So I received this really interesting question from a reader:

Hi FH,

Am turning 55 years old next year. Am single with no one financially dependent on me.

I plan to move out from my current stressful IT job in the next 2-3 years to an easier job that I think could provide me with $3k monthly in the next 2-3 years.

Objective is to have a retirement monthly income of 8k from my total investment in 5 years’ time. Is it possible? How to structure and shift my portfolio which is primarily 100% stocks to a lower risk portfolio that can provide a more stable regular income?

My current assets:

1) Property: Have a private property (fully paid).

2) CPF: Have maxed out my MA. Has $500k in OA and $350k in SA. SRS $250k of which majority in SG stocks and $100k annuity that gives a monthly payout $800 from 65yr onwards

3) Stocks (Cash):SG stocks $250k (70% Reit, 20% Banks, 10% Others), US stocks $280k (50% with a fund); CN/HK ETF $30k; Unit Trust $150k

4) No bonds though I just started to RSP into PIMCO Income Fund ~$5k

5) Cash: SSB $200k (have max out). $650k cash from joint properties divested due to demise of a friend and am thinking to deploy it back to property investment (which means am subjected to ABSD).

Not good in investment and don’t intend to spend lots of my time monitoring, so need a portfolio that is passive investing for me.

Am thinking if I should use the cash and OA to invest in a passive stock/bond/ETF portfolio or an investment ppty as it is more passive from rental income which I anticipate a rental income of $2.5k, no need to monitor like stocks. What is your thoughts?

Fyi.. it is difficult to get advice from financial adviser as most of them ends up asking me to buy annuity policies from them. Would like to hear your thoughts if any on use of independent financial adviser too.

Will be great to hear your thoughts.

How to get $8000 a month passive dividend income – Buy Stocks, REITs, T-Bills?

Very interesting question – so let’s get right into it!

For obvious reasons, I have tweaked some details to protect the privacy of the reader, so any resemblance with anyone you know is purely coincidental.

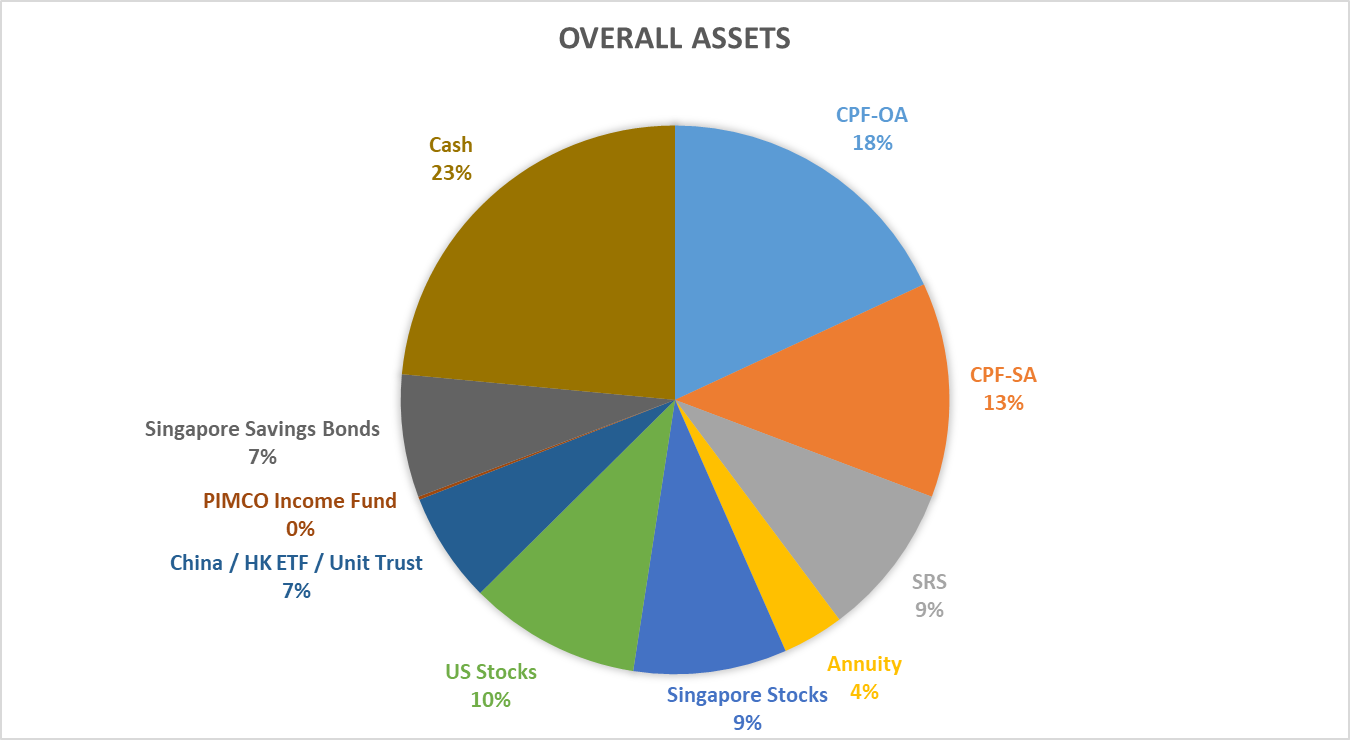

What are the assets that this investor has?

Let’s summarise the assets the reader has:

1) Property: Have a private property (fully paid).

2) CPF: Have maxed out my MA. Has $500k in OA and $350k in SA. SRS $250 of which majority in SG stocks and $100k annuity that gives a monthly payout $800 from 65yr onwards

3) Stocks (Cash):SG stocks $250k (70% Reit, 20% Banks, 10% Others), US stocks $280k (50% with a fund); CN/HK ETF $30k; Unit Trust $150k

4) No bonds though I just started to RSP into PIMCO Income Fund ~$5k

5) Cash: SSB $200k (have max out). $650k cash from joint properties divested due to demise of a friend and am thinking to deploy it back to property investment (which means am subjected to ABSD).

I did a simple pie chart to summarise, and this is what the asset allocation looks like.

What is the dividend yield on this portfolio?

I assumed a fairly reasonable (in my view) dividend yield of:

- 2.5% for cash (still very achievable today)

- 3.0% for Singapore Savings Bonds (assume this was locked in during the 2023/2024 period

- 5.0% yield for Singapore stocks

With the reader’s current portfolio size of $2.7 million.

You know what – without any big changes to current asset allocation.

You’re probably looking at $7,000 a month in passive dividend income.

Not too shabby really – and very close to the $8,000 a month target.

| Asset Class | Amount | Interest / Dividend | Per Year |

| CPF-OA | 500,000.00 | 2.50% | 12,500.00 |

| CPF-SA | 350,000.00 | 4.00% | 14,000.00 |

| SRS | 250,000.00 | 5.00% | 12,500.00 |

| Annuity | 100,000.00 | – | 9,600.00 |

| Singapore Stocks | 250,000.00 | 5.00% | 12,500.00 |

| US Stocks | 280,000.00 | 0.00% | – |

| China / HK ETF / Unit Trust | 180,000.00 | 5.00% | 9,000.00 |

| PIMCO Income Fund | 5,000.00 | 5.00% | 250.00 |

| Singapore Savings Bonds | 200,000.00 | 3.00% | 6,000.00 |

| Cash | 650,000.00 | 2.50% | 16,250.00 |

| Total | 2,765,000.00 | 83,800.00 | |

| Per Month | 7,716.67 |

Should the investor invest the $650,000 in an investment property and pay ABSD?

The biggest decision facing the investor today.

Looks to be what to do with the $650,000 cash freed up from selling the investment property.

The investor wants to top up the cash with CPF-OA to buy another investment property.

Let’s crunch some numbers to see if this makes sense.

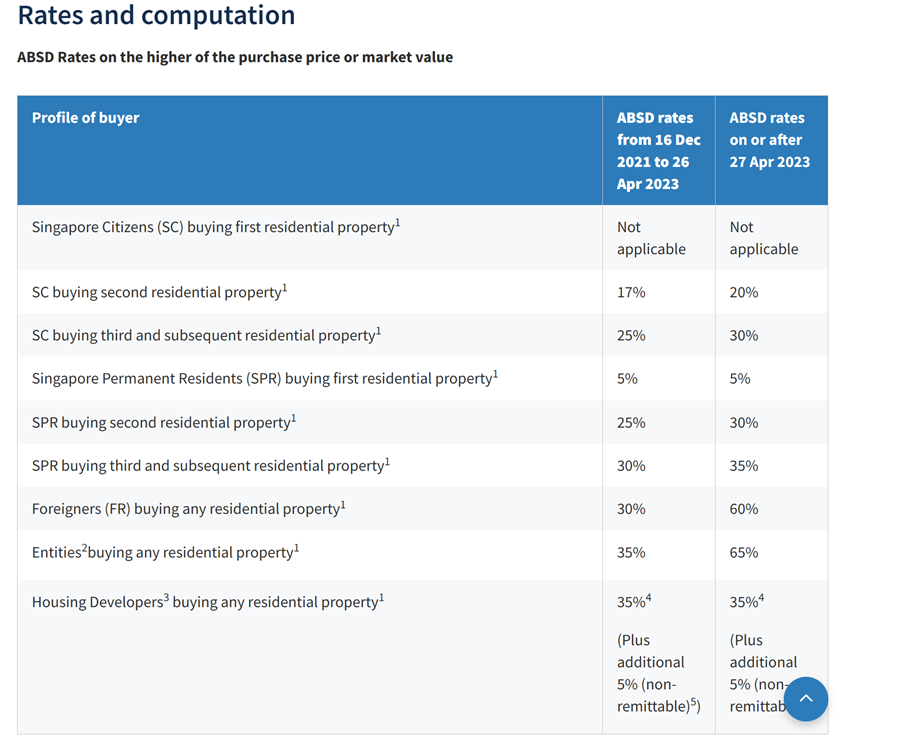

20% ABSD makes it frankly very prohibitive to buy a second property

The investor already has a property, and will pay ABSD on the second property.

ABSD rates below – a whopping 20% for the second property.

Let’s just assume he tops up $350,000 from CPF-OA, and buys a property for around $1 million.

20% ABSD is $200,000.

Let’s say another 5% expenses to cover stamp duty, lawyer fee, renovation costs, agent fees, maintenance etc.

With a $1 million cash amount, realistically you’re only buying a property at about $750,000.

Latest gross rental yield in Singapore is about 3.4%.

That works out to $25,500 a year gross rental, or about $2125 a month in gross rental.

For a $1 million investment.

That’s a miserable 2.55% gross yield.

Not much higher than the latest T-Bill yield.

What if you invest that $1 million in a mix of cash and REITs instead?

In the alternative, let’s just say you split it simplistically into 60% REITs, 40% cash.

That works out to a $43,000 a year dividend income, or $3580 a month.

| Cash | 400,000.00 | 2.50% | 10,000.00 |

| REITs | 600,000.00 | 5.50% | 33,000.00 |

Even if we switch to something more conservative and invest 60% in risk free Singapore government bonds.

That’s still $37,000 a year dividend income, or $3083 a month.

| Cash | 600,000.00 | 2.50% | 15,000.00 |

| REITs | 400,000.00 | 5.50% | 22,000.00 |

Both offer significantly higher yields, even with a very healthy allocation to cash to tide through any stock market volatility.

My Personal View here? Buy property or stocks/REITs?

My personal view here.

I just don’t see Singapore property as a great investment opportunity if you have to pay ABSD.

That 20% really wipes out a huge chunk of investment returns.

You’re effectively down 20% right from the get go – and you need very solid investment returns to make up for that.

And given where Singapore property prices are trading today (not cheap), and given all the additional transaction costs with real estate (buyer stamp duty, lawyer fee etc).

I don’t see it as an amazing investment for this investor.

If the goal were wealth preservation / store of value then sure the answer would be completely different.

But as a way to generate passive dividend income, I find it hard to justify buying a second property and immediately losing 23% of your investment sum on day 1 (ABSD and buyer stamp duty).

How to get $8000 a month passive dividend income – Buy Stocks, REITs, T-Bills?

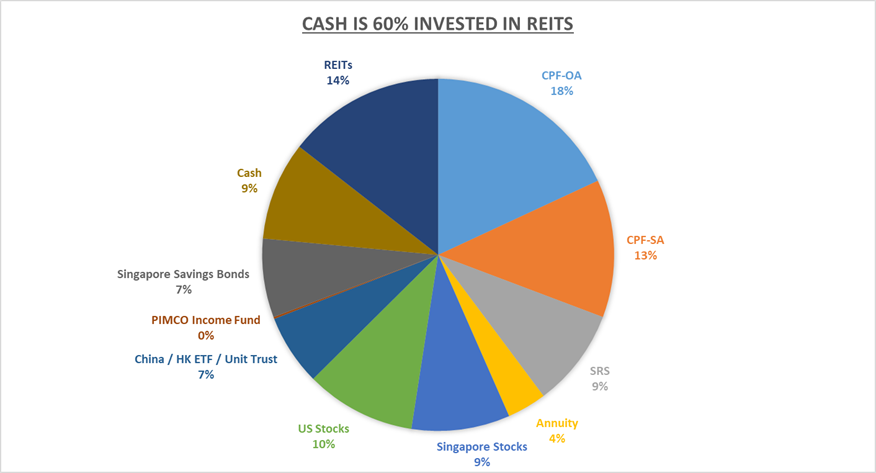

Let’s assume that instead of buying a second property.

We take 60% of that $650,000 and buy a broadly diversified REIT portfolio.

You know what – that simple tweak alone brings the portfolio up to $7983 a month in passive dividend income.

With a very minimal switch, and largely preserving the rest of the portfolio mix in CPF-OA, US stocks, China stocks, Singapore Savings Bonds etc.

| Cash is 60% invested in REITs | |||

| Asset Class | Amount | Interest / Dividend | Per Year |

| CPF-OA | 500,000.00 | 2.50% | 12,500.00 |

| CPF-SA | 350,000.00 | 4.00% | 14,000.00 |

| SRS | 250,000.00 | 5.00% | 12,500.00 |

| Annuity | 100,000.00 | – | 9,600.00 |

| Singapore Stocks | 250,000.00 | 5.00% | 12,500.00 |

| US Stocks | 280,000.00 | 0.00% | – |

| China / HK ETF / Unit Trust | 180,000.00 | 5.00% | 9,000.00 |

| PIMCO Income Fund | 5,000.00 | 5.00% | 250.00 |

| Singapore Savings Bonds | 200,000.00 | 3.00% | 6,000.00 |

| Cash | 250,000.00 | 2.50% | 6,250.00 |

| REITs | 400,000.00 | 5.50% | 22,000.00 |

| Total | 2,765,000.00 | 95,800.00 | |

| Per Month | 8,716.67 | ||

What is the key risk with this dividend portfolio?

The biggest risk with this portfolio?

I would say that for an investor who admits that he is “Not good in investment and don’t intend to spend lots of my time monitoring, so need a portfolio that is passive investing for me.”

The portfolio above is a very broad mix of assets, that does require constant effort and monitoring.

I mean I don’t have the exact breakdown of the portfolio, but the portions invested in SRS, Singapore Stocks, US Stocks, China, don’t exactly strike me as a completely hands off portfolio.

So yes I think the current portfolio with a minor tweak to invest the cash in REITs will achieve the target monthly payout.

But it may require some active monitoring on the part of the investor.

Follow Financial Horse to avoid missing any post!

Free weekly newsletter:

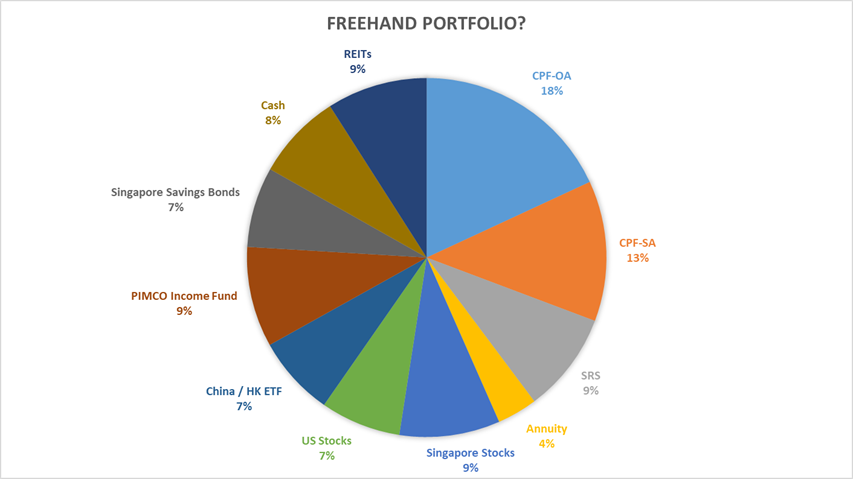

How I would do it? If this were me?

Which got me thinking.

If this were me, and I had a completely freehand to shift the portfolio around?

How would I do it?

I eventually came up with something like that below:

| Freehand Portfolio? | |||

| Asset Class | Amount | Interest / Dividend | Per Year |

| CPF-OA | 500,000.00 | 2.50% | 12,500.00 |

| CPF-SA | 350,000.00 | 4.00% | 14,000.00 |

| SRS | 250,000.00 | 5.00% | 12,500.00 |

| Annuity | 100,000.00 | – | 9,600.00 |

| Singapore Stocks | 250,000.00 | 5.00% | 12,500.00 |

| US Stocks | 200,000.00 | 0.00% | – |

| China / HK ETF | 200,000.00 | 5.00% | 10,000.00 |

| PIMCO Income Fund (or other bond fund) | 250,000.00 | 5.00% | 12,500.00 |

| Singapore Savings Bonds | 200,000.00 | 3.00% | 6,000.00 |

| Cash | 215,000.00 | 2.50% | 5,375.00 |

| REITs | 250,000.00 | 5.50% | 13,750.00 |

| Total | 2,765,000.00 | 99,925.00 | |

| Per Month | 9,060.42 |

Thought Process? Behind the passive dividend income portfolio?

You can see that almost 46% of the portfolio (or $1.265 million) is invested in a mix of CPF, Singapore Savings Bonds, and Cash, so the portfolio continues to be relatively low risk.

And for the stocks / REITs component, frankly I would just buy a broadly diversified ETF.

Something like Lion Phillip S-REIT ETF or Nikko AM Asia REIT ETF for REITs.

S&P500 for US stocks.

MSCI China or Hang Seng Tech for China.

You get the idea.

You’re just looking to buy broad exposure, that you would be comfortable with if you were completely unable to touch your portfolio for the next 10 years.

The tricky one is Singapore stocks.

The closest proxy is STI ETF, but with the STI ETF there is a fair bit of overlap with the REIT portfolio.

Alternatively you could just buy the 3 Singapore banks and call it a day.

No right or wrong here, and frankly I might tilt towards the latter.

Buy a broad REIT ETF, buy the 3 local banks in equal size, and maybe throw in one or two other high paying Singapore dividend stocks for good order.

Are REITs still a good buy in 2025?

I get a lot of questions on whether REITs are still a good buy in 2025.

I recall reading a bank analyst report recently recommending investors underweight banks and overweight REITs.

Thesis being that with slower US economic growth, risk for interest rates is tilted to the downside – which is good for REITs and bank for banks.

Which coincidentally, was exactly my train of thought – until I saw that bank report which led me to question maybe I wasn’t actually that smart after all (if even banks are writing about it, surely that is priced in right?).

So yes gun to my head I would prefer REITs over banks today for the reason above.

But if investing has taught me anything, it is to have a view, express it, and then prepare for the possibility that you are 100% wrong.

So a portfolio broadly split between banks on the one hand, and REITs on the other, could be a decent way to hedge this.

You can see my full portfolio breakdown, and the REITs / Stocks I am keen to buy, on FH Premium.

What about investment grade bonds?

In this new paradigm of higher interest rates.

I actually really like bonds as well.

You can get about 5% yield on a broadly diversified portfolio of investment grade bonds, hedged back to SGD.

Of course, this is not risk free as risk free yield is 2.5%, so anything higher and you need to take on risk.

But as a portfolio diversifier, while still generating good yield – I really like bonds as an alternative.

PIMCO GIS Income fund which the investor bought is one such option, and I did a more detailed review on this fund here.

Thoughts on use of independent financial adviser?

There was also a question on the use of independent financial adviser.

I’m not here to break anyone’s ricebowl, so don’t worry.

What I would say, is that with all investment advice – never forget that the final decision maker is you.

Only you can decide what is the right decision for your situation.

So with that in mind, I don’t see any harm in sourcing for views from anyone willing to give you a view – as long as you apply an independent judgment into deciding whether it makes sense.

Who knows, maybe such an adviser may be able to think of novel points that you didn’t previous consider yourself?

Closing Thoughts: What if I want a bit more upside / juice?

And of course, this being Financial Horse.

What if we want the portfolio to have a bit more oomph, a bit more upside?

Then boy – the world is your oyster.

US Tech, Crypto, China are all interesting to me after the recent sell-off.

I’ve been sharing my views on that actively on FH Premium, and you can see what I’ve been buying (or selling) on FH Premium.

But this is definitely into the realm of higher risk investing, and not for everyone

Love to hear what you think!

What would you do differently?

This post is written on 21 March 2025 and will not be updated going forward. My latest views on markets, my Stock watchlist and full Personal Portfolio, are shared on FH Premium.

Hi FH,

Two points I wish to make here.

1. The reader said:

“SRS $250 of which majority in SG stocks and $100k annuity that gives a monthly payout $800 from 65yr onwards”

I thought the reader meant that he has $250k in SRS which is invested majority in SG stocks and in a $100k annuity. But you seem to interpret it as he has $250k in SRS invested majority in SG stocks and another annuity in hand worth $100K.

2. The column headline of your tables shown should be “Per Year” instead of “Per month” for all the asset classes shown, except for the annuity asset class.

Thanks GH, my replies below:

1. My bad on the annuity numbers and the per month – I have updated the tables.

2. Actually you are right – my interpretation may be wrong. If so then the numbers need to be adjusted accordingly. The 100k SRS works out to $400 a month in dividends, so the numbers should be adjusted to that amount.

Hi, I am interested in know how you came up with 5% annual returns for categories like SRS, Singapore stocks and China ETFs, etc? Is this 5% from capital gains? Or dividend? I think it’s very optimistic to assume 5% yearly consecutively is achievable? As these are equities after all, there’s no guaranteed your investment won’t go the other way. The reader also said he is turning 55 which means CPF SA will be gone.

If you buy blue chips like DBS, UOB, OCBC, Singtel, Keppel etc – dividend yield is about 5% today. That’s where I got the number from. But I do agree that returns are not smooth, and there will be down years.

Hi FH,

I am interested in know how you cane up to 5% annual returns for investments like SRS, Singapore stocks and China ETFs? Is this 5% from capital gains? Or dividend? As these are equities after all, there’s no guaranteed your investment here do no go the other way. The reader also said he is turning 55 which means CPF SA will be gone.

I think there are fee only advisors like providend. Have not used them before though.. Anyone use them before and able to comment?

Not tried personally as well.

Sorry I just came across this which is 6mths old now but I was interested to know the impact of CPF life premiums on the portfolio. The aim is to retire in about 5 years time, and the investor turns 55 next year. So in 2026 a decision has to be made on BRS, FRS or ERS. That will affect the balance of the CPF account and the interest that can withdrawn. Also SA is closed at 55 years old so the 4% on SA is not valid. CPF Life kicks in at 65 years old but until then the interest that can be withdrawn on CPF OA balance will need to be net off the premium for CPF Life depending on the scheme chosen (BRS, FRS, or ERS). The analysis does not take into account the lifestage of the investor – turning 55 and when retirement happens are crucial details.