I’m sure most of you guys have heard of the Singapore Airlines (SIA) Retail Bonds by now. It’s a 5 year bond yielding 3.03% per annum that is open to retail investors and that will be listed on the SGX. It’s really been covered to death by the popular media, but I’ll try my best to add something new to the discussion.

Basics: SIA Retail Bonds

The SIA Retail Bonds (fund docs available on their website) comes hot on the tails of the previous Astrea IV Retail Bonds and Temasek Retail Bonds. It definitely looks like like Temasek is trying their best to open up the local retail bonds market, so we’re probably going to see a lot more of such offerings going forward.

The key features of the SIA Retail Bonds are set out below:

| Coupon Rate | 3.03% p.a. |

| Tenor/ Duration | 5 years |

| Coupon Payment | Semi-annually |

| Application Fee | S$2 |

| Min. Amount | S$1,000 and in multiples of S$1,000 thereof |

| Issue Date | 28 March 2019 |

| Maturity Date | 28 March 2024, or earlier if sold in the secondary market on SGX |

| Application Period | Opens: 20 Mar 2019 (Wed), 9am Closes: 26 Mar 2019 (Tue), 12pm |

| Public Offer | S$300 million to Public, S$200 million to Institutional and Accredited Investors. Option to upsize to S$750 million. |

| Use of CPF/ SRS Funds | Not applicable |

Yield

Okay, I know what everyone is going to say here: 3.03% is a joke. And you know what? I get that. Objectively speaking, 3.03% is quite pathetic.

However, I do think that we need to take a step back and look at the global macro environment here.

In the current climate, a 5 year risk free Singapore Savings Bond (SSB) yields 2.01%. The 5 year Singapore Government Security (SGS) trades at 1.92%. A solid blue chip REIT like CapitaLand Mall Trust and Mapletree Commercial trust yield about 4.8% now, while a utility play like Netlink Trust is yielding around 5.8% (for the record, I think Netlink Trust is relatively cheap now). So the SIA Retail Bonds are trading at a 1.02% premium to the risk free rate, and about 1.77% less than a blue chip REIT.

SSBs

| Year from issue date | 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | 10 |

| Interest, % | 1.96 | 1.96 | 1.96 | 2.05 | 2.12 | 2.17 | 2.26 | 2.35 | 2.43 | 2.49 |

| Average return per year, %* | 1.96 | 1.96 | 1.96 | 1.98 | 2.01 | 2.03 | 2.06 | 2.10 | 2.13 | 2.16 |

At the same time, the global macro climate seems to be deteriorating pretty quickly. Just this week, we had Jerome Powell’s Fed announce that they anticipate no more rate hikes in 2019 due to poor economic data. That has spooked markets, causing a crash in the long end of the treasury yield curve, and the first inversion in the yield curve (3s10s) since 2007. For the newer investors among us, a yield curve inversion usually precedes every recession, with the time lag ranging anywhere from 6 months to 2 years. To add a bit more colour, the US 10 year treasury now yields 2.43%, down from a whopping 3.2% just 6 months ago in October 2018. You can say what you want about the equity markets and the massive rebound in 2019, but the credit market is a lot smarter (and way bigger). If the credit market is signalling that longer term economic growth is in trouble, I listen.

So yes, I absolutely get it when commenters out there are saying that a 3.03% yield is objectively low. But hey, when you look at this bond in conjunction with the global macro environment, and the alternatives available, I think a 3.03% yield isn’t too bad really.

Default Risk

There’s a pretty good article from another blogger I follow on why the default risk on this SIA 5 year Retail bond is real. I’ve extracted some of the key arguments below:

- Airline industry is fiercely competitive, and it is not going to get any easier anytime soon

The airline industry is notoriously competitive. It is notoriously capital intensive and low margin.

As Richard Branson put it best – “If you want to be a millionaire, start with a billion dollars and launch a new airline.”.

Just several headlines from the last few years from my time following the industry:

Fund injection into Malaysia Airlines continues: Khazanah – The Sun Daily

Shut down or sell off Malaysia Airlines, aviation analysts say – Today Online

At least 5 medium-size EU airlines to go bankrupt in 2018-2019 – Aerotime News Hub

And for those who remember the brief budget route between Singapore and London with Norwegian Airlines:

Norwegian Air Shares Plunge During Bid to Raise Cash – Bloomberg

And of course, the privatization of Tiger Airways by SIA in 2015 at 1/3 its IPO price.

Singapore Airlines to delist and privatise Tiger Airways – Business Times

The short of it is just that running an airline is one of the toughest businesses in the world.

As Buffett put it best, “When a management with a reputation for brilliance tackles a business with a reputation for bad economics, it is the reputation of the business that remains intact.”

- Huge CAPEX requirements and increased debt levels mean a weakened balance sheet

| 2018 | 2019* | 2020* | 2021* | ||

| Cash From Operations | $2,611 | $2,411 | $2,633 | $2,734 | |

| Capital Expenditure | -$5,210 | -$5,867 | -$5,294 | -$4,950 | |

|

-$2,599 | -$3,456 | -$2,661 | -$2,216 |

* estimates from Capital IQ

I think the numbers speak for themselves. SIA had a pretty strong balance sheet going into 2018 but that balance sheet is set to weaken dramatically as CAPEX requirements increase.

Not upgrading their fleet is not an option in the face of increased competition throughout the region. These cash expenditures will have to be funded either via debt or equity which is what is happening now.

- Assessment of what the next 5 years will look like

One of the most important things I stress even when it comes to bonds are that you still need to think about what the business will look like 5 years from now.

In this case, my job is to think about whether the money raised used to fund the aircraft purchases have a high chance of working out.

In this case, I can only describe my view as being… foggy.

As stressed earlier, the airline industry is notoriously competitive and we’ve seen a spate of airlines undergoing massive distress even with record low interest rates and a fairly benign operating environment.

I can only imagine the situation to be far worst in the case of a recession and find it hard to be optimistic given that other airlines are also expanding and upgrading their fleets throughout the region.

For the record, I absolutely agree with all the arguments above. I also dug up the full year numbers for the past 4 years, and they really do paint a picture of a company with increasing capex requirements (and decreasing cash flow). If this keeps up, it’s definitely going to impact the strength of their balance sheet. And given the way the airline industry is shaping up, with heavy competition from the Middle East and Chinese carriers, I don’t see any choice but for SIA to keep up the capex investments, or risk falling into obsolescence.

| Revenue | 31/03/2018 | 31/03/2017 | 31/03/2016 | 31/03/2015 |

| Total revenue | 15,806,100 | 14,868,500 | 15,238,700 | 15,565,500 |

| Cost of revenue | 11,501,600 | 11,220,300 | 11,702,200 | 12,307,000 |

| Gross profit | 4,304,500 | 3,648,200 | 3,536,500 | 3,258,500 |

| Cash and cash equivalents | 2,568,300 | 3,380,500 | 3,972,400 | 5,042,700 |

| Change in cash and cash equivalents | -812,200 | -591,900 | -1,070,300 | 158,800 |

But leaving aside all these arguments, I think you absolutely cannot forget who we’re talking about here. This is Singapore Airlines we are talking about, not Hyflux. It’s our national carrier, where Temasek holds a 55% stake. I understand that the cashflow numbers don’t look great and this is going to impact the balance sheet, but at the end of the day, companies go bankrupt not because they run out of cash from operations, but because they can’t refinance their debt. And realistically speaking, I think the chances of SIA ever being unable to refinance in the next 5 years are incredibly slim.

The way I see it, the most plausible situation that results in a SIA restructuring (and bondholders getting wiped out) plays out like this. The global economy slows massively in the next 2 to 3 years. As a result, demand for air travel drops greatly. At the same time, Middle East and Chinese competitors continue investing in capacity, increasing supply at a time when demand is falling. This results in huge margin compression that affects SIA’s profitability. SIA continues investing heavily in capex and depletes their balance sheet. All 3 local banks refuse to continue refinancing SIA. Temasek refuses to step in via an equity injection to save SIA. The company is forced to restructure.

Leaving aside all the steps that would need to happen to even result in this scenario, the implications of Temasek (and the government) allowing our national carrier to fall into restructuring would be massive, both politically, and reputationally. We pride ourselves on being a small nation with iron clad finances and currency stability. How is the bankruptcy of a national carrier that is 55% owned by the national sovereign wealth fund going to look for business sentiment?

Realistically speaking, I think the chances of a default on the SIA Retail Bonds in the next 5 years are incredibly slim, but of course, non-zero.

The risk free rate today is 2.01%. Anything higher and you have to take on risk. If I absolutely had to choose, I would say that the risk-reward on the SIA Retail Bonds is still attractive, especially when viewed in light of the global macro picture.

Liquidity

I’ve talked about liquidity to death in the past, so I won’t dwell on it too much here. Bottom line: these SIA Retail Bonds are listed on the SGX, so you will be able to sell them on the secondary markets. Taking a quick look at the Astrea IV and Temasek Retail Bonds, the trading volume is incredibly low, so if you’re planning to sell the SIA Retail Bonds, do expect a large bid-ask spread (ie. you may not be able to sell at the price quoted on the exchange), and expect to have to queue the order for a while.

Because of the liquidity issues though, I’m not so sure whether you can buy these and count on getting your money back in a hurry if there is a recession. If too many people rush for the exits during a recession, the price may crash, in which case your best bet is just to hold the bonds to maturity. So if you’re buying the SIA Retail Bonds, you should at least be prepared to hold them to maturity to get all your money back.

How does this fit into your portfolio?

These SIA Retail Bonds turned out to be a lot more boring than I expected. The Astrea IV bonds were interesting because of the highly unique securitisation structure used to mitigate the risk of default, and the Temasek Retail Bonds were interesting because, well, they were risk free. These SIA Retail Bonds are just a garden variety company bond from a Temasek linked company.

The difference was that before this, you needed to be an accredited investor or institutional investor to get access to such bonds, and you had to invest S$250,000 a lot, so this move definitely opens up more possibility to retail investors here in Singapore.

I think these bonds are actually great for:

- High net worth individuals with excess cash – If you’re a high net worth individual with 5 properties, a couple of million on the stock market, a Ferrari, and collectible art pieces, you’re probably looking to diversify your portfolio. These SIA Retail Bonds are a great choice.

- Retirees who want a low risk investment that is higher than the risk free rate – If you’re a retiree who mainly wants to preserve capital, and earn a return higher than the risk free rate, I think these SIA Retail Bonds are a great choice too. There aren’t really many choices out there that would fit your investment criteria, and this is one of the safer ones.

What you will need to factor into your decision on whether to subscribe though, are the following 2 points:

Temasek opening up the Retail Bond market – It’s quite clear that Temasek is trying to open up the Retail Bond market. In the coming years, we’re probably going to see more Retail Bonds being offered to the Singapore retail market. If you miss this one, you could always try your luck on the next offering. What I hear is that there may be another Astrea Bonds the pipeline, and the coupon on those tend to be higher (of course the risk goes up as well). If you want to take on more risk for a higher return, you may want to consider waiting for what comes next.

Interest Rate movements – Depending on which point of view you’re coming from, SIA was incredibly unfortunate with its bond pricing. They priced the bonds on 20 March, literally right before Jerome Powell announced no further rate hikes in 2019, sparking a rout in fixed income yields. Had they priced it a few days later, we may even be looking at a sub 3% yield.

If this interest rate trend keeps up though, it’s possible that the next few retail bond offerings may have even less attractive yields. In fact, this is already taking place for Singapore Savings Bonds, where the 10 year yield has come down from 2.45% in Jan to 2.16% in April. One school of thought is that it may be better to lock in a 3.03% now, than to wait a few months only to see the next issue come in with a sub-3% yield.

Closing Thoughts

I have mixed feelings on these SIA Retail Bonds. I think they make perfect sense for high net worth individuals or retirees. Given my risk profile though, I’m not so sure if they’re right for me. My strategy thus far has really been to stick with risk free investments (SSBs), or go big on things like REITs and shares, or higher yielding fixed income like Astrea IV. I’m not so sure how the SIA Retail Bonds fit into that strategy.

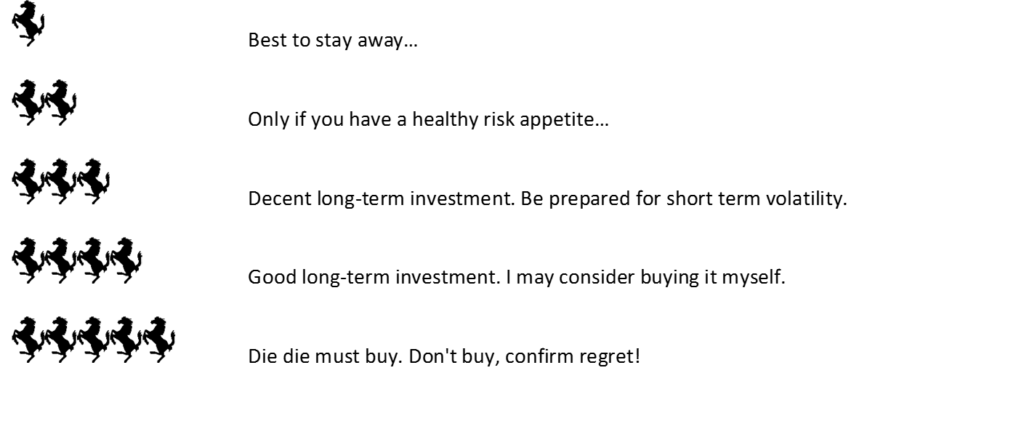

In any case, I’ll give these SIA Retail Bonds a 4 Horse rating. I think the yield is fairly priced, default risk is incredibly low, such that the risk-reward is attractive. There’s a specific class of investors who will love these bonds, and if you fit into that class, absolutely go for it.

SIA Retail Bonds Rating

Till next time, Financial Horse, signing out!

Enjoyed this article? Do consider supporting us and receiving additional exclusive content!

Like our Facebook Page for more great articles, or join the Facebook Group to continue the discussion!

Dear Financial Horse

Can you please discuss DOW plunges on 22 March 2019?

[…] – If you want to dig more into whether SIA has the money to pay you based on its fundamentals Financial Horse – If you want to know the current interest rate environment and what type of investors are […]

[…] mentioned in the original article, I think these bonds are perfect for a very specific kind of investor, […]