First off – my apologies.

I know that I’ve been doing a lot of posts on Singapore Savings Bonds and T-Bills recently.

I’ve just been getting a ton of questions – Investors can’t get enough of SSB/T-Bills it seems.

And given elevated macro risk, I think for a long only retail investor, that’s just the safest place to be for now.

But I know many long-time readers are here for macro views.

Much of it has moved over into the premium Patreon service, but I do want to keep general readers appraised of my thinking as well.

So today, let’s talk about an asset class most of you love – REITs.

Why I think REIT prices will struggle in 2023 (as a Singapore Investor)

The short version, is that I think REIT prices will struggle in 2023.

The slightly longer version, is that there are 3 key points to discuss:

- Interest rates may stay high for a while

- This has not been fully priced in

- Forced selling just starting to play out (liquidity mismatch)

Interest rates may stay high for a while

Okay, I know we are all sick of discussing interest rates.

But no discussion on REITs will be complete without touching on the interest rate outlook.

Higher interest rates mean higher refinancing costs for REITs, and higher cap rates for real estate.

Bad, and bad.

What is the latest Interest Rate outlook?

Serious investors should read the full transcript of Powell’s speech last week.

I did a detailed summary for Patrons, but to sum up.

The Feds will slow the pace of rate hikes going forward.

Powell doesn’t want to overtighten and be forced to cut rates too soon.

And given that higher interest rates take some time to work their way into the economy, he wants to slow down the pace of hikes as we approach terminal rate.

Hi words:

… my colleagues and I do not want to over tighten because, you know, I think that cutting rates is not something we want to do soon. So that’s why we’re slowing down and, you know, going to try to find our way to what that right level is.

BUT – bringing inflation down to 2% remains the official target.

So while the pace of hikes will slow, how high interest rates go, and how long they stay high – will depend on what is required to bring inflation down to 2%.

The key to breaking inflation, lies with the labour market

I’ve been saying this for a while.

If Powell is serious about bringing inflation down to 2%.

He needs to break the US labour market.

Powell’s words:

“Finally, we come to core services other than housing, and this spending category covers a wide range of services from health care and education to haircuts and hospitality.

This is the largest of our three categories, constituting more than half the core PCE index. Thus, this may be the most important category for understanding the future evolution of core inflation.

Because wages make up the largest cost in delivering these services, the labor market holds the key to understanding inflation in this category.

In the labor market, demand for workers far exceeds the supply of available workers, and nominal wages have been growing at a pace well above what would be consistent with 2% inflation over time. Thus, another condition we’re looking for is the restoration of balance between supply and demand in the labor force, in the labor market.”

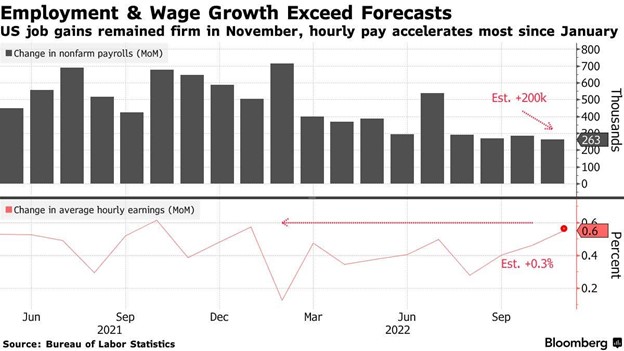

Last week’s Labour Report was a disaster

Which is exactly why last week’s labour report was so crucial.

Basically, the Feds won’t pivot until inflation comes down.

For inflation to come down, you need unemployment to go up (to weaken a tight labour market).

Before unemployment can begin to go up, you need to see wage growth start to come down.

And November’s wage grew 0.6% month on month – the highest growth in 2022.

That’s right.

After the fastest rate hiking cycle in 30 years.

Taking us from 0% to 3.75% in less than 9 month.

The labour market is still roaring along, and barely even showing signs of slowing down.

What does this mean for investors?

Many of you have asked how long will interest rates stay at ~5%.

Nobody knows the answer to that, not even Jerome Powell himself.

But what I do know – is that talks of interest rate cuts are still too early.

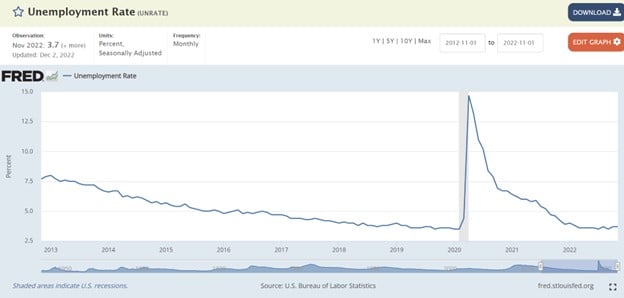

Before you can start thinking about interest rate cuts, you need to see the labour market softening up, and unemployment going up.

Typically speaking, you want to see 3 consecutive months of flattish / negative wage growth, before you can start to think about unemployment going up.

With November hitting the highest wage growth all year – we’re not there yet.

Think of it this way – We need to go from A (wage growth flat/negative) to B (unemployment going up) to C (inflation going down), before we can start cutting.

And for now, A has not even happened yet.

As Powell put it:

“Currently, the unemployment rate is at 3.7%, near 50-year lows, and job openings exceed available workers by about 4 million. That is about 1.7 job openings for every person looking for work. So far, we’ve seen only tentative signs of a moderation in labor demand.”

But gun to my head?

If Powell is really serious about bringing inflation down to 2%?

He may need to keep rates high perhaps 12 months or more, which takes us into end 2023 / early 2024.

Can the economy / markets hold up?

BUT – can the economy take another 12 months of higher interest rates?

Especially when you consider how much leverage is in the system today?

Frankly I don’t know the answer.

But I do think there is a good chance something will break before Powell succeeds in his quest to bring inflation down to 2%.

My base case – is that at some point in the next 12 – 24 months, Powell will be forced to give up on the inflation fight, and be forced to accept a higher level of inflation going forward.

This has not been priced in (for Singapore REITs)

But we’re getting ahead of ourselves.

Markets are forward looking, but they seldom look forward more than 12 months.

If you’re an active investor doing market timing, you should only be thinking about the next 3 – 6 months (possibly 12).

Based on the discussion above – interest rate cuts are not coming yet.

And if interest rate cuts are not coming yet – many REITs are looking very pricey.

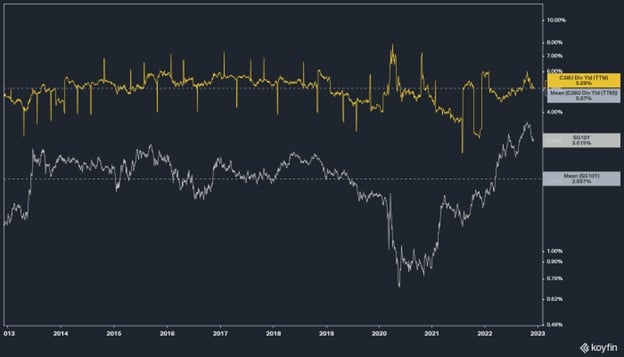

Let’s use CICT as an example – CapitaLand Integrated Commercial trust (Singapore REIT)

Now of course this is ultimately a REIT by REIT level analysis.

Some Singapore REITs are cheap, some are not.

But for discussion’s sake – let’s just use a crowd favourite – CapitaLand Integrated Commercial Trust.

I plotted the dividend yield (yellow) against the 10 year SGS yield (white) below.

You can see how the 10 year SGS yield is well above 1 standard deviation.

But CICT’s dividend yield is still well below 1 standard deviation.

CICT’s long term yield spread against the 10 year SGS is about 3%.

Let’s say conservatively we assume a peak 3.5% on the 10 year SGS this cycle.

You’re looking at 6.5% yield on CICT at fair value.

That’s about a 20 – 30% drop from current prices.

That’s even before higher financing costs (for Singapore REITs)

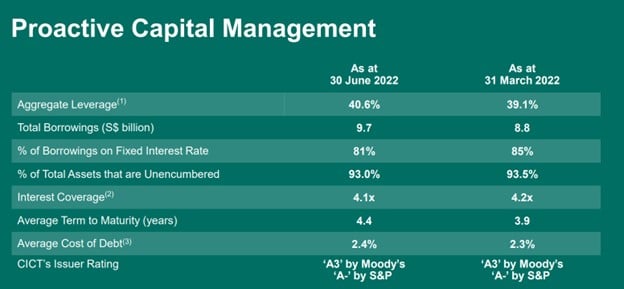

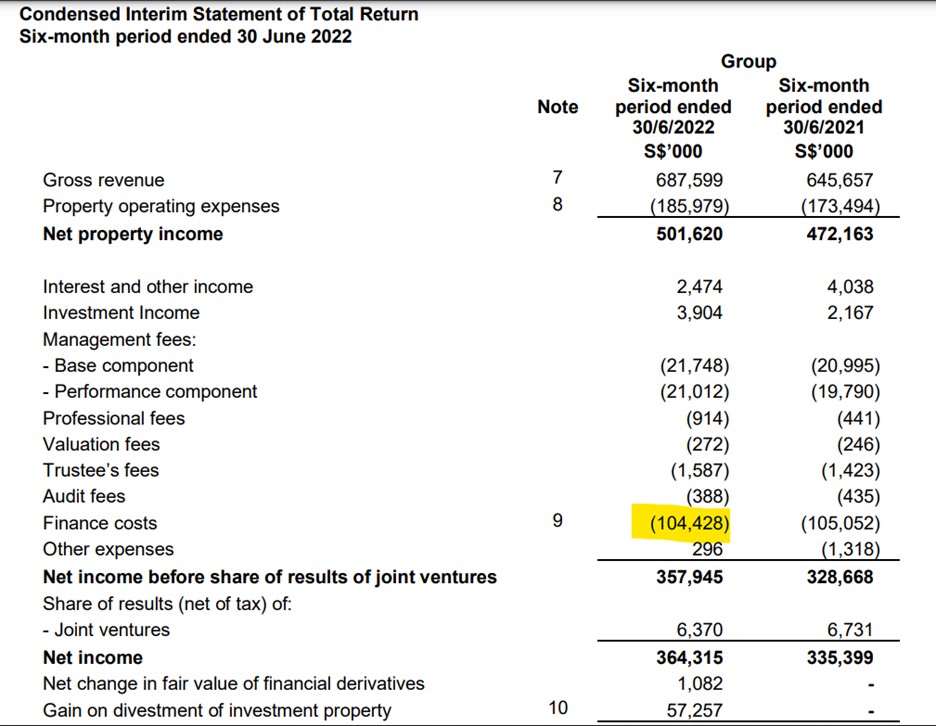

CICT’s weighted cost of debt is 2.3%.

If interest rates stay up, and we assume they refinance at 3.5% (which is still very low).

You’re looking at a 45% increase in financing costs.

The $104 million interest expense will balloon to $151 million.

Working out to an 11% drop in DPU.

Which means a 5% dividend yield, is now 4.45% (assuming no change in rent etc).

For the record – I get that CICT’s debt is well spaced out.

But the longer the interest rates stay up, the more this will be a problem.

Which is exactly my point.

Most REIT investors are expecting the Feds to cut us back to zero interest rates in 2023.

But think about our discussion above.

What if interest rates stay up longer than people expect?

That’s even before higher cap rates (for Singapore REITs)

And I haven’t even started talking about higher cap rates.

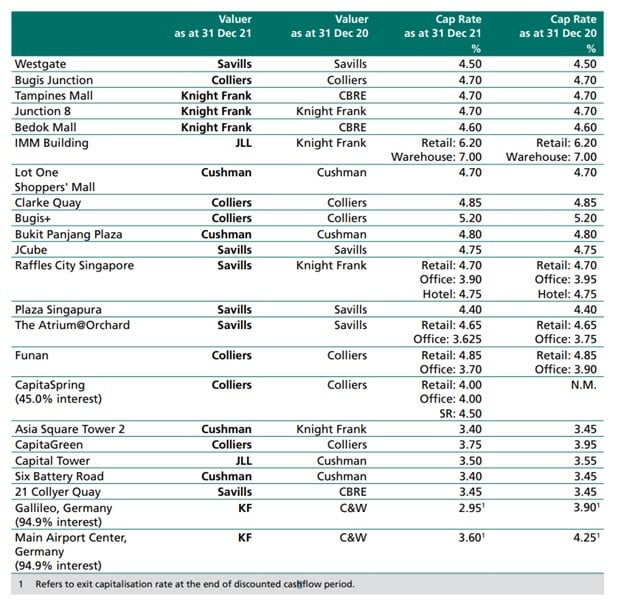

I extracted the cap rates for CICT below.

On average, you’re looking at 3 – 5% cap rates.

Cap rates basically tell you how expensive a property is.

If you get 30,000 a year in rental income, and the property is worth $1 million, that’s a 3% cap rate.

The lower the cap rate, the more expensive the property.

A cap rate of 3 – 5% makes sense when interest rates average 1%.

But when interest rates soar to 4 – 5% in 2023, you tell me if it these cap rates still make sense.

Who will buy commercial real estate at a 4% cap rate, when they can get the same yield from a T-Bill, risk free?

BTW – we share commentary on Singapore Investments every week, so do join our Telegram Channel (or Telegram Group), Facebook and Instagram to stay up to date!

I also share great tips on Twitter.

Don’t forget to sign up for our free weekly newsletter too!

[mc4wp_form id=”173″]

Forced selling just starting to play out (liquidity mismatch)

For the record, I am not singling out CICT here.

Nor am I singling out Singapore real estate.

The points I raise above, apply to global real estate.

And in my view, the pain for commercial real estate globally – it’s only just beginning.

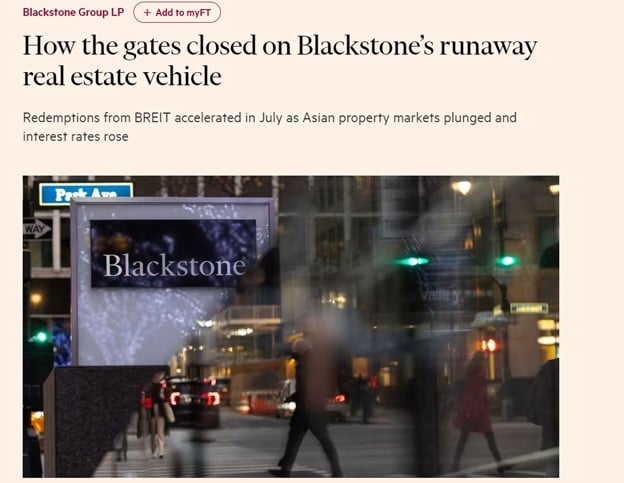

Blackstone gates redemption on private REIT

There’s a good article from the FT recently.

It talks about the troubles facing Blackstone’s REIT, a $69 billion US REIT.

Extract below (emphasis mine):

In July, Blackstone chief executive Stephen Schwarzman recounted a surprise meeting with an investor in the firm’s $69bn-in-assets private real estate vehicle designed for wealthy individual investors.

The person had approached Schwarzman to tell him the fund, called Blackstone Real Estate Income Trust, or BREIT, was his largest position. “I love you people. This is so amazing. All of my friends are losing a fortune in the market and I’m still making money,” recounted Schwarzman of the meeting on a quarterly earnings call.

In fact, investors were pulling money from BREIT at the time, alarming close watchers of Blackstone. Investors withdrew more than 2 per cent of its net assets that month, according to sources familiar with the matter and securities filings, exceeding a threshold at which Blackstone can limit investor withdrawals.

Asian investors had been pulling cash from the fund during the spring and summer as property markets in the region plunged. Some carried high personal leverage and were hit with margin calls, said two people familiar with the matter. BREIT, the value of which has risen this year, could be sold at high prices to meet the cash calls.

As the selling intensified and moved beyond Asia, Schwarzman and Blackstone’s president Jonathan Gray each added more than $100mn to their investments in BREIT this summer, said a source with knowledge of the matter. Blackstone declined to comment on the purchases.

Blackstone chose to not place any limits on investors hoping to withdraw money from BREIT in July. Though it has always told its investors the product is only semi-liquid, such a move could have sparked fears among investors that they could not easily get their money out. But a growing tide of redemption requests forced BREIT to announce on Thursday it would finally raise “gates” — allowing the fund manager to limit the volume of assets redeemed — through to the end of the year.

The move has sent shockwaves inside Blackstone, tarnishing what has become the biggest engine of asset and fee growth inside the world’s largest alternative asset manager. On Thursday, Blackstone’s shares fell more than 7 per cent and a host of analysts downgraded their outlook on the company over fears that the decision could cause its growth to stall.

Forced selling just starting to play out (liquidity mismatch)

This is the point I’m trying to make.

Real estate is an illiquid asset class.

REITs turn real estate into a liquid asset class, where you can buy/sell positions easily.

But there is no true liquidity.

The liquidity is an illusion.

If a significant % of the investor base wants their money back at the some time, that illusion of liquidity will be shattered.

Think about Luna and UST, once investors started selling.

Market is undervaluing liquidity

And my view – is that this market is underpricing the importance of liquidity.

Singapore REITs are a slightly different product, because they can be traded on the open market. And even then, if too many investors want their cash back at the same time, you will have problems.

But a bulk of real estate globally is held via private funds.

The longer interest rates stay up, the more important cash becomes.

And the longer this plays out, the more real estate investors will want their cash back.

At some point, the redemption requests will come in, and all these private funds will need to find a way to give investors their money back.

We are nearing the tipping point, where many of these funds are turning from net buyers to net sellers.

Over the next 12 – 24 months you’re going to see a lot of real estate come to market.

And my suspicion – with higher financing costs, the market will struggle to absorb this real estate, especially if you’re a seller looking for 2021 prices.

Will we see a crash in REIT prices?

Many of you want to know if REIT prices will collapse in 2023, just like March 2020.

Frankly, I don’t know.

It depends on whether we get a liquidity event, and the jury is still out on that one.

It’s also possible there is no crash, and REIT prices just trade sideways for a while.

Many of the secular tailwinds for REITs are gone.

Low interest rates powered REIT returns the past decade – due to cheap borrowing costs, and cap rate compression.

If I am right – both will reverse this decade.

How I will invest in a REIT market like that?

I hate to say this, but a market like that would be brutal.

It would be a PvP (player vs player) kind of market.

Unlike the past 10 years, where the returns came from just buying and holding on, as the rising tide of fed liquidity lifts all boats.

In a market like that, the money you make comes from taking it from another investor.

You make money from another investor selling / buying at the wrong price.

In other words – it calls for more active positioning, both in terms of what REITs you buy, and what price you buy (or sell).

So just to be very clear – I’m not saying Singapore REITs are a bad investment. I’m just saying you need to be much more selective, and active in your approach.

At the right price, anything could be a good buy.

This applies to tech as well

Now a lot of the points I discussed above apply to tech as well.

In a higher inflation, higher interest rate climate, tech is also a lot less sexy.

Because firstly the cost of capital goes up, so the strategy of borrowing cheap capital to grow market share at all costs goes out the window.

And secondly, in a higher inflation world, growth is everywhere.

The past decade companies struggled to grow, so investors loved tech for their growth potential.

But today – Pepsi can raise the price of Doritoes 10% and consumers have no choice but to accept.

So growth from tech companies is a lot less sexy, because in an inflationary world – everyone is a growth company.

Just like REITs – individual names can do well of course, but the secular tailwind for the asset class is gone (for now).

Which is why I see investors with a long tech long REIT portfolio, and it just screams to me investing for the past decade.

That portfolio would have done well had you bought it in 2012.

But this is 2022.

Which sectors have the secular tailwinds this decade?

This article is getting long, and I want to wrap up.

But a quick note on what might be the winners for this decade.

Interestingly – the market may be providing clues.

Look at the 3 month performance of the different sectors.

The best performers?

Energy, Materials (Metals), Banks, Industrials.

The boring, Ah Gong stocks that fell out of favour the past 15 years.

In a higher inflation higher interest rate world – these might be the guys that would benefit.

They can raise prices (pricing power), and they generate a ton of cash flow.

And they are less vulnerable to higher interest rates.

Of course – there is recession risk.

So I’m not saying go out and put 100% of your portfolio into energy because there is a good chance the Feds tighten us into a recession in 2023.

But look past the short term, and I can kind of see the mid term secular tailwinds from a higher inflation world – powered by insufficient supply, and higher demand due to US-China cold war, and green energy transition.

The exact names to look at is beyond the scope of this article, but you can check out my stock watch on Patreon if you are keen.

Now, can I be wrong on the above?

Yes, absolutely, 100%.

People think of investing like chess.

But it’s not.

Investing is like poker.

It’s all about probabilities.

The future is never cast in stone.

It’s always about (1) the probability of a win, and (2) how much you make when you win.

And in investing – never be afraid to change your mind.

Just like in Poker, once each card is revealed – the probabilities change.

Change your mind accordingly.

I see many investors stubbornly sticking to their views, because they said it publicly in the past and fear looking stupid.

Don’t.

If the facts change, change your mind.

That’s just how investing works.

Closing Thoughts: What would make me change my mind?

Perhaps the most important question in this article – what would need to happen, for me to change my mind on the above?

I thought about it for a bit.

And my answer – If the Feds succeed in controlling inflation, bringing it down to 2% long term.

If that happens, then I think you take everything I wrote about above and throw it out the window.

Because if the Feds succeed in bringing inflation down to 2% without triggering a deep recession, then it means the whole narrative of structural inflation this decade needs to be relooked.

And this could allow a return to a disinflationary world, with lower inflation, and lower interest rates – basically how the past decade looked like.

And if that happens, then yes absolutely you want to build a long duration portfolio – long tech, long REITs, long bonds.

Personally I don’t think that will happen.

I think this problem is bigger than something interest rates can solve.

It’s a story about US-China cold war forcing new supply chains to be built.

It’s a story of green energy requiring massive infrastructure investment.

It’s a story of underinvestment into commodities / energy coming back to haunt us, and the shifting away from US supremacy into a more multipolar world.

But like I said, I’m not afraid to change my mind.

If something happens to disprove my views, I’m happy to do a 180 and change my mind completely. As I will my portfolio positioning.

If you want my latest, updated macro views, do consider supporting Financial Horse as a Patron.

At S$15 a month you get the premium weekly market updates like this.

At $25 a month you get my full stock and REIT watchlist, and at $40 a month you get my full personal portfolio.

Trust Bank Account (Partnership between Standard Chartered and NTUC)

Sign up for a Trust Bank Account and get:

- $35 NTUC voucher

- 1.5% base interest on your first $75,000 (up to 2.5%)

- Whole bunch of freebies

Fully SDIC insured as well.

It’s worth it in my view, a lot of freebies for very little effort.

Full review here, or use Promo Code N0D61KGY when you sign up to get the vouchers!

– Free USD150 ($212) cash voucher

I did a review on WeBull and I really like this brokerage – Free US Stock, Options and ETF trading, in a very easy to use platform.

I use it for my own trades in fact.

They’re running a promo now with a free USD 150 (S$212) cash voucher.

You just need to:

- and fund S$2000

- Make 1 US Stock or ETF trade (you get USD100)

- Make 1 Options trade (you get USD50)

1080-1080-002-1024x1024.jpg)

Looking for a low cost broker to buy US, China or Singapore stocks?

Get a free stock and commission free trading .

Get a free stock and commission free trading with .

Get a free stock and commission free trading with .

Special account opening bonus for Saxo Brokers too (drop email to [email protected] for full steps).

Or for competitive FX and commissions.

Looking to buy Bitcoin, Ethereum, or Crypto?

Check out our guide to the best Crypto Exchange here.

Do like and follow our Facebook and Instagram, or join the Telegram Channel. Never miss another post from Financial Horse!

Looking for a comprehensive guide to investing that covers stocks, REITs, bonds, CPF and asset allocation? Check out the FH Complete Guide to Investing.

Or if you’re a more advanced investor, check out the REITs Investing Masterclass, which goes in-depth into REITs investing – everything from how much REITs to own, which economic conditions to buy REITs, how to pick REITs etc.

Want to learn everything there is to know about stocks? Check out our Stocks Masterclass – learn how to pick growth and dividend stocks, how to position size, when to buy stocks, how to use options to supercharge returns, and more!

All are THE best quality investment courses available to Singapore investors out there!

Or the answer could like in China’s reopening.

Ideally, this will resolve the supply chain & manpower crunch.

Such an interesting conundrum.

US trying to cool the market without breaking it.

China trying to reopen without catastrophe.

Well China’s reopening only helps the goods inflation.

But their reopening may worsen energy inflation because of increased oil demand.

And like Powell says, the key now is US services inflation, which is driven primarily by US wage growth.

But I suppose the short answer is that where inflation goes in 2023 is anyone’s guess! At the very least I would be keeping a close eye on wage growth and employment numbers going forward.

Dear FH,

Thanks for a very thoughtful and insightful article providing much food for thought. I agree with many of your points and that 2023 will be an interesting one for REITs.

A few comments on my end.

1. My view is that we are in the midst of the “Great Reset” and should not hold our breaths for the Fed rate to come down.

– For participants who have been in the market for the last decade or two, what they have experienced may feel normal but in fact the period from 2008 is a great anomaly.

– From the mid-60s till 2008, the Fed funds rate has been between 4-6% or higher for the vast majority of the period. There was a big drop following the 2000 dotcom crash but by the mid 2000s, it was climbing back to hitherto normal levels.

– From 2008, there was a great experiment to cut interest rates to zero and even negative levels and when inflation did not rise, governments became addicted to cheap stimulus and theories like Modern Monetary Theory arose to justify this. What was not taken sufficiently into account was the accession of China into the WTO in 2001 and the enormous impact this had on reducing inflation around the world through more efficient and lower cost supply chains, a phenomenon now in reverse.

– The huge surge of inflation recently, while exacerbated by Western sanctions on Russia, is viewed by serious economists as primarily due to the huge monetary and fiscal stimulus that governments provided over the past decade and I think it is probably safe to say that cockamie theories like MMT are now dead and Central banks are now sufficiently psychologically scarred to not go down the path of monetary stimulus with reckless abandon anytime in the near to medium term.

– Therefore, it is likely that we will return to a world of 4-6% interest rates as a norm after a period of adjustment.

2. What does this mean for REITs?

– A look at US REITs performance from 1973 to 1994 shows that during this period of high Fed interest rates, REITs did rather well. In fact, the total returns of an index of non-IPO REITs showed a total return of 37% higher than the S&P 500, based on an MIT paper.

– For the factors that you have well illustrated in your article, REITs are likely to be under pressure for a while as interest rates continue to rise and stay high. Their prices will have to adjust downwards to provide an adequate yield spread over risk free and to allow for cap rates to adjust.

– Yet, there is one important factor which you did not mention in your analysis which is the impact of inflation on rental rates and property valuations. Over the medium term, REITs will capture greater rental income through increased rents and this will compensate for higher interest rates and expenses, restoring their yield spread over risk-free and this accounts for their good performance even during times of high interest rates. The ability of REITs to do this varies widely by type of REIT, hospitality REITs can do this very quickly as their rates are adjusted daily whereas data center REITS locked into long term contracts with rental pegs to inflation having lower upper limits will find it more difficult. Property valuations will also rise with inflation in the mid term.

– So, long story short, I would expect pricing pressures on REITs in the short-term in response to the factors you have laid out and a recovery in the mid-term as rentals adjust. For a long-term investor utilizing REITs as a source of income, these fluctuations in stock valuation are not very important in the broad scheme of things as one can be confident that stock prices will eventually recover in the mid term and as long as one is generating a steady stream of passive income, one can just sit back and collect rent while allowing the REIT managers to do the work of running the properties.

3. Other implications of the “Great Reset”

– There are huge implications for the bond market and hence the return of the 60-40 portfolio. The 60-40 is dead, long live the 60-40! as well as the financial stability of the system given that the huge amounts of debt governments and corporations have piled up over the past decade but I will maybe leave these thoughts to another day.

– It is also possible that given this, the Fed will have to eventually accept long-term inflation at 3% instead of 2% but even in this scenario, I think it is more likely that interest rates in the mid to long term will revert back to the historical mode (as opposed to mean or median) of 4-6% and that the days of unlimited stimulus and interest rates of 0-2% without worry about side effects of inflation are now truly behind us.

Hi CMC,

Very insightful comment.

Some thoughts from me:

1. I think the key question for the developed economies is what is the trade-off between inflation / unemployment that they are willing to accept. If they want to bring inflation down to 2%, they need to bring unemployment up drastically, which brings with it many political problems. For now markets are thinking inflation can go down to 2% without any trade-offs on unemployment / recession, which to me looks a bit unrealistic.

How the G7 economies decide to strike the balance here I don’t know, and how this plays out will determine how to invest.

But I am expecting that the end result here (leaving aside how we get there), is that the G7 will be forced to accept a higher level of inflation going forward (than the official 2% target).

2. I actually spent a lot of time looking at US REITs performance from 1973 to 1994 a while back.

You are exactly right that US REITs did well over that time period. But a bit more granularity is required.

Namely – US REITs did very well from 1980s to 1994. But from 1973 to 1979, returns were abysmal. You’re looking at 20-30% drops in real estate prices, and quite a number of REITs went bankrupt.

Of course, the 1970 – 1994 data is clouded by demand v supply dynamics, economic growth etc, and even then the performance varied from city to city.

So there are definitely ways to outperform in this climate. But at the very least, a more active approach is required.

3. Yes I’ve been thinking about rental growth as well.

My hunch though, is that rental growth will not keep up with increase in interest rates. And the reason why is due to a mix of supply vs demand (fairly balanced), and inability for tenants to pay higher (because they are already squeezed on higher manpower, higher food, higher energy, higher interest expense etc).

Could I be wrong? Absolutely.

But for now, pull up the latest rental reversion numbers and you’re looking at flattish to low single digit growth. Nowhere near enough to offset the higher interest expense.

4. I think the 60-40 is dead. I think most investors will be forced to simply increase cash allocations, and accept the higher volatility in the equities portion of their portfolio. Because when stock-bond correlations go positive, there is no longer an effective hedge for downside risk in stocks (short of active management or options hedging).

And the implications for private asset classes like VC/PE/Private Real Estate Funds are going to be mind blowing.

But like you said – that is a topic for another day. 😉

Hi FH,

A few comments on my end

1. You are absolutely right that Central banks face a Hobson’s choice between fighting inflation and unemployment – there will not be an easy solution and it will not be pain free. Volcker chose fighting inflation at the expense of unemployment and Powell is saying the same. Whether he will actually do it is anyone’s guess. But inflation affects 100% of voters whereas unemployment at its peak affects maybe 10%. It is unsustainable for governments from a social stability standpoint to have inflation as high as it is today, all the strikes in the UK being a case in point. Plus the governments outside the US which do not print the USD literally cannot afford to raise pay in line with inflation at these rates without the risk of going bust or raising taxes to unpalatable levels. Sunak said as much this week. Plus raising wages in line with inflation sets off the dread wage-price spiral of unending inflation. So I think they will have to stop inflation no matter what. Maybe not at 2%, maybe at 3% but it cannot be very high on a long term basis.

2. Also agree with you on the risk of REITs going bust. To me that is the greatest danger with individual REITs and one has to be very careful about this.

3. On rentals keeping pace with interest expense, I am not sure we should be looking at comparisons with current rental reversions – at today’s inflation, nothing is keeping pace, not corporate profits, dividends, pay raises, nothing except REITs dividend yields at today’s depressed prices in fact. The pace of interest rate rises this year is similarly extraordinary but this pace of rise will not be sustained for long although the absolute rate could stay at historically normal levels (read high for last decade) for a very long time. Rental reversions will not keep pace with interest rate rises over the short term but over a 3-5 yr perspective, they will likely adjust to the new reality. That’s why I referred to the medium term in my earlier comment. A lot depends on one’s time horizon and I typically take a 5-10 yr view when investing. Over a 3-5 yr or 10 yr perspective, at long as a REIT does not go bust, I believe that REITs will adjust and do well as an asset class. Collecting above inflation yields while waiting for the adjustment is not a bad pasttime.

4. On the 60-40, I would have to respectfully disagree with you. The 60-40 is dead this year because the past couple of decades have lowered bond yields so much that it was unable to play its traditional stabiliser role. Frankly, it is a crazy world when you have corporates issuing negative interest rate debt and there was nowhere to go but down once interest rates normalize, regardless of equity market performance or recession. However, with Fed rates returning to 4-6%, investment grade corporate will have to get to 5-8% yield eventually. At these rates, the “great reset” brings back normality and the 60-40 portfolio starts to have meaning again. Investors will buy high quality bonds for the relatively safe yield it provides in choppy equity markets and times of economic uncertainty. Stock-bond correlations will go back to being negatively correlated and so the cycle resets and begins again.

Hi CMC,

Good points.

Some thoughts from me.

1. Yes, you are aboslutely right. This is the question investors should be asking. But we can debate and theorize all we want as to the right balance between inflation / unemployment, but ultimately 1 man (or 1 bank) is going to decide how this plays out – Powell.

And the longer this goes on, the more pressure he is going to face from the private sector and from politicians. You already see Elon and Cathie talking about the negative impact of rate hikes, expect more of this to come.

So while we may have our views on how Powell will move, we should still remain humble and watch what he says closely.

4. I think we might be talking about different variations of the 60-40.

I thought you were referring to the traditional 60-40, where the 40 went into US Treasuries to offset equities volatility. That I think is dead.

But it seems you are referring to a variant of the 60-40, where the 40 goes into IG credit. That’s quite a different portfolio because the IG credit will not offset equities decline in a crash, which means significantly higher portfolio volatility.

This variation I think will still remain relevant, but it will look a lot like the portfolio I talked about, which is higher equities allocation, and the rest in cash / debt. This means much higher volatility because you don’t have treasuries to absorb the equities decline in a crash.

You can actually argue that such a portfolio should be 80-20, since without treasuries to offset the equity volatility, one might as well just allocate higher into equities anyway. But I suppose for retail investors, this ultimately goes back to individual risk appetite.

Btw if you haven’t already seen it – Blackrock’s 2023 outlook is worth a read.

You may not agree with them, but it helps to understand their view at least.

https://www.blackrock.com/us/individual/insights/blackrock-investment-institute/outlook

Great comment CMC, to a great article too by FH. Appreciate it.

Thanks, appreciate it!

Great article! Does the argument of cap rates being lower than t-bill/deposit rates apply to residential investment properties too? Current net rental yield is also lower than mortgage interest rates, making investment property unattractive. Will that eventually lead to softening residential property price? Doubt rental can continue to go up at current rates to justify rising prices.

Residential real estate (I presume you mean Singapore) is quite unique because the demand is tightly controlled via TDSR and ABSD, while supply is also tightly controlled via government land sales.

So Residential real estate in Singapore is not so “free market” as compared to commercial real estate, and the analysis becomes much more nuanced.

Because you dont just look at the interest rate impact, you also need to consider demand vs supply, and possibility of government intervention.

I shared my thoughts in a recent article, you can check it out here: https://financialhorse.com/dbs-ocbc-uob-mortgage-rates-soar-to-4-5-will-this-crash-the-singapore-property-market-in-2023/

Hi FH, great post!

Just a question though, regarding the liquidity issue that you mentioned. You stated that the liquidity of REITs are an not actually based in reality, but isn’t in irrelevant? Since I doubt REIT Managers are liquidating assets to realise NAV. Thank you!

Well I think the point is that even if the REIT is strong and does not need to liquidate its real estate. Other private funds (or investors) might not be in the same situation – and they may be forced to sell.

Which may negatively impact the overall real estate valuations.

Very insightful presentation of different viewpoints from FH and CMC.

Always enjoyed your articles FH.

Thanks for your posts.

Thanks for the kind words – hope it helps!

How about Reits raising the rental rates to offset the increasing interest rates?

This is more of a mid term thing than short term.

If you look at the rental reversions you’re looking at flat to low single digits for now.

So yes, agree that higher rentals will eventually come into play, but we’re not seeing it yet. For now rising interest expense and rising risk free is the main consideration.