I’ve been having a bunch of great discussions with readers recently.

And I found that the discussion always came back to one question – Will the stock market crash in 2021?

So I figured let’s bite the bullet.

Let’s survey all the evidence out there, and try to answer this.

Will the stock market crash in 2021?

We’re looking at the Big Picture today

Now I do want to emphasize this article will focus on stock averages – basically the big picture view.

Within averages, individual sectors and stocks can outperform.

But that’s a separate topic.

The focus today is on the big picture.

BTW – We just launched a massive Christmas Promotion for all investing courses.

If you’re stuck in Singapore in December, why not learn to invest? 2021 will not be straightforward for markets – likely with lots of opportunities for investors!

Check it out here!

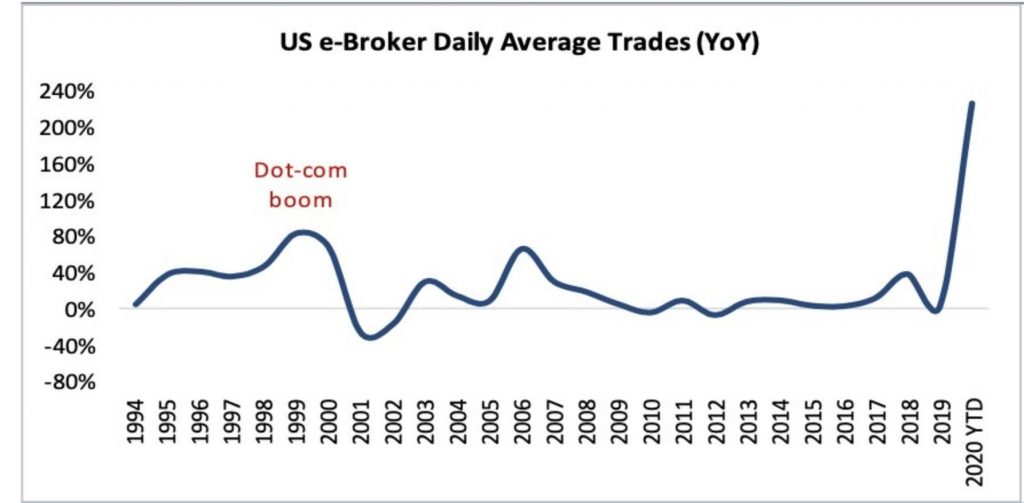

Retail Sentiment is very strong

Retail investor sentiment is very strong.

Daily trading volume growth has soared this year, surpassing even the dot-com levels of growth.

IPOs are hot as hell – traditionally a late cycle indicator.

Airbnb, Doordash, Snowflake all doubled on IPO. The last time tech IPOs were this hot was in 2000.

History tells us that when sentiment is this strong, it usually doesn’t end well. But it doesn’t offer any clues as to timing – the party could go on for quite a while before it ends.

What do the market technicals tell us?

So we need to look at something a bit deeper.

This was what I wrote for Patrons earlier this week:

200 Day Moving Average (DMA)

The chart below shows the points where more than 90% of S&P500 stocks trade above their 200 DMA (as it is right now).

Historically, when that happens, stocks either (1) experience a short term decline (9 – 12 month horizon, 6% to 19% drawdown), or (2) stay rangebound for a while.

Composite Valuation

A composite valuation score from one of the macro guys I follow (inputs are a blackbox so we won’t know exactly what goes in).

But the takeaway here is that usually when things get this bullish, short term returns from 3 to 12 months out tend to be negative, but they start improving from 12 months out.

Breadth Momentum

Breadth momentum is also really strong.

And historically, such strong breadth momentum is usually not a sign of a bear market rally, or a market top.

Most of the time, this happens within a broader bull market and higher highs lie ahead – But with a risk of a short-term drawdown.

What does this mean?

It’s quite a lot of information to digest, so I’ll sum it up.

What history suggests, is that:

- When sentiment is this bullish (based on stocks above 200 DMA), stocks usually have a drawdown or stay rangebound for a while (6 to 12 months)

- When breadth momentum is this strong, it usually means we are not in a bear market rally or a market top. It’s usually part of a broader bull market with higher highs ahead – But with the possibility of short-term drawdowns.

- Certain segments of the market (IPOs, disruptive tech) are showing bubble like tendencies. Retail participation in the market is also very high and slightly euphoric, which is not a good sign, but doesn’t offer clues on timing.

BTW – we share commentary on the COVID crisis every weekend, so please sign up for our mailing list, its absolutely free.

It’s a weekly newsletter that goes out every Sunday, and rounds up the week’s posts so you never miss anything.

Don’t forget also to join our Telegram Channel!

[mailmunch-form id=”928667″]

Lessons from WWI and WWII

I came across a great article this week that compared the vaccine news, to the V-day parades after WWI and WWII.

And the lesson there, was that:

- The US/UK economies did very well during wartime because of government support

- In the 12 months following “Victory”, stocks performed very well as sentiment was very strong – everyone thought the good old days would come roaring back

- As time wore on, it became clear things were not going back to pre-war status, and that real economic growth would stay slow for a while. Stocks fell eventually.

- Post-war, economic growth and inflation stayed low for a few years.

- But they eventually recovered, with a slightly longer term horizon.

If we apply that today, it sort of fits in so far.

Very strong economic performance during 2020’s “war time” when we are battling the COVID crisis.

There was a very strong recovery in stocks after the “victory” vaccine news and the hope of life going back to normal.

But if WWI/WWII is any guide, the post-war recovery would be tricky. Without the right policy moves and support, economic growth and inflation could stay low for years.

This time could be different

Now everything we looked at above is based on historical patterns.

We’re looking at what happened in the past, for clues on what happens going forward.

But as any history student knows, history rhymes, but never repeats.

So there could be any number of reasons why this time is different.

Maybe the stimulus will kick in, maybe the vaccine drives insane consumer demand, maybe retail sentiment has distorted the market.

So we need to add another layer of analysis –reasoning from base principles. What do macro fundamentals tell us?

Macro Perspective – the Insolvency Phase

This is what I wrote for Patrons this week:

I believe that 2021 may be the insolvency phase of this crisis.

The underlying problem here is that consumer demand habits have shifted permanently.

Like we talked about earlier this week – some retail demand has moved online permanently, and some office demand has moved to flexi-working permanently.

The problem so far, is that the government has bailed everyone out on a blanket approach.

Let’s have a simple example.

Imagine that offline retail has changed permanently because of shoppers moving online. The total market size used to be $100 pre-COVID, but post-COVID it will only be $80.

This $100 used to be split among 5 shops, so $20 each.

During COVID, the government stepped in with $20 stimulus to raise the total market to $100.

So the 5 stores still earn $20 each, and all is fine.

At some point in 2021/2022, governments will need to decide whether to stop that stimulus.

Once they stop it, the market falls to its new natural of $80.

If the same 5 stores stick around, that’s $16 each, which is a 20% decline in revenue for each of them.

1 of them will need to go under, so that the remaining 4 players still have $20 profit each.

It’s a simplistic analysis, but I think broadly that’s what the next phase will look like.

Government bureaucrats will need to become kingmakers – deciding who lives and who dies.

So there will be insolvencies, especially in the old world sectors permanently impacted by COVID.

And the focus is on managing the process. Ensuring that the insolvencies don’t happen all at the same time, giving the economy time to adjust structurally (eg. the workers in the shop that closes can move to an eCommerce player).

What is the trade-off here?

It’s very different from previous recessions like the Asian Financial Crisis where a whole bunch of companies were allowed to go bankrupt, all at the same time.

This time around, the government is stepping in very strongly, and managing the entire process.

Which leads to the question – what is the tradeoff?

By doing things this way, how will things differ from past recessions?

And I think the answer is that with this approach, real GDP growth will stay low for the foreseeable future, as the economy manages this structural transition.

Sure, year on year numbers will be high because 2020 is such a low base, but trend numbers will look very different.

US nonfarm payrolls are set out below, and I suspect economic growth will track something like this.

A sharp recovery from the bottom, but slow growth going forward, and significantly lower than the pre-COVID trend.

BUT – Monetary Policy will be a tailwind

But that’s the economy. And today we’re looking at the stock market.

For stocks, we also need to look at the other critical component – monetary policy.

And the bottom line is, the Feds are incredibly dovish.

They basically came out the past week to say that:

- Interest rates at staying at 0% until 2023 earliest

- Interest rates are not going up until we see sustained consumer price inflation higher than 2% (which realistically is not happening for a while – all the inflation is in asset prices)

- Bond buying via QE will remain unchanged until there is substantial improvement in the economy.

Which, to sum it up for the newer investors – the Fed has your back for the foreseeable future.

And… easy money is not going away until the economy is roaring again.

That’s a very, very powerful tailwind for stocks and financial assets in general.

Sure, the economy will suck for a few years, but as long as money is easy, asset prices can still continue going up.

FH, can you summarise everything so far?

This post has been a pretty technical one, so I’ll do my best to sum it up simply:

- Market technicals suggest the possibility of a short-term pullback (6-to-12-month horizon), but that the midterm trend is positive.

- Bullish retail sentiment suggests the possibility of an eventual short term retrace

- WWI/WWII suggest that the post-war recovery will be long and hard. Economic growth and inflation (consumer price) will likely stay low for a while. Policy support from governments will be crucial to watch.

- Macro fundamentals suggest that economic growth will stay low for a while, as economies and governments manage this structural transition.

- Monetary policy will stay easy for the foreseeable future, until 2023 at the earliest. Monetary stimulus will not stop until there is significant economic recovery, which will take a while.

What is my take on this?

How to invest will depend a lot on your holding period.

I can’t speak for any of you, so I’ll share my own thinking as a long term investor.

I’ve become tactically cautious since the Nov elections.

I’m still buying, but I’ve slowed my rate of purchases.

And going forward the bigger the rallies, the more cautious I will get.

But in 2021, I would view any pullbacks as a buying opportunity.

I think with the Feds in play, any stock market crash will not be allowed to last. If things get really hairy, I do expect the Feds to step in.

They’ve shown that in 2020, and I don’t see why 2021 is any different.

They’re just boxed in here unfortunately. If they keep this up they’re propping up the asset bubble and the rich get richer, but if they let the bubble burst the economic impact will be horrendous, and we see the Great Depression 2.0.

And between an asset bubble and Great Depression 2.0, I think the Feds will pick asset bubble any day.

With a broader 3 – 5 year perspective, I do expect the economy to manage the structural transition, and be nicely set up for a new phase of growth (just like post WWI and WWII). This is where I think a broader fiat currency depreciation will come into play, setting the stage for a new long term cycle.

For those who are keen, you can check out my portfolio positioning (with weekly buy/sell updates) on Patron.

Closing Thoughts: Diversification is a free lunch

I’ve always thought of investing as Poker, and not chess.

In Chess, the chance of a beginner beating a grandmaster in a single game is literally zero (unless you’re Beth Harmon). Never happening.

In Poker, the chance of a beginner beating a world class player in a single hand is actually very high. The beginner can draw a hand full of aces, bet big, and beat the world class player. Without really knowing what he’s doing.

But the more hands played, the more the world class player will improve. Over time, his experience of the game and systems can come into play.

I think investing is the same.

You can make a lot of money in the short term without the right processes in place. You can invest into a bull market where everything goes up, and make a ton of money without really knowing what you’re doing.

But holding onto the returns longer term is a different story. Longer term, the right systems and processes will need to come into play to deliver good returns.

And I just think that with the kind of massive uncertainty the world is going through right now, it would be foolish not to hold a diversified portfolio.

This article is what I think as at 19 Dec 2020, but I could be wrong, or something could happen tomorrow that changes this entirely.

Nobody knows. 2020 is the perfect example, where a bat flying around in Wuhan changed the entire course of human history.

But with diversification, you ensure that regardless of the outcome, your portfolio will continue to hold its value, and it will continue to perform.

And that’s really why diversification is the only free lunch in investing.

Start with a diversified portfolio as the base, and then tilt accordingly based on your risk appetite.

I would absolutely love to hear your thoughts. Let me know what you think!

BTW – We just launched a massive Christmas Promotion for all investing courses.

If you’re stuck in Singapore in December, why not learn to invest? 2021 will not be straightforward for markets – likely with lots of opportunities for investors!

Check it out here!

Hi FH. I really enjoy reading your posts, great summary for busy people. I agree with you that a crash in 2021 is unlikely, and that in the longer term, real economic numbers will begin to have an impact on stocks. But in 2021 it is worth keeping an eye on emerging economies + PIIGS. Those are the weak links in the system. And there are definitely more than few ‘Soros’ like people out there waiting to work some magic and leave countries in the dust.

Hi Little Monkey, thanks for the kind words. And yes, I do agree with you. I do think there will be big moves in the FX markets coming soon, setting up for a Soros like kind of trade.

Hi fh, it’s patreon and not patron. Patrons are poepls who pay for your content on your Patreon.

Got it! 🙂