A bit of background.

If you are a regulator, and you are going to close a bank on Friday.

You better have something ready to announce by Monday morning, to prevent a broader bank run.

In my weekend articles, I wrote that historically speaking – a buyout is the most common path taken.

In a buyout, you get a JP Morgan to buy Silicon Valley Bank for cents on the dollar, while the Treasury provides a Federal Guarantee to cover the losses.

Buyout failed because US Government refused to foot any losses

As it turns out, the buyout option failed because the US Government refused to cover any portion of the losses (for political reasons).

Here’s the reporting from the FT:

Neither SVB nor Signature — leading lenders for the start-up community and cryptocurrency industry — was likely to be acquired by a rival bank as all the potential buyers had so far walked away, said people with direct knowledge of the negotiations and who have been working with SVB and the government.

PNC, a large US bank, and Canada’s RBC were invited to buy SVB but decided against bidding, said people with direct knowledge of the matter.

America’s five largest banks, including JPMorgan and Bank of America, would also not be buyers, these people said.

For a transaction to make sense for any buyer, the US government would be required to cover part of their losses, said a person working with SVB.

Fair enough, in situations like that if the Treasury doesn’t want to backstop losses, it would be tough to find a buyer to buy out the bank wholesale (because you don’t know what kind of liabilities you’re taking on – it’s a black box as there is no time for extensive due diligence).

FYI that this is an important point to note, because it gives you an idea of what the political stance from the Biden administration is – namely that post 2008 there is a lot of sensitivity around using taxpayer dollars to bail out bank shareholders and bondholders.

This will have big implications as we progress in this rate hike cycle and bigger stuff breaks.

So the US Government doesn’t want to be seen using taxpayer’s moneys to cover the losses, but the deposits still have to be made whole to prevent a broader bank run.

What next?

This is a premium Patreon post. I am making it available to all readers in the hopes that this might help you make sense of what is going on.

If you find this useful, do support Financial Horse as a Patreon. You can get regular premium updates just like this, together with my full REIT and stock watchlist.

Sign up here.

Joint Statement from the Treasury, Federal Reserve, and the FDIC

Here’s the Joint Statement from the Treasury, Federal Reserve, and the FDIC (full link here):

There are effectively 3 parts to the “Bailout”:

- All Depositors will be made whole

- Shareholders and bondholders will be wiped out

- Additional Funding Programs from the Feds

All Depositors will be made whole

Extract from the statement below:

“After receiving a recommendation from the boards of the FDIC and the Federal Reserve, and consulting with the President, Secretary Yellen approved actions enabling the FDIC to complete its resolution of Silicon Valley Bank, Santa Clara, California, in a manner that fully protects all depositors. Depositors will have access to all of their money starting Monday, March 13. No losses associated with the resolution of Silicon Valley Bank will be borne by the taxpayer.”

Basically, all depositors will be made whole.

No haircut on the deposits.

If you held $100 million with Silicon Valley Bank on Friday, you will get access to $100 million on Monday (despite only $250,000 being FDIC insured)

Note how careful they were to stress that “no losses will be borne by the taxpayer”.

This is a political issue.

I suppose the question then is that if the taxpayer is not covering the losses, who is covering the losses?

Shareholders and bondholders will be wiped out

Per the joint statement:

“Shareholders and certain unsecured debtholders will not be protected. Senior management has also been removed. Any losses to the Deposit Insurance Fund to support uninsured depositors will be recovered by a special assessment on banks, as required by law.”

A big political statement here.

In line with taxpayers not covering any losses, they want to make it clear that shareholders and bondholders will be wiped out.

This is in line with the sentiment post-2008, where depositors will be made whole, but shareholders and bondholders will not be bailed out using taxpayer funds again (avoiding a big criticism of the 2008 bailout).

I suppose it’s easy to stick to your principles when it’s a regional bank like Silicon Valley Bank, I doubt this would be the case if it were a Bank of America going under.

Who is really footing the bill here?

To answer the question of who is really footing the bill here.

The shareholders and bondholders are probably going to be wiped out, so they will take significant losses.

And any remaining losses will be paid from the insurance fund that is capitalized by premiums paid by banks. Basically, it will be paid out of insurance that is paid for by all of the banks in the US.

But practically speaking, this was a liquidity problem, not a solvency issue.

Most of the underlying assets haven’t really gone bad, so the ultimate losses here are likely to be minimal.

But note how the handling of this was designed specifically so that taxpayers would not have to foot the bill.

Additional Funding Programs from the Feds

And finally the big one:

“Finally, the Federal Reserve Board on Sunday announced it will make available additional funding to eligible depository institutions to help assure banks have the ability to meet the needs of all their depositors. “

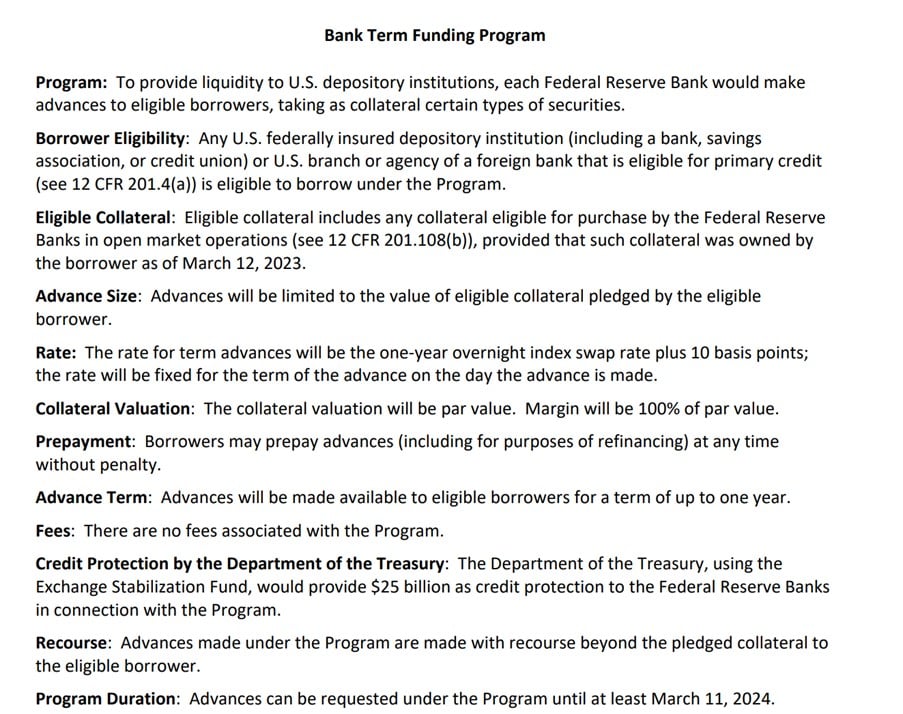

The Feds are announcing a new funding program, called the Bank Term Funding Program (BTFP) to backstop liquidity needs in the banking sector.

What is Bank Term Funding Program (BTFP)

You can refer to the press release from the Feds for the full details.

I extract the key highlights below:

“The additional funding will be made available through the creation of a new Bank Term Funding Program (BTFP), offering loans of up to one year in length to banks, savings associations, credit unions, and other eligible depository institutions pledging U.S. Treasuries, agency debt and mortgage-backed securities, and other qualifying assets as collateral. These assets will be valued at par. The BTFP will be an additional source of liquidity against high-quality securities, eliminating an institution’s need to quickly sell those securities in times of stress.

With approval of the Treasury Secretary, the Department of the Treasury will make available up to $25 billion from the Exchange Stabilization Fund as a backstop for the BTFP. The Federal Reserve does not anticipate that it will be necessary to draw on these backstop funds.”

Exact details of the program below:

What is Bank Term Funding Program (BTFP) in plain English?

Think of it this way:

- You bought US Treasuries in 2021 at $100

- These Treasuries are now worth $90 on the open market (due to interest rate increases)

- Now you need $100 back, but you don’t want to sell it on the open market because you will get $90 only

- You can now deposit the Treasuries with the Feds, who will give you a loan for $100

- You do need to pay interest on the loan though

In plain English, the Feds will loan you money equivalent to the par value of your Treasuries.

So you don’t need to sell them on the open market and realise the mark to market loss.

Had this been in place last week, Silicon Valley Bank would not have failed

Just for the record – had this been in place last Friday, Silicon Valley Bank would not have failed.

And this BTFP, basically prevents a second Silicon Valley Bank from playing out, as banks will no longer have liquidity problems arising out of mark to market losses on Treasuries.

At least for the next 12 months, until this Bank Term Funding Program runs out.

What are the implications?

In simple English:

- Depositors at Silicon Valley Bank will take no losses.

- Shareholders / Bondholders get wiped out.

- New measures put in place by the Feds to prevent a repeat of Silicon Valley Bank for the next 12 months.

All fine and dandy?

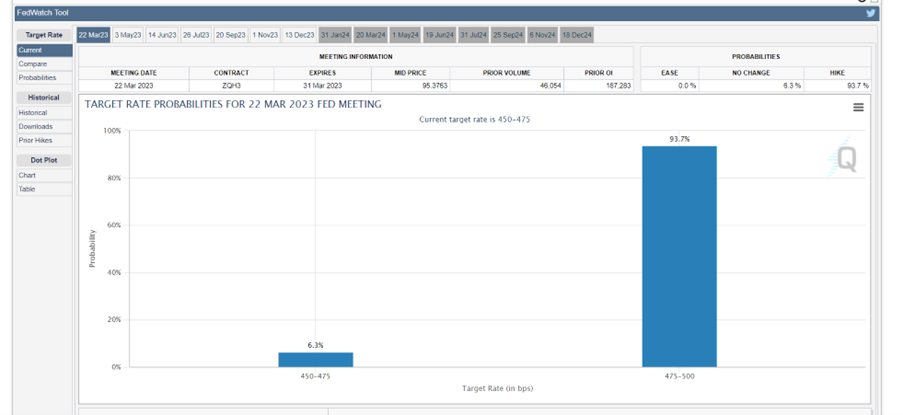

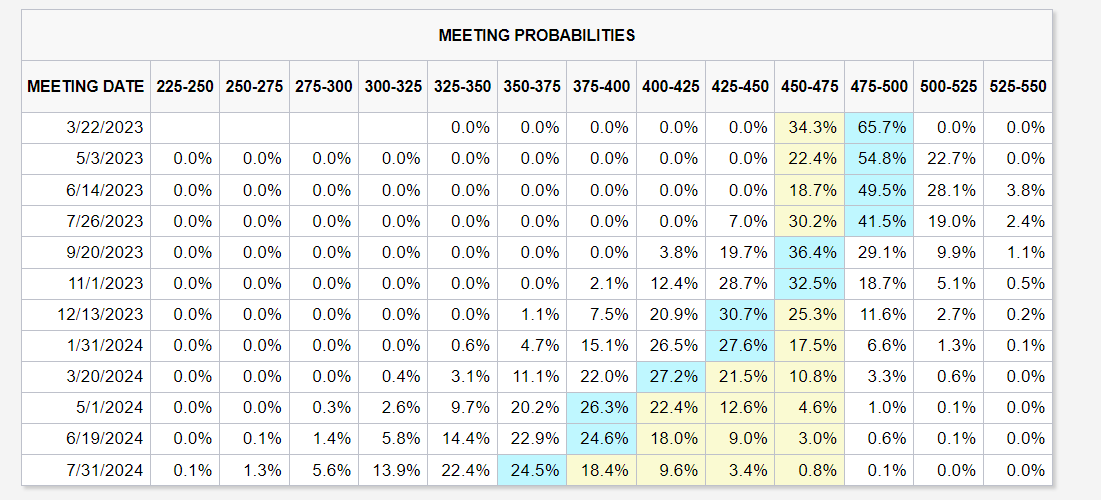

What was the market reaction? – 100% of 25bps hike, and Terminal Rate of 5.25% (vs 5.75%)

The market reaction to this news is very interesting.

Whereas a day ago we were looking at 60%+ probability of a 50 bps hike at the March FOMC.

The market is now pricing in a 93% chance of a 25 bps hike.

With a 6% chance of no rate hikes at all.

Terminal interest rates have also plunged from 5.75% to 5.25%.

Effectively, the market took 2 whole interest rate hikes off the table as a result of this “bailout”

Goldman is now calling for no interest rate increase in March.

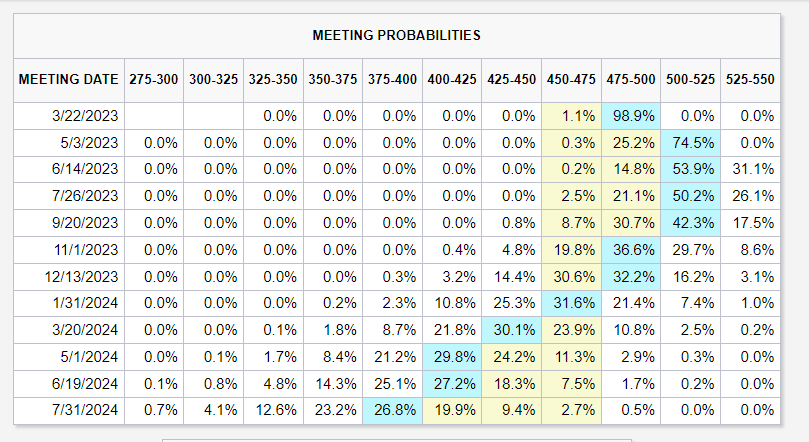

Update (730pm 13 March) – Well market moves fast, because as of 730pm, here’s the latest market pricing.

Market is now pricing in only a 65% chance of a 0.25% rate hike in March.

And get this straight – market thinks 1 rate hike from here and the Feds are done.

Interest rate cuts forecasted for second half of 2023…

If this market pricing is correct, I shudder to think what’s going to happen next to inflation.

Is this a “Pivot”, or kicking the can down the road?

Is this response is justified?

With this “Bailout”, depositors are made fully whole again.

While the “Bank Term Funding Program” puts in place contingencies to ensure that no other bank will run into a liquidity issue because of mark to market losses on Treasuries.

With this in place, the short term panic should be contained.

Look at how strong futures are rallying.

Does this necessarily justify taking 2 whole rate hikes off the table?

If it does – what happens when inflation comes roaring back?

Personal view – I don’t see this as a Fed “Pivot” in the sense that we are back to QE and easy money.

I see this as the Fed doing what it takes to prevent short term liquidity issues from blowing up.

Ie. They are kicking the can down the road.

A bank failed, the Treasury didn’t want to backstop losses so nobody bought the bank, so the Feds stepped in to make depositors whole and prevent a broader bank run.

That’s literally the function of the Feds.

I’m not sure this changes that much on inflation.

But I’m not stubborn enough to insist on my views. Let’s watch how things play out the next few days, and respond accordingly.

February CPI numbers come out on Tuesday, that will be crucial to watch for the Fed’s position on rate hikes.

Should one sell DBS Bank Stock and Astrea Bonds?

I’ve been getting some questions on whether one should sell DBS Bank Stock / Astrea Bonds.

Let me just share some general views here.

You should ask yourself if you are making this decision based off of:

- Silicon Valley Bank’s failure and it’s direct effects

- Silicon Valley Bank as a wake-up call that sheds light on the broader risks in play here.

On (1) – I said over the weekend that I don’t see direct systemic risk arising out of Silicon Valley Bank’s failure.

A lot of the factors are unique to Silicon Valley Bank, and as of now there is no broader cross asset contagion.

With the “Bailout” from the Feds, the risk of immediate contagion went down a whole lot.

But if your concern is more on (2).

That after Silicon Valley Bank you have started to realise that many investors over the past decade have been making bets on low interest rates lasting forever.

And that the rapid rise in interest rates threatens to upend that entire sector of the financial economy.

And that if you mark a lot of investments including private real estate, VC or PE to market prices (based on current levels of interest rates), you don’t know who’s actually solvent or not.

Then well – that’s exactly what I’ve been saying for a while, and that’s a wholly different question.

As the Warren Buffet quote goes – only when the tide goes out do you discover who’s been swimming naked.

Personal view – I don’t see contagion arising from Silicon Valley Bank directly.

But I doubt if Silicon Valley Bank is the biggest thing to break this cycle.

I still see the Feds continuing to keep at it, until something big enough breaks that forces them to pivot.

But let’s see.

This is a premium Patreon post. I am making it available to all readers in the hopes that this might help you make sense of what is going on.

If you find this useful, do support Financial Horse as a Patreon. You can get regular premium updates just like this, together with my full REIT and stock watchlist.

Sign up here.

Trust Bank Account (Partnership between Standard Chartered and NTUC)

Sign up for a Trust Bank Account and get:

- $35 NTUC voucher

- 1.5% base interest on your first $75,000 (up to 2.5%)

- Whole bunch of freebies

Fully SDIC insured as well.

It’s worth it in my view, a lot of freebies for very little effort.

Full review here, or use Promo Code N0D61KGY when you sign up to get the vouchers!

– Get up to USD 500 worth of fractional shares

I did a review on WeBull and I really like this brokerage – Free US Stock, Options and ETF trading, in a very easy to use platform.

I use it for my own trades in fact.

They’re running a promo now with up to USD 500 free fractional shares.

You just need to:

- and fund any amount

- Maintain for 30 days

Looking for a low cost broker to buy US, China or Singapore stocks?

Get a free stock and commission free trading .

Get a free stock and commission free trading with .

Get a free stock and commission free trading with .

Special account opening bonus for Saxo Brokers too (drop email to [email protected] for full steps).

Or for competitive FX and commissions.

Do like and follow our Facebook and Instagram, or join the Telegram Channel. Never miss another post from Financial Horse!

Looking for a comprehensive guide to investing that covers stocks, REITs, bonds, CPF and asset allocation? Check out the FH Complete Guide to Investing.

Or if you’re a more advanced investor, check out the REITs Investing Masterclass, which goes in-depth into REITs investing – everything from how much REITs to own, which economic conditions to buy REITs, how to pick REITs etc.

Want to learn everything there is to know about stocks? Check out our Stocks Masterclass – learn how to pick growth and dividend stocks, how to position size, when to buy stocks, how to use options to supercharge returns, and more!

All are THE best quality investment courses available to Singapore investors out there!

Hi FH, I’m new to this, so this might be a very obvious question to you, but why did HSBC acquire the UK subsidiary of SVB? Like you mentioned above, there’s no time for HSBC to conduct thorough research, the amount of liability HSBC could be taking is unknown. HSBC CEO said it will strengthen their commercial bank business, which is true, but the risk taken on by HSBC seems unneccessarily huge. I appreciate all feedback!

It’s a bit of a risk-reward kind of analysis.

Yes there’s no time for extensive due d, but based off public figures you can kind of guess that the hole in their books isn’t that big (this isn’t FTX).

I suppose HSBC weighed the risks in light of getting SVB’s banking relationships (especially with the UK tech / biotech sector), and decided it was worth it!

measured and balanced article, many thanks.

No worries, glad it helps!

hi FH, why do you think HSBC acquired Silicon Valley Bank’s UK subsidiary? Like you mentioned above, there isn’t time for a comprehensive analysis of SVB. The CEO said it will strengthen their commercial banking ops, but isn’t HSBC taking on a unnecessarily huge risk given the unknown liabilities surrounding SVB?

It’s a bit of a risk-reward kind of analysis.

Yes there’s no time for extensive due d, but based off public figures you can kind of guess that the hole in their books isn’t that big (this isn’t FTX).

I suppose HSBC weighed the risks in light of getting SVB’s banking relationships (especially with the UK tech / biotech sector), and decided it was worth it!

Dear FH,

I have a question for you that is not related to the above SVB saga. However i am not sure where to send this question to you therefore i type it here. Sorry about it.

In today Straits Times page A20, there is an article on a SGX listed property developer company “Hong Fok”. The writer commented that this company

– Dividend payout is very little dividend

– They pay their director fat salary

– The NTA per share is about $3.45 and current share price is about $1

The writer concluded that for any investor who want some exposure on property stock can consider this stock.

What i do not understand is why would any retail small time investor like myself would consider a stock like this that has history of paying low dividend and stock price does not seems to be able to rise?

Hope you can help me understand the logic of the writer recommendation.

Thank you

Hi aaa,

Unfortunately I don’t follow this stock (or this writer) so it’s hard for me to comment.

Many reasons come to mind – ranging from potential conflicts of interests to the more innocent (maybe he really does like the stock)!

Whatever the case, I would never buy a stock simply based on what I read in the newspapers – I would still do my due dilligence on it. 😉

Dear FH,

Thank you for taking time to reply me. I appreciate it. Agree totally that due diligence is still a must.

Cheers