I’ve been getting quite a few requests to cover the UK Gilts incident (Gilts are the UK Government Bonds).

Just like Credit Suisse last week, this is one of those that as interest rates start to go up, you start to see who has been “swimming naked”.

Unlike Credit Suisse though, the UK Gilts market does have the potential to trigger systemic risk globally.

There’s a lot more going on than meets the eye, and it is not over by any means.

So it’s worth taking some time to understand what is going on, and the broader implications on markets.

This article is a premium Patreon article, written on 11 October 2022. If you find this article helpful for you, please do consider signing up for the Patreon subscription. Most of the regular macro updates (like this) have moved there.

Let’s start at the top

To really understand what is happening today, we need to start in the 1970s.

In the 1970s, President Nixon took the US off the gold standard, triggering a wave of inflation. This only ended in the 1980s after interest rates went to 18% (among other things).

After the 1980s, inflation went away for the next 40 years.

With inflation out of the picture– monetary policy (via interest rates controlled by central banks) reigned supreme.

From the 1980s to 2008, every single economic crisis was fought with interest rates.

When things got bad enough, interest rates were cut, and the problem went away.

2008 – Enter QE

This ended in 2008.

In 2008, the Federal Reserve cut interest rates to zero.

And they couldn’t go any further.

So they started on QE (Quantitative Easing) – printing money to buy government bonds.

But inflation was not a problem yet, so all was fine. They did round after round of QE, that inflated asset prices globally.

2020 – The return of inflation

Everything changed in 2020.

In March 2020, COVID happened.

After COVID, governments started giving money directly to consumers.

And that, has triggered the return of inflation the first time in 40 years.

Backdrop the past 6 months

And that’s where our story begins.

Once inflation comes into play, monetary policy as a tool becomes ineffective. Inflation is also deeply unpopular, which is bad news for any democracy.

Over the past 6 months+, the Feds have gotten very hawkish to combat inflation.

They have hiked US interest rates aggressively.

Generally speaking, the higher your interest rates, the stronger your currency.

This has led to a strong USD against every currency.

This is good if you’re selling to the US (because your goods become cheaper in USD).

But this is bad when you buy goods priced in USD (because you need more local currency to buy the same goods).

It just turns out a very critical global resource known as oil (and commodities), is priced in USD.

Enter the UK

Now the Bank of England (the UK central bank) was actually earlier to hike interest rates than the Fed.

Unfortunately, they had to slow their pace of rate hikes recently (the Feds hiked by 0.75%, but the Bank of England only hiked 0.5%).

Now the people running the Bank of England are no fools, so why did they do this?

The simple reason is that as much as they want to hike interest rates to strengthen the pound.

Higher interest rates will crush the domestic UK economy due to higher borrowing costs.

Bank of England’s Dilemma

The dilemma for the BoE can be summed up as follows:

- The BoE needs to hike interest rates to keep up with the US Feds, to avoid a weaker pound (which would raise inflation)

- However, if they raise interest rates too much too fast, they will cause a UK recession

Unfortunately, the US inflation situation is very bad, so the Feds are hiking very fast.

Almost no other central bank in the world can keep up, without breaking their domestic economy

So you know how Western economists always mock “Emerging Markets” for not raising interest rates fast enough when they have a balance of payments crisis due to a weakening currency?

Well, when the tables are turned, the Western economists are forced into making the same mistakes.

Who’s laughing now?

The Catalyst – Liz Truss & Kwasi Kwarteng

So that’s the backdrop.

Now, enter the catalyst.

The catalyst, as it turns out, is the newly installed Conservative Party leadership (Liz Truss as Prime Minister and Chancellor Kwasi Kwarteng).

Their plan to save the UK economy, runs like this:

- Tax cuts for the corporations and the rich

- Increase spending by subsidizing household energy costs

Now any JC econs student can tell you that (1) means less money for the government from taxes, and (2) means more money to be spent by the government.

Less money coming in, more money going out.

So… where is that money going to come from?

The Feedback Loop

Well, it’s a bit of a chicken and egg.

But what happened next can be summed up like this:

- Investors realized that a lot of new debt is going to be issued to fund this budget

- More debt means interest rates go up

- As interest rates go up, the value of bonds go down.

- So investors holding onto Gilts suffer big losses, and some of them start to sell – further driving prices down

- At the same time, the pound starts to weaken as investors move their money out of the UK

- This means higher inflation due to a weaker pound, which means the BoE needs to raise rates even more to combat inflation

At some point, the cause and effect becomes blurred, and it builds into a feedback loop.

What UK Pension Funds have been doing with their money…

Now, enter the pension funds.

Think of it like the UK version of CPF.

Every month, workers pay a portion of their salary to the pension funds. And when they retire, the pension funds pay them an amount every month.

So pension funds are the ultimate long term investors.

BUT – and this is important, the future liabilities of the pension funds are fixed, based on how much they need to pay out when the pensioners hit retirement.

So you can calculate their total future liabilities.

Now, how do you value a future liability, based on present value?

You value a future liability, just like you value stocks – by applying a discount rate to it.

And the discount rate, is the market interest rate.

So to put it very simplistically:

- When interest rates go up, the present value of the Pension Fund’s future liabilities goes down

- When interest rates go down, the present value of the Pension Fund’s liabilities goes up

Why is this a problem?

Now why is this a problem you ask?

Interest rates are going up, so the value of the Pension Fund’s liabilities are going down, no?

Now I suggest you think of it from the perspective of a well-paid pension fund manager.

Every quarter, you need to go to the board of directors and explain to them how much assets you have today, versus your liabilities.

If your assets are less than your liabilities (ie. You are underfunded), you get a bunch of tough questions on what you’re going to do to solve it.

If your assets are less than your liabilities for more than a few quarters, then well, you’re fired.

Now remember, interest rates have been going down for 40 years, especially so the past 15 years.

So this has been a very real problem for the past 40 years, and especially so the past 15 years.

And these very well paid fund managers have been searching for a solution for quite a while now.

And especially so for the past 15 years, since 2008.

Enter… Liability-Driven Investment

Of course, Wall Street have a solution.

Liability-Driven Investment (LDI).

LDIs work like this.

In technical jargon – it is a hedging strategy to hedge your liabilities to the extent required to offset whatever is causing the increase in your liabilities (the fall in interest rates).

Or practically speaking, it means the UK Pension Funds took an absolute ton of leverage, and bet on interest rates going down.

Remember, pension funds are in trouble because interest rates going down increase the present value of their liabilities. And this was a big problem the past 15 years.

So the solution of course, is to make a giant bet on interest rates going down.

Basically, even if interest rates stay at 0% for the next 30 years, you are fine because you make enough money from your bet that interest rates stay at 0%, that you use that money to pay off all the pensioners.

Is this a risk-free bet?

So now you can go to your quarterly board meeting and tell the board that hey your assets are higher than your liabilities.

If you have a savvy board, they will probably ask you what is the risk involved in this strategy.

In which case you just pull up your backtested returns from the past 40 years.

And you explain to them that running this strategy any time the past 40 years is basically foolproof.

After all, interest rates have only been going down the past 40 years.

Why would that change, you tell your board?

So the Board is pleased, and you get a nice bonus for the year

All is well.

BTW – we share commentary on Singapore Investments every week, so do join our Telegram Channel (or Telegram Group), Facebook and Instagram to stay up to date!

We also share great nuggets of wisdom on Twitter.

Don’t forget to sign up for our free weekly newsletter too!

[mc4wp_form id=”173″]

The stage is set…

As with all great investment strategies.

They work… until they don’t.

As discussed above, the factors driving this move have been building for a while now.

It just so happened to be Liz Truss that broke the markets.

The sequence of events that started with Liz Truss’s new budget, led to a feedback loop that led to a big rise in UK interest rates.

Margin Calls

Now remember you are a pension fund.

You just made a massive bet that interest rates will only go down.

Now, interest rates are soaring to multi-decade highs.

And now the Bank who executes the trade for you, is calling to ask for more “margin” because of your massive losses.

And so you sell some Gilts to raise cash, which only drives prices lower, increasing your margin call.

Eventually, you start to realise that all the other pension funds are doing the exact same thing (selling Gilts).

And suddenly you realise all the buyers have vanished, because nobody has the balance sheet to buy Gilts at the kind of size the market is selling, especially not with that kind of volatility.

And now you really panic, because if you can’t sell your Gilts, you cannot raise the money to meet the margin call.

And if you can’t raise the money, the bank is going to liquidate your Gilts.

Into a market without buyers, which would effectively break the Gilt market, and bankrupt your pension fund.

Bank of England is forced to step in

And that’s when you realise you need to call your buddies at the Bank of England.

As it turns out, that morning, every Pension Fund is calling the Bank of England.

Every Pension Fund is telling them that if they don’t step in to bail out the Gilts market, all the pension funds are going to be margin called that Afternoon.

And of course, situations like this are what the Bank of England exists for.

This is systemic risk, that would have melted down the UK financial system as we know it.

So the Bank of England steps in, and announces an emergency plan to buy Gilts.

The very announcement alone is sufficient to stave off the short-term panic, and force short covering by speculators.

Is the crisis averted?

So yes, the short term crisis is averted.

The short term, liquidity crisis is averted.

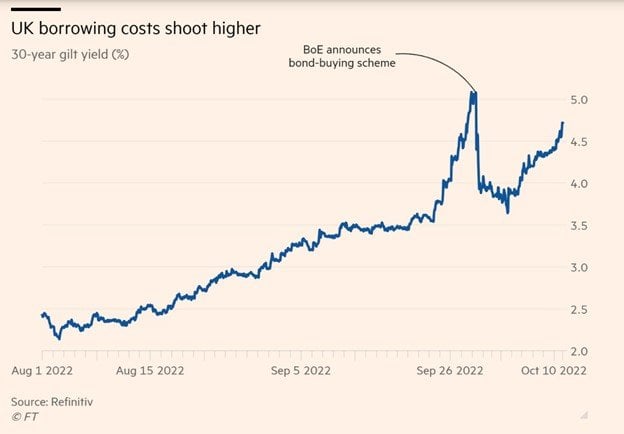

But look at the chart above.

Interest rates are creeping back up to where they were before the Bank of England was forced to step in.

Just like we saw with the Bank of Japan, the market is starting to test the Bank of England’s resolve to buy Gilts, at the amounts required to maintain stability.

And just like the BOJ, the BOE will have 2 choices – (a) buy unlimited amounts of Gilts to stabilize the market, or (b) allow interest rates to go up.

And that’s where we are today.

What about the pension funds?

Now if you’ve been following the above, you’ll realise this crisis for the pension funds is not over by any means.

The Pension Funds, are still betting on interest rates going down (via LDIs).

If interest rates continue going up, they are still going to get margin called.

So all the Bank of England has done for now, is buy time.

It buys time, for the Pension Funds to go to their banks and unwind all their positions in an orderly manner.

But if they unwind all these positions at a huge loss, how do they meet their future obligations to the pensioners?

Don’t forget that this is just the UK pension funds. The US pension funds have been doing the same thing, just with slightly different mechanics.

What is the key takeaway here?

In 2008 terms, the Gilt market breaking is Bear Sterns.

It is a small event, that will be contained, and will not trigger contagion by itself.

But the dynamics that caused Gilts to break, are still very much in play.

And they will continue to fester, until something bigger breaks.

Or until the Feds give up on hiking interest rates.

This leverage unwind may be more dangerous than 2008

In 2008, the leverage was primarily limited to bank leverage, with a bit of spillover into the insurers.

If you followed the above, you will realise that ironically it was the solution to 2008 – QE and unlimited money printing, that has set the stage for this crisis.

Low interest rates since 2008 have forced pension funds and asset managers out the risk curve.

More money went into long duration, and illiquid assets like real estate and private equity.

All while QE has lulled everyone into a false sense of security.

Risk managers backtested their risk models into 40 years of declining interest rates.

That’s all gone now.

As interest rates blast higher, all existing risk management and stress testing looks out of date.

This triggers forced asset sales the same time as the Feds are tightening, creating pro-cyclical flows.

All while money stuck in illiquid real estate and private equity needs to be redeemed to meet immediate cash requirements.

If you find this article helpful for you, please do consider signing up for the Patreon subscription. Most of the regular macro updates and changes to my portfolio positioning have moved there.

At S$15 a month you get the premium weekly market updates like this one.

At $25 a month you get my full stock and REIT watchlist, and at $40 a month you get updates on changes to my portfolio positioning.

Don’t be penny wise pound foolish!

– Free US Stock, Options and ETF trading (Free USD130 (S$185) in Tesla shares)

I did a review on WeBull and I really like this brokerage – Free US Stock, Options and ETF trading, in a very easy to use platform.

I use it for my own trades in fact.

To get the USD130 (S$185) in Tesla shares, you just need to:

- and fund S$200

- Make 1 US Stock or ETF trade (you get USD100 in Tesla Shares)

- Make 1 Options trade (you get USD30 in Tesla Shares)

Trust Bank Account (Partnership between Standard Chartered and NTUC)

Sign up for a Trust Bank Account and get:

- $35 NTUC voucher

- Whole bunch of freebies – A free packet of rice (1kg), a free Kopitiam Kaya Toast set, a $1.99 Double Mushroom Swiss at Burger King, and 50% off KFC Zinger Set just to name a few.

- 1.0% base interest on your first $50,000 (up to 1.4%)

Fully SDIC insured as well.

It’s worth it in my view, a lot of freebies for very little effort.

Full review here, or use Promo Code N0D61KGY when you sign up to get the vouchers!

Looking for a low cost broker to buy US, China or Singapore stocks?

Get 100 USD in Apple Shares with, a zero commission broker.

Get a free stock and commission free trading with.

Get a free stock and commission free trading with.

Special account opening bonus for Saxo Brokers too (drop email to [email protected] for full steps).

Orfor competitive FX and commissions.

Looking to buy Bitcoin, Ethereum, or Crypto?

Check out our guide to the best Crypto Exchange here.

Do like and follow our Facebook and Instagram, or join the Telegram Channel. Never miss another post from Financial Horse!

Looking for a comprehensive guide to investing that covers stocks, REITs, bonds, CPF and asset allocation? Check out the FH Complete Guide to Investing.

Or if you’re a more advanced investor, check out the REITs Investing Masterclass, which goes in-depth into REITs investing – everything from how much REITs to own, which economic conditions to buy REITs, how to pick REITs etc.

Want to learn everything there is to know about stocks? Check out our Stocks Masterclass – learn how to pick growth and dividend stocks, how to position size, when to buy stocks, how to use options to supercharge returns, and more!

All are THE best quality investment courses available to Singapore investors out there!

FYI – We just launched the FH Property Series. Everything you need to know to buy a property in Singapore, completely free of charge.