After the recent T-Bills auction, I’ve been getting a flood of questions on T-Bills.

The recent T-Bills was massively oversubscribed, seeing $14.2 billion applications for a $4.5 billion issue size.

Because of this, the yields went down to 4.0%.

And allotment for non-competitive dropped to 49% only.

A lot of you have asked:

- Does it still make sense to buy T-Bills with CPF-OA?

- Should you still buy T-Bills or just buy Fixed Deposit or Singapore Savings Bonds?

- Should you apply for competitive or non-competitive bid for T-Bills going forward?

So I wanted to share some thoughts in this article.

Does it still make sense to buy T-Bills with CPF-OA?

Short answer – yes.

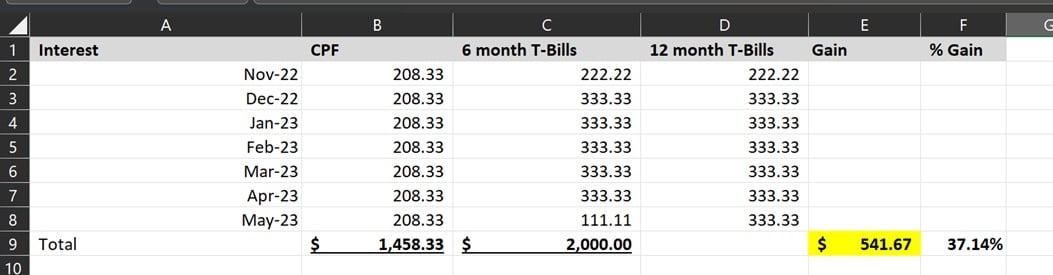

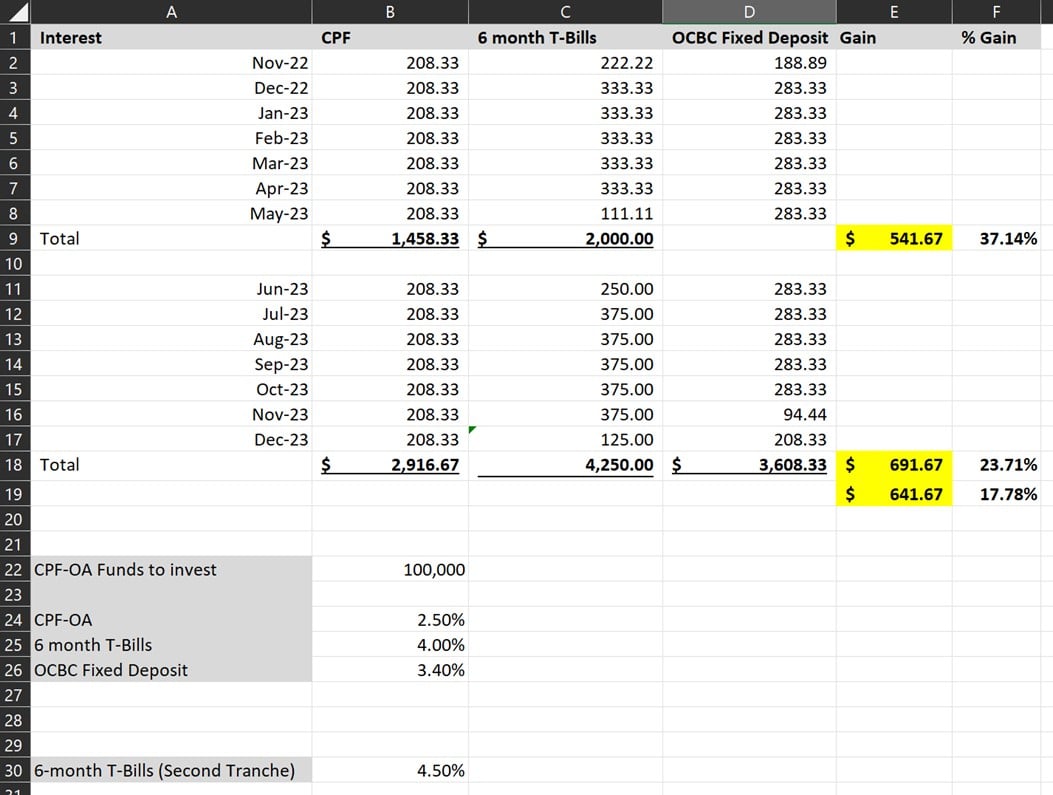

Assuming you invest $100,000 CPF-OA in 6-month T-Bills, you will make an extra $541.67 using the latest 6-month T-Bill interest rates of 4.0%.

That’s even after accounting for the 1 month lost CPF-OA interest:

There are quite a few points to note though, and you can check out my previous article here for the full thought process.

But to sum up, the key considerations are:

- Is it worth your time and effort?

- Buy 6 months or 12 month T-Bills?

- What other risks to consider?

Is it worth your time and effort to buy T-Bills with CPF-OA?

Don’t forget you can only invest what is left after setting aside $20,000 in your CPF-OA.

And on $100,000 CPF-OA, you’re making $541 over 6 months.

And buying T-Bills with CPF-OA cannot be done online, it must be done in person at the bank branch (any of the 3 local banks).

Which means a 1 – 2 hour wait approximately.

So yeah… you might want to decide if it’s worth your time and effort to buy T-Bills with CPF-OA.

Of course, the more money you have in your CPF-OA, the more worth it it becomes.

What about compounding?

Some of you have asked about the loss of compounding effect for the $100k CPF OA.

Now T-Bills are issued at a discount, so you effectively get the “interest” upfront.

Which means T-Bills will have a superior compounding effect (vs CPF-OA).

But frankly when you’re compounding over 6 months, the difference is miniscule.

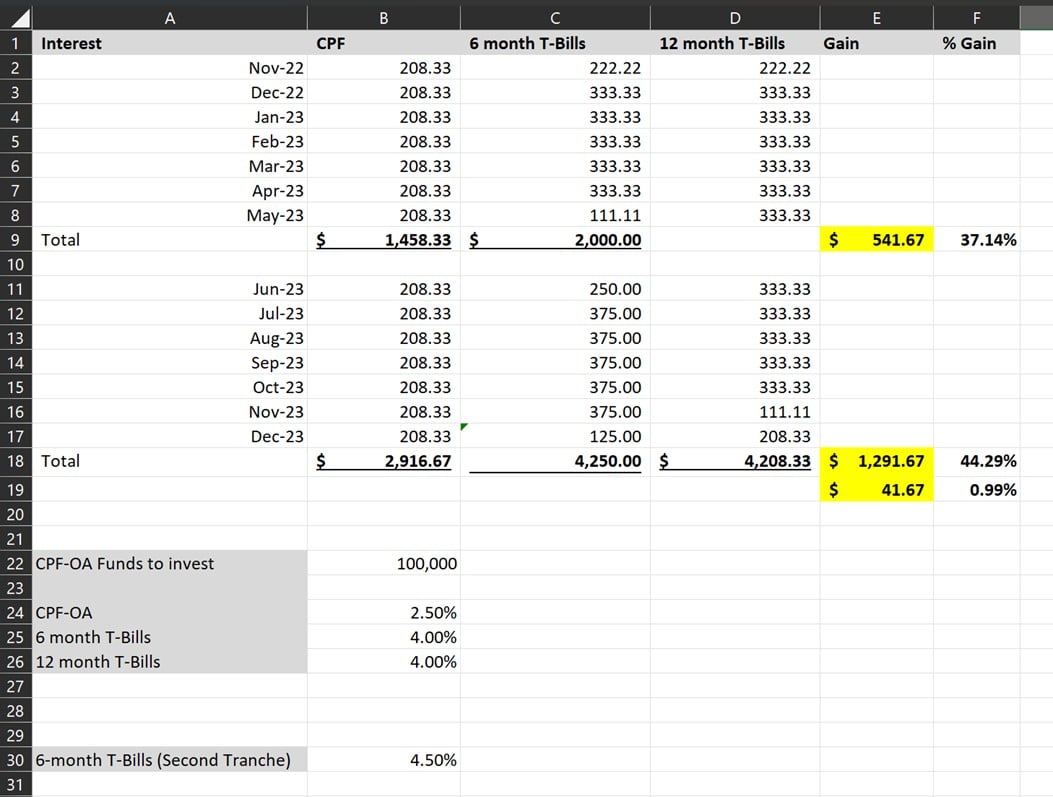

Buy 6 months or 12 month T-Bills?

I ran the numbers below.

The answer depends on:

- Where will T-Bills interest rates be in 6 months when you roll over the money?

- Can you roll over the T-Bills the same month without losing another month of CPF interest?

Assuming that:

- You roll over T-Bills the following month (losing another month of CPF-OA interest)

- The next tranche of T-Bills in 6 months is 4.5%

- The 12 month T-Bills are issued at 4.0% interest rates

You make an extra $41.6 going with 6 month T-Bills.

Long story short – the numbers are close, and there are a lot of assumptions involved.

But let me just spare you the trouble.

There are no more 12-month T-Bill auctions for 2022.

So if you want to buy T-Bills with CPF-OA any time this year, you need to go with the 6 month T-Bills.

Beggars can’t be choosers.

What other risks to consider when buying T-Bills with CPF-OA?

The biggest one?

CPF-OA interest rates going up.

If CPF-OA rates do go up, you won’t benefit because you already bought the T-Bills with CPF-OA money.

Now – Will CPF-OA rates go up?

It’s a tricky political issue, because HDB mortgage rates are tied to CPF-OA.

And interest rates were stuck at rock bottom the past 10 years while CPF-OA didn’t go below 2.5%.

Now that interest rates go up, CPF-OA goes up immediately?

Not an easy one to call, and I leave it up to you to decide.

Long story short – if you think CPF-OA interest rates will go up soon to match T-Bills, then it wouldn’t make sense to buy T-Bills with CPF-OA.

Using CPF-OA to buy T-Bills loses you a month of CPF-OA interest, so there is opportunity cost involved. Not to mention spending an hour in a bank queue is not my idea of fun.

You can buy Fixed Deposit with CPF-OA

Sidenote that while you cannot buy Singapore Savings Bonds with CPF-OA, you can buy Fixed Deposits.

Unfortunately, you can’t just put it into any off the shelf fixed deposit, it needs to be a special “CPF-OA” approved Fixed Deposit with one of the 3 local banks:

For now, the only such fixed deposit I know of is OCBC at 3.4%.

Again you need to go down to the bank to place Fixed Deposits with CPF-OA, and I’m hearing up to an hour wait at OCBC.

And interest rates are still lower than T-Bills at 4.0%, although you can lock in rates up to a year.

For illustrative purposes I ran the numbers below assuming 6 month T-Bills rolled over the following month at 4.5% (losing an extra month of CPF-OA interest).

Answer is that the 6 month T-Bills comes out ahead of OCBC Fixed Deposit by $642 over 12 months, but again, there are quite a number of assumptions involved with this.

That being said, if you wait a couple of months, I think there’s a good chance that UOB or DBS come up with similar CPF-OA Fixed Deposit products too, at possibly even higher interest rates.

So it might pay to wait a little.

Should you still buy T-Bills or just buy Fixed Deposit or Singapore Savings Bonds?

The answer to this question will depend very much on the interest rates on T-Bills.

How are T-Bills interest rates determined?

Now I get a lot of questions on how T-Bills interest rates are determined.

Let’s give a very simple example.

Imagine:

- There is $100 worth of T-Bills to be issued

- $50 of non-competitive bids received

- $80 of competitive bids received

Out of the $100 issue size – $40 (40%) will be set aside for non-competitive bids.

Of the remaining $60, they will be matched to the $100 of competitive bids.

So the competitive bids are arranged from the lowest to highest bids, and the lowest bids are matched first.

The bid yield for the $60th dollar of competitive bid – and that is the cut-off yield.

So if the $60th dollar of competitive bid was 4.0%, that would be the cut-off yield.

And 4.0% would be the yield for this round of T-Bills.

Everybody gets T-Bills at 4.0%, regardless of whether you applied for competitive or non-competitive.

How much allotment does the non-competitive bid get?

Using the example above – 40% of the issue size ($40) is allocated to non-competitive bids.

$50 of non-competitive bids was received, so it will be pro-rated.

Each person who applied non-competitive will get 40/50 allocation, or 80% allotment.

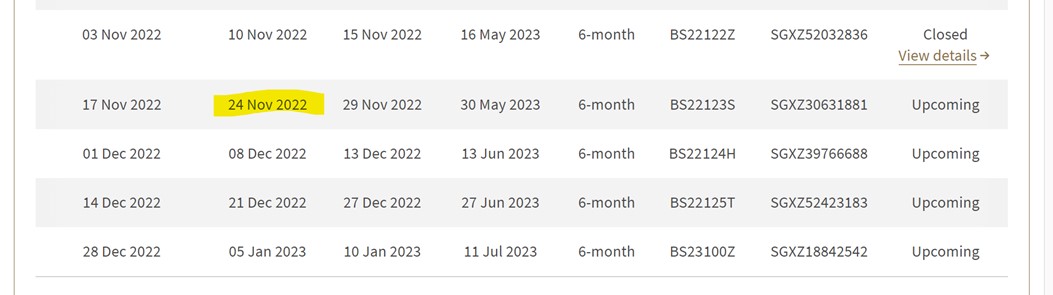

Next T-Bills Auction is 24 Nov 2022

Just a shoutout that the next round of T-Bills auction is on 24 November.

If you are putting in a cash application you need to submit by 23 November.

If you’re buying with CPF-OA you probably want to play safe and get it done by 22 November.

What is the anticipated yield on next 6 month T-Bills?

Based on the above– trying to predict the exact T-Bill yield in advance is incredibly tough, because it depends on each individual bidder.

That being said, we can still try to make an educated guess based on latest market pricing.

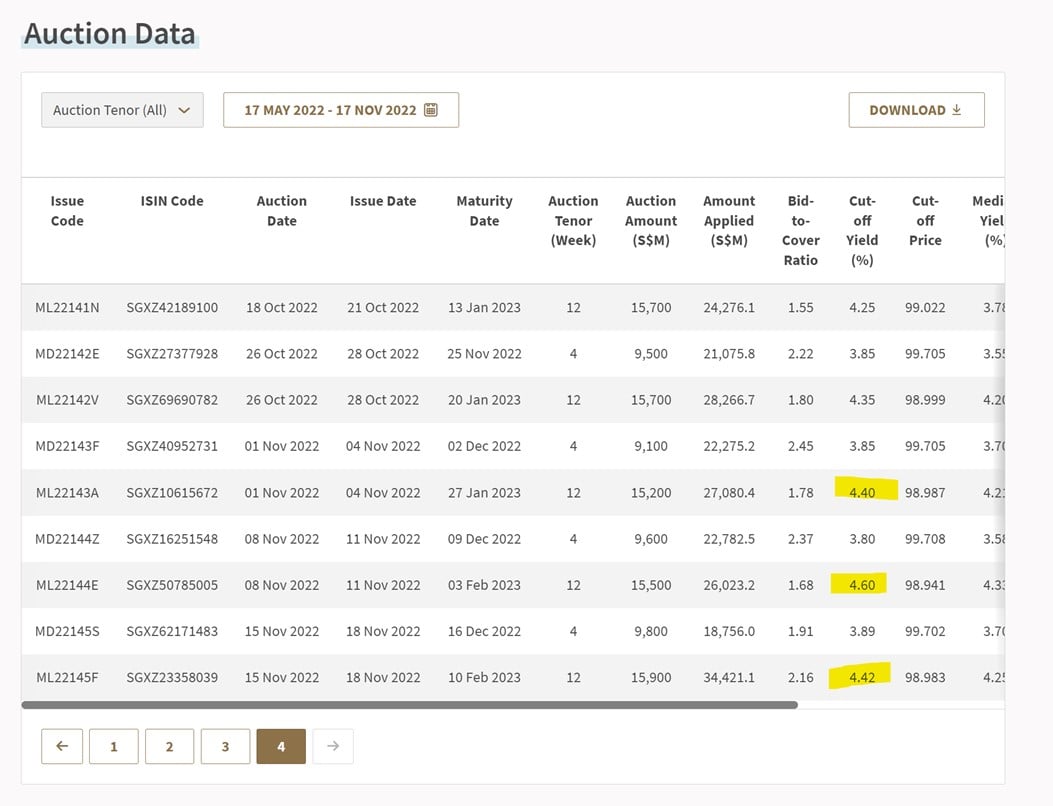

The most recent 3 rounds of 12 week MAS bills closed at 4.4 – 4.6%:

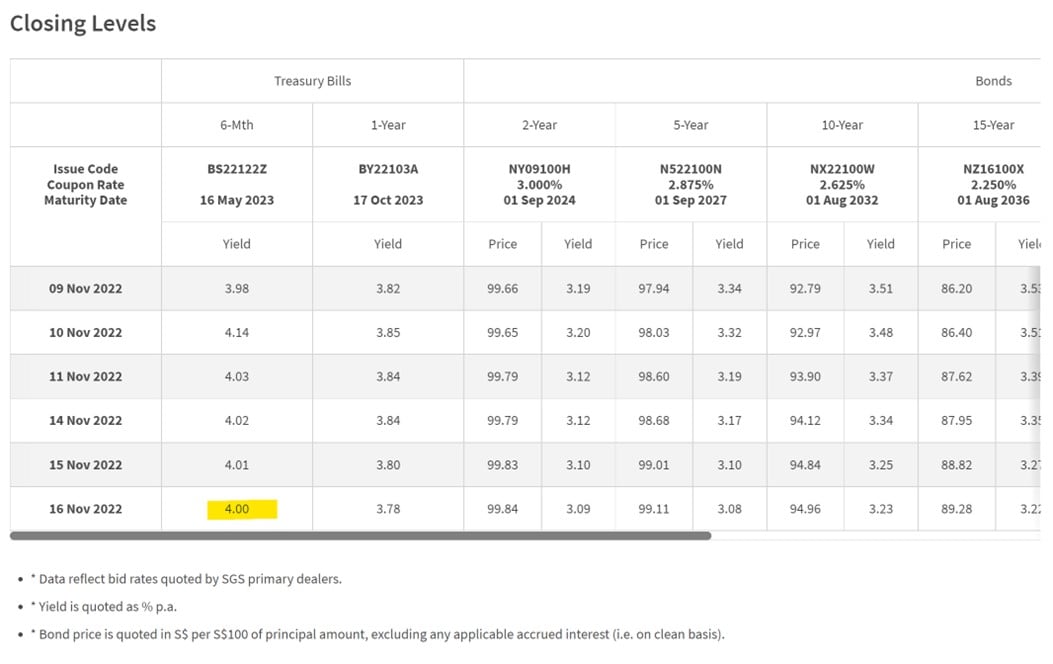

The latest 6 month T-Bill is trading at 4.0% on open market:

The complexity is that the last T-Bill auction showed very high retail demand for T-Bills, which could lead to unpredictable yields (retail tends to be more unpredictable than institutional).

So FH… what’s your estimate on the next T-Bill auction yield?

That being said, I know many of you just want a ballpark figure.

So with the caveat that I could be wildly wrong – I would say a range of 4.0% – 4.5% on the next T-Bills.

But do understand that the final cut-off yield for the T-Bills is determined by matching demand and supply, and cannot be conclusively determined without knowing all the exact auction bids.

So do take these numbers with a pinch of salt.

BTW – we share commentary on Singapore Investments every week, so do join our Telegram Channel (or Telegram Group), Facebook and Instagram to stay up to date!

Don’t forget to sign up for our free weekly newsletter too!

[mc4wp_form id=”173″]

What if the yield is very low… and I am forced to buy with a non-competitive bid?

With a non-competitive bid you’re buying at whatever the cut-off yield is.

If the cut-off is 3.5%, you’re buying at 3.5%.

If the cut-off yield is 1.5%, you’re buying at 1.5%

Sure, it’s a low risk outcome, but why take the risk when you can just put in a competitive bid for the T-Bills?

How does a competitive bid vs non-competitive bid work for T-BIlls?

Let’s take the most recent T-Bill auction, with a cut-off yield of 4.0%, and 49% allotment for non-competitive bids.

If you applied $100,000 non-competitive, you would get $49,000 T-Bills at 4.0% yield.

If you applied $100,000 competitive at 3.99%, you would get $100,000 T-Bills at 4.0% yield.

If you applied $100,000 competitive at 4.01%, you would get 0 T-Bills.

If you applied $100,000 competitive at 4.00%, you would get some T-Bills depending on the supply-demand matching at 4.00%.

Simple enough?

Should you still buy T-Bills or just go with Fixed Deposit or Singapore Savings Bonds?

So coming back to this question.

The best Fixed Deposit pays around 3.9% now.

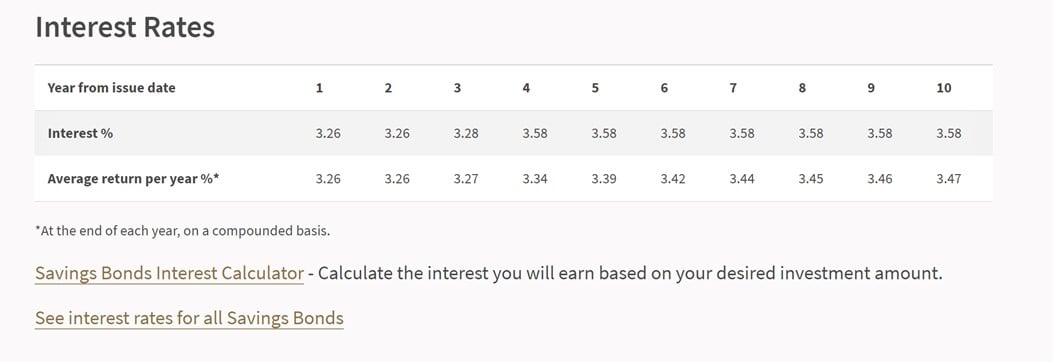

The latest Singapore Savings Bond pays 3.26% first year.

So I would say any T-Bill within my indicative range of 4.0% – 4.5%, probably worth a buy (in my books).

Which is easy enough to get around with competitive bidding.

What yield should you bid for competitive bidding for T-Bills?

Unfortunately there’s a bit of a game theory problem here.

Because the lower the yield you bid, the more likely you are to get full allocation.

But the more people that do this, the more likely the cut-off yield is going to drop.

So… I don’t want to comment too much on what yield you should be using for competitive bidding, to avoid messing up the auction dynamics.

All I would say is that the latest MAS T-Bill closed at 4.42% cut-off yield.

That’s probably fair market value to me.

But please for the love of god, don’t submit a competitive bid below the previous cut-off yield of 4.0%.

You’re just spoiling the yield for everyone else. 😉

Trust Bank Account (Partnership between Standard Chartered and NTUC)

Sign up for a Trust Bank Account and get:

- $35 NTUC voucher

- 1.5% base interest on your first $75,000 (up to 2.5%)

- Whole bunch of freebies

Fully SDIC insured as well.

It’s worth it in my view, a lot of freebies for very little effort.

Full review here, or use Promo Code N0D61KGY when you sign up to get the vouchers!

WeBull Account – Free USD150 ($212) cash voucher

I did a review on WeBull and I really like this brokerage – Free US Stock, Options and ETF trading, in a very easy to use platform.

I use it for my own trades in fact.

They’re running a promo now with a free USD 150 (S$212) cash voucher.

You just need to:

- Sign up here and fund S$2000

- Make 1 US Stock or ETF trade (you get USD100)

- Make 1 Options trade (you get USD50)

Looking for a low cost broker to buy US, China or Singapore stocks?

Get a free stock and commission free trading Webull.

Get a free stock and commission free trading with MooMoo.

Get a free stock and commission free trading with Tiger Brokers.

Special account opening bonus for Saxo Brokers too (drop email to [email protected] for full steps).

Or Interactive Brokers for competitive FX and commissions.

Looking to buy Bitcoin, Ethereum, or Crypto?

Check out our guide to the best Crypto Exchange here.

Do like and follow our Facebook and Instagram, or join the Telegram Channel. Never miss another post from Financial Horse!

Looking for a comprehensive guide to investing that covers stocks, REITs, bonds, CPF and asset allocation? Check out the FH Complete Guide to Investing.

Or if you’re a more advanced investor, check out the REITs Investing Masterclass, which goes in-depth into REITs investing – everything from how much REITs to own, which economic conditions to buy REITs, how to pick REITs etc.

Want to learn everything there is to know about stocks? Check out our Stocks Masterclass – learn how to pick growth and dividend stocks, how to position size, when to buy stocks, how to use options to supercharge returns, and more!

All are THE best quality investment courses available to Singapore investors out there!

FYI – We just launched the FH Property Series. Everything you need to know to buy a property in Singapore, completely free of charge.

Perhaps u can put an example on the loss of compounding effect for the $100k CPF OA as well

Actually T-Bills are issued at a discount, so you effectively get the “interest” upfront.

Which means T-Bills will have a superior compounding effect (vs CPF-OA).

But frankly when you’re compounding over 6 months, the difference is miniscule.

Are you able to comment on whether you will lose the month cpf oa interest if the application for t bills is not given as you bidding yield is higher then the strike yield?

That’s a good question. I suspect the answer is yes, but suggest to confirm with your CPF agent bank when submitting the application.