So I received this great question from a reader:

Hi FH,

I am looking to retire soon, so I want to build up some passive income.

I have about $1.2 million that I can invest at the moment, currently spread across multiple investments.

I would like to get your views on where is the best place to park that money?

I have narrowed it down to 2 options:

- Buy an investment property and rent it out for passive rental income

- Buy a combination of REITs / US Stocks / Dividend Stocks for dividend yield

For option 1, I can use my spouse’s name to buy the property, so there will not be ABSD.

I prefer not to take up a mortgage if possible, because of high interest rates.

For option 2, I am open to relooking my portfolio once in a while.

But I do not want to spend too much time keeping up to date with what’s going on in my portfolio.

So it should be a semi-passive buy and hold portfolio.

My concern is that property prices in Singapore are very high at the moment, and rental market is weakening, so this may not be the best time to buy.

Yet US stocks etc are at all time highs, so I am also worried to buy a lot of stocks right now.

Hence writing in to get your views on the 2 options above.

How to earn $6000+ a month in passive dividend income? Buy REITs, dividend stocks, or investment property? (as a Singapore Investor in 2024)

Very interesting question indeed.

The reader suggested 2 options:

- Buy an investment property and rent it out for passive rental income

- Buy a combination of REITs / US Stocks / Dividend Stocks for dividend yield

But if you really think about it.

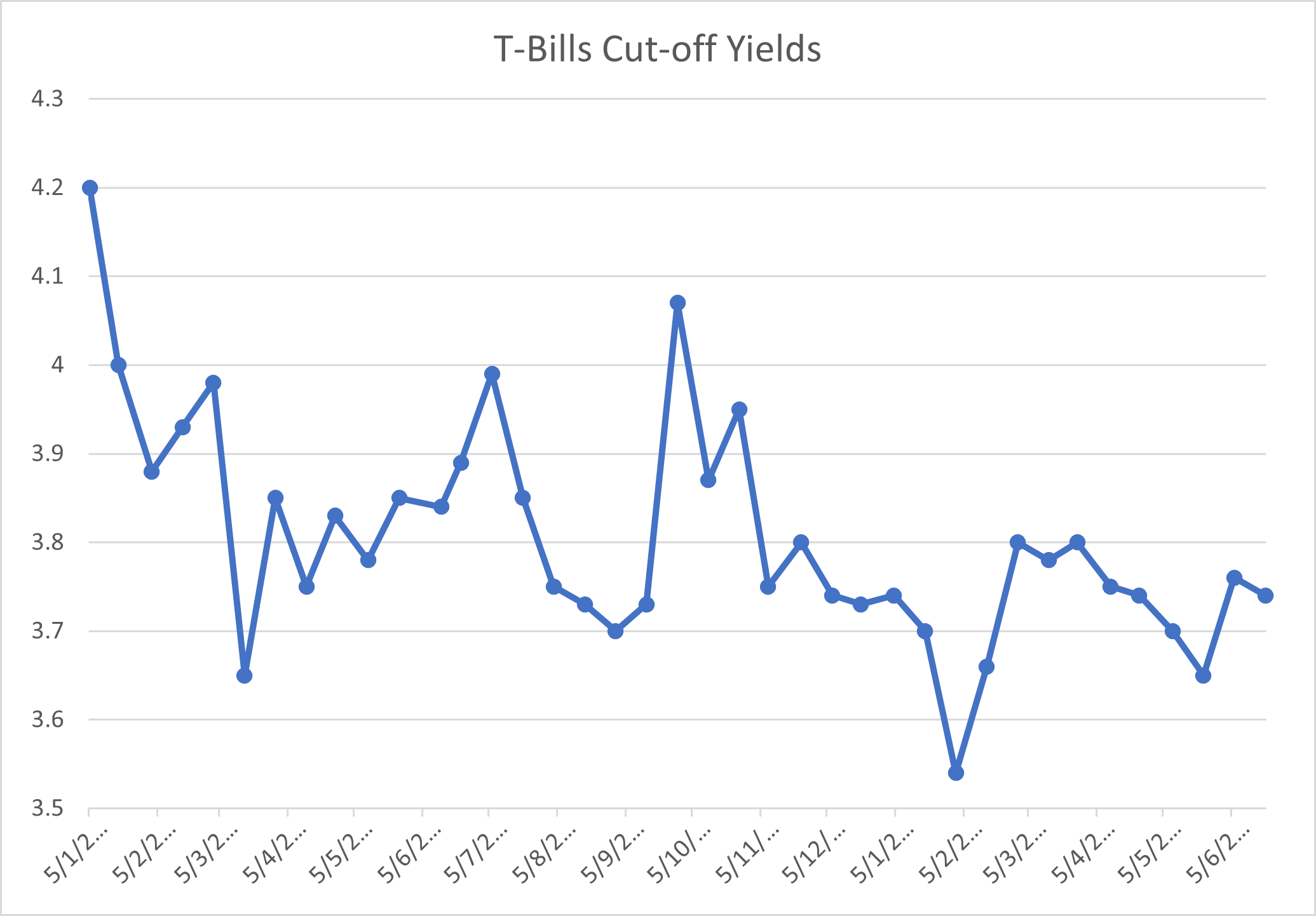

In this day and age, when T-Bills are yielding 3.74% risk free.

There’s actually a third option –invest the money fully in risk free Singapore government bonds like T-Bills or Singapore Savings Bonds.

So I updated the list to 3 options below:

- Just park the cash in risk free T-Bills / Singapore Savings Bonds etc

- Buy an investment property and rent it out for passive rental income

- Buy a combination of REITs / US Stocks / Dividend Stocks for dividend yield

Option 1 is risk free and worry free, so let’s start by discussing this.

How much passive dividend income if you park in risk free Singapore government bonds? (Option 1)

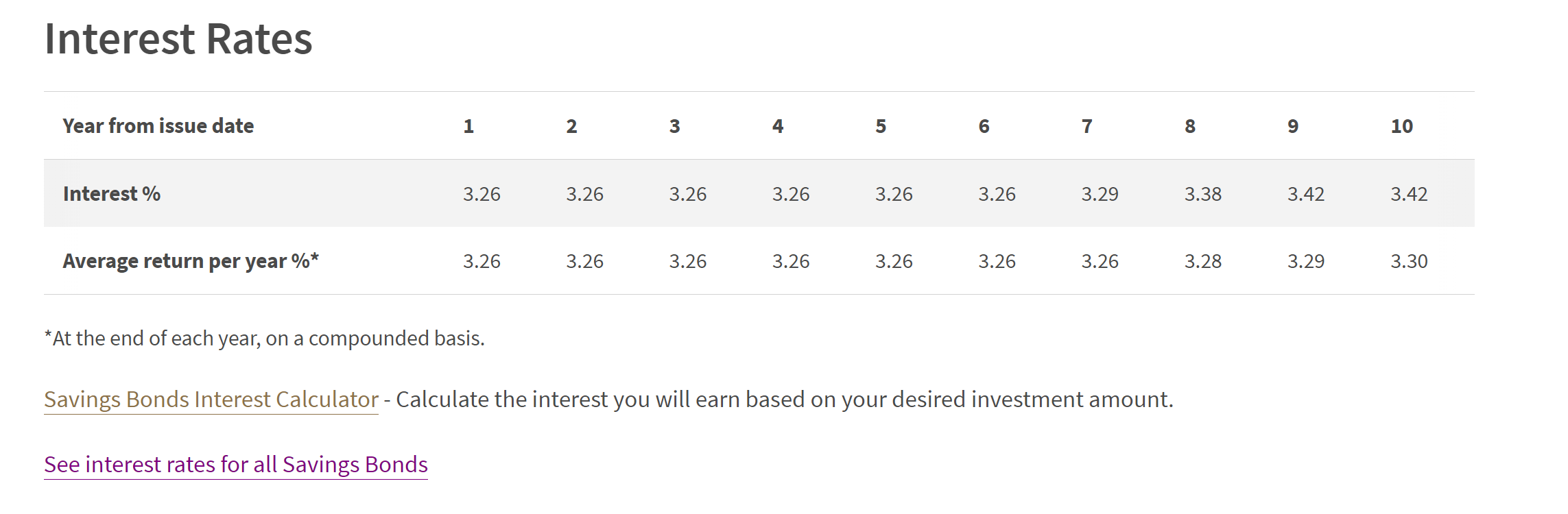

The latest Singapore 10 year government bond yields 3.25%.

In fact if you buy the latest Singapore Savings Bonds you’re looking at an even higher yield of 3.30%.

Between the reader and his spouse, they buy a combined $400,000 Singapore Savings Bonds.

If you mix in T-Bills at 3.74% yield, you can actually get an even higher blended yield (but it does expose you to interest rate risk because you don’t know where interest rates will be in 6 months).

Let’s say that you can invest that $1.2 million risk free at a 3.25% yield long term.

You’re looking at $39,000 a year in passive dividend income.

That’s $3250 a month in passive dividend income.

For something that is risk free, fully backed by the Singapore government.

Sure, some of you may think this is too low.

But at the very minimum, you need to know that this is the baseline risk free option, if you choose to take zero risk.

|

Option |

Asset Class |

Passive Dividend Income |

|

1 |

Buy risk free Government Bonds |

$3250 a month |

How much passive dividend income if you buy an Investment Property and rent it out? (Option 2)

According to this website:

“Average gross rental yields in Singapore stands at 4.35% (Q2, 2024). Previously, in Q1, 2024 the average gross rental yield stood at 4.65%.”

What this means simplistically is that if you buy a property for $1.2 million, you can expect to get about $52,200 a year in gross rental income.

$4350 a month on average – although this is gross (before expenses), and average numbers.

Let’s try to refine the numbers a bit more.

The exact rental income will be higher or lower depending on which property you buy and where

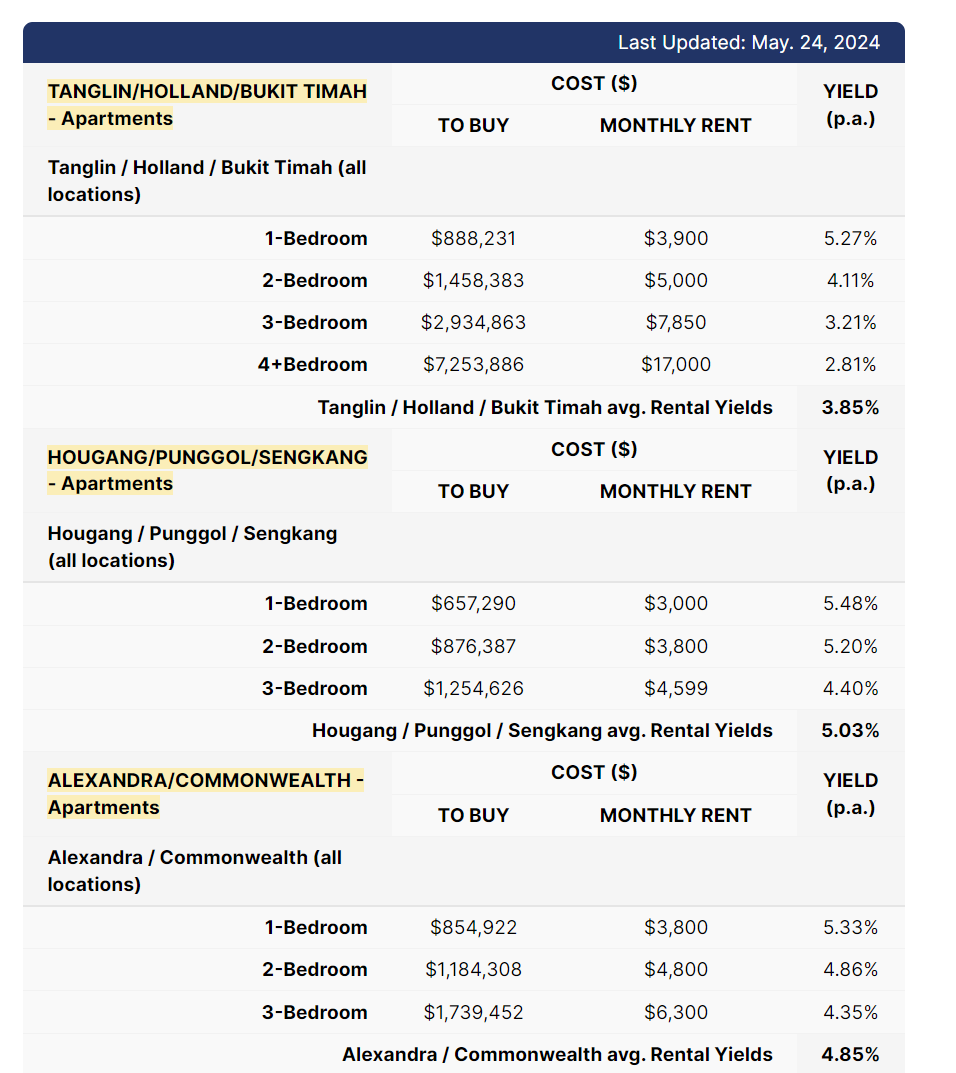

You can see the further breakdown in rental yields by location below.

You can see how in demand locations like Tanglin actually have a lower yield (because of higher selling price).

While other locations like Sengkang has a higher yield (because of lower selling price).

Looking at the list below, the highest yield for $1.2 million purchase amount is a 3 bedroom in Hougang / Punggol / Sengkang, at a 4.40% yield.

So, not all that different from the average yield we used above.

But this is gross rental income – don’t forget expenses, and stamp duty

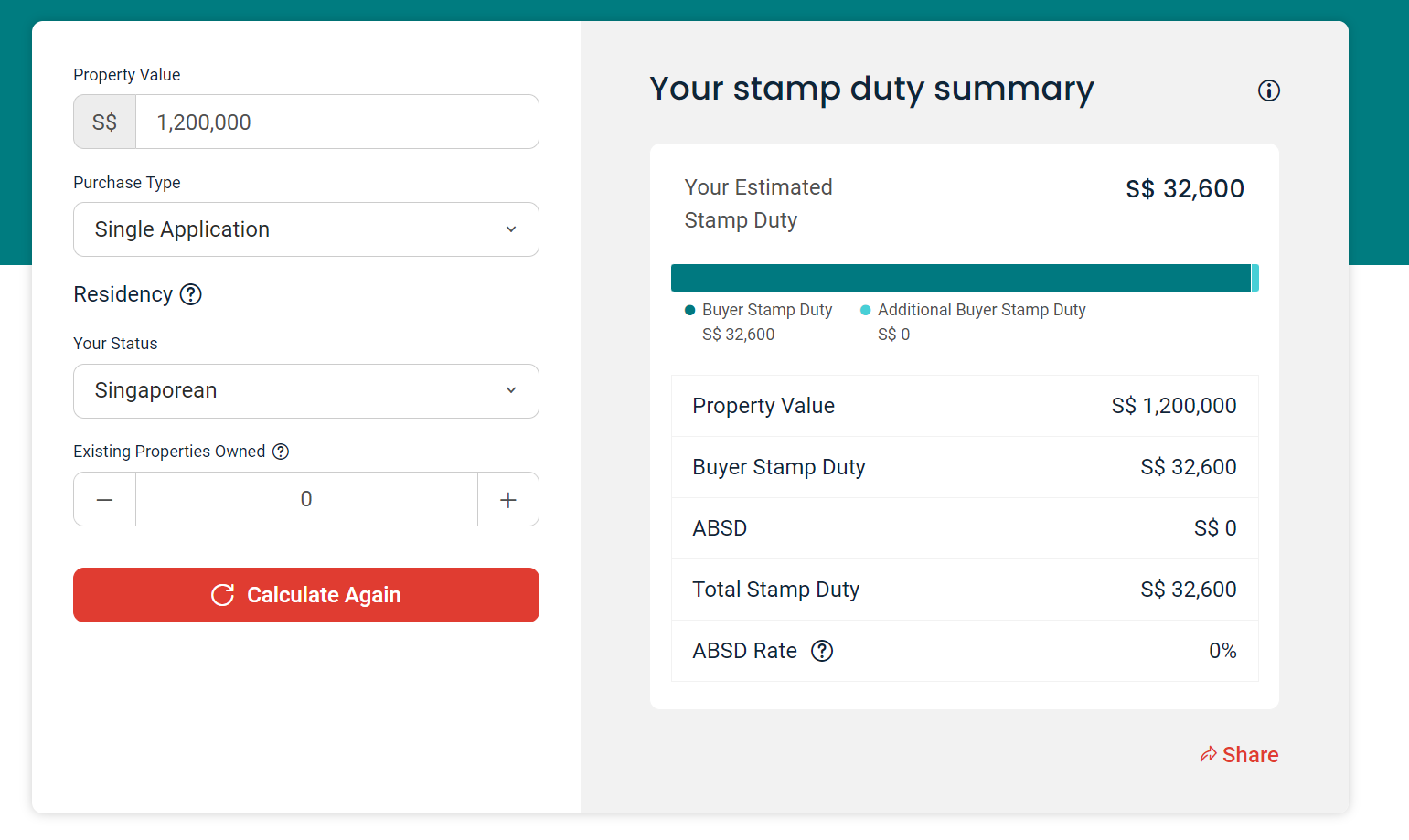

If you buy a $1.2 million property tomorrow.

Even without ABSD, you’re looking at $32,600 in stamp duty.

This means effectively you’re only investing $1.167 million.

And don’t forget the yield above is gross rental.

Let’s say we minus 15% for expenses (including agent fee, MCST maintenance fees, repair bills, furniture etc – many landlords will tell you the 15% is probably on the low side).

Running all the revised numbers above, gets us to a net rental income of $43,660 a year.

Or $3640 a month in passive income.

Wait… Buying an investment property does not produce a significantly higher yield than risk free government bonds?

This is pretty unbelievable stuff because based on the discussion above, you can get $3250 a month just by investing the money in risk free government bonds.

All that work to buy a rental property, lease it out, deal with agents and tenants, and you’re only getting an extra $390 a month?!

|

Option |

Asset Class |

Passive Dividend Income |

|

1 |

Buy risk free Government Bonds |

$3250 a month |

|

2 |

Buy an investment property and rent it out for passive rental income

|

$3640 a month |

But… Investment property has the potential for capital gains

But to be absolutely fair, I think the big advantage that an investment property has going for it (that buying government bonds doesn’t).

Is the possibility of capital gains, and rental increases in the longer term.

This provides some kind of an inflation hedge.

If you invest $1.2 million in government bonds at a 3.25% yield.

Yes you will get the $3250 a month in dividend yield.

But 10 years later the principal $1.2 million will stay exactly the same.

If you buy an investment property, there is a chance that in 10 years time the investment property would be worth more than it is today.

There is also a chance that rents can go up.

But… can investment property prices fall?

This can work both ways though.

If prices can go up, they can also go down.

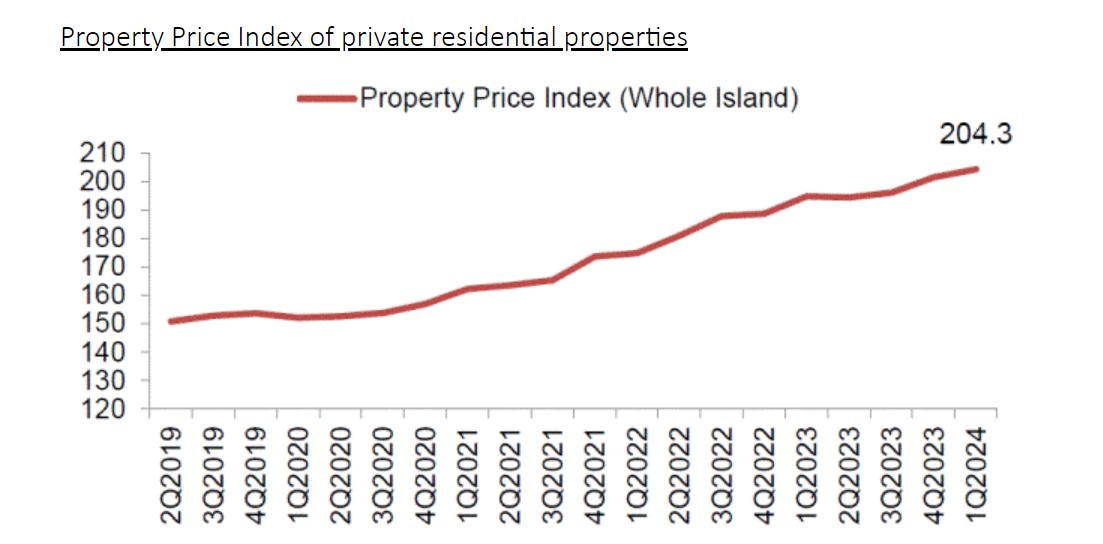

For now at least, property prices are still going up – although the pace of increase has slowed drastically from the 2021/2022 madness.

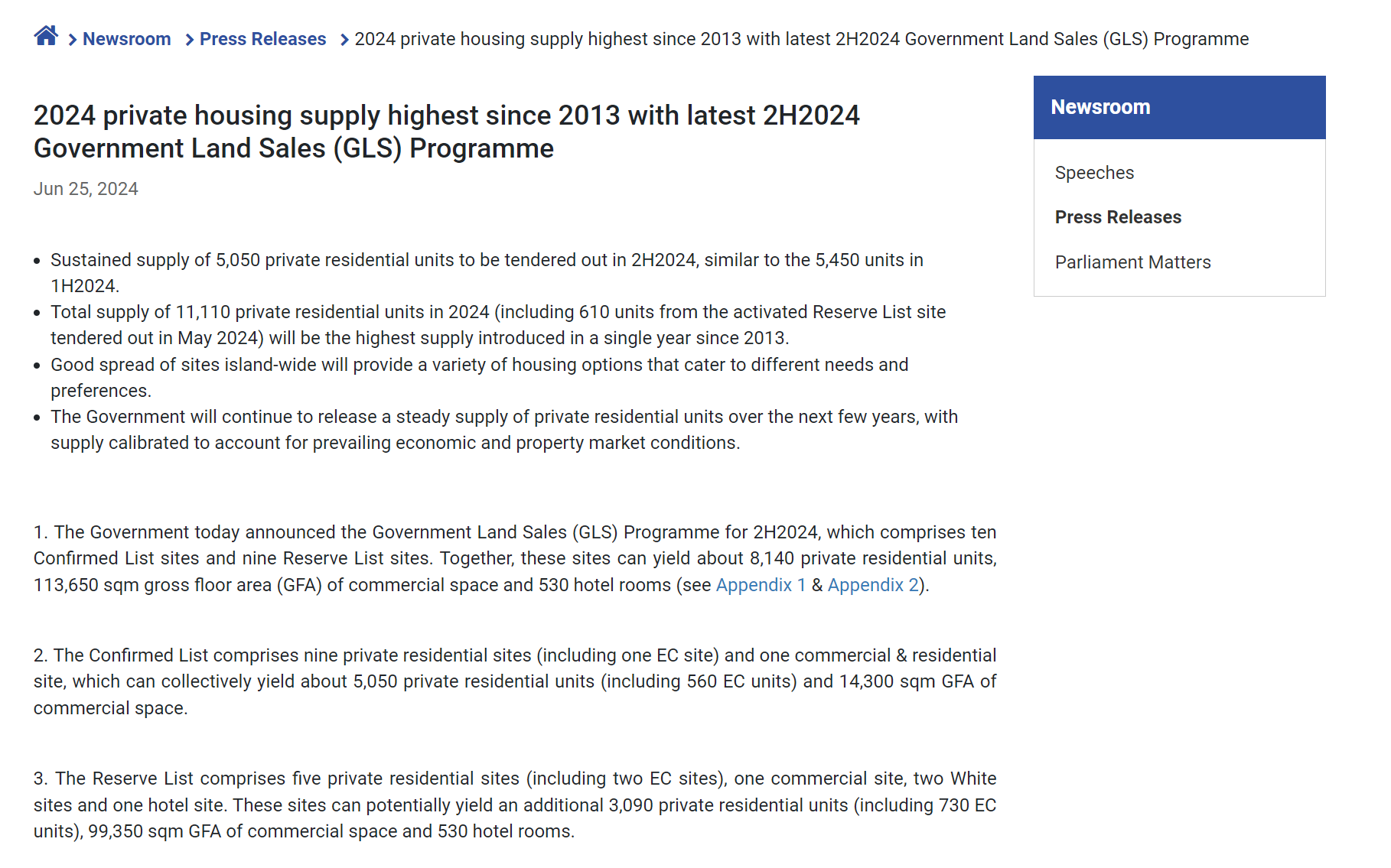

What does concern me – is that fact that the government is releasing a lot of new land supply.

Here’s the press release from MND showing that 2024’s private housing supply is the highest since 2013.

Yes, I know that this is to correct for the undersupply in homes we saw during the COVID years.

But real estate is as simple as demand-supply.

If supply is going up, where is the demand coming from to absorb all the new supply?

Foreigners are no longer buying (in a big way) due to ABSD, and Singaporeans can only buy 1 each because of ABSD.

This implies the bulk of the new supply needs to be absorbed by new households (whether Singaporean or immigrant).

And with a declining birth rate, I don’t see that increasing drastically unless something changes on the immigration front.

Have rental yields peaked for Singapore real estate?

You may argue that as a buy and hold investor, you don’t care about property prices.

You only care about the rental yield.

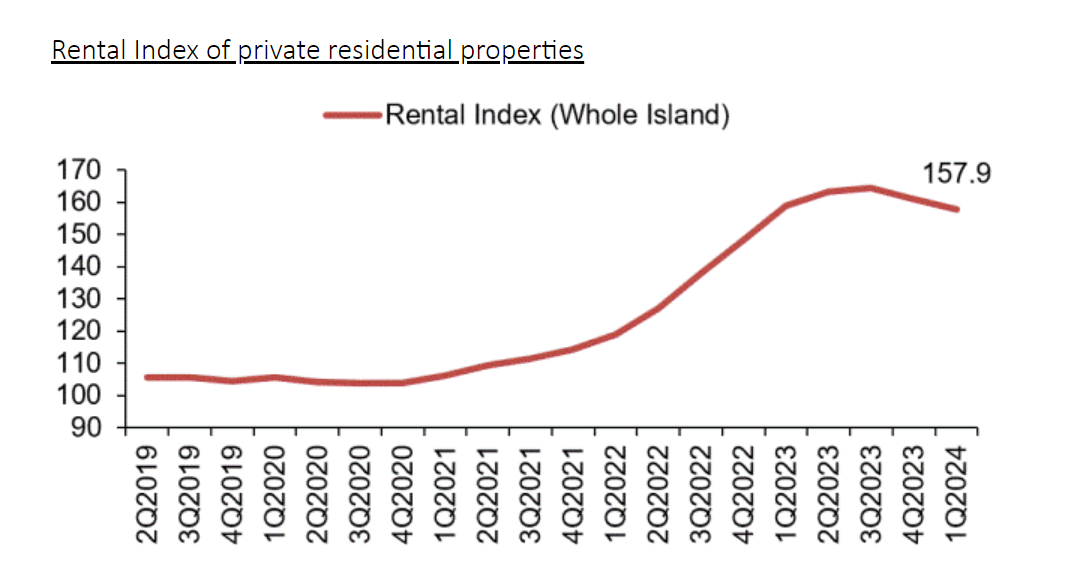

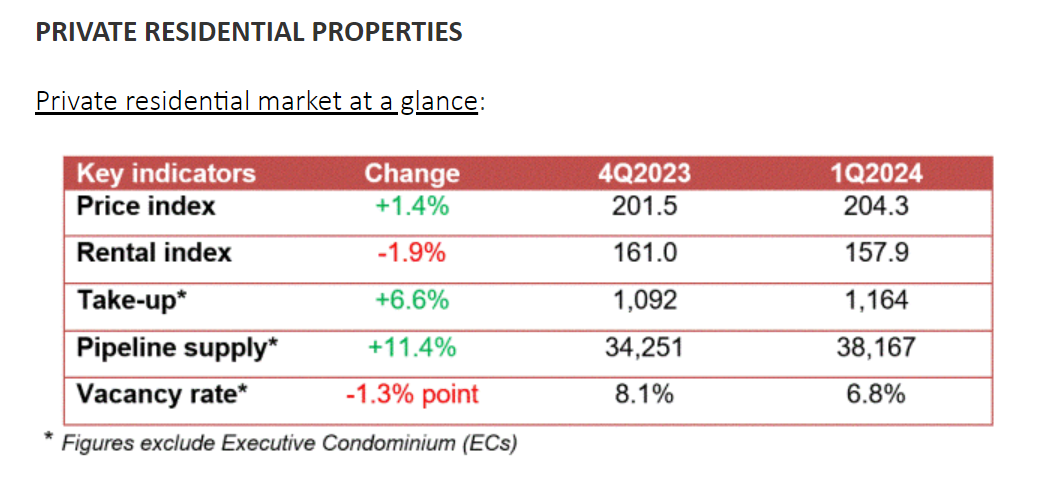

On that note – if you look at the latest URA data, you’ll clearly find that rental prices peaked in mid 2023, and have been on a decline ever since:

In the most recent quarter, rents were down 1.9% across the board.

Much of this is due to lower rental demand from foreigners, as the job market for expats has cooled.

So the rental yield numbers above that we assumed above are as of today.

Whether they hold up the next few quarters, really depends on how the economy holds up.

Don’t forget there’s a lot of new supply coming online as well.

BTW – we share commentary on Singapore Investments every week, so do join our Telegram Channel (or Telegram Group), Facebook and Instagram to stay up to date!

I also share thoughts on Twitter regularly.

Don’t forget to sign up for our free weekly newsletter too – with weekly roundups every Sunday!

What’s the bottom line – Will we see capital gains on Singapore property prices? Rental increases

Long story short – in the long term, Singapore real estate prices and rents will probably track economic growth.

If Singapore’s economy does well, I think you’ll see property prices go up, and rents go up.

But the short term is harder to predict, and going to come down to demand-supply dynamics.

With so much new supply coming online, you need to see an increase in demand to match the supply.

And for now it’s not so clear where that demand is going to come from.

How much dividend income if you buy a combination of REITs / Dividend Stocks? (Option 3)

What if you buy a mix of REITs and Dividend stocks, for dividend yield?

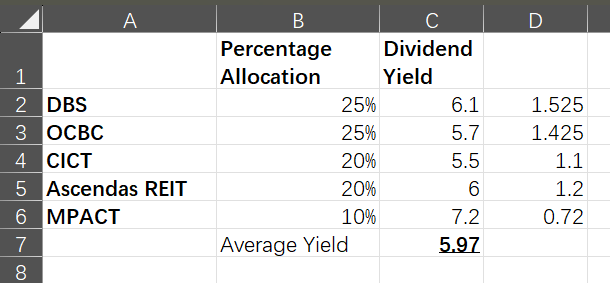

Let’s just say you split the money 50-50 among Singapore bank stocks and REITs.

For discussion’s sake only – let’s say you buy DBS and OCBC for the banks, and you buy CICT, Ascendas REIT and Mapletree Pan Asia Commercial Trust for the REITs.

If you do that, you can get about a 6% dividend yield in today’s market.

Note these are indicative stocks only, you can see the full list of stocks / REITs I am keen to buy on FH Premium.

How much passive dividend income a month?

Assuming you invest $1.2 million at that 6% dividend yield.

That’s $72,000 a year.

Or $6,000 a month in passive dividend income.

Note that as this is dividend income, it is net of expenses and tax free too.

So interestingly, dividend stocks seems to be the highest dividend income of the 3 options:

|

Option |

Asset Class |

Passive Dividend Income |

|

1 |

Buy risk free Government Bonds |

$3250 a month |

|

2 |

Buy an investment property and rent it out for passive rental income

|

$3640 a month |

|

3 |

Buy a combination of REITs / US Stocks / Dividend Stocks for dividend yield

|

$6,000 a month |

What is the risk with buying REITs and dividend stocks? As a passive dividend investor?

As we all know, buying REITs and dividend stocks are not without risk.

There are 2 key risks to talk about:

- Micro risk (eg. Stock not doing well)

- Macro risk (eg. Recession)

Single stock risk (eg. Stock not doing well)

Here’s the chart of Mapletree Pan Asia Commercial Trust.

I can pull up the chart of many other former blue chip dividend stocks like Singtel or Singpost, but you get my point.

Sometimes a stock that you think is a safe dividend stock.

Just turns out to not be the case – and you suffer capital losses / dividend cut because the REIT or stock is not performing well.

There’s an easy fix for this one though, which is via diversification.

Instead of just buying 5 stocks per my illustration above.

You can expand it to a list of 15 – 20 stocks (you can see the full list of stocks / REITs I am keen to buy on FH Premium.).

That should significantly cut down on the single stock risk.

But this would significantly increase the amount of effort to keep track of all that is going on in the portfolio.

Macro risk (eg. Recession)

And even if you diversify, this doesn’t remove macro risk like recessions.

Here’s the 20 year chart for DBS Bank.

You can see how while the stock goes up over time.

There are periods like 2008, 2015, 2018, 2020, where the stock went down sharply for a few years.

And this may look fine on a chart when you know that the share price recovers eventually.

But trust me when you’re living through it and your investments are down 40% and you don’t know if they will ever recover.

It’s a completely different feeling altogether, especially so for a retiree.

Are these risks worth it? For the higher passive dividend income?

Long story short.

I think it’s clear that of the 3 options, buying REITs / dividend stocks provide the highest dividend income at $6,000 a month.

But it’s also the highest risk option, with the most volatility.

Not for the faint of heart.

Whether this is worth it, and whether one has the capability (or emotional fortitude) to use this option.

I suppose that is for each investor to answer for himself.

How to earn $6000+ a month in passive dividend income? Buy REITs, dividend stocks, or investment property? (as a Singapore Investor in 2024)

I updated the table below to include what I see as key risks with each approach:

|

Option |

Asset Class |

Passive Dividend Income |

Risks |

|

1 |

Buy risk free Government Bonds |

$3250 a month |

Does not hedge inflation well in the longer term, as no upside potential. |

|

2 |

Buy an investment property and rent it out for passive rental income

|

$3640 a month |

Short term, rentals / property prices will depend on demand supply dynamics.

Longer term, it will depend on Singapore’s economic growth. |

|

3 |

Buy a combination of REITs / US Stocks / Dividend Stocks for dividend yield

|

$6,000 a month |

Need to pick single stocks well.

Even if you do so, still vulnerable to market wide risks. |

Which approach would I go with? For Passive Dividend Income as a Singapore Investor?

Option 1 – Buy risk free Government Bonds

I don’t think Option 1 works for the longer term.

The main problem is that it has no capital gains potential, so in the longer term you may see buying power eroded due to inflation.

It works for short periods of time (or if your principal amount is very big).

But if you’re investing for a multi decade period, I think you do want an asset class like property or stocks that can keep pace with inflation.

Option 2 – Buy investment property and rent it out for passive rental income

My personal view is that I am not a big fan of buying an investment property today.

I know it’s a bit hypocritical of me to say this because I myself own an investment property.

But I purchased my investment property before the large jump in prices post 2022.

The way I see it – at today’s market prices, at today’s rental yields, and with all the new land supply being released by the government.

If I had to make the same decision again today, I don’t see myself buying an investment property today.

Option 3 – Buy a combination of REITs / US Stocks / Dividend Stocks for dividend yield

That leaves option 3.

And yes, I may be somewhat biased towards this option because this is literally all I write about on Financial Horse.

And you do have to acknowledge that this is the most risky option of the 3.

If you buy a Singapore property, you’re probably not going to wipe out 40% of your capital even if we get a bad recession.

With stocks or REITs, you could see well in excess of 40% capital losses in a true market sell-off.

So with this option, you do need to manage risk well, and you must understand what it is you’re buying.

What I would add is that you don’t have to invest the full $1.2 million in dividend stocks or REITs.

You can for example set aside $400,000 to buy Singapore Savings Bonds or T-Bills, and only invest the rest.

If you play around with the cash in this way, you can try to achieve a dividend yield somewhere between $4000 – $6000 a month, based on the level if risk you are prepared to take.

|

Option |

Asset Class |

Passive Dividend Income |

|

1 |

Buy risk free Government Bonds |

$3250 a month |

|

2 |

Buy an investment property and rent it out for passive rental income

|

$3640 a month + capital gains/loss potential |

|

3 |

Buy a combination of REITs / US Stocks / Dividend Stocks for dividend yield

|

$6,000 a month + capital gains/loss potential |

It’s not a binary decision too.

If things change down the road and property becomes cheap, you can always choose to sell the stocks and buy a property then.

Closing Thoughts

The final point I wanted to add is that the market is pretty efficient like that.

Stocks / REITs are the most risky option, but offers the highest payoff if you get it right.

But because of its very nature, it’s not for everyone.

The benefit of an investment property (Option 2) is that because the Singapore government controls demand-supply tightly, you probably won’t lose a lot of money even if you’re wrong on this.

So it’s a less risky option.

But because of that, and because of today’s prices, I don’t think the upside would be as high.

You cannot buy a property today and expect to see the same kind of returns the previous generation saw, when Singapore moved from third world to first world status.

Singapore today is already a leading first world financial centre, and that is reflected in the property prices today.

Whatever the case, this is my take on the issue, and I would love to hear your thoughts on the 3 options above.

Which option would you go for in today’s market?

This article was written on 28 June 2024 and will not be updated going forward.

For my latest up to date views on markets, my personal REIT and Stock Watchlist, and my personal portfolio positioning, do subscribe for FH Premium.

OCBC Online Equities Account – Trade on 15 global exchanges, all via the OCBC Digital Banking App!

Did you know that can you trade shares on your OCBC Digital Banking App?

With an OCBC online equities account, you can buy stocks, local ETFs, REITs, bonds and more directly through your banking app.

Everything on one app! Fuss-free funding, with access to 15 global exchanges

For SGD trades, you can fund and settle automatically via your OCBC account.

And for FX trades, you can settle using the foreign currency held in your OCBC Global Savings Account.

This means fuss-free trade settlement and minimising forex costs – saving you time and money.

Start trading with your OCBC Online Equities Account here!

Buy Bitcoin, Ethereum, and crypto on Coinhako – 10% off trading fees

I use Coinhako to purchase Bitcoin, Ethereum and crypto.

Enjoy 10% off trading fees using:

Invitation Code: CwHdSgU

Or sign up link: https://www.coinhako.com/affiliations/sign_up/CwHdSgU

Check out my full review on how to buy Bitcoin / Ethereum.

– Get up to USD 2500 worth of shares

I did a review on WeBull and I really like this brokerage – Cheap US Stock, Options and ETF trading, in a very easy to use platform.

I use it for my own trades in fact.

They’re running a promo now.

You can get up to USD 2500 free shares.

You just need to:

- Fund USD 500

- Execute 5 trades

Trust Bank Account (Partnership between Standard Chartered and NTUC)

Sign up for a Trust Bank Account and get:

- $35 NTUC voucher

- 1.5% base interest on your first $75,000 (up to 2.5%)

- Whole bunch of freebies

Fully SDIC insured as well.

It’s worth it in my view, a lot of freebies for very little effort.

Full review here, or use Promo Code N0D61KGY when you sign up to get the vouchers!

Portfolio tracker to track your Singapore dividend stocks?

I use StocksCafe to track my portfolio and dividend stocks. Check out my full review on StocksCafe.

Low cost broker to buy US, China or Singapore stocks?

Get a free stock and commission free trading .

Get a free stock and commission free trading with .

Get a free stock and commission free trading with .

Special account opening bonus for Saxo Brokers too (drop email to [email protected] for full steps).

Or for competitive FX and commissions.

As Reits looks like all time low. This seems to be better timing aligning with option 3. Chances of getting reit stock price appreciation along with dividend yield is higher.

I would definitely go with option 3.

Fair enough! I dont think there is a right or wrong here. It depends very much on the investor and his/her strengths as well.

For #3, you can suggest the reader etf or trust .

True. That hedges the single stock risk, but not the macro risk. Actually something as simple as the STI ETF might work. Since the exposure is mainly banks and REITs.

Wouldn’t a variation of the “110 – age” rule for stocks/bonds be more prudent for a *retiree*? As opposed to the somewhat false trichotomy of the options given?

If he truly needs 6k/month all supported by only the 1.2m portfolio, he might need to reconsider his retirement or his expenses…

Since even pushing the limit at 4% SWR, is only 48k/year with 1.2m

(I think for Singapore, 3-3.5% is more prudent, hence the “pushing limit” wording.)

“But I do not want to spend too much time keeping up to date with what’s going on in my portfolio.”

This looks like a candidate for a Boglehead-like portfolio with whole market indexes ETF for both the equities and bonds components. 🙂

Want to squeeze more % out of portfolio, it’s inevitable to be up to date and follow what’s going on…

Right?

That’s a good point. Good comment.

In the table you created. Property has potential of capital appreciation and no depreciation? Are you aware that every year, there are Properties sold that lost money?

Sorry that’s a typo. I meant to say capital gains/loss potential for property as well.

If the reader is going to retire soon and needs the passive income soon, then go for combination of dividend/interest from REITs, stocks and bonds (T-bills, government bonds etc.) seems better choice than investment property.

Because for investment property, it is best to take loan and then rent out. In this way, we are making use of a small amount of invested money in down payment and any expenses to get the return from other people’s money (bank loan). Then, the tenant helps to pay down slowly for the rest of the amount of the property. This is using leverage to play property. And it needs a longer time frame to yield best results.

However, if the retiree needs the passive income soon, then just go for paper investments, making sure it is diversified, and not focused on only a few stocks or a few REITs or bonds alone.

Interesting comment. I guess the worry for a retiree to take a loan is that once he stops work he won’t have new cash flow coming in, and has to depend on the rent to pay the mortgage. Increases the risk if something goes wrong (eg. rental yields drop). But I get what you mean, using debt is the more “efficient” route.

To me REITs as a class is not very attractive as long as the interest rates is going to be higher for longer. Essentially they need to give out 90% of their income as dividends in order to give shareholders a 5 to 7% yield. Monitoring their gearing, you can already see that even blue chips like CICT has a gearing of 40% or more. Int rates risk is going to affect the DPU and that is why you see this risk priced into the REITS price now. On the other hand banks, even at their high valuation now can give you a 5 to 6% yield with just 50% payouts and retain a solid low risk balance sheet.

Do we expect interest rates to go low as it was before? Honestly I don’t really have much faith in how things are progressing on the macro front. With the wars and supply chain restructuring, energy inputs will get higher and supply chain lengthening. Inflation seems to be entrenched for the moment. REITs as a class may never be the same as before when we had it good for the last 10 to 20 years of QE. Remember that low interest rates were never the default scenario before we were spoilt on the golden years of QE. Having said that, there are risks on the horizon that the FEDs cannot engineer a soft landing or a trigger event that sends the US into a recession (like CRE imploding or sudden outbreak of escalatory war, or the US finally reaching the cliff edge of their USD34Trillion debt). Sorry to paint such a dark future. Depending on the scenario, it might be the best opportunity to deploy more cash or the worst risk you can ever take. One must weigh these carefully when the time comes.

STI ETF is not attractive to me. You can see the STI performance and it should be obvious that the returns is poor compared to an S&P index fund (find a Irish domiciled one).

My own option is the buy all three SG banks progressively and keep some monies in a T bill ladder that you can deploy progressively in case there is an opportunity. Always keep some cash for emergencies. Equities will always be a risk but it is still my preferred option with a mix of T bills.

Thanks for the great comment. I generally agree with you on this, and shared some thoughts in last week’s article: https://financialhorse.com/how-i-may-invest-100000-in-reits-in-2024-are-reits-still-a-good-investment-as-a-singapore-investor/

As a retiree or anyone who doesn’t want unnecessary hassle, I would not recommend property investment.

It can be tedious, troublesome and worrisome. This is especially between tenancies and when encountering difficult tenants.

People who find it easy psychologically is usually because they are sitting on large unrealized capital gains.

Fair enough!