Unless you’ve been living under a rock the past 12 months, you’ve probably realised that property investments are really hot right now.

Here’s one of the questions I received:

Thanks FH! Property market in SG has been a huge topic as of late, was hoping to have some discussions in this area as property probably makes up a significant portion of everyone’s assets.

With not many opportunities in the stock market now, was wondering if we fall back on the old school mantra of “buy property to build wealth”? And whether property is still a “safe” asset like it was in the previous decade?

At the time same time with housing market being on a high these days, was wondering if we should even be expecting prices to further appreciate from what it is currently? Or rather, are we buying in at a peak?

Especially comparison and considerations for choosing or allocating between the 2 asset class –

property- rental & store of wealth

v/s

stock/etf/fund – growth & dividend

For somebody reaching 50 soon with 15 yrs retirement horizon

And on a related note:

– who is that target audience that should be the ones considering property/private properties given the wider macro

– how does property fare as an investment asset and is there a better alternative

Is Singapore Property still a good investment in 2023?

Almost every property agent seems to be calling for further increases to property prices and rentals.

Anecdotally, I also know of many who just bought their first property (or an investment property) the past year.

It’s gotten to the point where you have videos like this making the rounds:

Live through enough cycles, and you start to notice the warning signs of euphoria.

So… can this rapid increase in Singapore property prices keep up?

Let’s start by understanding the key factors driving this rally.

Headwind – Property Prices keeps going up… (despite rising interest rates)

A big headwind, is interest rates.

This has been the fastest pace of interest rate hikes in 25 years.

All that excitement over 4% on a T-Bill.

Also means that that you’re looking at 4.25% on the latest DBS fixed interest rate mortgage.

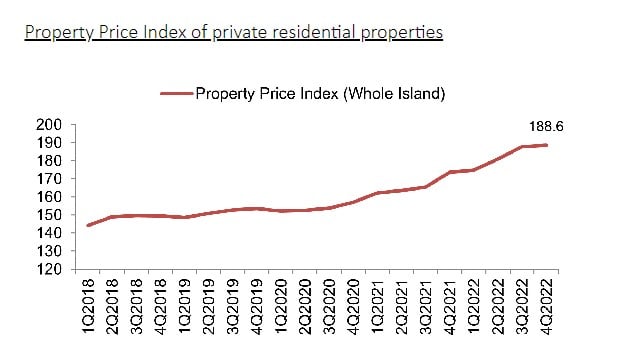

And yet… Singapore property prices just keep going up:

What gives?

Why do Singapore property prices keep going up?

The answer I suppose, is the reason why the price of almost everything is going up in the world.

Demand is too high, relative to supply.

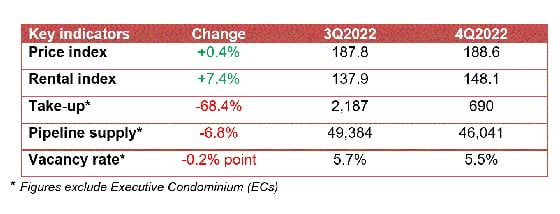

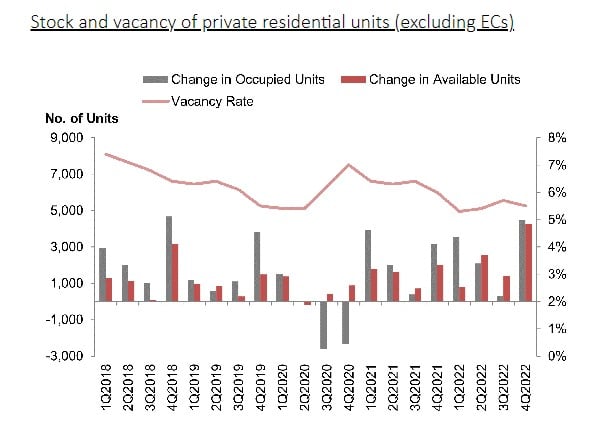

Look at the latest 4Q 2022 numbers below.

Pipeline supply down 6.8%, vacancy rate down 0.2%.

Rental index up a mind blowing 7.4%.

Why is Supply so tight for Singapore Property?

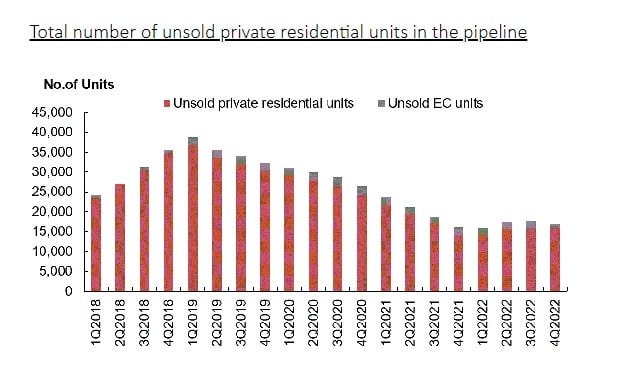

The supply situation for private residential property in Singapore looks dismal.

A lot of construction projects were delayed during COVID, so when demand rebounded after COVID, there just wasn’t enough houses to go around.

Even if you include EC units, pipeline supply is the lowest it’s been for the past 5 years.

Property takes years to construct, so by looking at the projects under development today you can have a rough idea of how much supply will come online in the next few years.

If you look forward the next 5 years, you’ll find that the supply situation doesn’t improve significantly too:

Yes, almost 40,000 new homes will be ready in 2023 if you count public housing, but given the backlog on demand from the past few years of COVID delays, am not sure if this will be sufficient to meet all the demand.

Demand for Singapore property is very high

At the same time, demand for property is very strong.

It’s a combination of factors – from locals buying property, foreigners coming in to rent / buy, locals renting their own place to work from home.

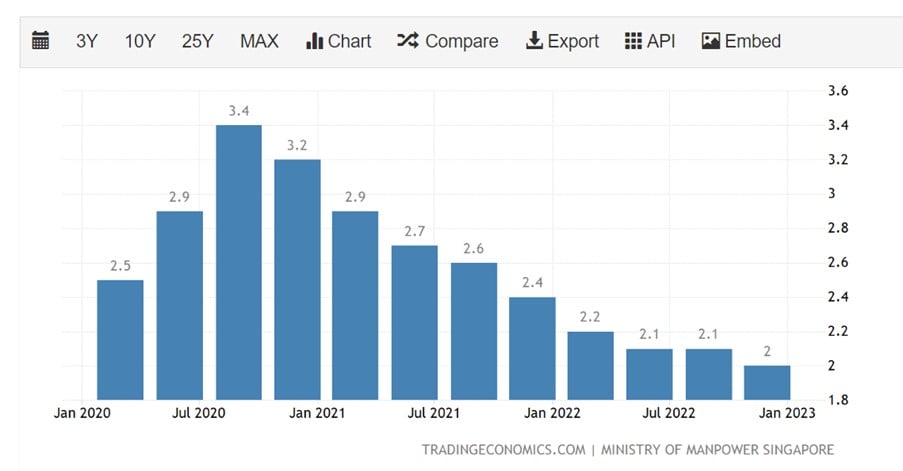

The key underlying factor is a red hot labour market – driving strong demand for property.

Vacanry rate are the lowest in 5 years.

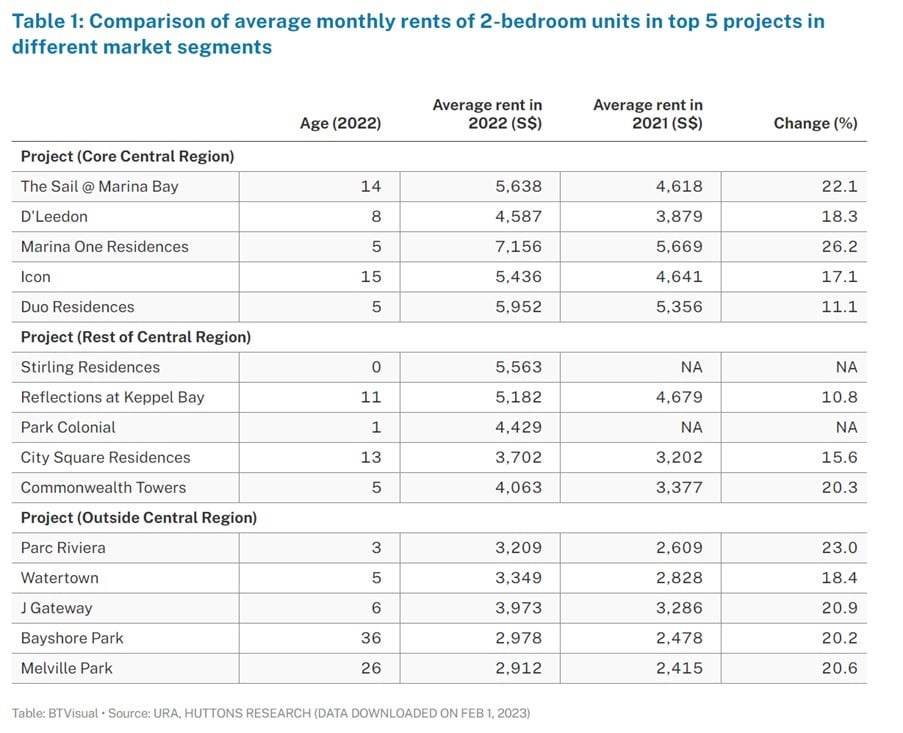

Here’s a chart from the BT summarising the blistering pace of rental increases in 2022.

You’re looking at 20% increase in rental for the more popular developments, which is pretty unbelievable stuff:

Is Singapore Property a good buy at these prices?

Let’s run some numbers.

A 2 bedrooom in Duo goes for $6000 monthly rental, or $72,000 a year.

Let’s say you spend $7,000 on agent fees and repairs, leaving a net rental income of $65,000.

Assuming the 2 bedroom costs $2 million (probably on the low side frankly).

That’s a 3.25% cap rate on the property.

When you’re paying 4.25% on your mortgage, and you can get 4% risk free on a T-Bill.

I mean, I’m not saying real estate is overvalued at these prices.

But if you’re buying at these prices, you better have some view on whether:

- Interest rates will go back down in the mid – longer term

- Rental rates will go up even further

Valuations wise, you need a 30% increase in rental just to bring cap rates in line with current levels of interest rates.

BTW – we share commentary on Singapore Investments every week, so do join our Telegram Channel (or Telegram Group), Facebook and Instagram to stay up to date!

I also share great tips on Twitter.

Don’t forget to sign up for our free weekly newsletter too!

[mc4wp_form id=”173″]

Short Term Price Outlook for Singapore Property?

That being said, cap rates are just valuations.

As every stock investor knows – just because something is overvalued, doesn’t necessarily mean it will drop tomorrow.

The market can remain irrational longer than you can stay solvent.

For prices to collapse, you need to have one of two things to happen:

- Forced sellers

- Buyers to disappear

Forced Sellers for Singapore Property?

Because of ABSD and TDSR rules, recent buyers are not over leveraged.

This isn’t 1997 or 2007 where buyers have 5 or more properties each, financed mostly via leverage.

Most of the new buyers only have 1 – 2 properties max due to ABSD and TDSR requirements.

Even if they lose their job, they’re more likely to cut back on other expenses than to sell their house.

And for older buyers, they’re not so inclined to sell too because ABSD rules mean that they cannot buy back a new property easily.

So short term, it’s hard to see where the flood of sellers could come from.

Buyers of Singapore Property to disappear?

At the same time, the job market remains very tight.

Employees are still employed.

Foreigners are still coming in.

Wage growth is good.

Unless we have a sharp move up in unemployment, not easy to see demand from buyers disappearing overnight too.

So while prices may be on the high side here, it’s hard to see a sharp drop in property prices unless the Feds hike us into a deep recession.

Which may happen for sure.

But as of now, with the US economy reaccelerating and inflation picking up, we’re not at that point just yet.

But can prices keep going up longer term? Long Term Returns for Singapore Property?

But what if you’re buying for the long term?

Long Term returns for property will almost exclusively track GDP growth.

So it goes back to Singapore’s continued success as a financial centre.

Longer term, more housing supply will come online (whether from BTOs or new residential property).

While the ageing population will free up more housing supply (unless matched by an equivalent rise in immigration).

My views on Singapore Property Prices?

Personal views here – and I could definitely be wrong on this.

I don’t think you will see a sharp correction in Singapore house prices in the short term.

Rising interest rates are a potent headwind, but the tight supply situation will take time to work out – preventing a sharp drop in prices.

Without a flood of sellers, there just won’t be enough liquidity in the market to meet the demand.

But at these prices, I do think you’re pricing quite a fair bit of the future price increases already.

So you do need to be more realistic about long term returns buying at these levels.

Interestingly, prices dipped slightly in January 2023, but whether this is a one-off or whether it will be sustained is not clear:

Flash estimates from SRX and 99.co on Monday (Feb 27) showed that overall condo resale prices in January dipped 0.6 per cent month on month.

In the Rest of Central Region (RCR), prices were down 0.2 per cent. In the Outside Central Region (OCR), where prices have risen the most over the past year, they fell 1.2 per cent. However, prices in the prime Core Central Region (CCR) rose by 2.5 per cent in January from December.

Who should consider buying real estate as an investment?

To answer the question on what type of investors should consider buying real estate?

I think it will make sense for 2 types of investors:

- If you need a property to live in

- If you already have a lot of money

If you need a property to live in (don’t market time your house)

I’m not a fan of those strategies where you market time your primary residence.

You know, those who sell their property and rent a place, hoping to buy back cheaper down the road.

Yes, if you get it right you look like a genius.

If you get it wrong, you may end up without a home and priced out of the housing market.

Generally speaking, if you need a house to live in, just go ahead and buy one within your budget instead of trying to market time.

Save the market timing for your other investments.

If you already have a lot of money (wealth preservation)

If you already have a lot of wealth, then the considerations are different too.

Here you are looking primarily at wealth preservation, instead of wealth growth.

In which case I think Singapore residential property is fantastic.

Given the tightly regulated supply/demand situation of Singapore residential property, you probably won’t lose a lot of money long term.

Which is more than you could say if you put your money in any other asset class (or country).

What if you are building wealth?

What if you’re looking to build wealth instead.

Should you buy a property, or go with stocks / REITs?

What about Stocks / REITs?

First off – stocks / REITs is not really a fair comparison.

The universe of stocks / REITs is just so broad.

You can buy anything from a US oil exploration company to a China bank to a European logistics REIT.

If you’re a good stock picker, there is much, much, much more room to outperform in Stocks / REITs.

But real estate carries with it 75% leverage.

Nobody runs the same amount of leverage for Stocks / REITs.

So it’s just not a fair comparison.

For a 50 year old with 15 years horizon – property or stocks/REITs?

To answer the reader’s question.

I think it depends on your existing asset allocation, and your level of knowledge / expertise.

If you already have 3 houses in your family name, then maybe you don’t want to buy another and incur ABSD, while increasing your allocation to property.

But if property investing is your life and blood, and you don’t know the next thing about stocks, then okay I can see why another property would make sense.

I just don’t think we are living in the 2010s low interest rate regime anymore.

Nor are we living in the 1970s where Singapore will go from third world to first world status in 1 lifetime.

The “easy” returns for property are made.

Going forward into a regime of higher interest rates, the answer needs to be more nuanced.

You need to decide which is the best investment for yourself.

Based on your existing portfolio, and your level of knowledge.

What would I do – Buy Singapore Property or Not?

Long time FH readers should know that I have 2 private properties (1 in my name 1 in spouse’s name).

So it doesn’t make sense to buy a third and pay ABSD.

After accounting for ABSD, the returns won’t make sense.

And it will leave me overexposed to Singapore residential property.

At the same time it doesn’t make sense for me to sell my existing property because of the transaction costs to be incurred (agent fee, stamp duty etc).

And also because I intend it as a long term investment, not a market timing thing.

What if I didn’t own an investment property though?

What if I only owned 1 house that I was staying in today?

Would I decouple from my spouse to buy another?

Frankly – I don’t think I will.

I think at these prices, you’ve already priced in a lot of future returns.

And interest rates at this level is a potent headwind.

Buying a 3% cap rate property makes little sense to me in an era where the risk free interest rate is 4%.

Unless interest rates drop, you need to see a 33% rental increase just to reach fair value.

The fact that everyone is so bullish on property also makes me draw pause.

I mean just look at the story below.

Live through enough cycles, and you find that when the whole market is bullish on something, you usually want to think twice.

What is the alternative investment I would put money in?

That said, I don’t think stocks/REITs are sufficiently attractive given the higher risk free rates.

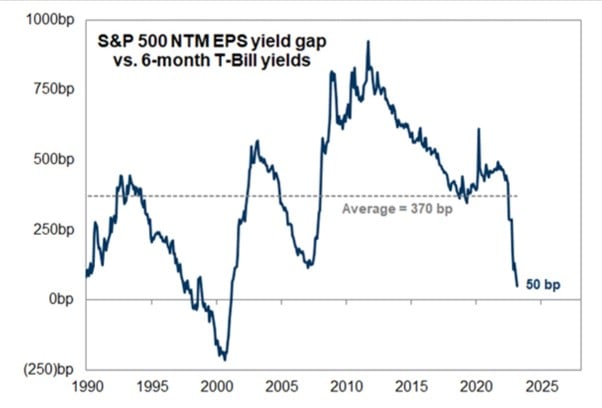

Look at the S&P500 EPS yield gap vs the 6 month T-Bills.

It’s the lowest it’s been since the Dot Com bubble.

Again, this doesn’t mean that the market will collapse tomorrow.

What it does mean though – is that the future returns are significantly reduced (if you buy at these prices).

In markets – there are times to play defensive, times to play aggressive.

With interest rates marching up, and valuations not coming down commensurately, I’m not that excited by asset valuations across the board.

I just don’t think risk assets (especially long duration assets) are priced properly given the higher risk free rates.

Not when I can get 4% risk free on a T-Bill – which might go even higher as 2023 plays out.

For now at least, I’m happy to sit mostly in cash, and let the market play itself out.

Either interest rates need to come down, or asset prices need to come down.

Looking at how hot the US job market and consumer spending is, I’m not sure if the former will happen.

As always, this article is written on 3 March 2023 and will not be updated going forward.

If you are keen, my full REIT and stock watchlist (with price targets) is available on Patreon, together with weekly premium macro updates. You can access my full personal portfolio to check out how I am positioned as well.

Running an Exclusive Promo for Stocks MasterClass now!

|

Learn:

|

Trust Bank Account (Partnership between Standard Chartered and NTUC)

Sign up for a Trust Bank Account and get:

- $35 NTUC voucher

- 1.5% base interest on your first $75,000 (up to 2.5%)

- Whole bunch of freebies

Fully SDIC insured as well.

It’s worth it in my view, a lot of freebies for very little effort.

Full review here, or use Promo Code N0D61KGY when you sign up to get the vouchers!

– Get up to USD 500 worth of fractional shares

I did a review on WeBull and I really like this brokerage – Free US Stock, Options and ETF trading, in a very easy to use platform.

I use it for my own trades in fact.

They’re running a promo now with up to USD 500 free fractional shares.

You just need to:

- and fund any amount

- Maintain for 30 days

Looking for a low cost broker to buy US, China or Singapore stocks?

Get a free stock and commission free trading .

Get a free stock and commission free trading with .

Get a free stock and commission free trading with .

Special account opening bonus for Saxo Brokers too (drop email to [email protected] for full steps).

Or for competitive FX and commissions.

Do like and follow our Facebook and Instagram, or join the Telegram Channel. Never miss another post from Financial Horse!

Looking for a comprehensive guide to investing that covers stocks, REITs, bonds, CPF and asset allocation? Check out the FH Complete Guide to Investing.

Or if you’re a more advanced investor, check out the REITs Investing Masterclass, which goes in-depth into REITs investing – everything from how much REITs to own, which economic conditions to buy REITs, how to pick REITs etc.

Want to learn everything there is to know about stocks? Check out our Stocks Masterclass – learn how to pick growth and dividend stocks, how to position size, when to buy stocks, how to use options to supercharge returns, and more!

All are THE best quality investment courses available to Singapore investors out there!

Dear FH

Incisive analysis, as usual

Add in the income tax and non-occupier property tax plus condo monthly maintenance and it becomes a no brainer – except for the very rich who need “diversification “ and also for those who want to prepare to pass their wealth to the next generation imminently !

For the rest of the salaried folks, it makes little sense to buy even without leverage!

For someone who needs their first house and intend to live there, it is of course the best thing

You very accurately pointed out the link between GDP and house prices and unless there is a major economic or Geo-political event, house prices will trudge upwards in land scarce SG. Also, our “aspirational” buyers will always be fond of upgrading to Condos and this will act as a floor for prices and rents

Long term owner- occupiers- best thing to do

Not for creating passive income as the yield on investment will be under 2% even without leverage after accounting for all outgoings etc etc

Regards

Garudadri

Very much agreed!

I think the analysis would have been different just 1 – 2 years ago, when interest rates were stuck at zero bound and a wave of inflation looming.

But today, with the risk free at 4% and prices having gone up so starkly, I’m a lot less optimistic about the risk-reward.

Yes sure, long term the prices will still go up. But at these prices you’re already baking in a fair bit of future returns, while higher interest rates make the investment a more tricky one.

Thanks.

I am having the similar situation as you. we have 1 HDB, 2 small private units rented out (decoupled)

I have built up some cash again, and I am hesitating whether to bite the bullet to buy another private.

Will you do that?

have not found any other asset class which is safter/better than SGP properties.

Well I can’t comment for your personal situation, as this is ultimately a personal decision.

For me I probably won’t be buying. Once you add ABSD in, and at these prices, I think returns may not be so attractive.

I’m mostly heavy cash now, but I do expect to be deploying most of that cash into stocks/REITs eventually as this cycle plays out.

Hi FH, big fan of your analysis! Just a question, don’t you think that the government will step in if property prices drops too much? Letting Singaporeans see their property lose value will impact the government negatively especially with elections looming. I acknowledge your points regarding headwinds, but governmental intervention is a huge tailwind for Singapore property.

Yes – absolutely agree. Which is why I dont see a sharp decline in property prices too.

It’s the thing about valuations right. You can crunch the numbers and realise that valuations are on the high side. But it doesn’t mean prices will drop in the next few months.