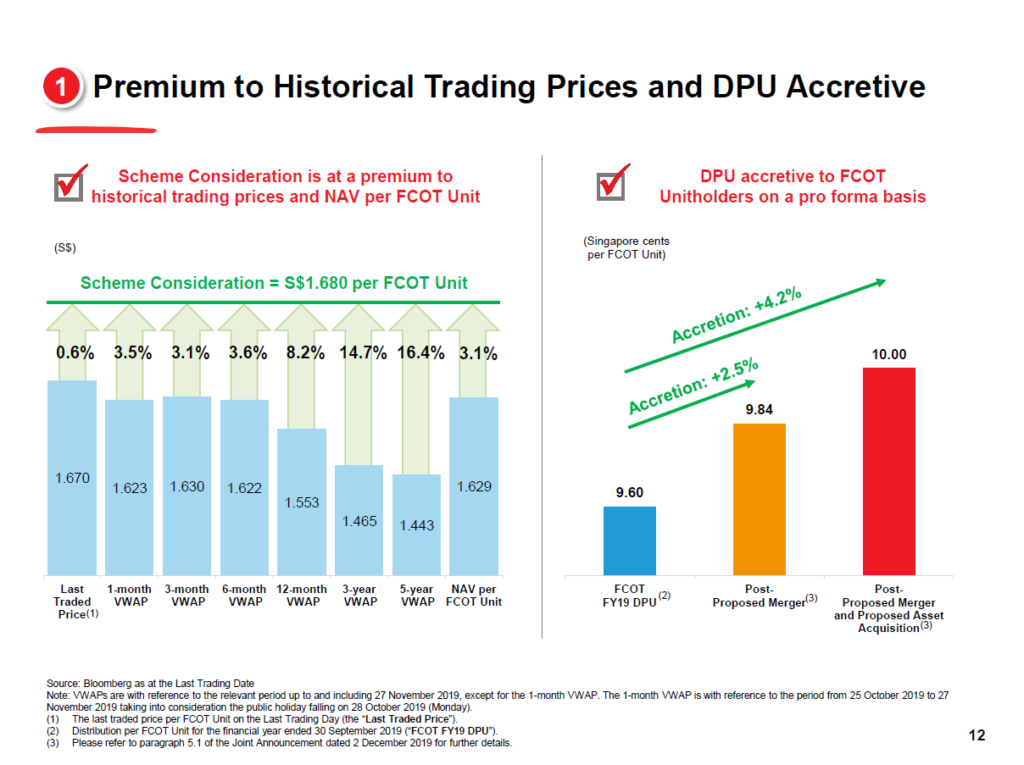

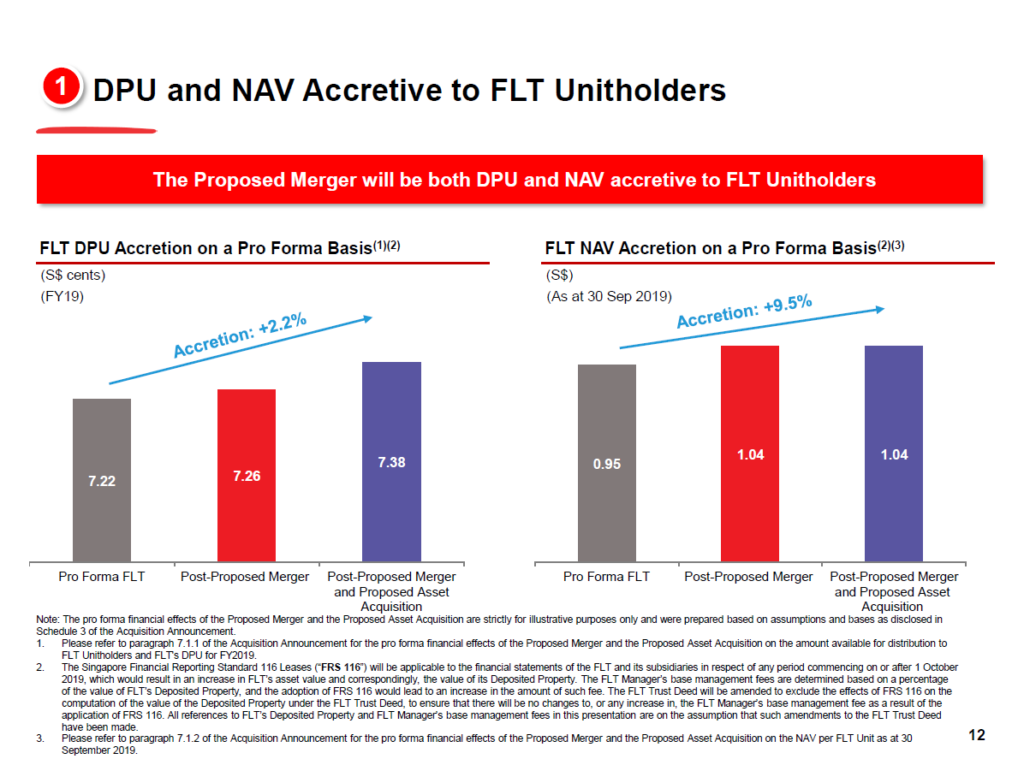

One other quick point that I wanted to talk about. When I first looked at the charts below, it looked as if the acquisition was hugely DPU accretive to both Frasers Commercial Trust and Frasers Logistics and Industrial Trust.

Now that can’t be right, because this is a 1 + 1 transaction. Simply putting two apples together does not create 3 apples, so it doesn’t make sense that the transaction should be DPU accretive to such a big extent.

As it turns out, FLT is in the midst of an asset acquisition that is DPU accretive, so a fair big of the DPU accretion comes from the acquisition, and not the REIT merger. To be fair it’s quite clearly disclosed in the announcement, I just missed it the first time around.

Long story short, the transaction is DPU accretive, but only by a small amount.

Closing Thoughts: Do I like this acquisition as a FCOT unitholder?

Member of my family hold units in Frasers Commercial Trust, so technically I am vested in Frasers Commercial Trust. And as a Frasers Commercial Trust unitholder, I am not a fan of this deal.

A huge part of the original thinking behind the acquisition of FCOT was for the Singapore exposure, and now it’s going to be diluted by the merger with FLT.

FCOT’s units are also being bought out at 1.68, which is 1.03 times book value and 5.7% yield, while I’m getting FLT units at 1.24, which is 1.28 times book value and 5.7% yield. I know it’s not a good comparison because of how differences in geographies affects valuations, but I can’t help but think I would still prefer to keep the old FCOT units and just enjoy a distribution every year. Either that or a bigger premium for the FCOT units would be nice.

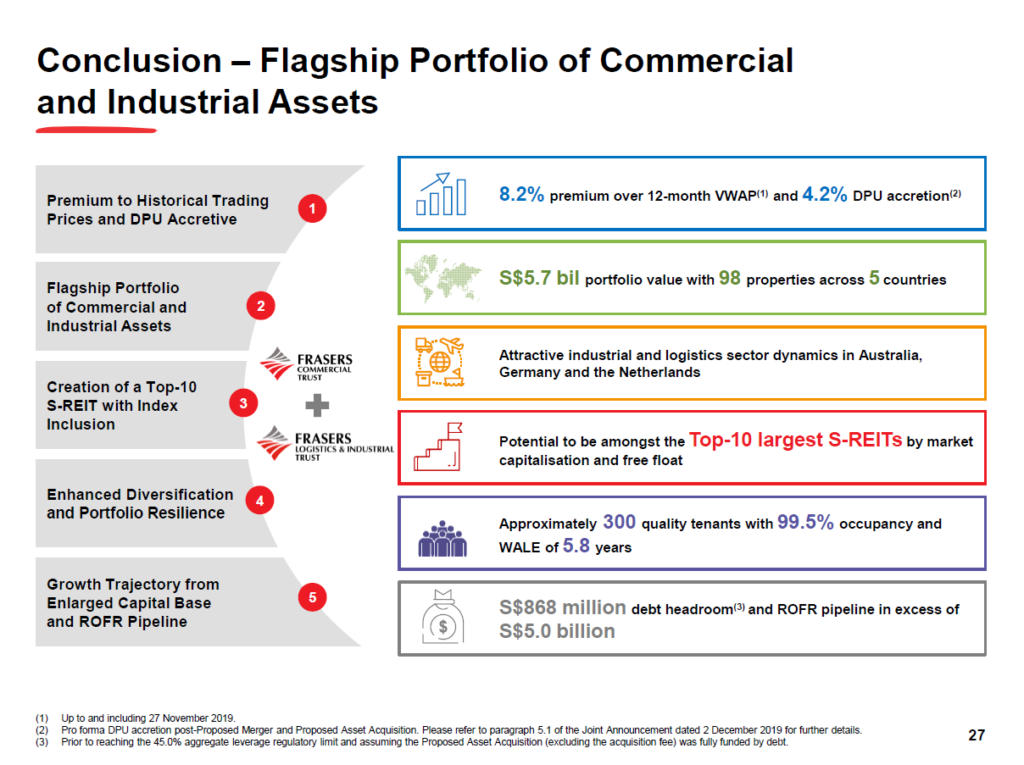

That said, I don’t deny that this acquisition is a good one for the REIT, and is in some ways, a must-do. The REIT industry is rapidly consolidating, and smaller REITs are going to get left behind. With a 1.5 billion market cap, FCOT would have faced such issues down the road (and is already facing them now), so in the bigger scheme of things, it is probably good for both Frasers Logistics and Industrial Trust, and Frasers Commercial Trust.

What do you guys think about this merger? Share your comments below!

Looking for a comprehensive guide to investing? Check out the FH Complete Guide to Investing for Singapore investors.

Support the site as a Patron and get market and stock watch updates. Big shoutout to all Patrons for their support!

Like the Financial Horse Facebook Page and join the Facebook Group (Singapore Stocks) or Facebook Group (China/HK Stocks) to continue the discussion!

I hold units in FCOT for 10 years now, bought when the price was on either side of $0.80. I also have units in FLT mainly from the IPO. Since buying FCOT the A$ had declined quite dramatically vs the S$, so its ability to increase its dpu over the years was to me rather impressive. However, in the last 2 years, the dpu had stagnated. And, after a few rounds of ‘capital recycling’ its portfolio of properties had not seen any growth, which led me to believe that it is difficult to find commercial properties at prices that can enhance its distribution payouts to maintain its historical yields. I had thought that some Thai properties might be injected into FCOT but that seems unlikely to happen.

The offer price at 1.03 to book value is certainly too low. Even if we add in the dpu for the next 2 quarters to Mar ‘20 and for part of the following quarter until completion the total offer price is still only ~1.10 to book value. I believe the timing of the offer is disadvantageous to FCOT as the A$ is at or near its lowest vs S$ having depreciated by ~15% over the last 5 years. So apart from valuing the offeror FLT at a much higher P:B, FLT may benefit substantially by a recovery in the A$ exchange rate down the road. Of course, we can’t be sure if that will/can happen if the current topsy turvy state the world is in continues!

That’s a really good comment. Unlike some of the other REIT mergers where it was quite neutral (Ascott REIT and Ascendas Hospitality for eg), I think this merger on the other hand may favour FLT slightly rather than FCOT holders. So FCOT holders like myself (and yourself, thanks for the sharing 🙂 are naturally less enthused about this deal.

Great comment though! Absolutely agreed on this.

Hello,

Would like to ask why is a sudden increase of REIT mergers these days? What is your take for the latest merger involving Capitalland?

The way I see it, it reflects a maturing in the REIT industry. If you trace the development cycle of the US REIT industry (which is far deeper and more sophisticated), they also went through a similar phase as well. I don’t see it as being good or bad necessarily, just a natural evolution of the REIT industry. We will definitely see many more of these down the road.

That’s interesting. If that’s the case, is it possible that you would give a detailed/analysis(article) of performing US REIT in the near future?

Sure, I’ll look into it. 🙂

Are you a Patron/Course member? I might release the article via there instead.