Disclaimer: The following post is sponsored by LU Global, all opinions and views expressed in this article are courtesy of Financial Horse.

Probably the biggest thing in South East Asia (and perhaps globally) these days is wealth management. Private wealth management is big because of a confluence of factors: (1) regulatory changes making it harder for banks to make money on traditional lending and trading, forcing them to go into alternative businesses like wealth management, (2) the explosion of wealthy individuals in Asia, and (3) technology radically transforming the investment landscape both in terms of access to information, and access to products.

In recent years, we’ve had roboadvisors like StashAway, fund management platforms like MoneyOwl and EndowUs, and even the banks coming in with things like the DBS and UOB Roboadvisors. This increased competition has been great for investors like us, where we now have a much more diverse range of investment options to choose from.

So I was very excited when some of the mega Chinese players started coming in to the market as well. The latest one in particular, was LU Global, a member of the Ping An group.

Basics: What is LU Global?

From their FAQs:

LU Global is the online wealth management platform operated by Lu International (Singapore) Financial Asset Exchange Pte Ltd (Co. Reg No 201702479G). We are a member of the Ping An Group, as well as a related entity of Shanghai Lujiazui International Financial Asset Exchange Co., Ltd (“Lufax”), which operates China’s leading online wealth management platform Lu.Com

Ping An Group is a massive financial institution in the China market, so I was really excited to see what they could bring to the Singapore market.

How does LU Global work?

The easiest way to think of LU Global is this: It’s an online platform that brings you access to sophisticated investment opportunities. For instance, while you usually only can get access to publicly listed ETFs through roboadvisors, through LU Global, you can get access to private funds. Sounds great right?

Unfortunately, though, there’s a catch. If you’re a Singapore resident, you can only use LU Global if you’re an accredited investor (defined below):

An accredited investor is an individual who meets either of the below criteria:

Net personal assets (a) whose net personal assets exceed in value S$2 million (or its equivalent in a foreign currency). An individual’s primary residence can only account for up to S$1 million of the individual’s net personal assets, or the amount after deducting any credit facility secured by the primary residence, whichever is lower; or

Net financial assets (b) whose financial assets (net of any related liabilities) exceed in value S$1 million (or its equivalent in a foreign currency); or

Net income (c) whose income in the preceding 12 months is not less than S$300,000 (or its equivalent in a foreign currency).

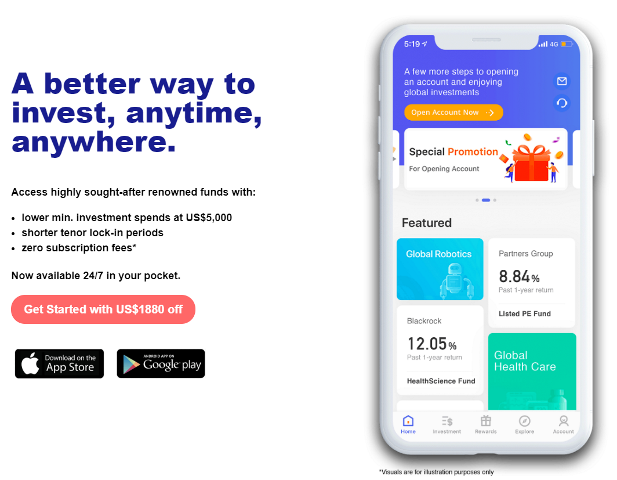

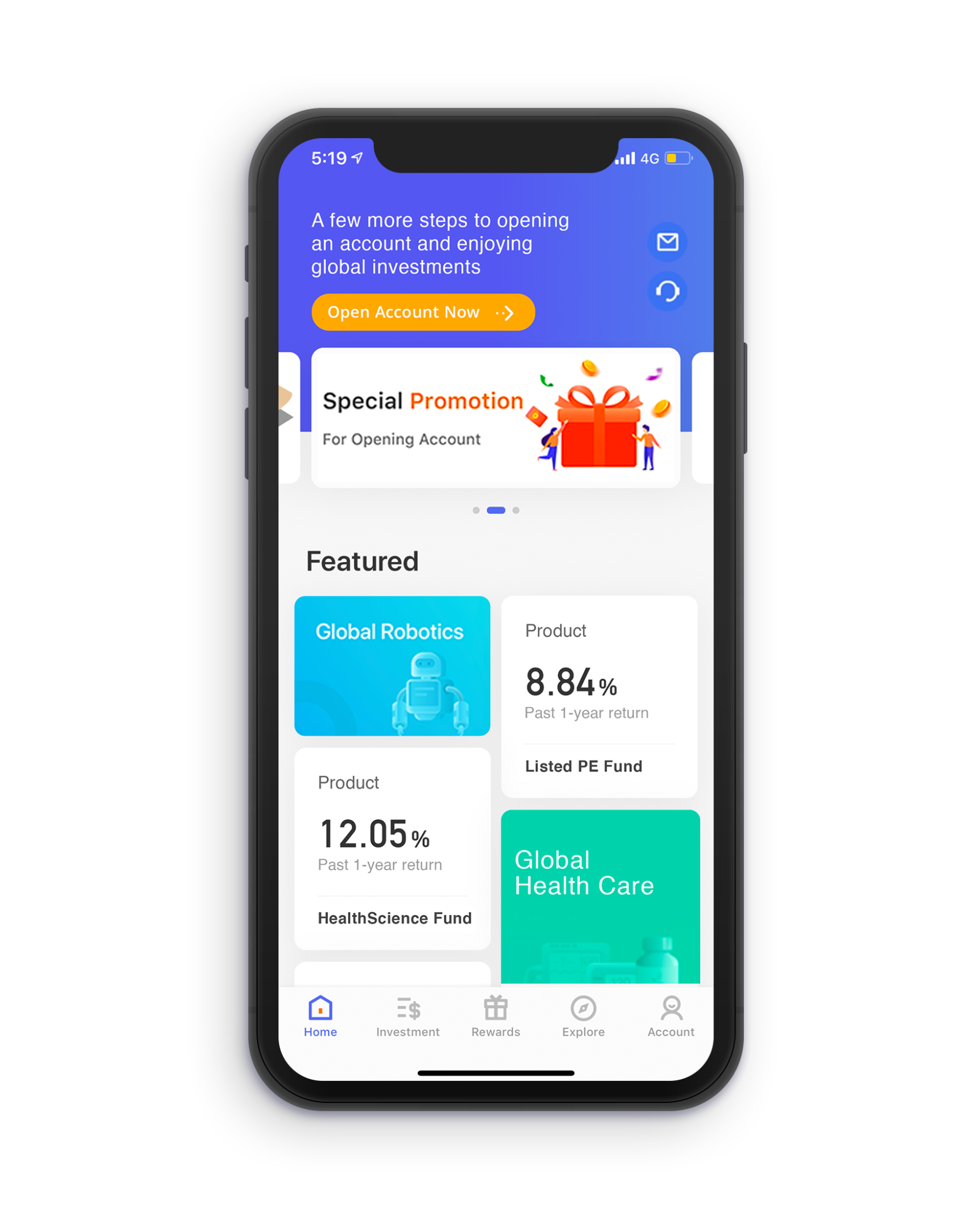

They have a website at https://lu-global.com/, but it’s a mobile only offering, so you’ll need to download the app to look through the products.

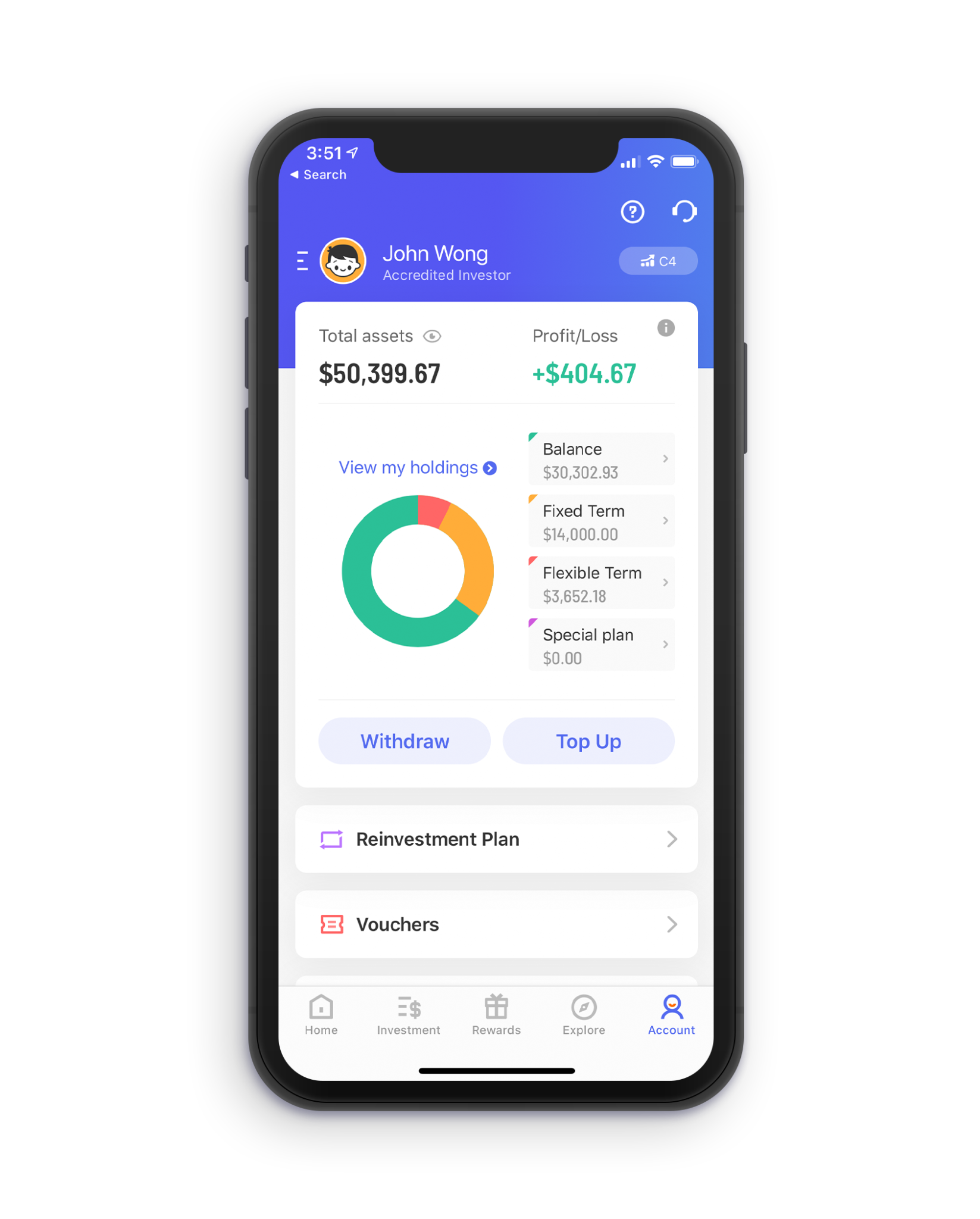

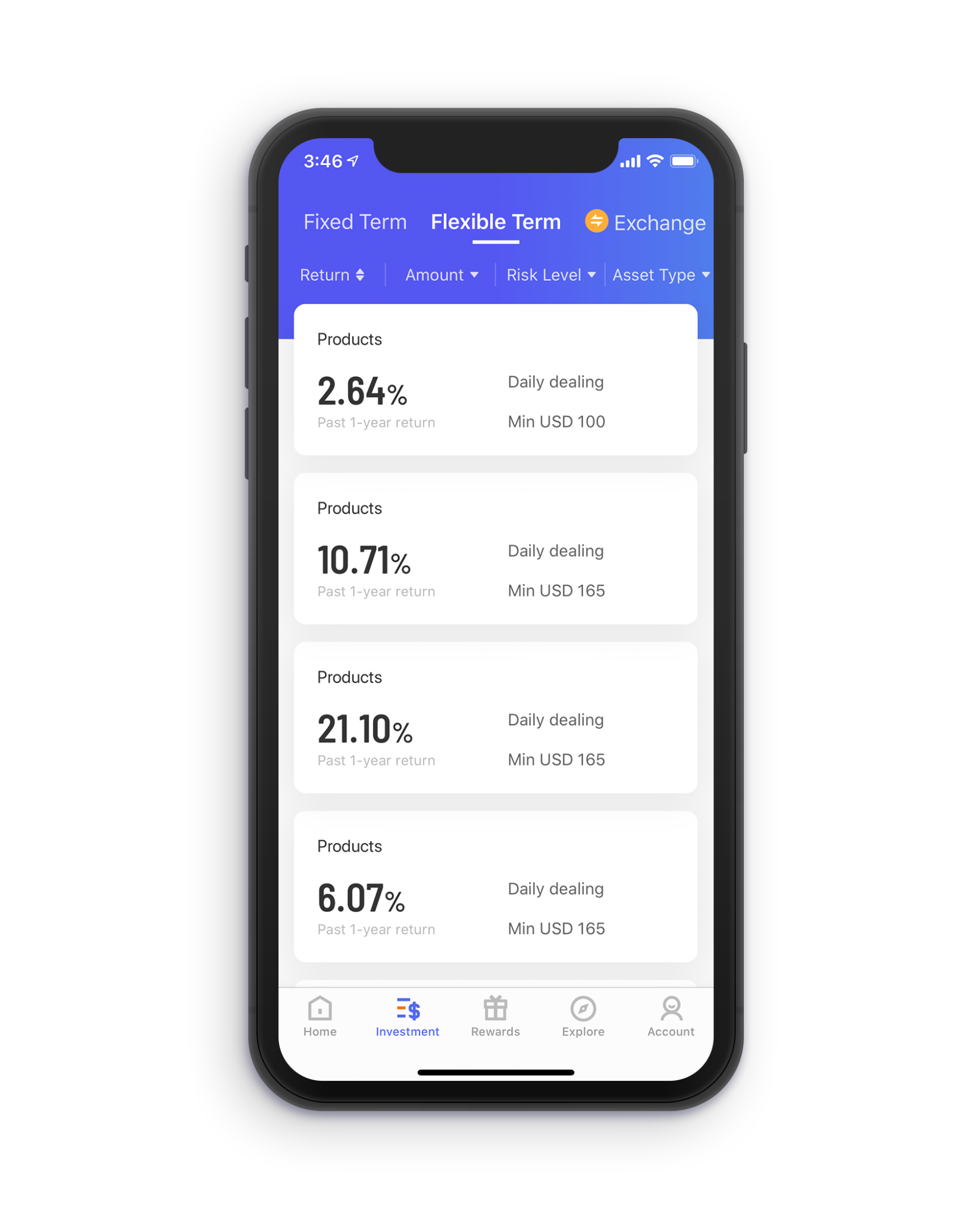

Once you download the app, you’ll be able to view all the products they have. And you can click on individual funds to get more information about them. The list of funds available is pretty impressive, and includes funds from Amundi, Blackrock, Pimco etc.

What I like about LU Global?

Access to sophisticated products with small minimum sums and low subscription fees

By far the main advantage of LU Global can be broken down into 3 points:

- Access to sophisticated funds

- Small minimum investment amount

- No subscription fees for fixed term funds

Typically, the only other way that you can get access to these funds is via (1) a broker, or (2) a financial adviser (eg. by buying a product through Prudential, Great Eastern etc).

Both of which have their own problems.

The broker method usually entails paying a subscription fee (or sales charge), which is a percentage of the amount invested when you first buy in, and requires a fairly significant minimum investment sum. And the financial adviser method usually locks you in on a long-term contribution plan (you know, those contribute $1000 a month for 10 years style plans).

With LU Global, you get direct access to the underlying funds, with no subscription fee (on fixed term products), and at significantly smaller minimum investment sum (varies from fund to fund, but can be as low as USD 1,000).

Tech platform is amazing

The other thing that I really like about LU Global, is just how amazing the app is. As a millennial myself, I do most of my banking and investments via my mobile phone these days, and the fact that the LU Global app is silky smooth and fully functional, is just amazing.

They’ve definitely picked up a lot of good traits from Ping An’s technology, and it shows in the mobile app.

Fund Fees

Long story short, when you invest in LU Global, you don’t need to pay subscription fees / sales charges when you buy fixed term funds.

You only need to pay the management fee on the underlying funds (ie. Expense ratios), which in any case, is payable for all investors of the fund.

Returns of the underlying funds depends on the fund manager

Of course, because you’re investing in actively managed funds, the underlying performance depends on how great the fund manager is.

If you’re good at picking and you get a good manager, your investment return has a higher likelihood of outperforming benchmarks.

If you’re unlucky though, the active manager could underperform the index.

So it really depends a great deal on your ability to pick fund managers, which is an entire topic in itself. This is a problem that you’ll face regardless of how you access these funds.

The way I see it though, you’ll really need to take some time out and analyse the funds, to determine which one is right for you, given your overall risk appetite and asset allocation.

Closing Thoughts: Who is LU Global meant for?

Because LU Global requires accredited investor status, it does limit a large part of the Singapore market. If you’re a fresh grad with not much savings, you’re most likely going with a roboadvisor or buying a wealth management product through a financial advisor from Great Eastern etc.

If you’re an accredited investor though, it really depends on what kind of an accredited investor you are. If you’re an ultra-high net worth individual, you probably already have an army of private bankers chasing after you, in which case a product like this may make less sense.

I think the sweet spot is for those accredited investors with a net worth of around $3 million to $10 million. At that level, you may not get access to the best products even through private banking, and a platform like LU Global could be a very interesting alternative. It would also be a good pick for more tech-savvy investors who will enjoy the convenience of a mobile app.

With LU Global, you can get access to a whole bunch of sophisticated funds, with low minimum sums, and low fees. That’s a pretty great deal.

If you’re not a Singapore resident, you can get access to this great investment platform as well. It’s a good way to get exposure to some sophisticated funds at a low cost and at low investment sums.

Check out LU Global’s app here if you’re interested!

Looking for a comprehensive guide to investing? Check out the FH Complete Guide to Investing for Singapore investors.

Support the site as a Patron and get market and stock watch updates.

Join the Facebook Group (Singapore) or Facebook Group (China) to continue the discussion!