So… the next T-Bill auction is on 8 December 2022.

This will be the second last T-Bill auction for 2022.

However, interest rates for the most recent T-Bill auction has come down to 3.9%.

With Fixed Deposits offering up to 4.0% interest rates – are T-Bills still attractive?

Next T-Bill Auction on 8 December

If you want to apply, do get your cash applications in by 9pm on 7 December 2022 (Wednesday).

Or if you’re using CPF-OA, you’ll want to get it done by 6 December.

What is the estimated yield for the next T-Bills auction?

As discussed in previous articles – T-Bills interest rates are determined by auction.

40% of the issue size is set aside for non-competitive bids, and the rest of the issue size is matched up to the competitive bids.

The point where it is cut-off, is the yield for the T-Bills.

So it is incredibly hard to predict the exact T-Bill yield beforehand, because it comes down to each individual bid.

But of course, we can get some clues from the market.

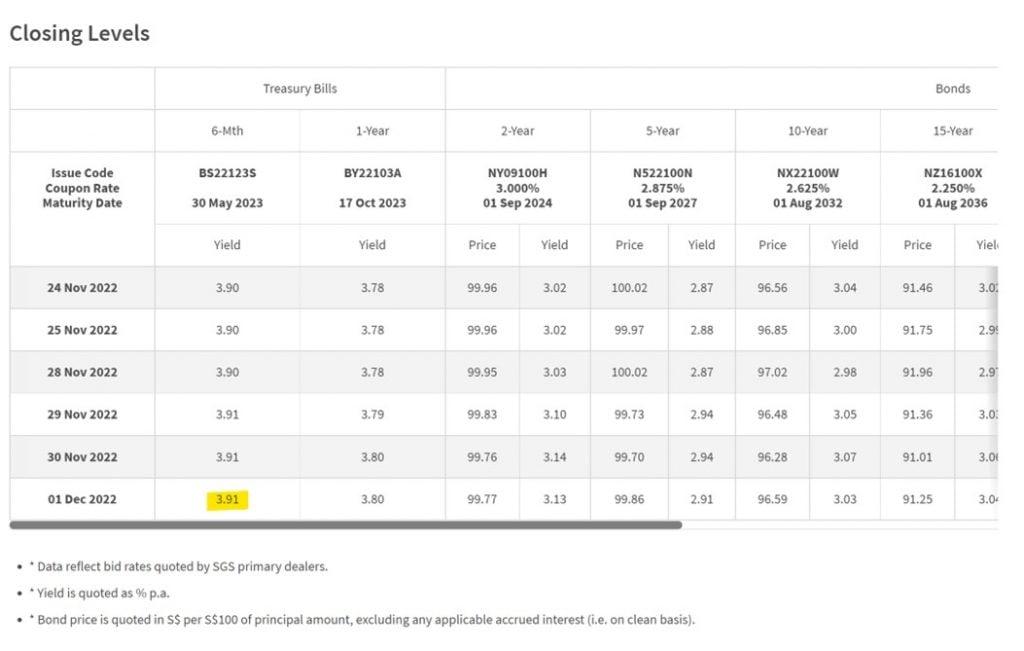

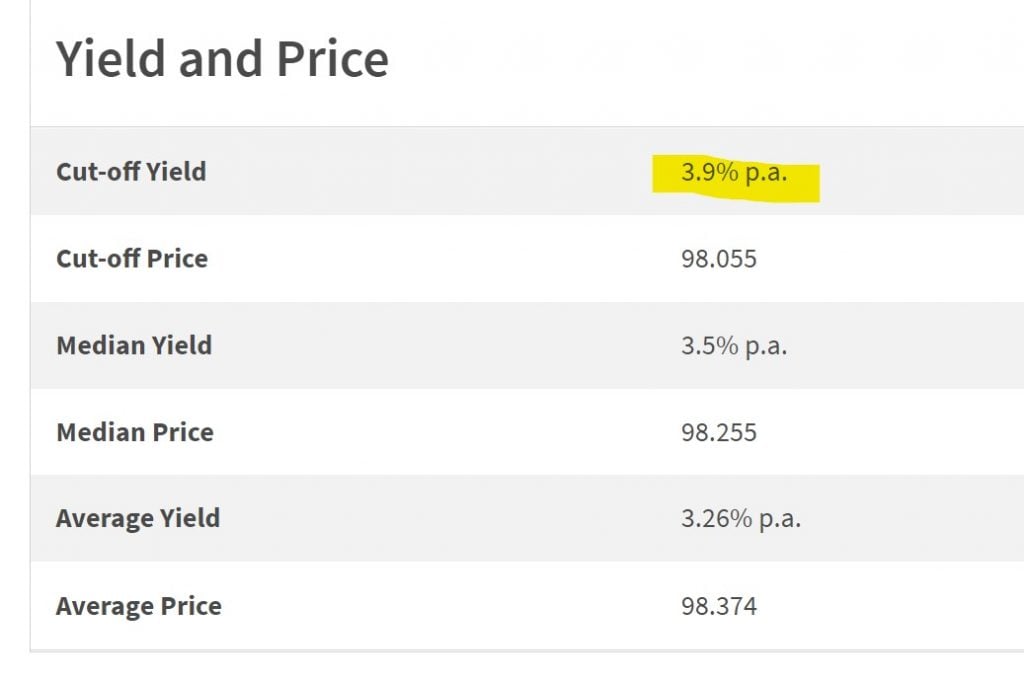

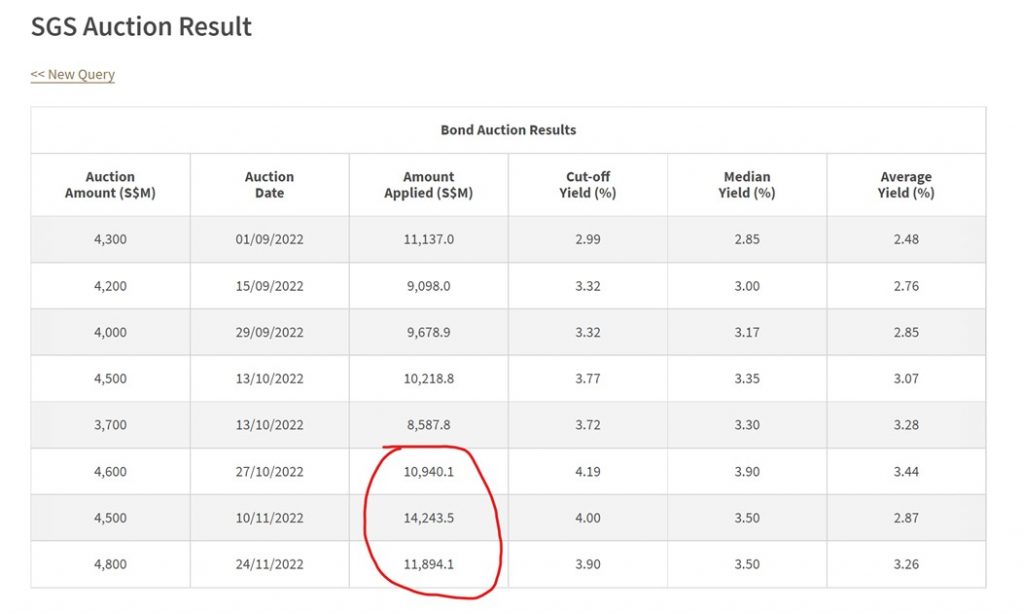

Latest T-Bills Auction (3.9%)

The most recent T-Bills auction closed at 3.9%:

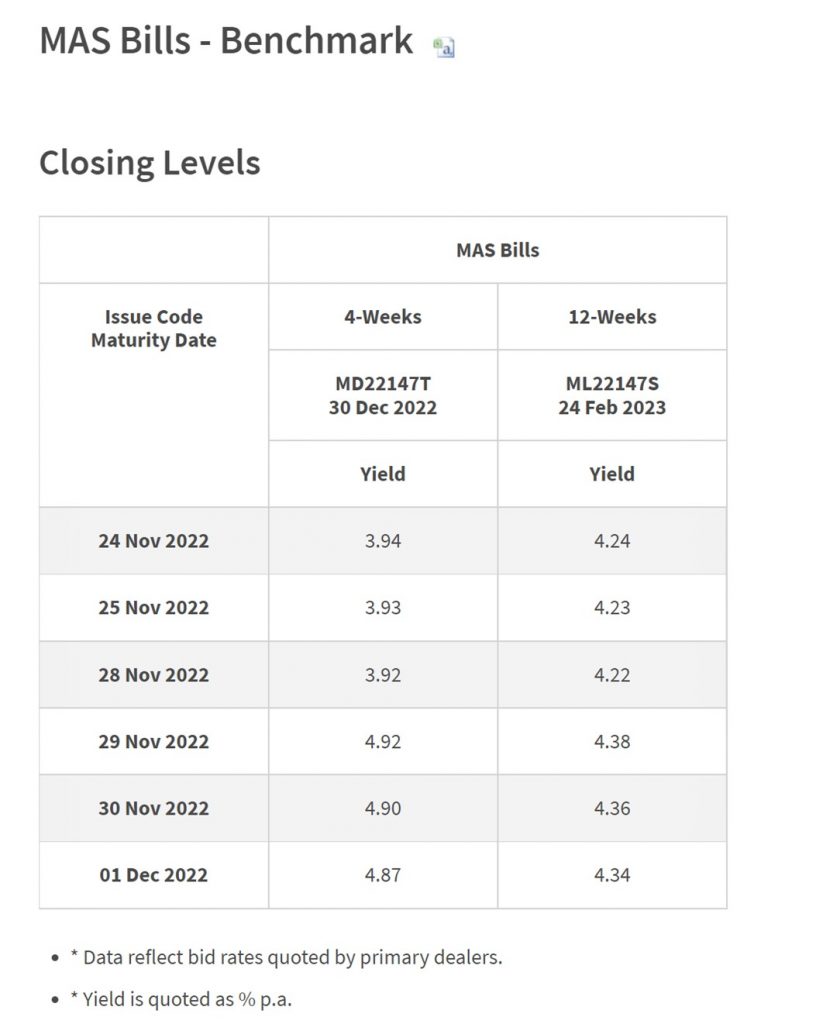

MAS Bills (4.34%) / Singapore Government Securities (3.91%)

The latest 12 week MAS Bills trade at 4.34%.

While the 6 month T-Bill trades at 3.91% on the open market:

So if you purely use the market prices, then the 6 month T-Bills should be about 3.9% to 4.3%.

Interest rates are trending downwards?

However, interest rates are trending down since early November, after the dovish US inflation print.

Powell’s dovish speech this week did not help matters:

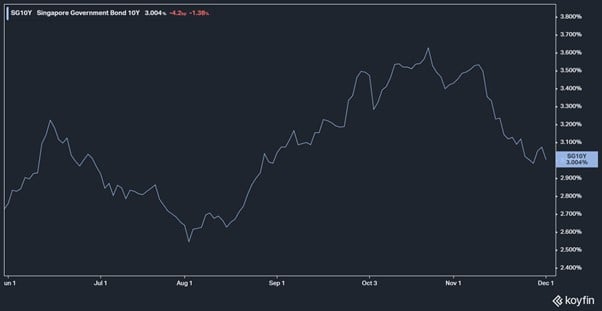

Same story with the US 2- and 10-year treasury.

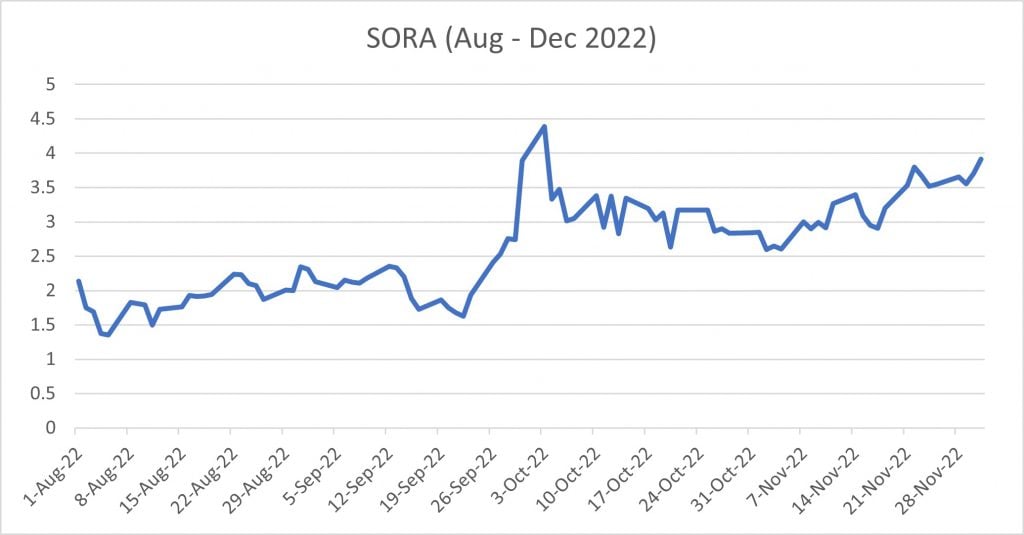

What about SORA?

From MAS: The Singapore Overnight Rate Average or SORA is the volume-weighted average rate of borrowing transactions in the unsecured overnight interbank SGD cash market in Singapore between 8.00am and 6.15pm.

So SORA gives you a good measure of SGD interbank liquidity.

Interestingly, SORA has been trending up since early November, despite global interest rates coming down.

This is very interesting, and suggests that funding market stress may be building.

That said, for T-Bills, I think the fact that government bond interest rates are trending down is probably the bigger factor.

So you might see T-Bills come down further from the previous 3.9% auction cut-off yield.

What about retail demand?

The big wildcard though – is retail demand.

You can see how investor demand for the last 3 T-Bill auctions is absolutely massive, coming in at more than $10 billion (vs a $4 billion+ issue size):

How much retail demand we will see on the next T-Bills auction?

Not an easy call.

4.0% seems to be the threshold where investor demand goes up a lot.

At 3.9%, fixed deposits are actually quite an attractive alternative.

So will retail investors still continue to bid so strongly for T-Bills, when they can get similar yields from Fixed Deposit?

Frankly, I have no easy answers for this.

What is the anticipated yield on the next T-Bills?

Gun to my head, I think you might see the next T-Bills cut-off yield come in anywhere from 3.8% – 4.0%.

But do bear in mind the exact yield depends on auction mechanics, and cannot be predicted with a high degree of certainty.

The big wildcard would be how strongly retail investors turn up for this auction.

And whether they decide it’s not worth the time and effort, and just go for Fixed Deposit instead.

BTW – we share commentary on Singapore Investments every week, so do join our Telegram Channel (or Telegram Group), Facebook and Instagram to stay up to date!

I also share great tips on Twitter.

Don’t forget to sign up for our free weekly newsletter too!

[mc4wp_form id=”173″]

Is Fixed Deposit a better buy than T-Bills?

Which brings us to the more interesting question.

Assuming the next round of T-Bills comes in at 3.8% – 4.0%.

Is Fixed Deposit a better buy?

A 6 months fixed deposit with CIMB yields up to 4.00% interest rates.

Fixed Deposits are SDIC insured, so risk free up to $75,000.

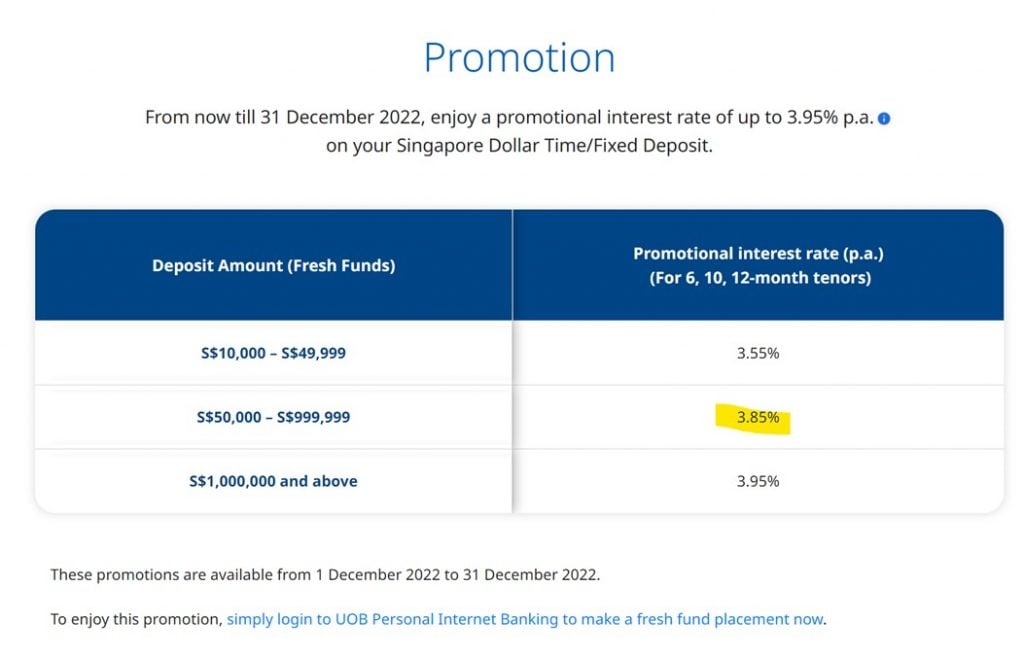

If you prefer a local bank, you can get 3.85% with UOB for 6, 10 or 12 months tenor.

Very, very attractive.

Fixed Deposit – Don’t need to bother with auction or allotment

With fixed deposit you don’t need to bother with competitive or non-competitive bidding.

Or how much you get alloted.

Or having to wait for the next auction, and losing the interest in the interim.

With Fixed Deposit, you can get it done instantly online (if you already have online banking with the bank).

Fixed Deposit – Can get the money back before maturity…

And with Fixed Deposit, you can request to break it any time.

Okay I get that the ability to break fixed deposit is ultimately subject to the bank’s discretion.

But if you go with a local bank it *shouldn’t* be rejected.

Do note that you do have to pay a small penalty though, usually in the form of lower accrued interest.

I put my cash into Fixed Deposit this week

Because of that, I actually find Fixed Deposit very competitive when compared to T-Bills these days.

In fact I actually deployed a decent chunk of cash into UOB’s 6 month fixed deposit at 3.85% just this week.

For all the reasons above – I didn’t need to bother with auction mechanics, waiting for the next auction, worrying about allotment, worrying about interest rates etc.

I could deploy whatever amount I wanted, instantly with UOB – at what is frankly quite decent interest rates:

Must submit competitive bid for T-Bills – 3.85% minimum?

That said, for those who do want to try their luck with T-Bills, I think you absolutely MUST, MUST, MUST submit a competitive bid this time around.

Remember – A non-competitive T-Bill bid means you will be allotted at whatever the cut-off yield is.

When you can easily get 3.85% from a UOB fixed deposit, it’s just not worth the risk to apply for a non-competitive bid for T-Bills, and risk getting allotted at below 3.85%.

I think you must submit competitive, and the floor price should at least be 3.85%.

You can even argue that the floor price should be 3.95% because that’s what you can get on a 6 month CIMB Fixed Deposit, and frankly I won’t argue with that.

Will I still be applying for the T-Bills?

I shared my updated approach to cash optimisation in yesterday’s article:

The way I see it, I still value liquidity highly in this climate, given elevated macro risk.

But once I have my minimum liquidity set aside, I don’t mind locking the money up for higher interest rates.

So my priority is:

- High Yield Savings Account for instant liquidity (eg. DBS Multiplier, UOB One, Trust Bank – whatever floats your boat)

- Singapore Savings Bonds for liquidity of up to 1 month away

- Rest into a mix of T-Bills / Fixed Deposit for higher yield, while sacrificing liquidity

I will only buy T-Bills if they are issued at a premium to Fixed Deposit

T-Bills only make sense to me if they offer a higher interest rate than Fixed Deposit, for the reasons mentioned above.

But given that DBS waives the $2 application fee, I don’t mind just putting in a competitive bid to try my luck.

Who knows, maybe everyone would have flooded to Fixed Deposits, and we have a surprise jump in T-Bill yields?

What competitive bid would I put for T-Bills?

Anything above 4.0%, I probably wouldn’t mind putting some cash into T-Bills.

With competitive bids you can actually submit a few bids, for example:

- $10,000 for 4.0%

- $20,000 for 4.2%

- $50,000 for 4.5%

And so on.

And you only get allotted each tranche if the cut-off yield is above the yield you bid for.

So using the example above, if the cut-off yield is 4.1%, you’ll only get $10,000 worth of T-Bills at 4.1%.

Do note that the cash is deduction from your account at the time you make the application.

So there is a small bit of opportunity cost.

But if you make the T-Bill application right before the cutoff (9pm on 7 Dec), you actually get refunded the cash once the auction results are out the next day, so you don’t lose the liquidity for long.

Long story short – I’ll probably still put in a competitive bid for the T-Bills, but anything below 4.0%, I might just go with fixed deposits instead.

And I will bid accordingly.

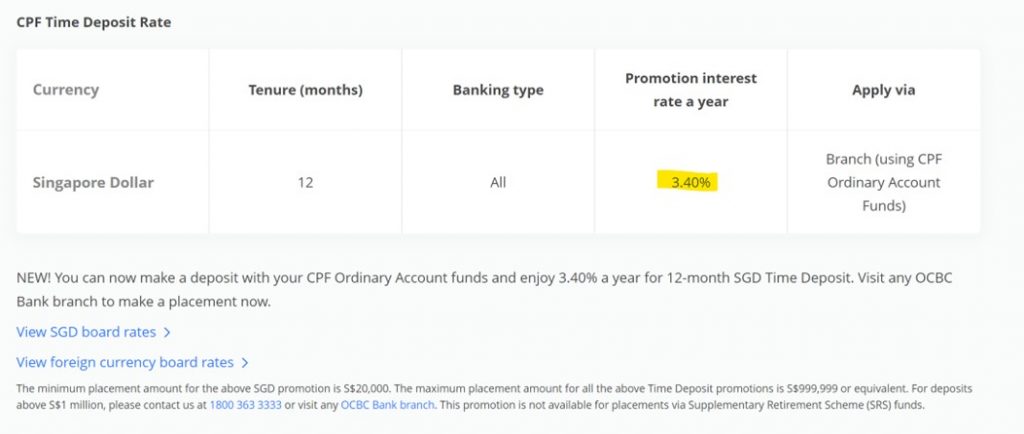

What about CPF-OA applications?

For those who are using CPF-OA to buy T-Bills for a “risk-free” carry trade.

You can check out my previous article here for the full considerations.

I would say it probably still makes sense to apply, unless you think that CPF-OA rates will go up any time soon.

CPF-OA cannot be used for Singapore Savings Bonds, and the only Fixed Deposit option for CPF-OA is at 3.4% with OCBC:

I don’t think T-Bills will go as low at 3.4% this auction, so you probably still get a better return on T-Bills

FAQs from the media… Singapore Savings Bonds vs T-Bills

Separately… I was asked to comment on the attractiveness of T-Bills vs Singapore Savings Bonds recently.

I thought the questions posed were frankly quite good.

So I’ve extracted the questions, and my responses, below.

Hopefully this gives you additional colour into the difference between the two instruments, and my general thought process:

Why have the yields of the past two T-bill auctions been dropping after it hit a record high of 4.19%, especially since the US Fed has continued on its rate hiking cycle?

Likely to be a combination of 2 reasons:

- Possible increased retail investor demand. Retail investors who want to get full allocation may submit lower competitive bids (especially for those using CPF-OA to purchase T-Bills – who need to go down to the bank to apply, and don’t want to make a wasted trip). This could skew yields lower.

- Since the latest US CPI print in early November came in below expectations, market has started to price in a more dovish Fed. So interest rates have come down quite a bit since early November, and you see this reflected in global interest rates. So for Singapore interest rates to come down slightly is not unexpected.

Subscription numbers are also down for both SSBs and T-bills. Are they losing their allure?

One possible reason could be that much of the liquidity from retail investors has already been deployed. Which leaves less liquidity to go into the new SSB/T-Bills.

Another reason is that fixed deposit interest rates have gone up quite a bit the past few months, and you can get up to 3.85% on a 6-month fixed deposit with UOB today.

That’s higher than 1-year SSB yields, and very competitive with T-Bills.

And with Fixed Deposit you don’t have to worry about allotment limits, competitive vs non-competitive bidding, and you can put the money in any time with very little uncertainty.

So it’s possible a lot of the money has moved into alternatives like Fixed Deposit.

I myself decided to put some cash into the UOB Fixed Deposit this week instead of T-Bills.

Is it still worthwhile to invest in T-bills and Singapore Savings Bonds?

Both are quite different products.

T-Bills have high short-term yields, but at the expense of liquidity (not easy to sell before maturity, as a retail investor).

They’re a good way to benefit from high short term interest rates, for investors who don’t need the money recently.

Singapore Savings Bonds can be redeemed easily (get your money back at the start of the next month), and can be held for up to 10 years. But the short-term yields are not so good.

They’re good if you want the option to get the money back any time, while also being able to hold up to 10 years – and still getting decent interest rates.

So it’s really up to each investor to decide what’s the right balance between yield (returns) and liquidity.

I would say both have a place in a Singapore investor’s portfolio, together with Fixed Deposits.

What is your investment strategy re Singapore government securities?

I value liquidity a lot in this climate, given elevated macro uncertainty.

So I am still applying for my maximum allotment of Singapore Savings Bonds each month.

I like Singapore Savings Bonds because I can get the money back very quickly (start of the following month), to the point where I am prepared to take a lower short term interest rates on them.

And worst case if interest rates drop drastically next year, I always have the option to hold for up to 10 years.

After that, it’s really choosing between T-Bills and Fixed Deposit.

T-Bills are hard to exit before maturity for retail investors, so to me they only make sense if they offer a good interest rate premium over Fixed Deposits.

With latest T-Bills at 3.9%, I can get 3.85% on UOB’s 6 month Fixed Deposit.

And with a Fixed Deposit I don’t have to worry about bidding, auction mechanics, allotment etc. And I can deploy it immediately, without having to wait for the next auction (opportunity cost of the money).

So Fixed Deposits are quite competitive vs T-Bills right now, unless we see T-Bill interest rates go up again.

I myself decided to put some cash into the UOB Fixed Deposit this week instead of T-Bills.

Trust Bank Account (Partnership between Standard Chartered and NTUC)

Sign up for a Trust Bank Account and get:

- $35 NTUC voucher

- 1.5% base interest on your first $75,000 (up to 2.5%)

- Whole bunch of freebies

Fully SDIC insured as well.

It’s worth it in my view, a lot of freebies for very little effort.

Full review here, or use Promo Code N0D61KGY when you sign up to get the vouchers!

– Free USD150 ($212) cash voucher

I did a review on WeBull and I really like this brokerage – Free US Stock, Options and ETF trading, in a very easy to use platform.

I use it for my own trades in fact.

They’re running a promo now with a free USD 150 (S$212) cash voucher.

You just need to:

- and fund S$2000

- Make 1 US Stock or ETF trade (you get USD100)

- Make 1 Options trade (you get USD50)

1080-1080-002-1024x1024.jpg)

Looking for a low cost broker to buy US, China or Singapore stocks?

Get a free stock and commission free trading .

Get a free stock and commission free trading with .

Get a free stock and commission free trading with .

Special account opening bonus for Saxo Brokers too (drop email to [email protected] for full steps).

Or for competitive FX and commissions.

Looking to buy Bitcoin, Ethereum, or Crypto?

Check out our guide to the best Crypto Exchange here.

Do like and follow our Facebook and Instagram, or join the Telegram Channel. Never miss another post from Financial Horse!

Looking for a comprehensive guide to investing that covers stocks, REITs, bonds, CPF and asset allocation? Check out the FH Complete Guide to Investing.

Or if you’re a more advanced investor, check out the REITs Investing Masterclass, which goes in-depth into REITs investing – everything from how much REITs to own, which economic conditions to buy REITs, how to pick REITs etc.

Want to learn everything there is to know about stocks? Check out our Stocks Masterclass – learn how to pick growth and dividend stocks, how to position size, when to buy stocks, how to use options to supercharge returns, and more!

All are THE best quality investment courses available to Singapore investors out there!

FYI – We just launched the FH Property Series. Everything you need to know to buy a property in Singapore, completely free of charge.

Are these courses certified? I would love to join or buy to learn more.

Regards

Good choice – you can click the links here to find out more about each course!

https://financialhorsecourse.thinkific.com/collections

We do run promotions from time to time, so do keep an eye out for those! 😉

Just curious, why did you put your money in UOB FD at 3.85% instead of CIMB FD at 4%?

It was more than SDIC’s 75k insurance, and I didn’t want to worry about counterparty risk.

So I just went with a local bank for peace of mind.