As you have probably heard by now, the latest T-Bills yields fell to 1.85%.

At 1.85% suddenly T-Bills no longer look that attractive.

And fixed deposits start looking pretty attractive once again.

But – will this change down the road? Will banks start to slash their fixed deposit rates?

Couple of points I wanted to discuss:

- What are the Top Fixed Deposit Rates in Singapore today (July 2025)?

- What are the alternatives to Fixed Deposit? T-Bills a better buy?

- Where would I put my cash today?

Top Fixed Deposit Rates in Singapore offer 2.45% yield (July 2025)

The full table is further below in the article, but I’ve summarised the best interest rates for the 3-, 6- 9- and 12-month tenures below.

You’re looking at 2.15% for the 6 months tenure.

And 2.45% for the 12 months tenure.

Which very interestingly – is offered by DBS Bank.

| Tenure | Best fixed deposit interest rate (July 2025) | Bank |

| 3 months | 1.95% | Bank of China |

| 6 months | 2.15% | DBS/POSB |

| 9 months | 2.35% | DBS/POSB Bank |

| 12 months | 2.45% | DBS/POSB Bank |

DBS Bank’s 2.45% Fixed Deposit rate just looks very attractive in this climate.

Only problem is that the maximum you can deposit is $19,999:

Best Fixed Deposit Rates yield 2.10% if you deposit with Syfe Cash+ (to access institutional fixed deposit rates)

The rates above are assuming that you deposit with the bank directly as a retail customer.

Another way to do it is to use Syfe Cash+ Guaranteed.

The way this works is that you park the cash with Syfe, who will then deposit the cash into an institutional fixed deposit account.

This allows you access to institutional fixed deposit rates.

While these institutional fixed deposit rates are usually higher than retail fixed deposit rates, this is no longer the case.

Because these are the latest interest rates from Syfe Cash+ below:

- 3 months – 1.85%

- 6 months – 1.75%

- 12 months – 1.65%

Because of that you’re probably better off just sticking with the plain vanilla fixed deposit.

Note also that Syfe Cash+ is not SDIC insured, but given that the underlying is fixed deposits risk should be on the low side (but not risk free).

6-month T-Bills yields drop to 1.85% – Will T-Bills yields continue to drop?

Meanwhile, 6-month T-Bill yields continue to drop, coming in at 1.85% at the latest auction:

You can see this charted below, T-Bills yields have been steadily declining since the peak in mid 2022:

And frankly, I don’t see anything that suggests that will change going forward.

Sure maybe we get a mild rebound in yields.

But I don’t think we’ll be recovering back to the 3.0% range unless something material changes in markets.

Because of that I don’t think T-Bills are that attractive anymore today.

Comparing interest rates for T-Bills vs Fixed Deposits vs Syfe Cash+ Guaranteed across all tenures (July 2025)

I’ve tabulated the interest rates for the 3 cash options below, as well as with money market funds.

You can see how with the recent drop in T-Bills and institutional fixed deposit yields – actually retail fixed deposits are a pretty attractive option once again.

| 3 months | 6 months | 12 months | Risk Free | |

| T-Bills yields | NA | 1.85% | 1.88% | Yes |

| Fixed Deposit (direct to bank) | 1.95% | 2.15% | 2.45% | Yes (if below $100,000 SDIC limit) |

| Syfe Cash+ Guaranteed (Institutional Fixed Deposit Rates) | 1.85% | 1.75% | 1.65% | No |

| Money Market Funds | ~2.6% | No | ||

In fact viewed this way the 2.45% offered by DBS Bank looks like an outlier and pretty much a no brainer.

The only downside is that the maximum you can put in is $19,999:

Where would I put my cash today? For yield and liquidity?

If you haven’t already parked S$19,999 with DBS 12-mth FD at 2.45%, that’s the low hanging fruit.

After that, I would say park some cash in a high yield savings account like UOB One or DBS Multiplier if its not too much work to fulfil the requirements.

Yes the 3.3% yield is no longer amazing, but still better than alternatives.

If too much work to fulfil the requirements, or you have excess cash you need liquidity with, then money market funds like MariInvest SavePlus / LionGlobal MMF (~2.7 %) are great.

And if you have cash that you can lock up for the medium term (≥6 mths), I would say split between fixed deposits based on the list below.

And if you can take on even more risk – then perhaps a medium term bond fund like PIMCO Income Fund (but note this is not risk free).

I elaborate on each of the options below.

Never miss a market beat—ride with Financial Horse wherever you go!

Get timely insights, sharp analyses, and real-time alerts by subscribing or following us on your favorite platform:

Subscribe to our mailing list for exclusive content straight to your inbox, plus early access to special reports and FH Premium previews

Best Fixed Deposit Rates yield 2.45% – if you deposit directly with the bank (as of July 2025)

The full list of Fixed Deposit rates is set out below (bold being the most attractive for each tenure).

After the table I’ll share my views on:

- Will fixed deposit rates continue to decline?

- What are the alternatives to T-Bills and Fixed Deposit?

- Where would I put my cash today?

| Bank | Interest rate per annum | Tenure | Minimum amount |

| DBS/POSB | 2.45% | 12 months | S$1,000 (max S$19,999) |

| 2.35% | 9 months | S$1,000 (max S$19,999) | |

| 2.15% | 6 months | S$1,000 (max S$19,999) | |

| SBI | 2.00% | 6 months | S$5,000 |

| 1.90% | 12 months | S$5,000 | |

| Bank of China | 1.95% (mobile new placement) | 3 months | S$500 |

| 1.80% (mobile new placement) | 6 months | S$500 | |

| 1.75% (mobile new placement) | 9 months | S$500 | |

| CIMB | 1.85% | 3 months | S$10,000 |

| 1.75% | 6 months | S$10,000 | |

| 1.55% | 9/12 months | S$10,000 | |

| Citibank | 1.80% | 3 months | S$10,000 |

| 1.80% | 6 months | S$10,000 | |

| ICBC | 1.80% (mobile placement) | 3 months | S$500 |

| 1.75% (mobile placement) | 6/9/12 months | S$500 | |

| RHB | 1.80% (mobile placement) | 3/6 months | S$20,000 |

| 1.60% (mobile placement) | 12 months | S$20,000 | |

| Hong Leong Finance | 1.78% (mobile placement) | 9 months | S$5,000 |

| 1.73% (mobile placement) | 11/13 months | S$5,000 | |

| UOB | 1.75% | 6 months | S$10,000 (fresh funds) |

| 1.60% | 10 months | S$10,000 (fresh funds) | |

| Maybank | 1.75% (mobile placement) | 12 months | S$20,000 |

| 1.70% (mobile placement) | 9 months | S$20,000 | |

| 1.60% (mobile placement) | 6 months | S$20,000 | |

| OCBC | 1.50% (mobile placement) | 9 months | S$30,000 |

| 1.45% (mobile placement) | 12 months | S$30,000 | |

| Standard Chartered | 1.45% | 6 months | S$25,000 (fresh funds) |

| 1.50% | 15 months | No minimum | |

| 1.10% | 12 months | No minimum | |

| 1.05% | 9 months | No minimum | |

| HSBC | 1.05% | 3/6 months | S$30,000 |

Will fixed deposit rates continue to decline?

Short answer – probably yes.

The slightly longer answer, is that the market continues to price in quite aggressive rate cuts from the Feds.

Jerome Powell’s term is up in 2026, and you can bet that Trump is going to replace him with someone who will deliver on what Trump wants – being rate cuts.

In that climate, the SGD stands out for its stability, and relatively stable FX.

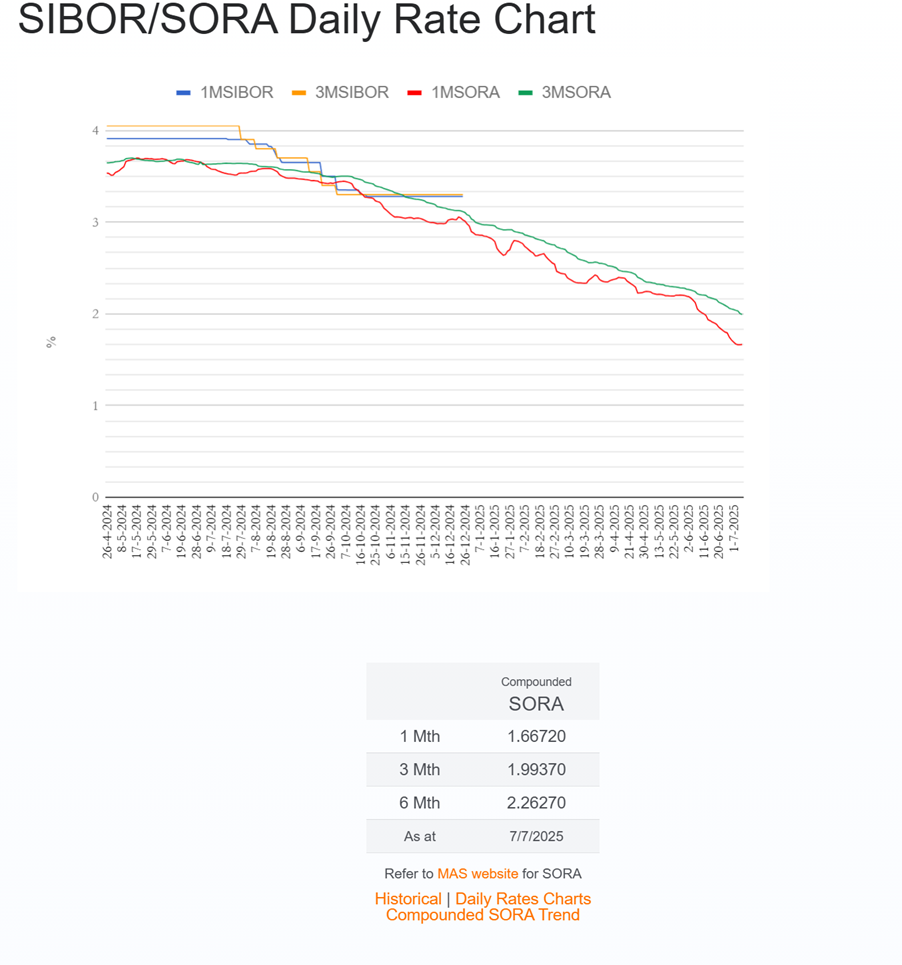

Combined, that seems to have created downward pressure for yields in Singapore – which you can see reflected in the 1 and 3 month SORA rates.

For now at least, unless something material changes in markets, I don’t see anything that would spark a reversal of this trend (but of course this being markets, it can change any time).

What are the alternatives to T-Bills and Fixed Deposit? To park cash?

Let me outline the key alternatives to T-Bills and Fixed Deposits below.

High Yield Savings Accounts – UOB One, DBS Multiplier, OCBC 360 etc

Interest rates for high yield savings accounts have been revised down of late.

UOB One has dropped interest rates – but still a decent option

UOB one has dropped their interest rates.

There’s a nice table from Milelion summarising the changes – effective interest rate on $150,000 has now fallen from 4% to 3.3%:

That said, if you can fulfil the criteria without too much trouble.

I still think it’s worth it, as the 3.3% is still higher than other options like fixed deposits, money market funds, or T-Bills.

That said, if you find it too much of a hassle, or don’t want to put the full $150,000 in, then just use the other options on this list.

Money market fund instruments (like MariInvest)

Alternatively there is MariInvest which is a money market fund that pays about 2.6% over the past 30 days for me.

But given T-Bills are yielding 1.85%, I think money market funds are a pretty decent option right now, especially since you get the T+1 liquidity.

There is some investor discretion required here as unlike T-Bills, money market funds are not risk free.

Singapore Savings Bonds are an acceptable alternative too

Interest rates on the latest Singapore Savings Bonds below.

You’re looking at 1.82% for the first 3 years, stepping up to 2.29% over 10 years.

I don’t think this is amazing, but you can see that it’s still comparable to T-Bills (T-Bills no longer look like that great a buy frankly).

PIMCO GIS Income Fund via Maribank

For more duration, you can consider buying a bond fund.

One example is the PIMCO GIS Income Fund, that you can access via Maribank.

I wrote a detailed review so do check it out if you are keen.

Bottom line is that these bond funds are quite a complex instrument, and not for everyone.

Because if interest rates go up, you can suffer mark to market capital losses.

And there is no way to hold to maturity as the bond fund will automatically reinvest proceeds.

So effectively there is some timing element involved here, in that you want to buy the fund when yields are high, and sell when yields are low, and if you do it the other way around you could see mark to market capital losses.

Best used only if you have a mid to longer term investment horizon.

Where would I put my cash today?

If you haven’t already parked S$19,999 with DBS 12-mth FD at 2.45%, that’s the low hanging fruit.

After that, I would say park some cash in a high yield savings account like UOB One or DBS Multiplier if its not too much work to fulfil the requirements.

Yes the 3.3% yield is no longer amazing, but still better than alternatives.

If too much work to fulfil the requirements, or you have excess cash you need liquidity with, then money market funds like MariInvest SavePlus / LionGlobal MMF (~2.7 %) are great.

And if you have cash that you can lock up for the medium term (≥6 mths), I would say split between fixed deposits based on the list above.

And if you can take on even more risk – then perhaps a medium term bond fund like PIMCO Income Fund (but note this is not risk free).

This post is written on 20 June 2025 and will not be updated going forward.

For my freshest market calls, the live Stock & REIT Watchlist, and full weekly-updated personal portfolio, unlock FH Premium today.

DBS has 6, 9 and 12 months tenors. Does the $19999 max apply to all of them in total (6mo + 9mo + 12mo = $19999) or each of them separately (6mo $19999 + 9mo $19999 + 12mo $19999)? Thanks for clarifying!

No – it applies across the board. So if you maxxed out the 12 months, you’re maxxed out with DBS.

DBS 2.45% for 12 mths, 18 mths or 24 mths, which better in the current environment?

Are the rates for 12, 18 and 24 the same? I guess it depends on how the rest of your cash is allocated duration wise. You’ll want to spread them out over a range of maturities.