After last week’s article on how to get $6000 a month in passive dividend income.

It turned out the option that attracted the most discussion was Option 3 – Buying a portfolio of REITs and dividend stocks.

Or to be more specific, the buying of REITs attracted a lot of discussion.

What are Singapore investors saying about REITs?

Here’s a sample of the discussion in the FH Telegram Group:

A: You mentioned seeing 40% capital loss in a true market sell off. My portfolio of “bluechip” REITs (MLT, MPACT, Ascendas, MIT, Keppel, Capland China, FLCT) is down pretty significantly compared to past 5 years prices. Do u think it’s considered a large enough market sell-off situation that we are in already?

B: I have been DCA for 6 months now, to get into the 6% dividend yield range. Out of ammo now. my average price now for MLT is 1.42, MPACT 1.25, MIT 2.19, Ascendas REIT 2.59. Keppel REIT 0.88, FLCT 1.04, CapitaLand China REIT is the worst. Down 20+% and my average now is 0.84. Trying to get rid of Suntec REIT which is a useless REIT. Im stuck at 1.16 for that

C: Jia you bro. Ya REITs is a very long term strategy to use dividends to cushion any capital loss.

D: In your list, I have MLT, MPACT, Ascendas and FLCT. Average price is around same as you except MLT only because i started to buy MLT only recently… Hang on together my friend

The discussion above seems to be trying to average down and hope for REIT prices to turn around.

But if indeed this decade is going to be one of higher interest rates, will we truly see a turnaround in REIT prices?

Are REITs still a good investment today?

Here’s another comment that I received:

To me REITs as a class is not very attractive as long as the interest rates is going to be higher for longer. Essentially they need to give out 90% of their income as dividends in order to give shareholders a 5 to 7% yield. Monitoring their gearing, you can already see that even blue chips like CICT has a gearing of 40% or more. Interest rates risk is going to affect the DPU and that is why you see this risk priced into the REITS price now. On the other hand banks, even at their high valuation now can give you a 5 to 6% yield with just 50% payouts and retain a solid low risk balance sheet.

Do we expect interest rates to go low as it was before? Honestly I don’t really have much faith in how things are progressing on the macro front. With the wars and supply chain restructuring, energy inputs will get higher and supply chain lengthening. Inflation seems to be entrenched for the moment. REITs as a class may never be the same as before when we had it good for the last 10 to 20 years of QE. Remember that low interest rates were never the default scenario before we were spoilt on the golden years of QE. Having said that, there are risks on the horizon that the FEDs cannot engineer a soft landing or a trigger event that sends the US into a recession (like CRE imploding or sudden outbreak of escalatory war, or the US finally reaching the cliff edge of their USD34Trillion debt). Sorry to paint such a dark future. Depending on the scenario, it might be the best opportunity to deploy more cash or the worst risk you can ever take. One must weigh these carefully when the time comes.

STI ETF is not attractive to me. You can see the STI performance and it should be obvious that the returns is poor compared to an S&P index fund (find a Irish domiciled one).

My own option is the buy all three SG banks progressively and keep some monies in a T bill ladder that you can deploy progressively in case there is an opportunity. Always keep some cash for emergencies. Equities will always be a risk but it is still my preferred option with a mix of T bills.

Frankly – the above is a really good comment that sums up most of the current concerns about REITs, and why most investors are choosing to buy banks (and park the rest in T-Bills) instead of REITs.

Personally I find the truth lies somewhere in between, so I wanted to share some views in this article.

I’ll split the article into 3 parts:

- Why are REIT prices falling?

- What is the outlook for REITs?

- How I may invest $100,000 in REITs in 2024?

Why are REIT prices falling?

The way I see it, it comes down to 2 reasons.

Higher Interest Rates

The first of course, is a no brainer.

Higher interest rates.

REITs are very sensitive to interest rates because:

- They are highly leveraged – higher rates means higher interest expenses

- Real estate prices are very sensitive to interest rates – higher rates means higher cap rates

- Market views them as “yield” plays – so if rates go up market demands a higher yield, which means lower REIT prices

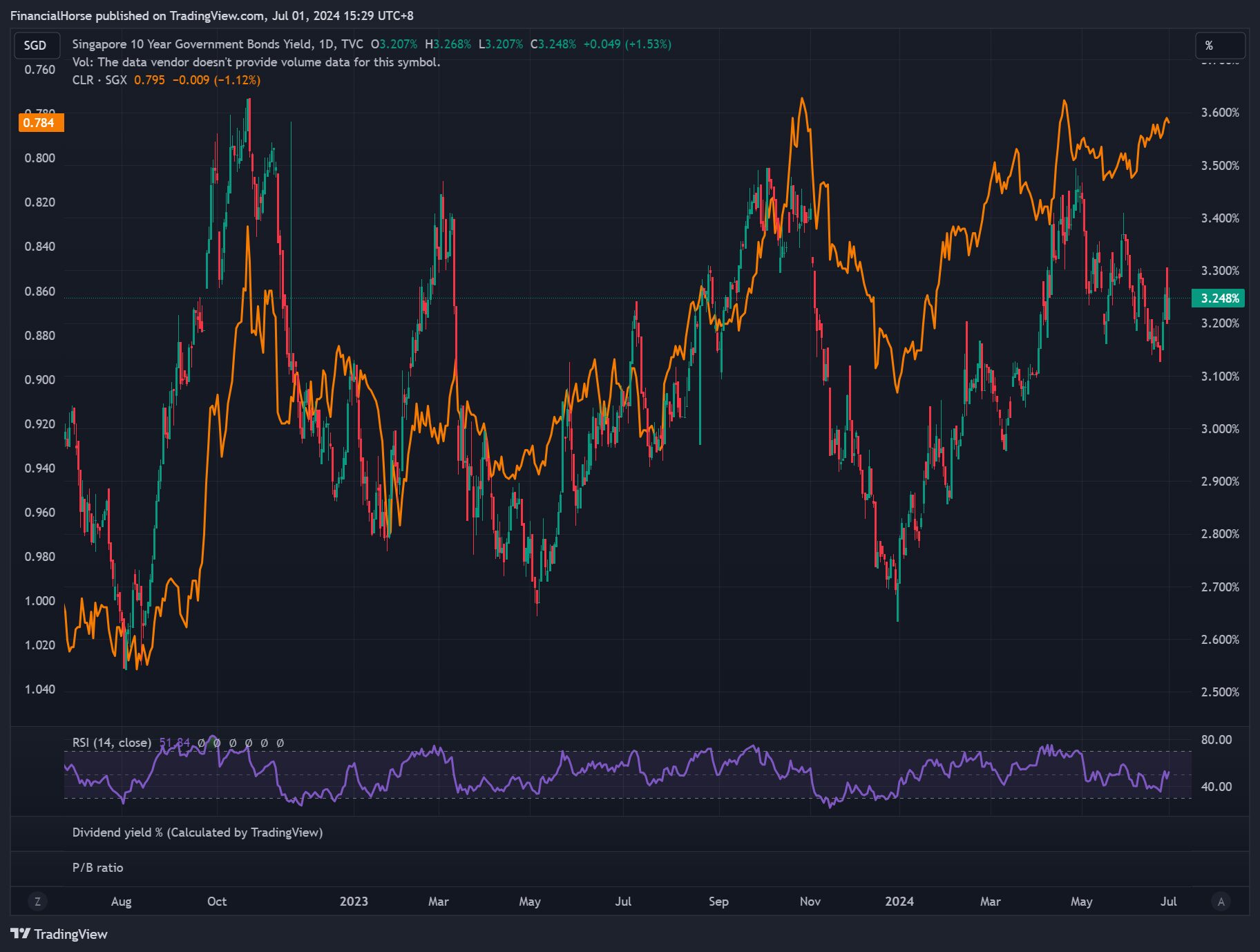

You can see below the Singapore 10 year government bond yield plotted against a REIT ETF (inversed).

For much of the past 18 months – when interest rates go up REIT prices drop.

So higher interest rates generally explains why the pure Singapore REITs like CapitaLand Ascendas REIT are not doing well.

Foreign real estate is not doing well (especially China)

For REITs that are holding primarily foreign real estate however.

There is a second reason.

Around the world, Singapore commercial real estate prices have actually been holding up pretty well.

Foreign real estate is doing many times worse – the biggest losers being China/Hong Kong real estate (due to China real estate crisis), and US offices (due to work from home trend).

Here’s Hang Lung, one of the largest HK listed blue chip property developers, with good quality properties in China and Hong Kong.

Share price is back at levels last hit in 2003 – unbelievable stuff.

Why is China real estate doing so poorly?

I’ve discussed this extensively for FH Premium subscribers.

Long story short is that China real estate is going through a painful deleveraging process, and all signs from Beijing are that this is unlikely to end any time soon.

They will step in to prevent systemic risk, but they are not going to step in to reinflate the real estate bubble.

Because of that, this overhang will hang over China real estate for a while.

And it’s why you see REITs like Mapletree Logistics Trust (with a lot of China exposure) performing poorly.

But frankly it’s not just China real estate though.

Here’s Frasers Logistics & Commercial Trust, another investor favourite with 50% AUM in Australian real estate.

Share price has retraced all the way to IPO price!

Global real estate has not been doing well of late, and actually Singapore commercial estate has been a bright spot.

What is the outlook for REITs? Are REITs still a good investment?

From a macro perspective, much will depend on the interest rate outlook for REITs going forward.

I could go on and on about the outlook for interest rates.

But let me cut to the chase here.

I agree with the commenter above that this is a fundamentally different paradigm for REITs vs the past decade.

When interest rates were at zero and the Feds had your back – it really didn’t matter what REIT you bought.

In a climate of zero interest rates, every single REIT will do well.

But that’s not the environment we are living in today.

This decade is likely to be one of higher interest rates (with a lot of volatility in between)

If Trump wins (and that’s the highest probability event priced in today).

He’s going to cut a lot of taxes, spend a lot of government money, and erect a lot of trade barriers.

That’s going to be inflationary, and who knows what happens to interest rates next.

If the Democrats win (with whoever they are going to field), I frankly don’t see them reducing the fiscal deficit one bit.

Look at what’s going on in France / UK, and it’s fairly clear that whoever wins the elections there is not going to be spending less money.

So this higher government spending is now a global phenomena.

This places big constraints on the Fed’s ability to cut interest rates.

Yes maybe we get a cut or two, but like the commenter said – does it get slashed back to zero?

BTW – we share commentary on Singapore Investments every week, so do join our Telegram Channel (or Telegram Group), Facebook and Instagram to stay up to date!

I also share thoughts on Twitter regularly.

Don’t forget to sign up for our free weekly newsletter too – with weekly roundups every Sunday!

What if we get a recession? With interest rate cuts?

Frankly we’re at the point where a mild recession could be the best thing to happen for REITs.

If you look at the economic data – it’s fairly clear that US economic growth has been slowing of late.

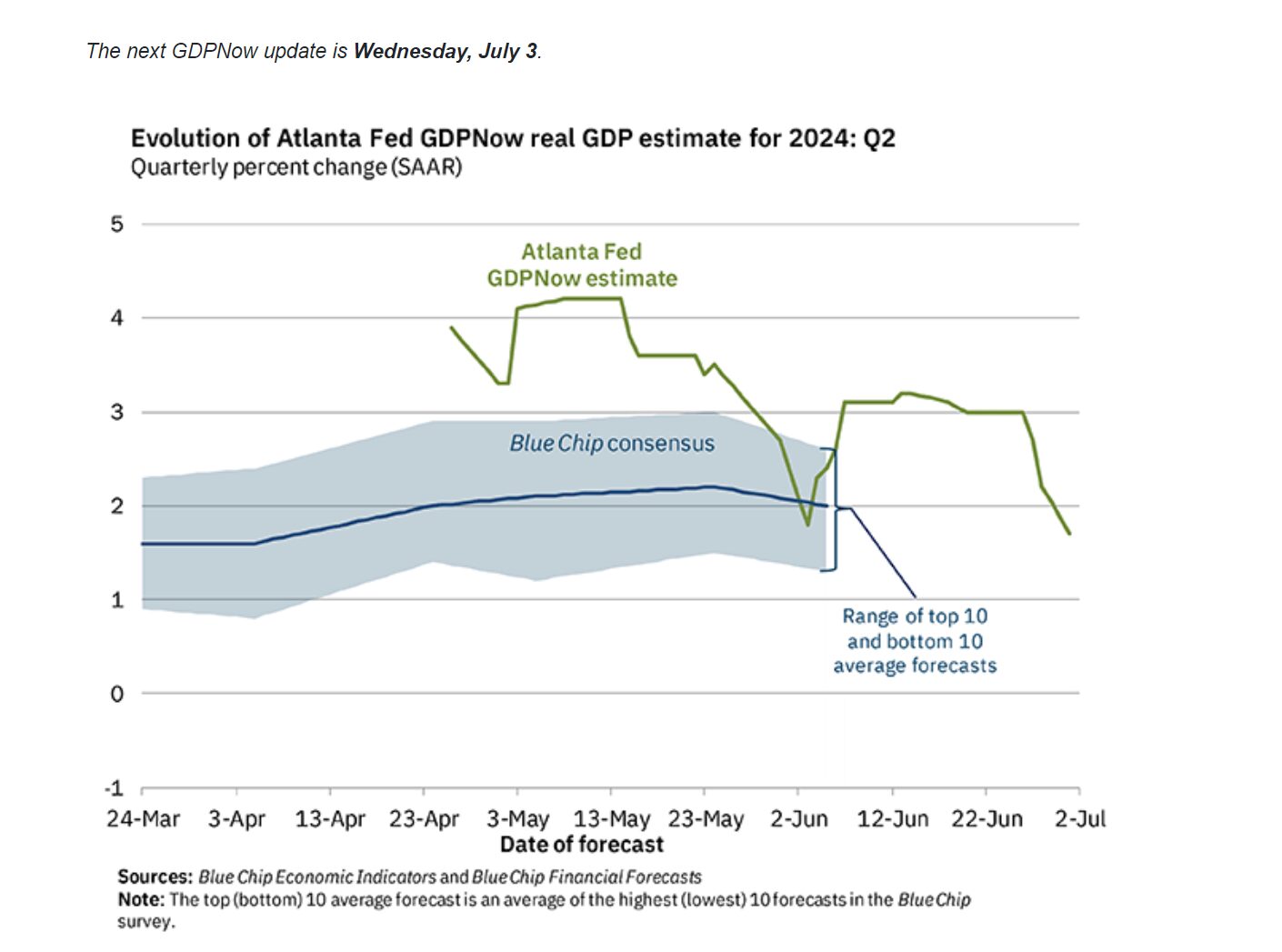

Here’s latest GDP Now, the numbers have been revised down sharply from 3% just a few weeks ago to 1.5% of latest count.

1.5% real GDP growth + 3% inflation means 4.5% nominal GDP growth.

If the Fed Funds rate is sitting at 5.5%, that’s going to slow the US economy further every day we sit with rates here.

No doubt that if we get rapid interest rate cuts that could be a powerful tailwind for REITs.

But I suppose the mid term goes back to the question above.

Even if we get a recession and rates are slashed to zero, how long would it stay there?

If the solution to every recession is for governments to spend a lot of money, it won’t be long before inflation roars back – and interest rates with it.

How I may invest $100,000 in REITs in 2024?

After the discussion above, it’s fairly clear we are in a different paradigm from the past decade.

Or as the reader described it:

Do we expect interest rates to go low as it was before? Honestly I don’t really have much faith in how things are progressing on the macro front. With the wars and supply chain restructuring, energy inputs will get higher and supply chain lengthening. Inflation seems to be entrenched for the moment. REITs as a class may never be the same as before when we had it good for the last 10 to 20 years of QE. Remember that low interest rates were never the default scenario before we were spoilt on the golden years of QE.

I don’t think you can buy and hold a basket of REITs and expect the same kind of smooth returns this decade.

Yes you can still make money off REITs, but it will be a much bumpier ride, with much more volatility along the way (which provides opportunity for active investors).

Central banks suppressed interest rate volatility for the past decade, and we are now back in a regime of higher interest rate volatility.

So the better question is that if you have $100,000 to invest, how much do you want to invest in REITs.

Assuming you decide you want to invest in REITs, I think there’s 2 ways to approach it:

- As an active investor

- From a portfolio perspective

Buy REITs as an active investor

With volatility, comes opportunity.

Here’s the share price for CapitaLand Ascendas REIT for the past 18 months.

You can see how it has traded in a very nice range, going to the higher end of the range when interest rates drop, and going to the bottom end of the range when interest rates are high.

If you’re an active investor, this would be heaven.

Especially compared to the past decade where REITs stayed flat for years.

There are portfolio benefits to REITs (as a Singapore Investor)

A lot of investors seem to think of REITs as a binary investment.

They see it as I make 10% on REITs, or I lose 10% on REITs this year.

A win-lose outcome.

But investing is not binary, and I encourage investors to look at it more expansively.

Let’s put it this way.

You know that REITs will do well if interest rates go down, but do poorly if interest rates stay high.

So if you buy some REITs, and also buy some stuff that does well if interest rates stay high, that could be a simple way to construct your portfolio.

That’s part of why investors like to pair REITs with banks today – as bank stocks will theoretically benefit if interest rates stay high and there is no recession.

How to hedge REITs from a portfolio perspective?

If interest rates stay high, it will depend on why interest rates stay high.

If they stay high because of high fiscal spending, and economic growth holds up, that could be good for stocks, and asset classes that would benefit include:

- Tech stocks

- Gold / Bitcoin

- Commodities

- Cyclical stocks (eg. Industrials, bank stocks)

- Cash (because short term rates stay high)

If interest rates stay high and economic growth slows, that’s probably not a good outcome for stocks in which case only things like bond / cash would benefit.

The point is that if you’re using this portfolio approach, don’t just buy REITs in isolation.

Look at how it fits into your portfolio.

There is significant uncertainty over how interest rates plays out the next 12 – 18 months.

So build a portfolio that does decently in various outcomes.

Buy stuff that will do well if rates stay high, buy stuff that will do well if rates drop.

And if your REITs are doing poorly, that’s completely fine because if means the rest of the portfolio is doing well.

That’s the kind of thinking I am using to construct my own portfolio – which you can see the detailed breakdown on FH Premium.

Which REITs to buy? As a Singapore Investor in 2024?

The way I see it, we are no longer in a rising tide lifts all boats scenario.

In this new paradigm – you must be selective about which REITs you buy.

REITs with China / Hong Kong real estate, I could see them staying weak for a while.

REITs with poor balance sheets, those could really suffer if interest rates stay high.

But with the right REITs, actually valuations are decent, you get exposure to high quality real estate, and you get a decent 5-6% yield while you wait.

Personally, I would focus on REITs with:

- Strong properties (primarily in Singapore)

- Strong balance sheet (not overleveraged)

- Good sponsor

In any case I don’t want to talk about specific names in this article, so do refer to the FH Stock / REIT watch on FH Premium for my fuller views on single REITs.

Closing Thoughts – This is not the last decade, picking the right REIT matters

But I want to stress again that valuations matter a lot.

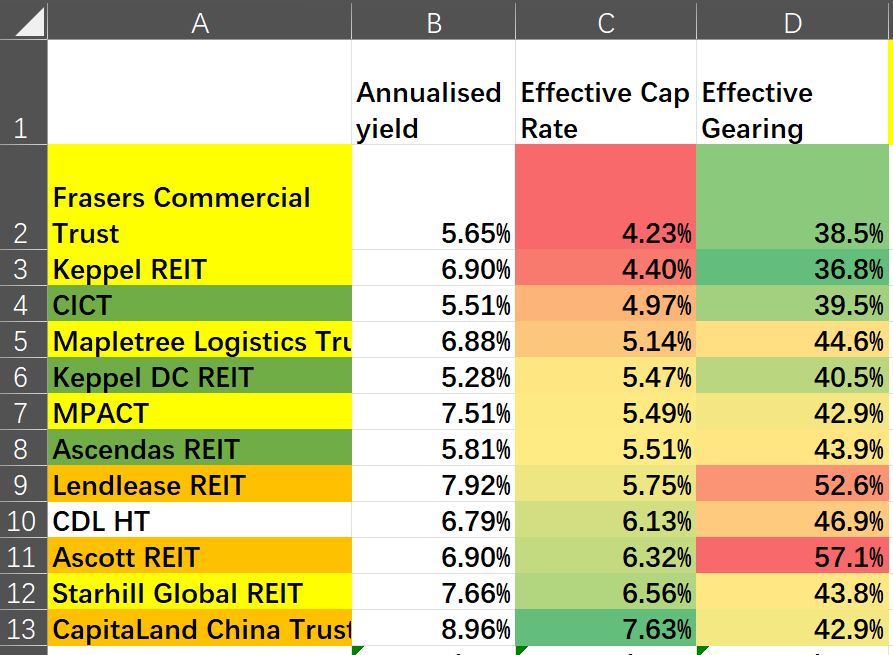

I’ve set out below the effective cap rates for the various REITs below (formula is Net Property Income / Market Cap + Debt Outstanding).

This gives you an idea of how much you are paying for each dollar of net rental income from the property portfolio.

Let’s say you’re deciding whether to buy CICT.

The question to ask yourself I suppose – is if the Singapore 10 year yield is 3.2% today, is CICT at 5% effective cap rate an attractive investment?

For its blue chip Singapore retail and office portfolio?

The full list of REITs I am looking at, and target pricing, is shared on FH Premium.

This article was written on 5 July 2024 and will not be updated going forward.

For my latest up to date views on markets, my personal REIT and Stock Watchlist, and my personal portfolio positioning, do subscribe for FH Premium.

– Get USD 400 cash voucher

I did a review on WeBull and I really like this brokerage – Cheap US Stock, Options and ETF trading, in a very easy to use platform.

I use it for my own trades in fact.

They’re running a promo now.

You can get up to USD 400 cash voucher.

You just need to:

- Deposit USD 2000 (or 10,000 for higher rewards)

- Execute 5 trades (for higher rewards)

Note that Webull is also offering zero commission for US options trading right now.

OCBC Online Equities Account – Trade on 15 global exchanges, all via the OCBC Digital Banking App!

Did you know that can you trade shares on your OCBC Digital Banking App?

With an OCBC online equities account, you can buy stocks, local ETFs, REITs, bonds and more directly through your banking app.

Everything on one app! Fuss-free funding, with access to 15 global exchanges

For SGD trades, you can fund and settle automatically via your OCBC account.

And for FX trades, you can settle using the foreign currency held in your OCBC Global Savings Account.

This means fuss-free trade settlement and minimising forex costs – saving you time and money.

Start trading with your OCBC Online Equities Account here!

Buy Bitcoin, Ethereum, and crypto on Coinhako – 10% off trading fees

I use Coinhako to purchase Bitcoin, Ethereum and crypto.

Enjoy 10% off trading fees using:

Invitation Code: CwHdSgU

Or sign up link: https://www.coinhako.com/affiliations/sign_up/CwHdSgU

Check out my full review on how to buy Bitcoin / Ethereum.

Trust Bank Account (Partnership between Standard Chartered and NTUC)

Sign up for a Trust Bank Account and get:

- $35 NTUC voucher

- 1.5% base interest on your first $75,000 (up to 2.5%)

- Whole bunch of freebies

Fully SDIC insured as well.

It’s worth it in my view, a lot of freebies for very little effort.

Full review here, or use Promo Code N0D61KGY when you sign up to get the vouchers!

Portfolio tracker to track your Singapore dividend stocks?

I use StocksCafe to track my portfolio and dividend stocks. Check out my full review on StocksCafe.

Low cost broker to buy US, China or Singapore stocks?

Get a free stock and commission free trading .

Get a free stock and commission free trading with .

Get a free stock and commission free trading with .

Special account opening bonus for Saxo Brokers too (drop email to [email protected] for full steps).

Or for competitive FX and commissions.

For REITs, I think everyone is too focused on the valuation (interest rates high, property and REIT valuation down) and cost side (interest rates high, higher interest expense).

How about the revenue side of the equation? In a scenario of strong growth, and accommodative monetary and fiscal policy + high growth high inflation, would the good quality REITs not be able to raise rentals at some point?

We all kind of made the same mistake in 2022 with the tech behemoths. Where everyone overly focused on the valuation impact from rising interest rates. The AI story certainly helped leaps and bounds sure… But the MAG7 (or whatever we call them these days) managed to grow earnings as well, and soon that became the market focus, and now we are at all time highs!

Interesting point. The problem is that the REITs have not been able to raise rentals quickly enough to offset the rise in interest expenses.

Interest rates are still the overwhelming factor, and you can see the huge move in REITs this week once Powell basically confirmed the Sep rate cut.

And frankly as a consumer you would hope they are not able to as well, because that higher rental usually translates into higher prices for consumers.

Of course, going forward once interest rate start going down, the difference in rental increase could be the key differentiator between the REITs that outperform and those that underperform.