There’s this interesting exercise that fund managers like to run. And it goes like this. Imagine that you’re a fund manager and you just raised x amount for a new fund. Because the fund is brand new, you own completely no investments at all. This means that over the next 6 to 12 months, you’ll need to deploy most to all of your cash. What do you invest in?

It’s a really interesting exercise because it forces you to set aside all your preconceived notions about investments, and look at them based on current prices. Sure. Mapletree Commercial Trust may be the best REIT ever, but are you really going to buy it at a 40% premium to book and a 4.15% yield?

The ground rules for this portfolio are:

The world is your oyster – Every single asset class, in every geography, is accessible. The world is your oyster.

Risk Profile is medium – This is a medium risk medium return kind of portfolio. It’s not intended to maximise returns, neither is it designed to minimise risk. It’s really just a balanced portfolio.

Perspective of a retail investor with S$10,000 to invest – When you’re a fund manager with $100 million, you can easily allocate into 100 different stocks to get broad exposure to the global economy. When you’re a retail investor investing $5000 each time, that becomes a lot harder.

I know a lot of readers out there are investing small sums each time, so this article is written from such a perspective – Here, we assume that the total amount available for investment is S$10,000.

Basics: More Defensive Asset Allocation

As I’ve mentioned in the FH Guide to investing, the most important thing is to always start with asset allocation, before going into picking the individual investments.

So what kind of an asset allocation is suitable in this macro climate?

My personal thinking is that we are at the later stages of the short term and the longer term debt cycles, for most developed economies around the world. Interest rates are at record lows, at a time when global growth is slowing. Throw in the US-China trade war on top of that, and you’ve got a good recipe for a global slowdown. I’ve shared my thoughts about this in greater detail previously, so do check that out. But long story short, is that we want an asset allocation with a more defensive stance.

Ray Dalio’s all weather portfolio is a good starting point for this exercise, since it’s designed to perform well in all kinds of economic conditions.

I’ve made some slight tweaks to it to adapt to what I think the global economy will look like in the coming years:

No commodities – One big change I made is to completely remove the commodities component. I think in the next year or two the global slowdown will hit the commodities market particularly hard, and the current bust is only just getting started. So we don’t want to be too heavily allocated to commodities.

20% Gold –What asset class do you want to own when global growth is slowing, central banks are running out of ammunition in monetary policy, and populist governments are popping up all around the world?

If you guessed gold, then you’re absolutely right. Gold as an asset class is just designed for shit hits the fan moment, and I can’t think of a better time to own gold than right now.

Sure, gold has had a big run-up, but it’s all about the risk reward here. If global central banks are able to solve the current slowdown, gold maybe goes back down to $1200 per ounce (from $1500 per ounce now). If global central banks can’t solve the slowdown (and I really don’t see how they can when they’re already at negative interest rates), gold could easily fly past $2000 per ounce.

So yeah, I really like the risk-reward of gold right now.

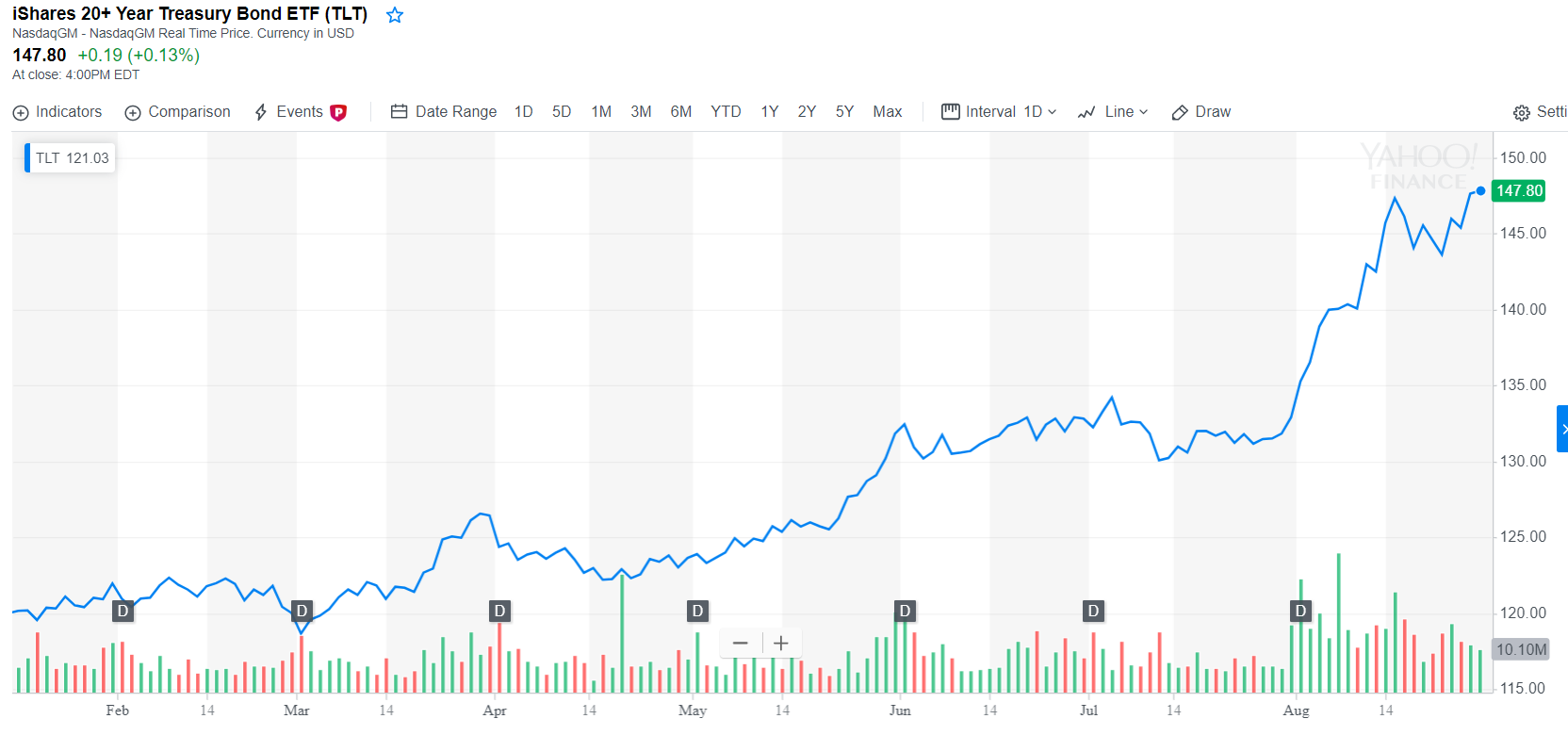

30% Long Term US Bonds – US Treasuries have had a monster rally. Just take a look at the 1 year chart below.

But I think the problem here is what do you invest in as an alternative?

In times like this, whether we like it or not, the USD is king. Sure, maybe in 20 years time the RMB will be the world’s reserve currency, but right now, if there’s a global flight to safety, every single institutional investor is going to pour into USD assets, and they’re going into US Treasuries.

And I know what you’re thinking. “But wait Financial Horse, the US 10 year Treasury yields 1.49% now. Why would I buy Treasuries at this yield? How much more can it fall?”

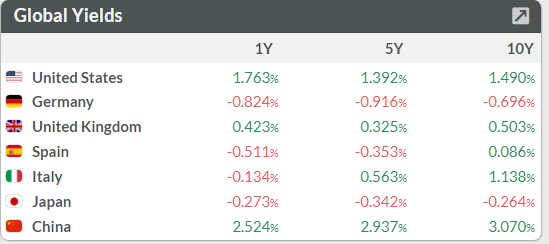

Well, a picture speaks a thousand words, and I’m just going to show you the table below.

The 1.49% US 10 Year is incredibly low on a historical basis, but we need to invest in the world as it is, not in the world as it used to be. And global yields across all developed nations are a complete joke right now. I mean Germany 10 Year at – 0.7% and Spain at 0.09%? Seriously? How is it that the Italian government is borrowing money cheaper than the US government?! With charts like this, I kinda get the rage from Trump.

So in the next recession, I think US 10 year yields may drop to the zero range pretty quickly, which means that US Treasuries may still be a good investment at these prices.

20% Intermediate Term Singapore Bonds – As Singaporeans, it’s never wise to have too much of your assets denominated in a foreign currency, even if that currency is the USD. It’s all about diversification you see.

Theoretically speaking, USD should go higher from here, as money flows out of Emerging Markets into US. But traditional economic theory doesn’t account for a guy called Trump. If he manages to fire Jerome Powell, or finds a way to depreciate the USD, then USD assets could drop like a rock.

So because of that, we’ll want 20% allocation to Singapore Government bonds. The yields are not great definitely, but they’re merely reflecting the current yield in Singapore government bonds. Beggars can’t be choosers really.

30% Stocks – I thought long and hard about this one. What is the right asset allocation to equities in this climate?

And ultimately, I took a look at my own portfolio (available here), the all-weather portfolio, and decided that 30% was the best, at least for this portfolio.

Having zero allocation to stocks is not a solution, because nobody knows the timing of the next recession. Stocks can easily go another 20% higher from here, and if you sell all your stocks now you’re going to miss out on that rally.

Going too heavily into stocks is not ideal too, because of where we are in the debt cycle. You don’t want to have a big allocation into stocks and get wiped out in the next crash. So personally, I settled on 30% for this portfolio.

How to execute this asset allocation?

With asset allocation out of the way, we now focus on execution.

20% Gold – $2000 in GLD ETF

I get a lot of questions on how best to invest in gold. Long story short, if you’re investing small amounts – use an ETF, medium amounts – use a gold savings account, large amounts for long periods – physical gold.

For $2000, we definitely want an ETF, so we go with GLD, for the ease of execution.

30% Long Term US Bonds – $3000 in TLT ETF

For US Treasuries, I went with the long-term treasury ETF, the TLT. This mainly invests in 20+ year Treasuries, which I felt was the best way to play the fall in US yields without touching complex products like Eurodollar Futures.

20% Singapore Bonds – $2000 in Singapore Savings Bonds

SSBs are pretty self explanatory, and have been discussed to death on this site, so we won’t dwell on them.

30% Stocks

$1000 in S&P500, $1000 in STI ETF, $1000 in Hang Seng Index

The problem with only having $3000 to invest in stocks is how to get meaningful diversified exposure without incurring excessive transaction fees. And the easiest way is to use an ETF.

I was actually deciding whether to use an all-world index like the IWDA. My main problem with such an index, is the undersized allocation to China, and the outsized allocation to the rest of the world (including Europe). The IWDA has a 60% allocation to US, a less than 4% allocation to China, and a 5% allocation to the UK. Does that sound like a good bet on the future of the global economy to you?

The way I see it, the 21st century will be dominated by 2 superpowers, the US, and China. And everyone else just rotates around the orbits of these 2 giants. So I would want my stock allocation to reflect that vision.

I’ve split the $3000 into 3 parts, with $1000 going into the S&P500, $1000 into the Hang Seng Index, and $1000 into the STI ETF because ultimately as Singaporeans, we want the Singapore exposure.

Of course, there’s no denying that stocks may have a rough year or two ahead. But that’s fine, because the worse that stocks do, the better that the bonds and gold in the portfolio will do.

Closing Thoughts

I get a lot of questions from readers on how best to invest money. Of course, the answer is never so straightforward, because how to invest your money depends on everything from your age, your income, your family dynamics, your risk profile and your experience in financial markets etc.

I’ve actually built the FH Complete Guide to investing for Singaporeans from scratch to set out a complete framework for Singaporeans to invest their money.

And in this article, I’ve tried to apply some of the principles in that course to evaluate the stage of the market cycle, formulate an asset allocation, and then pick stocks/ETFs to execute on that asset allocation.

Of course, it’s not intended to be tailored to your specific financial situation, so please don’t blindly copy the portfolio set out here. If you want to better understand how to tailor it for your profile, do consider checking out the FH Course.

That said, I genuinely think that the next year or two could see some volatility in financial markets. I think the pain has barely even started, and we’re going to be in for some very interesting times. I don’t want to come across as hyperbole, but I do think we could be in for a paradigm shift in the global sovereign debt markets.

And in such a climate, I do think more caution is warranted, which is why I went with a more defensive portfolio like the above.

But we’ll see.

What do you guys think! How would you invest $10,000 right in Singapore now? Share your comments below!

Looking for a comprehensive guide to investing? Check out the FH Complete Guide to Investing for Singapore investors.

Support the site as a Patron and get market and stock watch updates. Big shoutout to all Patrons for their support! Like our Facebook Page and join the Facebook Group to continue the discussion!

Hi! Why the Hang Seng Index rather than the MSCI China ETF? Thanks! This is quite a nice suggestion for $10k.

MSCI China ETF is fine as well, but personally I prefer the Hang Seng because of lower expense ratios, and the Hang Seng being more efficient than China A shares at the moment. I think that if you want to invest in A shares, it is best to do it via active investing because of the inefficiencies in the market. But yeah, it’s more of a personal choice, MSCI China is perfectly fine as well.

It should be fine buying IWDA, since the allocation to China should shift if and when China stocks take up a bigger percentage of the world stock value? Other than that all good!

Sure, that works as well! My preference though is to get the exposure to China now, rather than wait for IWDA to adjust it from the 4% to 20%. 🙂

For the Singapore Govt bond portion of the portfolio, Why not invest in the ABF bond etf?

The trade off here is that you are exposed to risk of capital loss, but the upshot is if you envision a world of ultra low yields, you stand to gain from capital appreciation. Singapore Govt bonds yields look quite attractive compared to other AAA countries at this juncture…

That’s a really good point. My concern with ABF bond ETF is the low liquidity, but I suppose that are numerous upsides as you rightly pointed out. So yeah.. I think it’s a really good suggestion.

Thanks for raising! 🙂

HI FH, on the 20yr UST, Blackrock launched DTLA on the London stock exchange (since May 2018) at 0.07% expense ratio (versus 0.15% for TLT). Cheaper, but newer and smaller and probably less liquidity. What do you reckon?

Yep, I think you’ve summed up the points perfectly. 🙂

Hi! Thanks for the article. I was just wondering if it makes sense to put a small % (perhaps 5%?) into cryptocurrency?

Sure, it really depends on your risk appetite and objectives. If you feel srongly on crypto, by all means go into it, but be careful on sizing, so as you mentioned, something like 5% wouldn’t expose you to such big losses if the asset class collapses. 🙂