Following my previous article on SingTel, a reader suggested to me that I should do a follow up article on Starhub and M1. When I saw her comment, I knew instantly that she was right. Reviewing SingTel in isolation without taking a corresponding look at Starhub and M1 would be an incomplete analysis.

Basics: Starhub

Starhub is one of 3 major telecommunications (telco) operators in Singapore, alongside Singtel and M1. Unlike SingTel, Starhub gets all of its revenue from Singapore.

From their corporate website, they describe themselves as:

StarHub is a leading homegrown Singapore company that delivers world-class communications, entertainment and digital solutions. With our extensive fibre and wireless infrastructure and global partnerships, we bring to people, homes and enterprises quality mobile and fixed services, a broad suite of premium content, and a diverse range of communications solutions. We develop and deliver to corporate and government clients solutions, such as artificial intelligence, cyber security, data analytics, Internet of Things and robotics. We are committed to conducting our business in a sustainable and environmentally responsible manner. Launched in 2000 and listed on the Singapore Exchange mainboard since 2004, StarHub is a component stock of the Straits Times Index, the SGX Sustainability Leaders Index and the SGX Sustainability Leaders Enhanced Index.

The Ugly

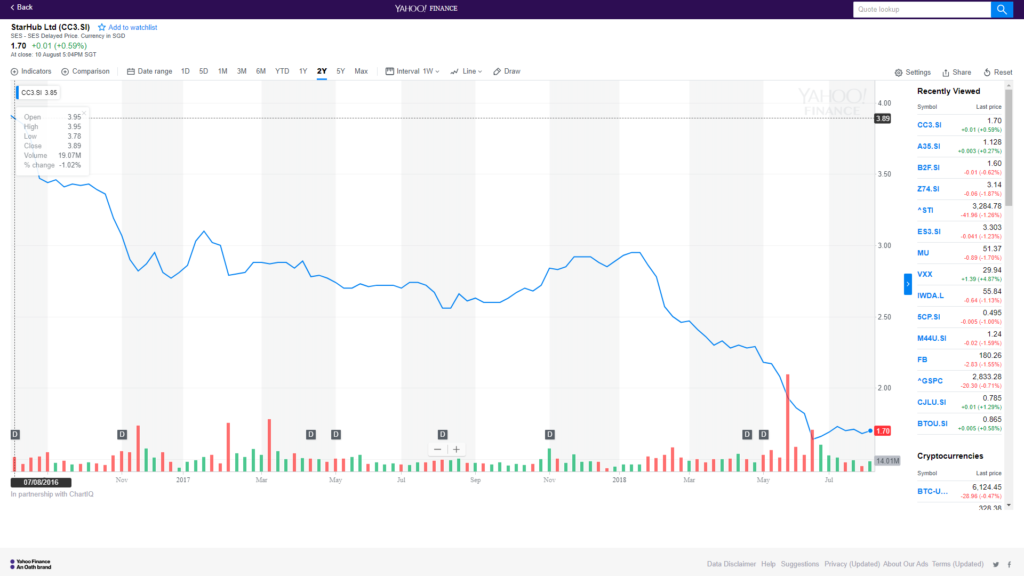

Share Price

Whatever way you look at it, the share price is an unmitigated disaster. It went from about S$4 two years ago to the current price of S$1.70, which is a glorious destruction of shareholder value, to say the least.

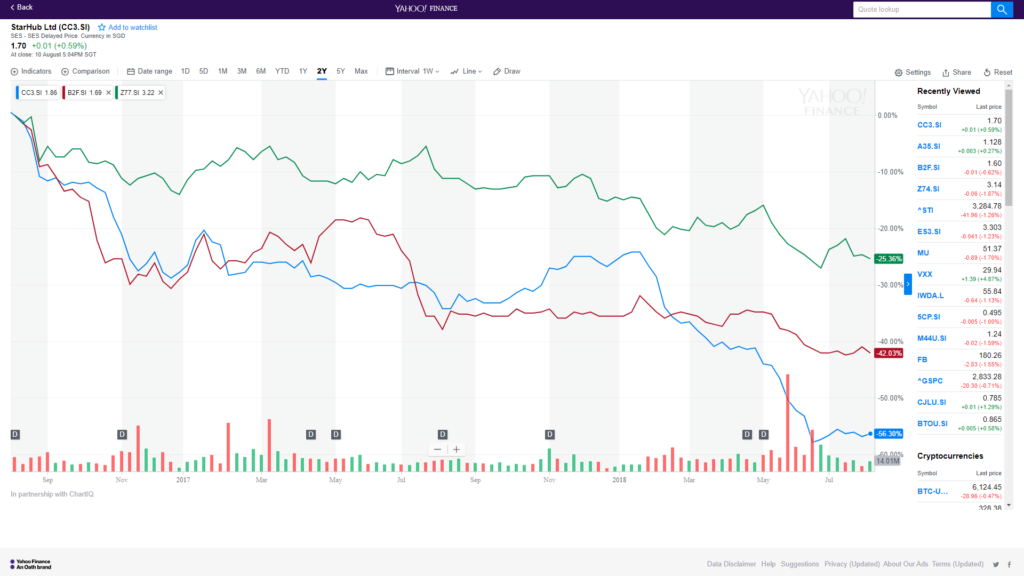

If you overlay the performance against M1(Red) and SingTel (Green), it actually looks even worse, because Starhub’s performance is by far the worst of the 3.

What happened, Starhub?

The telco business has fallen on hard times. Phone technology is starting to peak, with incremental upgrades between new phone upgrade cycles. These days, a 3 year old iPhone can perform almost all the functions a brand new iPhone can. At the same time, the rise of Xiaomi, Huawei and a host of other low cost phone brands from China have made it incredibly cheap to get a high end smartphone for a fraction of the cost of an Apple or Samsung phone. As a result, the need to re-contract at the end of every 2 year contract is getting a lot less compelling, and many of us are choosing to use a SIM only plan instead, or switch to a lower cost monthly plan. This translates to lower margins and lower Average Revenue Per User (ARPU) for the telcos.

At the same time, the government has decided that Singapore needs greater competition in the telco space, and decided to bring in a new telco in TPG Telco. They’re slated to launch in second half of 2018, so about anytime now. Once TPG Telco launches, I expect aggressive competition from TPG as they attempt to steal market share from the other 3 players. Singtel, Starhub, M1 are not going to sit around and watch that happen, so they are going to respond in kind, which will impact margins and ARPU even further. The local telco market is only so big, and unless TPG telco can grow the amount of total subscribers (I don’t see how they can, that’s population growth which is a government policy thing), whatever TPG telco gains, Singtel/Starhub/M1 loses. It’s likely to be a race to the bottom, and while that’s great for consumers, it’s not going to be pretty for margins.

The first 2 factors apply to all 3 local Telcos. But what caused Starhub to be hit so badly, is their emphasis on Pay TV. Many years ago in the early 2000s, I remember going with my parents to a PC Show to sign up for a cable TV package to catch the world cup. Those were the golden days of Pay TV. We’ve come a long way since then, and these days during every family gathering, our favourite topic is about which relative finally decided to stop subscribing for cable TV, and what took them so long?! In the 2000s, Discovery Channel and HBO were all the rage. These days, Discovery Channel (which Starhub no longer has due to a dispute over fees) and HBO can easily be supplanted by YouTube, Netflix, and I really shouldn’t be saying this but let’s get real, piracy. Starhub leveraged their “Hubbing” strategy very hard, which packaged TV, Broadband, and Phone lines together, and the cord-cutting really hit their top line.

It truly has been a perfect storm for Starhub, with a confluence of factors that resulted in the eroding of their business model, and share price.

Top line growth

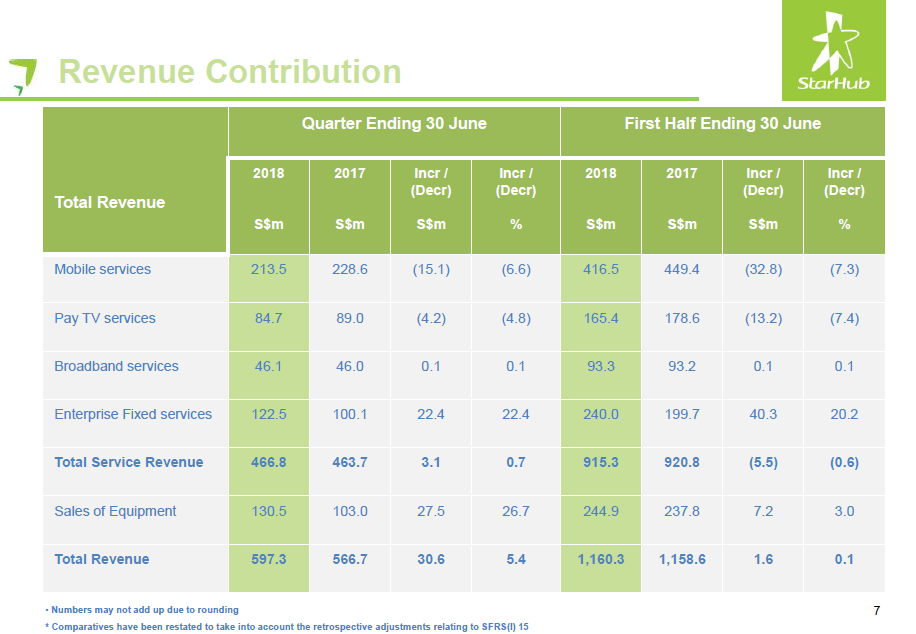

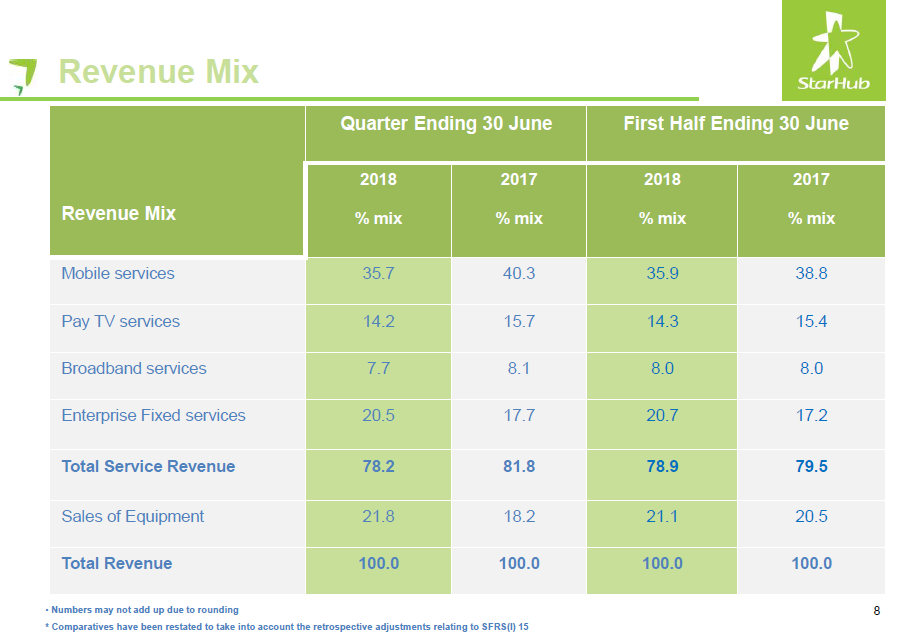

The financial numbers play out a similar story. Mobile revenue and Pay TV have been badly hit, down about 7% on a year on year basis. Broadband revenue is flat. Enterprise Fixed Services is up 20%, but this was largely due to consolidation of ASTL and D’Crypt (which Starhub bought recently) driving up revenues from managed services, so I wouldn’t read too much into it.

Mobile and Pay TV collectively make up about 50% of Starhub’s revenue, so the coming impact due to TPG Telco is likely to be huge. I do acknowledge that they’ve been trying to branch out into Enterprise Fixed Services through their recent purchase of Accel Systems & Technologies Pte Ltd (ASTL) and D’Crypt, but the added contribution from these guys is unlikely to make up for the decline in their core businesses once TPG comes into play.

If I were to summarise their business outlook simply over the next 12 month, it would probably be this: Revenue from Mobile Services and Pay TV are likely to see high single digit declines, possibly even higher depending on how aggressive TPG Telco is and how the 3 local players respond. Broadband is likely to stay flat, because there really isn’t much incentive to move to another player, although business strategy may change. Enterprise Fixed Services is likely to be the only bright spot, with low single digit increases.

Dividend Yield

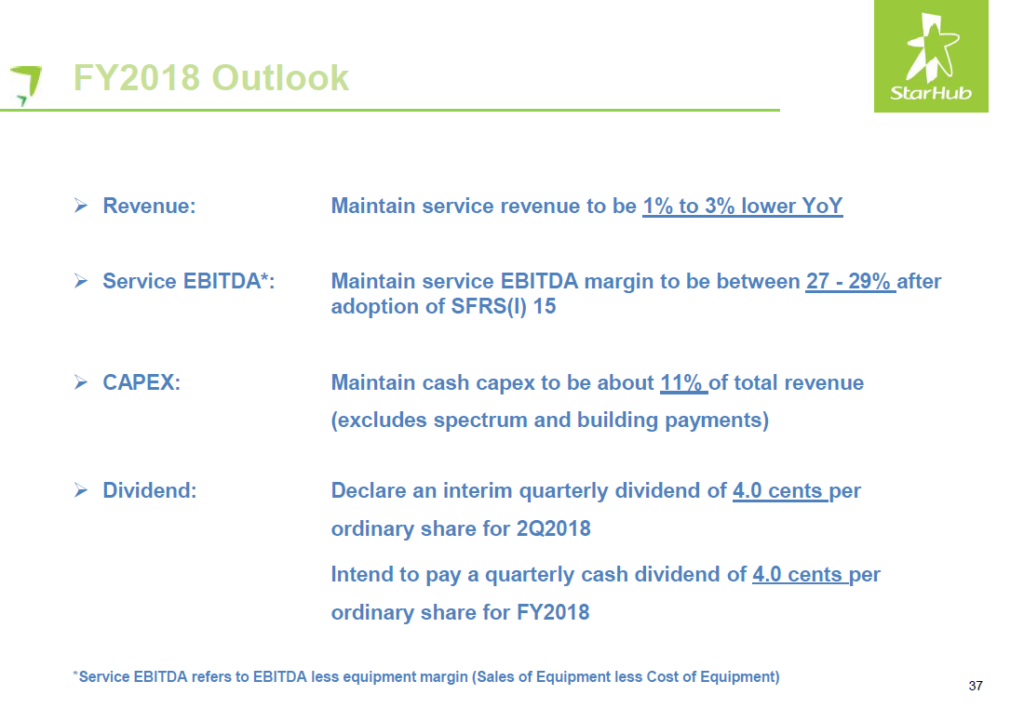

Starhub is currently committed to paying out a cash dividend of 4 cents per quarter. I couldn’t really believe this myself, so I went to pull up the slide to confirm my eyes weren’t playing tricks on me. At 4.0 cents per quarter, that works out to 16.0 cents a year, which at the latest price of S$1.70, is a mind blowing 9.4% dividend yield.

I’ve always said that when something is too good to be true, it probably is. If Starhub were paying a sustainable 9.4% dividend on stable cashflow, I would be dumping my life savings into this share (together with just about every investor out there), and the share price would jump. For comparison, Netlink Trust trades at about a 5.8% to 6% yield with a very sustainable cashflow, so that should give you some indication of the kind of risk premium we are looking at here.

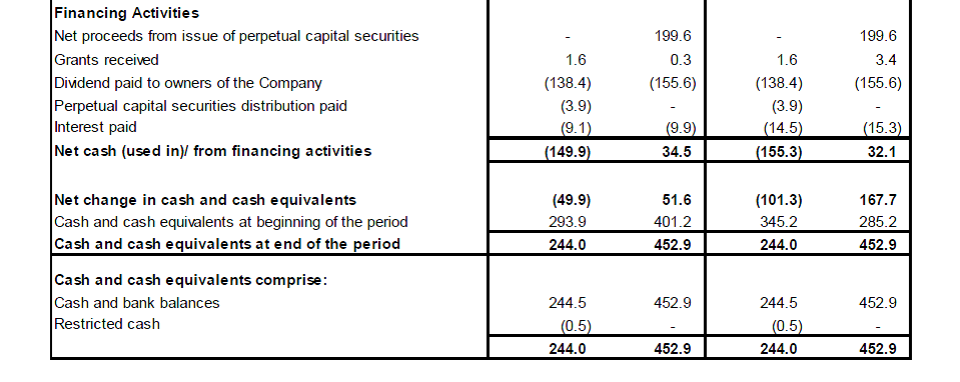

Anyway, I dug deeper into the numbers, and it turns out they’re actually burning through about S$50 million per quarter by maintaining their existing dividend policy. There’s 244.0 million cash left as at 30 June 2018, so if we assume that they don’t take on new financing to pay dividends, they can maintain the existing dividend for another 5 quarters before they deplete their cash position entirely.

DBS Research probably summarises it better than me when they say:

We expect sharp cut in dividends in FY19F. StarHub has committed to a payout of S$277m in annual dividends in FY18. We estimate that StarHub’s shareholder equity value will be wiped out in 2020 if it continues with similar magnitude of dividends. We project that StarHub will bring down its dividends to match the net profit level. While we have assumed 100% payout ratio from FY19F onwards, StarHub should, ideally, retain some earnings to invest in new business opportunities in our view.

If we assume that Starhub cuts their dividend down to the point where they are cash flow neutral, it implies about a 35% cut in dividend to a 6.0% yield. That’s actually still very respectable, and I suspect that’s what the market is pricing in. I am mind blown that Starhub doesn’t immediately cut their dividend, but continues to burn through S$50 million of their cash reserves each quarter, when as DBS pointed out, they could easily be deploying this cash into their core business.

Bottom line, don’t buy this stock expecting a 9.4% dividend. It will get cut, the only question is when, and how much.

The Good

Enterprise Services

I talked about Enterprise Services a bit earlier, so I won’t dwell too heavily on it. Unlike Mobile and Pay TV, Enterprise Services will probably see low single digit growth, and the new acquisitions of D’Crypt (a cybersecurity company) indicates that Starhub (much like SingTel) is looking to branch out into these areas. Cybersecurity is still a growing market very much in its infancy, and as the recent SingHealth hack shows, there is huge requirement for such services going forward. Starhub is certainly making efforts to go into this space, but as always, the devil is in the details. Whether they can execute on their strategy remains to be seen.

MVNOs

Mobile virtual network operator (MVNO) are operators that don’t own the wireless infrastructure, but rent it from an existing player. In Singapore, they include Circles.Life (partners with M1) and MyRepublic (partners with Starhub).

DBS Research summarises this point very well:

While StarHub has struck a MVNO partnership with MyRepublic, which could support the telco’s contracting mobile business, we believe it could take at least 1-2 years before StarHub records any meaningful contributions from MyRepublic.

Buyout

My personal view is that Starhub is going to face incredible challenges in its business going forward. The slowing of the phone upgrade cycle, the shift to SIM only plans, the cord-cutting, and the entry of TPG Telco are truly a perfect storm for Starhub. I suspect that management will try to compete over the next few quarters, but if things do indeed get a lot worse, what other options are on the table?

One potential way out, that has been mooted many times for M1, is a buyout strategy. After TPG comes in for a while, grabs market share, and after the dust settles into a 4 player telco market in Singapore, the person who buys over Starhub can instantly boost their market share significantly. If executed properly, and at the right price, such a buyer can also enjoy significant synergies and cost efficiencies.

Starhub currently has a market cap of S$2.94 billion vs M1’s S$1.48 billion. If its share price were to decline further, we could be looking at a market cap in the low S$2 billion range, which is actually pretty reasonable.

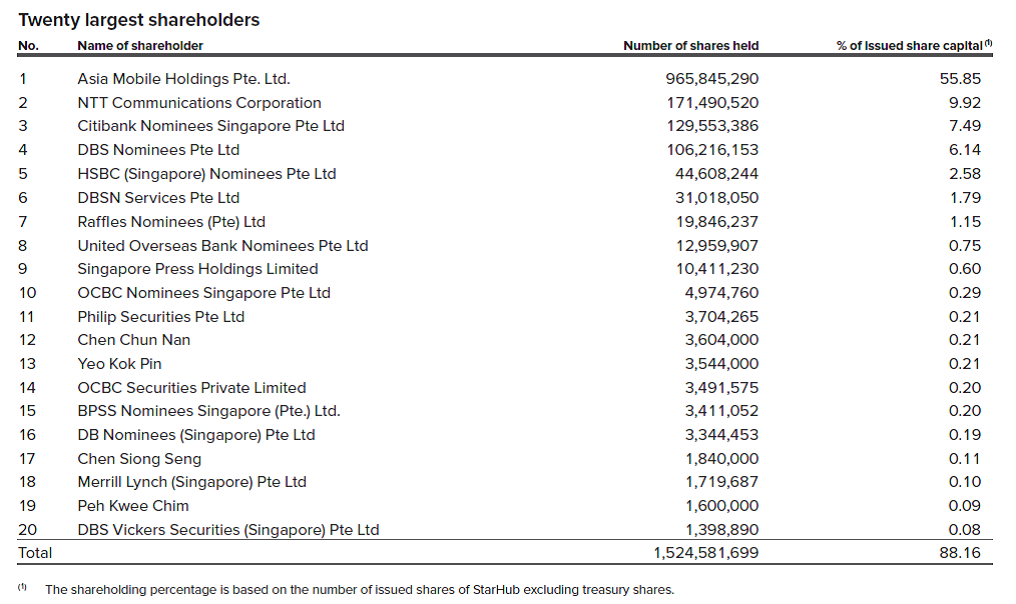

The single largest shareholder of Starhub is Asia Mobile Holdings Pte. Ltd., which is a jointly owned by ST Telemedia (parent company is Temasek) and Ooredoo (a Qatari telco group). If the price is right, and with the right moves from Temasek, a merger with another existing player may not necessarily be a bad idea.

The problem with playing a buyout strategy for a company with a declining core business, is that timing is everything. To illustrate, assume that you buy in at S$1.70, and over the next 12 months the price collapses to S$1.00. SingTel steps in with a buyout offer at a massive 50% premium to market price, which works out to S$1.50. So yes, you were right about the buyout, but because you got the timing wrong, you still lost money.

What is a fair value of Starhub?

DBS Research attempted a fair value analysis of Starhub, and they reached the following conclusion:

Maintain HOLD with an unrevised TP of S$1.42. Due to a lack of clarity on future free cash flows, we switch to peer multiple based valuation. We value StarHub at 12-month forward EV/EBITDA of 5.6x, which is at ~20% discount to the 7x regional average.

If we assume that StarHub revises their dividend policy to be cash flow neutral (ie. 100% payout ratio), that’s about a 7% yield on DBS’s target price of S$1.42. I’m not convinced that I would be keen to buy StarHub at that price.

Closing Thoughts

With SingTel, I made it very clear that my line in the sand was a 6.0% yield. If SingTel fell to the S$2.9 range (latest price is S$3.15), implying a 6.0% dividend yield, I would consider deploying some capital into SingTel. With Starhub though, I’m not confident enough to make the same statement. The core business is in a pretty tough spot, and there’s just too much uncertainty for me here. I really need to wait and see how TPG Telco plays out, before making any decision on Starhub. At the same time, I suspect that the number of Pay TV subscribers will eventually stabilise, but I have no idea what that number is, and how long it would take to get there.

Bargain hunters with a healthy risk appetite may choose to go in and play the rebound, and that’s absolutely fine. Do be careful with the dividend cut though. This typically causes share prices to drop further, but with the current negativity around this stock, it may well have already been priced in. Only time will tell.

Financial Horse Rating – Starhub

![]()

![]()

Financial Horse Rating Scale

Financial Horse has a set of 7 Commandments for Successful Investing, that I ask myself before making every investment, and that I will never break regardless of the situation. Enter your email below to receive a copy in your inbox!

[mc4wp_form id=”173″]

Enjoyed this article? Like our Facebook Page for more great articles, or join the Facebook Group to continue the discussion!