I was actually planning to write a piece on the commodities market and how to invest in commodities.

But then a lot of stuff started happening in the macro world and in financial markets last week.

So… commodities will have to wait.

Let’s talk macro.

Interest Rates are approaching the end game

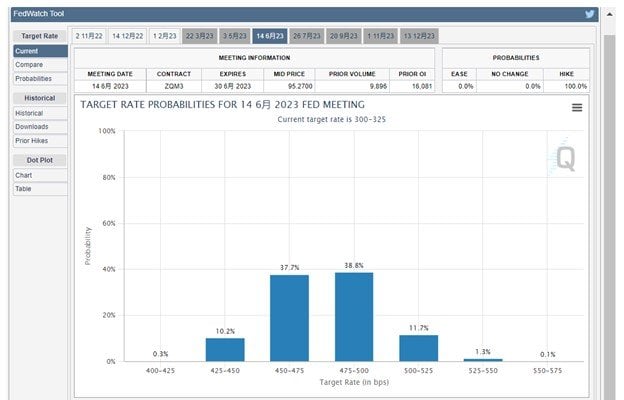

Remember how previously I said that I think cycle peak for Fed Funds Rate would be 5%, with possible overshoot to 5%+?

Well, after the latest Fed meeting and revised dot plot – futures are now pricing in a terminal rate of 4.75% – 5.0% by June 2023.

There’s probably room to go slightly higher, especially if inflation stays sticky.

But no denying that futures markets at least, are starting to price in the interest rate end game I’ve been talking about.

Treasuries are starting to wake up to this new reality.

The US 2 year trades at 4.2%, and the 10 year broke 3.7% last week.

Real interest rates (inflation adjusted interest rates) have shot up as well – going from deep negative the start of the year, to almost 1.5% today.

I extracted the 15 year chart below just to put this in reference.

Look at the rapid rise in real rates the past 12 months, and compare that with the rise in real rates from 2005 – 2007.

The Feds have done more tightening (to real rates) in the past 12 months than the entire 2005 – 2007 cycle.

You can argue that it’s because we were so deep negative in 2020 – 2021, and that’s probably true, but the pace of change is still astounding.

Commodities pricing in a recession

With a 5.0% terminal interest rate this cycle, the market is (rightly) becoming very pessimistic about the chance of a soft landing here.

Again, it’s not impossible, it’s just that it probably wouldn’t be my base case.

Commodities are pricing in this global slowdown and possible recession as well, with commodity prices coming down quite a bit the past month:

I’ve been talking about how the months/years ahead may see:

- Asian Financial Crisis 2.0

- Sovereign debt crisis

Let’s talk about each of them.

Asian FX looking like 1997

When I talk about Asian Financial Crisis 2.0, I mean it in the context of weakening Asian currencies.

Most of the big Asian economies are big exporters of goods, and importers of commodities and energy.

When the currency of one country weakens, their goods become cheaper (and more attractive) to the world. Left alone, this would boost the export competitiveness of said country.

Because of this, once any of the big Asian countries starts to depreciate its currency, the others may eventually have to follow.

The problem then – is that commodities and energy are priced in USD.

The more you depreciate your currency vs the USD, the more expensive commodities and energy become. Which means higher inflation, which domestically is very unpopular.

So that’s the broad overarching dynamic here, and when the Feds are hiking to 5.0% terminal interest rates, it supercharges the entire dynamic above, not in a good way.

Very few economies in the world will be able to keep up with the Feds on their current hiking path, which means the only way out is to depreciate their currency against the USD.

And that’s what we’re seeing.

Here’s USD/JPY, which is already back at 1997 levels.

The BOJ tried to intervene last week to defend the 145 level on the Yen, but this is a classic case of George Soros vs the Bank of England.

The Japanese can take more pain than the English, but there is only one way out for the Yen here – either the BOJ has to:

- raise interest rates above 0.25% on the 10 year (currently it is pegged), or

- the yen will depreciate more from here

Short term the BOJ may continue to try to defend the Yen, but I think eventually they will be forced to raise interest rates as well.

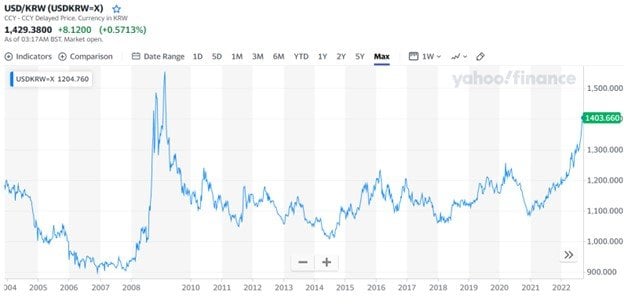

Here’s the Korean Won, rapidly approaching 2008 levels:

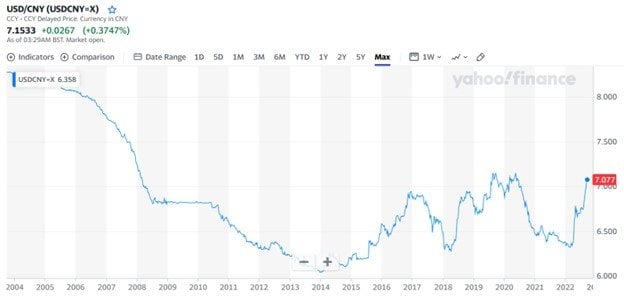

And here’s the Chinese Yuan, which has broken 7.

The Chinese have been keeping the RMB very tight the past year to avoid importing inflation, but even they are being forced to accept RMB depreciation in the face of rapidly tightening USD monetary policy.

Sovereign Debt Crisis

The other big one to keep an eye on, is the sovereign debt crisis.

This has already played out in countries like Sri Lanka, and will spread to more emerging markets before all this is over.

But the big one I want to talk about, is the Eurozone, the second largest economic bloc in the world.

The problem can be summed up like this.

Eurozone, like Asia, is a net commodities and energy importer.

Unfortunately, commodities and energy are priced in USD (or Russian Rubles, but that’s a topic for another day).

Because the Eurozone has stubbornly maintained interest rates at zero while the Feds are hiking 0.75% each time, the Euro has plunged against the USD – driving up the price of commodities when denominated in Euro.

This means higher inflation for the Eurozone.

Now the Europeans are no fools, so they realise they have to raise interest rates as well or the Euro will plunge. Which they have done so.

But there is no way the Europeans can hike to 5.0% to match the US Feds (their debt levels are too high, and economy is not as strong). Realistically, the terminal rate for the EU is probably about 2.75%.

This means they have to accept the euro will not return to where it was against the USD before this – meaning that inflation will stay.

The added complication for Europe is that because of the feud with Russia, energy prices will stay high this winter.

EU Governments will subsidise energy prices… Who will foot the bill?

Inflation is bad for popularity, so the solution for the Eurozone in the short term will be to subsidise energy prices.

There is no way they pay for this with increased tax revenue, which means the only way to pay for this, realistically, is by issuing more debt.

And now you see the problem.

The EU is going to have a huge increase in government debt. At the same time as Eurozone interest rates are going up from negative rates.

How are individual EU governments going to repay all that interest expense you say?

Well, now we’re finally asking the right question.

The market is asking the same questions as well.

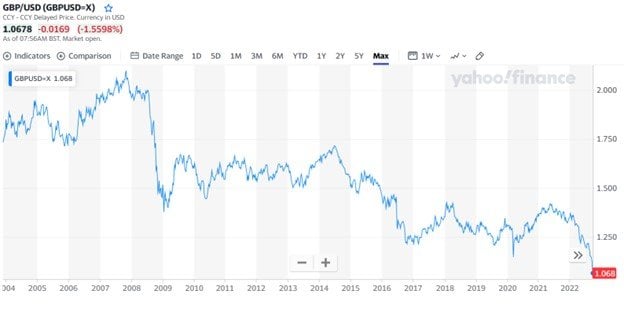

GBP/USD

Here’s the Pound against the USD.

The new government is trying to cut tax rates, while unveiling a big spending package to help consumers.

Where is the money going to come from then?

Market is rightly dumping GBP on the news:

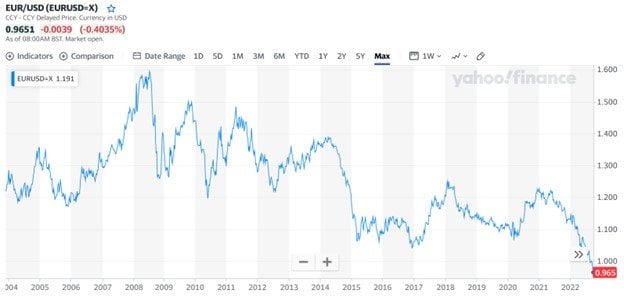

Euro/USD

Similar dynamic for the Euro:

What happens next?

Unfortunately, there are no easy answers here.

Singapore is in a privileged position because MAS has a very strong balance sheet, and our economy is doing well, so we are able to maintain a strong SGD. Our reserves are also strong enough that the government will be able to unleash multiple rounds of “GST Vouchers” and “NS Vouchers” to help alleviate the cost of living.

Very few countries in Asia or Europe boast a similar position.

Much will depend on how long the Feds keep interest rates at 5.0% for.

If we get a market meltdown early next year, and the Feds are forced to cut, maybe we avoid anything too bad.

If inflation stays sticky, the labour market holds up, US financial markets avoid contagion, then the Feds may hold at 5.0% for a while.

In which case the Asian FX and Europe situation may continue to deteriorate.

Stages of a bear market

Broadly, there are 4 stages of a bear market:

- Stage 1 – Market topping out, as savvy investors start to sell

- Stage 2 – Market decline due to drop in valuation multiples (valuations hit, no major earnings impact yet). Damage is limited to financial markets.

- Stage 3 – Real economy starts to slow. Corporate earnings are cut, refinancing risk starts to play out

- Stage 4 – Liquidity event and panic

Stage 1 took place from Nov 2021 to Jan 2022.

Stage 2 is currently playing out, from Jan 2022 till today.

Which leaves Stage 3 and Stage 4.

Before all this is over, the market will need to start pricing in earnings impact in Stage 3.

And we may or may not get a liquidity event in Stage 4.

Market has not priced in earnings impact yet

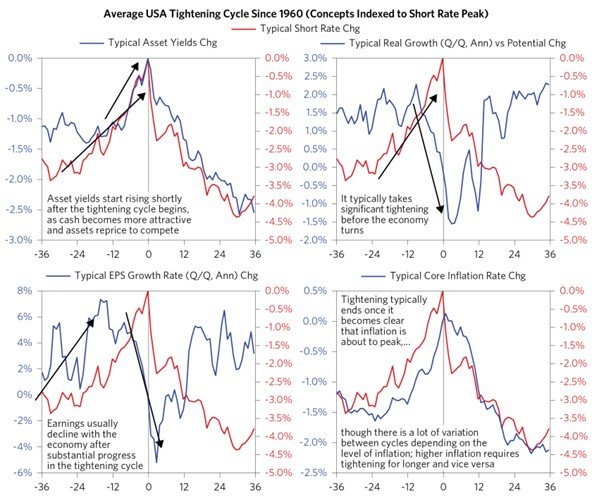

Bridgewater has a good report where they conclude:

Equities are discounting higher interest rates but not the tightening’s impact on growth and earnings or the possibility that even more tightening will be needed to bring inflation down.

It’s a good report and worth reading in full, but I will summarise the gist below.

Broadly, they find that:

- Rising interest rates impact asset valuation multiples very quickly (This is Stage 2, which we saw the past 9 months)

- However, it takes some time for the rising interest rates to impact the real economy, and cause earnings to decline (This will happen in Stage 3 to come)

- Inflation therefore comes down with a lag to the decline in the real economy (Inflation will come down in Stage 3)

- Therefore, the tightening cycle doesn’t end until it is clear that inflation will come down to reasonable levels (Feds will stay tight for longer)

They also find that:

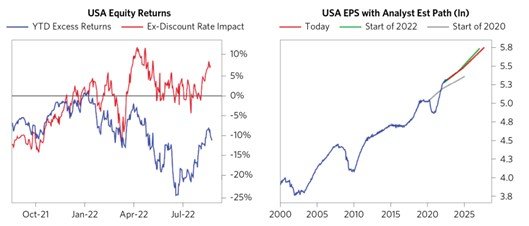

Equities are most vulnerable during the period when earnings decline and there is continued tightening and rising asset yields since inflation isn’t yet fully contained. The table below illustrates this—the combination of rising asset yields and EPS declines are by far the worst periods for equities. In this current cycle, we are still in a transition phase and haven’t yet reached the point where reported earnings or analyst forward EPS expectations have started to come down.

Basically, Bridgewater is trying to say, using my 4 stage framework above, is that:

- We are still in Stage 2 of this bear market, where financial assets are pricing in a decline in valuation multiples due to higher interest rates

- But historically speaking, the bigger declines usually come in Stage 3, where companies earnings are impacted, the same time as interest rates are going up

And Bridgewater reaches a similar conclusion, where we are right now – stocks have not fully factored in the potential drop in earnings to come, only the decline in valuation multiples.

This will not be as quick as March 2020

Now March 2020 was a very special market crash.

The economy went from 100 to 0 because of COVID lockdowns. And the stock market went from 0 to 100 because of supercharged, unlimited Fed liquidity.

So in March 2020, we had a very rapid decline, and a very rapid recovery in risk assets.

This time around, it is playing out more like a classic recession.

Where rising interest rates feed into lower valuations, into slower economic growth and so on.

Think 2008, not 2020.

This will take some time to play out, just as it takes some time for the rising interest rates to impact the real economy.

A usual bear market typically 12 – 18 months, and assuming we started in Jan 2022, we’re about 9 months in.

Of course, there is nothing “usual” about this market given how unprecedented the inflation levels are, how unprecedented the money printing was before this, and how unprecedented the bubble in financial assets was (and still is).

So the starting point is unprecedented, and you may argue the remedy needs to be equally drastic.

In which case a bear market lasting longer than average is a possibility we need to be alive to.

When to start buying?

As shared previously, I start buying when:

- Feds pivot to dovish

- Stocks fall to the point where valuations are attractive from a fundamental perspective

Feds pivot to dovish

This hasn’t happened yet.

It will happen in time of course, as the rising rates slowly suffocate the global economy.

The million dollar question that every investor is asking now is – What is the level of pain required before Jerome Powell changes his mind.

Is it S&P500 at 3000? 2500? 2000?

Or do we need to see financial markets contagion?

This is not an easy question to answer, but in any case, I don’t see a need to frontrun this.

I will wait for their announcement before I buy in this approach.

Stocks fall to the point where valuations are attractive from a fundamental perspective

Based on Bridgewater’s study above, and based on my own numbers, this has not happened yet.

Rough ballpark, we probably need another 20% decline before stocks are fairly priced for this new climate from a fundamentals perspective.

Closing Thoughts

Now I know this reads like a pretty gloomy post, but hey, I’m just telling it as I see it.

There are a lot of points to cover as things are moving very rapidly all around the world.

So I have not been able to cover everything in this article, but I have tried to cover the big points.

If there’s anything I missed out, or anything you want my views on – would love to continue this discussion in the comments below!