I was reading an article on Channel News Asia recently.

It was about the FIRE movement in Singapore (Financial Independence Retire Early).

It’s a personal finance movement – where the aim is to live a frugal life, and use one’s investment (or passive) income to cover their living expenses.

This allows you to gain financial independence, and retire early.

The article is pretty good, and worth a read if you’re interested in FIRE.

For me, there was one line in particular that stood out:

Under his FIRE plans, Mr Tan’s longer-term goal involves achieving a passive income of S$5,000 a month by the age of 40. He plans to attain this by amassing a S$2.4 million portfolio with 2.5 per cent dividends per annum, calculated based on potential expenses such as mortgage for a Built-To-Order (BTO) flat and daily expenses for food, transport and utilities.

S$2.4 million portfolio with 2.5 per cent dividends per annum?!

Now I generally think of myself as quite a conservative investor.

But when I read that line, I genuinely had a double take.

This guy wants to achieve a passive income of $5,000 a month.

And his plan is to save up $2.4 million, and invest it in a portfolio that pays 2.5% dividend a year?!

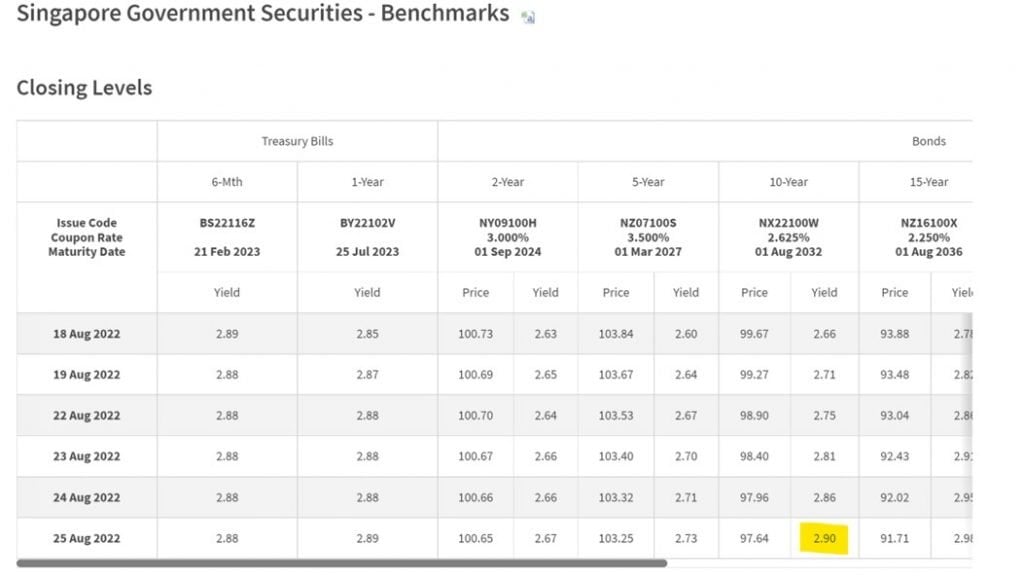

In case Mr Tan doesn’t know, the latest 10-year Singapore Government Security trades at a 2.9% yield.

So he can literally save up the $2.4 million, chuck it all into risk-free Singapore Government Bonds, and be done with it.

I don’t know, just seems like a very uncreative approach to problem solving.

What’s a more realistic dividend yield?

But this got me thinking.

2.5% dividend yield is probably a bit too conservative.

What’s a more realistic dividend yield?

I’ve done up the numbers above.

At 4% dividend yield, Mr Tan just needs to save up $1.5 million to hit his target ($5,000 a month).

While at 6% dividend yield, he just needs $1 million.

In other words – the higher the dividend yield, the less you need to save, and the earlier you can retire.

So let’s try to build a portfolio for each of the 3 dividend yields – 2.5%, 4.0%, and 6.0%.

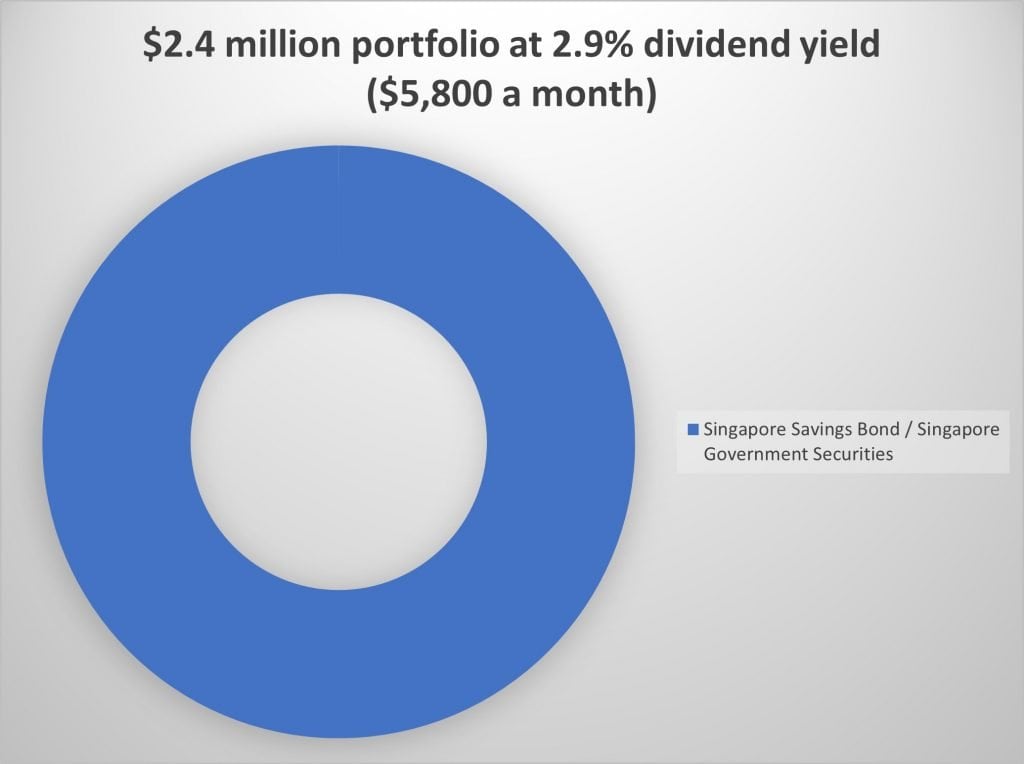

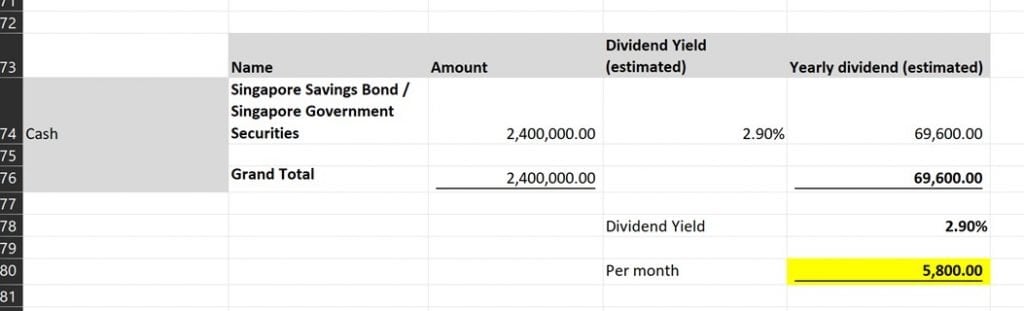

$2.4 million portfolio at 2.9% dividend yield ($5,800 a month)

Let’s start with the easy one.

If you have $2.4 million, you can invest it all into Singapore Government Securities.

At a 2.9% yield, you get $5,800 dividend income a month, well ahead of your target.

Problems with this 2.9% dividend yield portfolio

Now I know this portfolio is theoretically risk free because Singapore Government Securities carry no risk.

But I think that hides 2 key risks:

- Inflation

- Actually saving up the money

Inflation

First off – this portfolio has absolutely zero chance of appreciating in value.

You are never going to get a return above 2.9%, ever.

Sure, you can sell your SGS on the open market at a profit if interest rates drop, but then you’re just reinvesting that money at higher prices anyway.

So if you run a portfolio like this, you need to be absolutely certain on your living expenses of $5,000 a month.

Get it wrong, and you could be setting yourself up for trouble later on in retirement.

Actually saving up the $2.4 million

With this approach, you need to actually save up $2.4 million cash.

If you’re a high earning software engineer making $20,000 a month with no kids, that might be very achievable by 40.

If you’re an average earner with 3 kids, it could be a lot harder.

My personal views on the 2.9% dividend yield portfolio?

For what it’s worth, I actually don’t like this 2.9% portfolio that much.

It’s why I think bonds in this climate only work for the ultra-high net worth.

If you have $100 million to put into Singapore Government Securities, you can live very well off the $2.9 million a year.

If you only have $2 million, there are very real risks with running a portfolio like that.

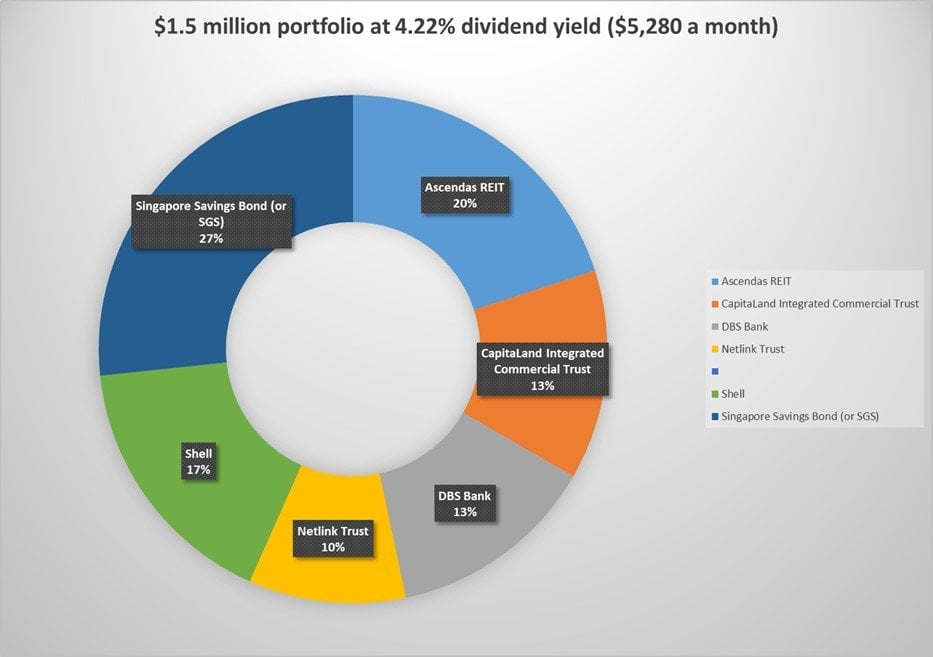

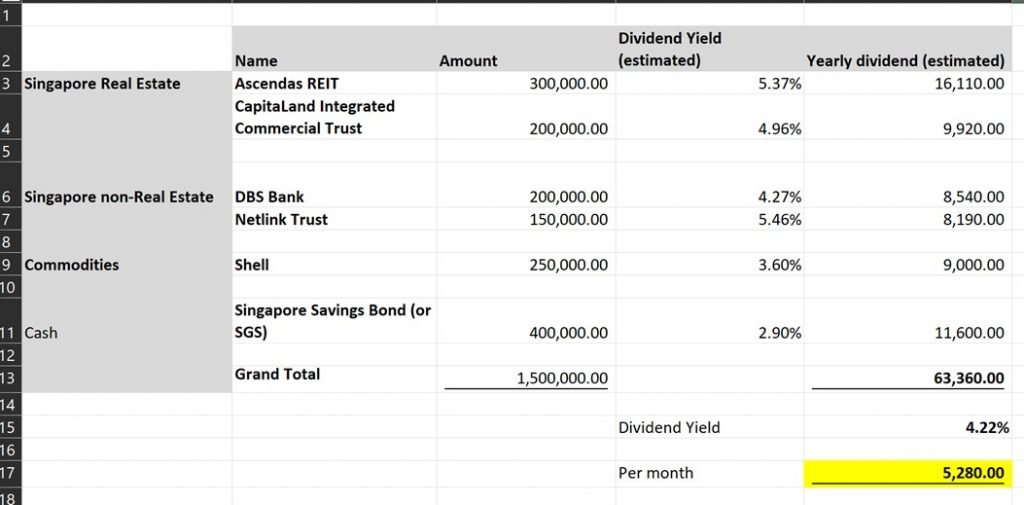

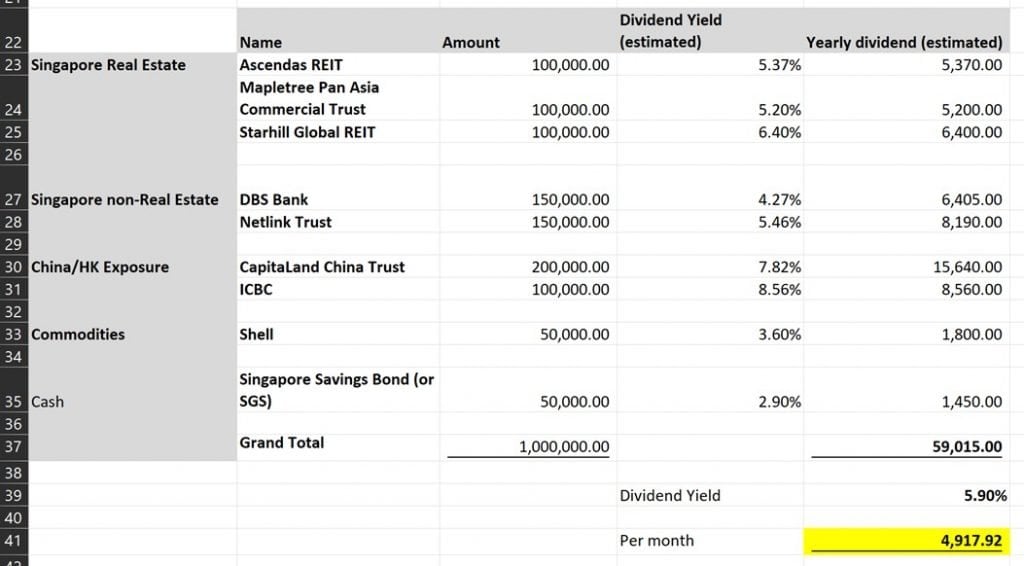

$1.5 million portfolio at 4.22% dividend yield ($5,280 a month)

I actually liked this 4.22% yielding portfolio a lot more.

Most of the names in here are blue chips and quite low risk – stuff like Ascendas REIT, CICT, DBS, Netlink etc.

Sure there’s some risk of a dividend cut if we get a bad recession, but dividends should resume eventually.

At the same time, the $400,000 allocation to cash provides a nice liquidity buffer and allows you to invest into any market crash.

While the $250,000 allocation to oil allows you to hedge inflation in the event inflation stays sticky.

Problems with this 4.22% dividend yield portfolio – Capital Gains potential not high?

The problem though, is that because this was intended to be a dividend yield portfolio, the capital gains potential is not very high.

I suppose the solution is to put some allocation into tech stocks or growth stocks for the capital gains.

But you will sacrifice some of the dividends though.

Capital gains are always tricky for retirement portfolios, because you can’t live off paper gains unless you actually sell your stocks.

And deciding when and what stocks to sell, becomes a form of market timing – not easy to get right.

If one is comfortable with market timing, I thought the better solution might be to play around with the $400,000 cash allocation.

You keep it in cash, until a market crash comes, and they you buy stuff on the cheap to juice returns.

BTW – we share commentary on Singapore Investments every week, so do join our Telegram Channel (or Telegram Group), Facebook and Instagram to stay up to date!

I also share great nuggets of wisdom on Twitter.

Don’t forget to sign up for our free weekly newsletter too!

[mc4wp_form id=”173″]

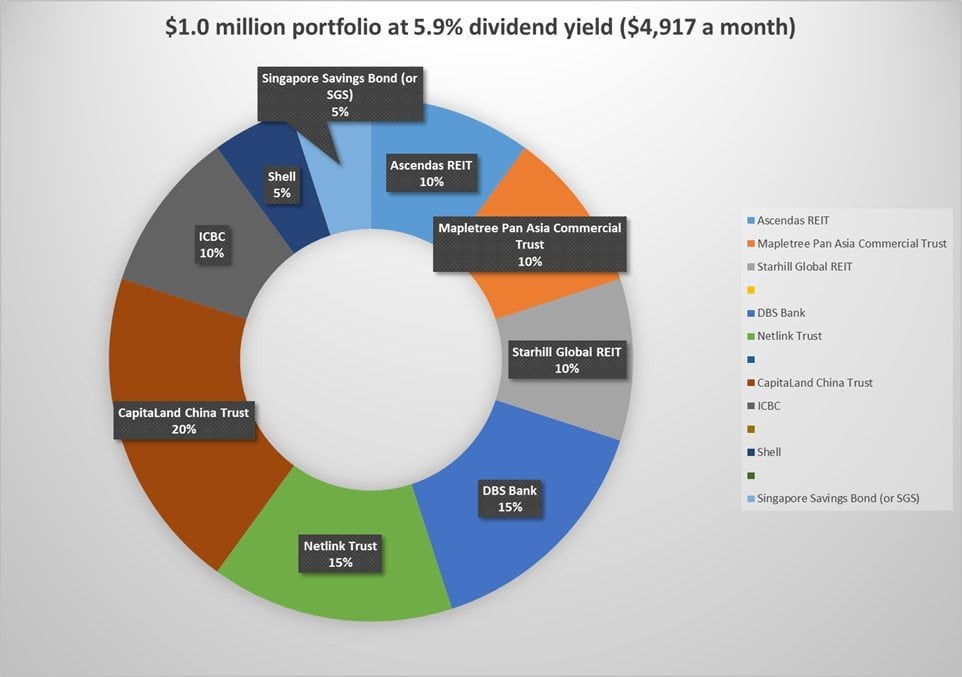

$1.0 million portfolio at 5.9% dividend yield ($4,917 a month)

For the record – I would not be comfortable running a dividend portfolio like this.

Especially not into retirement.

I just think this portfolio takes on too much risk to hit the 6% yield target – in the form of China exposure, and interest rate risk.

If China heads south, or if interest rates stay elevated for longer, there’s a real risk of capital loss for this portfolio.

Any solution to this?

I think any investor willing to run a portfolio like this, needs to have a risk management system in place.

You need to have a system that allows you to cut losses and close off positions when the situation turns against you.

At least that’s what I would do, if I were running a higher risk portfolio like this.

If you want to go pure passive with a portfolio like this, you could suffer big capital losses if things don’t play out as you expect.

Sidenote: Refinancing tool

With rapidly rising interest rates – it might pay off to look into refinancing if your loan is coming due.

I know a lot of you have been writing in for my views on fixed vs floating loans, and I plan to write a full article for this.

I think it ultimately comes down to whether you think the Feds are going to cut rates in 2023, and your personal risk appetite.

In the meantime, there’s a by Property Guru.

Do give it a try if you’re close to refinancing.

It’s completely free – you just input your mortgage details, and the tool lets you know whether you’ll save money by refinancing.

If the answer is yes, they’ll give you recommendations on what loan to take.

If the answer is no, you can set up a reminder for the tool to remind you when its time to refinance.

Do give it a try .

What is the key lesson I learned building these 3 Passive Dividend Income portfolios?

Building these 3 portfolios was very helpful for me in clearing my thoughts.

3 key takeaways for me:

- Estimating how much you need each month is not easy

- Deciding the level of risk you are prepared to take is not easy

- Do you even want to FIRE?

Estimating how much you need each month is not easy

Mr Tan estimated that he needs $5,000 a month to live off, for the rest of his life.

This was “calculated based on potential expenses such as mortgage for a Built-To-Order (BTO) flat and daily expenses for food, transport and utilities”.

But Mr Tan is 27 years old.

Trying to estimate how much you need to live off for the rest of your life, when you are 27 years old, is to me a fool’s errand.

There are 2 big problems that could throw a spanner in your estimations:

- Major Life Events

- Inflation

Major Life Events

There’s a reason why financial advisors always ask if (1) you are married, and (2) whether you have kids.

These are the 2 biggest life events, that can completely change your outlook on life, and change how you view money.

If you don’t plan on getting married or having kids, then yeah estimating how much you need is a lot easier.

If you do, you probably want to account for the fact that these events may fundamentally change your life goals.

And how much you need each month.

You may be okay with $5,000 a month, but what about your spouse? What if you want to give your kids a higher standard of living?

Inflation

You may think that you can survive off $5,000 a month, for the next 50 years.

But you are making that decision when your Bak Chor Mee costs $4 a bowl, and your BTO costs $500,000.

What if 20 years later, the Bak Chor Mee now costs $15 a bowl, and your BTO costs $2,000,000?

It’s an extreme example, but you get my point.

If I am right, we may be moving into a period of structural inflation this decade.

And there’s nothing that strikes fear into a retiree’s heart more than inflation.

The cost of living goes up, but your dividend income may not increase proportionately.

Deciding the level of risk you are prepared to take is not easy

The way I see it, the jump in level of risk + level of sophistication required to manage each portfolio jumps drastically from 2.5% to 4% to 6%.

To investors who are slightly newer to financial markets, it’s not easy to convey the subtle changes in risk at each level.

On the surface it looks like you’re getting a free lunch with a higher dividend yield, but when things head south (and trust me it will eventually), the risk profile of each portfolio is very different.

So it’s probably wise to take a cold hard look at your level of investing competency.

If you are not so familiar with markets, don’t try to run a 5-6% dividend yield portfolio into retirement.

It may look “passive income”, but nothing could be further from the truth.

Investment risks are very real.

Do you even want to FIRE?

Another line in the article stood out for me

Many of those who spoke to CNA argued for a more nuanced understanding of FIRE. The goal is rarely about stopping work entirely, but rather, about simply having that option.

Investment Moats’ Mr Ng noted that many people actually want to “build a sum of money that will give them options in order to give them security”, rather than quit working forever.

“Because what helps them achieve FIRE is that they are very productive people. So their brains cannot rest. Eventually they will need to do some work. It is whether they get paid. That’s where the optionality and security comes in; that is what everyone is looking for, not looking to quit,” he said.

…

And while the married couple Mr Chan and Ms Purushothaman might believe in financial independence, retirement is “optional”.

“For us, what financial independence really means is one word: Options. Options to pursue what we are passionate about and to do that without any financial constraints,” said Ms Purushothaman.

“When we’ve got that aspect covered now, what we’re passionate about could be continuing to work to develop our career aspirations. It could be taking a pay cut to do work that’s interesting or what we’re passionate about, to do volunteer work, or even to stop working to be with our family. Really, the sky’s the limit.”

…

Mr Loo is vocal about his support for the “FI” portion of FIRE, but “really disagrees” with the “RE” portion. The latter is “a huge taboo” to him.

“I’m a strong advocate that people should never retire. People say, ‘I want to retire early so that I can travel.’ Come on, how much can you travel? As a financial educator, I teach you how to become rich so that you can now pursue your passion for the rest of your life. Not so you can relax,” he said.

“In my case, I like to be an entrepreneur, but it involves a lot of risk. If I did not have those foundation layers below, I wouldn’t dare to be an entrepreneur; I have kids and loans to pay at that point in time. But because I had those layers, I dare to pursue those passions.”

Investing is hard… think about why you want to FIRE

Investing is not easy.

Trying to keep up with macro changes, company earnings, and managing your investment portfolio actively can be a full time job.

Creating and managing a portfolio that pays out 4-6% dividend yield year after year, without significant capital losses, is easier said than done.

So it’s probably wise to think about what it is about retiring early that appeals to you.

If you just hate your job, a simpler solution be to find a new job.

As opposed to saving up a couple million, and picking up all the investing skills required to manage an investment portfolio.

So in some ways I really agree with the CNA article – it’s better to view FIRE as an option.

FIRE is good because it gives you optionality – it gives you the freedom and courage to live the life that you want.

But the goal here, should never be FIRE in itself.

The goal, is to the live the life that you want.

How would I do it?

If I wanted to FIRE – I would probably use a 4% yield portfolio.

It’s quite clear for me that the 2.9% yield portfolio is too conservative, while the 6.0% dividend yield portfolio is too aggressive.

The 4% dividend yield strikes the best balance in my view, between dividend income, capital gains, and safety in cash.

I would probably mix in some stocks with capital gains potential though.

In any case, you can see my full personal portfolio with the list of stocks / REITs I am keen to buy on Patreon.

Closing Thoughts: Build in redundancies

One final point I wanted to make, is that if you are trying to build a retirement portfolio like this – it really pays to build in redundancies.

When you’re building a retirement portfolio, it’s literally your quality of life you’re playing around with.

So many things can go wrong when you are predicting for the next 30 years (or more).

Inflation could change the cost of living.

A big change in your life situation can change how much money you need.

A poor investment decision can wipe out a big chunk of your investment portfolio.

If you think you can retire off $5,000 a month, try to aim for a portfolio that can pay $7,000 a month.

So that when something goes wrong (and it probably will), at least you have some buffer in place.

Refinancing tool

With rapidly rising interest rates – it might pay off to look into refinancing if your loan is coming due.

I know a lot of you have been writing in for my views on fixed vs floating loans, and I plan to write a full article for this.

I think it ultimately comes down to whether you think the Feds are going to cut rates in 2023, and your personal risk appetite.

In the meantime, there’s a by Property Guru.

Do give it a try if you’re close to refinancing.

It’s completely free – you just input your mortgage details, and the tool lets you know whether you’ll save money by refinancing.

If the answer is yes, they’ll give you recommendations on what loan to take.

If the answer is no, you can set up a reminder for the tool to remind you when its time to refinance.

Do give it a try .

As always, this article is written on 26 Aug 2022 and will not be updated going forward.

If you are keen, my full REIT and stock watchlist (with price targets) is available on Patreon. You can access my full personal portfolio to check out how I am positioned for the coming downturn too.

Looking for a low cost broker to buy US, China or Singapore stocks?

Get 100 USD in Apple Shares with , a zero commission broker.

Get a free stock and commission free trading with .

Get a free stock and commission free trading with .

Special account opening bonus for Saxo Brokers too (drop email to [email protected] for full steps).

Or for competitive FX and commissions.

Looking to buy Bitcoin, Ethereum, or Crypto?

Check out our guide to the best Crypto Exchange here.

Do like and follow our Facebook and Instagram, or join the Telegram Channel. Never miss another post from Financial Horse!

Looking for a comprehensive guide to investing that covers stocks, REITs, bonds, CPF and asset allocation? Check out the FH Complete Guide to Investing.

Or if you’re a more advanced investor, check out the REITs Investing Masterclass, which goes in-depth into REITs investing – everything from how much REITs to own, which economic conditions to buy REITs, how to pick REITs etc.

Want to learn everything there is to know about stocks? Check out our Stocks Masterclass – learn how to pick growth and dividend stocks, how to position size, when to buy stocks, how to use options to supercharge returns, and more!

All are THE best quality investment courses available to Singapore investors out there!

FYI – We just launched the FH Property Series. Everything you need to know to buy a property in Singapore, completely free of charge.

Why not have a 4% dividend yield portfolio with 1.5mil and the remaining 900k in growth stocks or other assets with greater capital appreciation potential? This exposes him to potential upside, but yet gives him the passive income needed to feel financially independent. At age 40, he could choose to slow down his career or totally quit his job. If life should change and he chooses to continue to working, he can then just roll and reinvest the dividend income.

Realistically to get to that pool of capital by age 40 would require some allocation to growth. The luck of inheritance or being in a lucrative field aside. So that would definitely be some inertia in suddenly tilting the portfolio to a pure dividend one in one sudden move. Best to slowly adjust to allocation over time to tilt more towards income as he ages.

That’s a good idea actually. The more I think about it, the more I realise this is similar to the portfolio I am currently running – mix of the 4% yield portfolio and a capital gains portfolio.

I agree that saving the 2.4 million by 40 is not an easy ask. It’s definitely possible, but for someone who can do it, it just feels like he should probably aim a bit higher than just trying to retire by 40. He could I dunno, focus on trying to improve the world and help others or something. Otherwise, waiting till 40 to start living that phase of his life just seems like a waste.

Interesting read and insightful. But could there be another angle to this consideration? Perhaps his property (BTO flat) will appreciate in value to reach perhaps one million and above? That would give him another ‘option’ to realise some gains to be put into his war chest.

As the host put it very well, life situation may change, and so does the protaganist’s aspirations. Somewhere along the line he may want to upgrade to a private property and use the proceeds of his sale of BTO to purchase a private property. Then I suppose the well laid plans will need to be withdrawn. With property prices n rents going up like crazy, who’s to say it’s a bad move?

That’s interesting. But to realise the gains he needs to sell the BTO, and where would he stay?

Agree that life situation changes over time. At 27, it is not easy to forecast how the rest of your life may play out. Heck, even a 40 year old married with 2 kids may suddenly have a mid life crisis and decide he wants a different lifestyle!

I believe what “Mr Tan” is trying to achieve (which is pretty much common knowledge amongst the ERE/MMM FIRE community) is to spend less than what the portfolio is actually generating, to let the difference cover for inflation. (Now that inflation is so high, of course it is different, but no one has a proper solution for this anyways. Besides reducing spending)

TLDR; “Mr Tan’s” line of (conservative) thought is most probably along the line of having a portfolio say, generate 6% CAGR returns, only spend 2.5% CAGR.

That’s a really good point actually, thanks for pointing this out! Agree that this actually makes a lot of sense.

Just want to point out those China stocks listed in HKSE are subject to 10% tax, so an 8% stocks will not gives you $8k p/a, do check with your stocks borker before you “all in” :p

My bad, should have factored this into the calculations. Thanks for raising this!

If he is single at 27, the ssb max allocation is only $200k. Unless he is doing it as a couple.

Sorry probably should have clarified in the article that the SSB allocation can be spread around a mix of CPF, SSB, SGS, T-Bills, money market funds etc – whatever gives the highest yield, at the level of liquidity required!

FH,

Just a fast one, pretty straight forward answer. In Singapore, you can’t ignore property investment n rental income, if you want a decent size passive income. $2m can get you 2 condo (without loan) with potential income up to $7k or $8k per month. You also solve the problem of capital appreciation over time for the 2 property. Left with $400k is his emergency cash, maybe half into SSB. Rental income has alway been a good source of passive income.

Above advice is only for entertainment only.

The guy wants to buy a BTO though. If he then buys 2 condos worth 2m on top of that he’s looking at about $400k in ABSD, which really kills the future returns. If he gets creative with ABSD, he could probably buy another in the spouse’s name, but 2 might be a bit of a stretch.

But agree that if he can find a way around ABSD, could be a good solution.

A Patron raised the idea of industrial properties, which allows you to take up a higher LTV and avoids ABSD. But industrial properties are more tricky to execute, require a more sophisticated investor in terms of picking the right properties. But could work if done well.

Think the biggest problem with FIRE and its popularity is what it says about our work conditions. Young people are taken with FIRE cuz they don’t like work conditions, plain and simple. So if FIRE math makes it possible for young people to disengage from burnout and do something they really like, all the better.

Totally took profits off bear market rally. Now 60% in cash. I’ve studied the market conditions and think it is time to wait out the bear market. Only two problems:

1. Putting 60% cash in SSB makes it less agile for deployment (1 month to redeem). Putting it into REITs is slightly better for yield and liquidity, but REIT spreads will tighten with relentless Fed hikes, suggesting possible REIT price downside.

2. When to deploy? Market timing involves two right decisions: when to sell and when to buy back. I’ve usually done the first well, based on rebalancing, technicals and momentum. The 2nd decision is arguably harder, as it is fiercely contrarian. Any ideas?

Yeah, I agree with the point about Fire.

Some quick thoughts from me:

1. Could put some in high yield savings account. Sure, the yield is lower, but the liquidity is important to me, and worth paying for in my view.

2. When the Feds pivot would be the short answer, or at least when it becomes obvious the Feds will pivot. Anything before that – too tough to call a bottom.

When exactly that will happen I have no clue.

That said – if you want to trade, there are probably going to be many opportunities to trade on the way down. You can long or short, there are many opportunities across all asset classes with the current volatility!