Depending on who you ask, shopping malls are either the best investment of the year, or the worst.

And within shopping malls, there’s no area that’s been harder hit than Orchard Road. Because of, you know, the global pandemic and its impact on tourists.

Buying opportunity, or falling knife?

Let’s find out!

Which are the Orchard Road REITs listed in Singapore?

Held by REITs

The REIT-ed Orchard Road malls are:

- Ngee Ann City – Starhill Global

- Wisma Atria – Starhill Global

- Paragon – SPH REIT

- 313@Somerset – Lendlease REIT

- Plaza Sing – CapitaLand Integrated Commercial Trust (CICT)

- Mandarin Gallery – OUE Commercial REIT

We’ll focus on the REITs with a big allocation to Orchard Road. So we’ll leave out CICT and OUE Commercial REIT because those are more diversified plays.

Lendlease REIT v Starhill Global v SPH REIT

|

| Lendlease REIT | Starhill Global | SPH REIT |

| Price (22 Oct) ($) | $0.66 | $0.435 | $0.795 |

| Market Cap ($ million) | 770 | 950 | 2,200 |

| P/B | 0.77 | 0.55 | 0.78 |

| Yield (trailing twleve months) |

4.6% (June 2020) |

6.8% (June 2020) |

3.4% (Aug 2020) |

|

Properties |

313@Somerset – 70% Italian Business Park – 30% |

Ngee Ann City and Wisma Atria (Retail) – 55% Ngee Ann City and Wisma Atria (Office) – 15% Australia Retail – 13% Malaysia Retail – 13% |

Paragon – 64% Rail Mall and Clementi Mall – 15% Australia Retail – 21% |

I’ve set out a simple summary of all 3 REITs above. Some observations:

- All 3 REITs have about 70% allocation to Orchard Road malls

- Both SPH REIT and Lendlease REIT are at 78% book value

- Starhill Global is much cheaper at 55% of book value

- The yield numbers are for the past 12 months, which frankly don’t mean much in this COVID environment

We’ll compare the 3 REITs in 4 ways:

- Sponsor

- Properties

- Valuation

- Operational performance

1. Sponsor – Lendlease v YTL Corp v SPH

Lendlease (Lendlease REIT)

I’ve come to really appreciate Lendlease as a manager of retail malls in Singapore.

All their malls – Jem, Paya Lebar Quarter (PLQ), Parkway Parade, 313@Somerset, all have great tenant mixes, and very strong footfall.

If it happens once you might call it a flash in the pan, but since it happens for all their malls, they’re probably doing something right.

I really like Lendlease.

YTL Corp (Starhill Global)

YTL is not a flashy sponsor, and that’s probably a bit of an understatement. Very very quiet sponsor that doesn’t get much investor interest.

But their track record is decent, and they’ve treated their REIT decently well.

Sometimes, a boring REIT is good, as long as it pays good distribution, year after year.

Singapore Press Holdings – SPH (SPH REIT)

If you’re Singaporean, you probably have a love-hate relationship with SPH.

I’m not going to waddle into that debate, but I will say this:

SPH doesn’t have core real estate expertise unlike players like CapitaLand, Mapletree, or Lendlease. SPH’s core business is media (which is not doing so well these days). And the pipeline of assets SPH brings is also not very exciting.

But SPH is SPH, and there’s very little risk of sponsor abuse or insolvency, so it adds a lot of stability to this REIT.

It’s not an amazing sponsor, but definitely not a bad one either.

Winner: Lendlease, and then a tie between YTL and SPH

2. Properties

313@Somerset (Lendlease REIT)

The positioning of the malls are very different. 313@Somerset caters towards a local, younger crowd. Ngee Ann City, Wisma and Paragon cater to older, more affluent crowds (especially tourists).

It’s very obvious – just walk around each mall and you’ll notice the difference in shoppers immediately.

Because COVID hits tourism badly, I would expect 313@Somerset to perform the best short term.

Their audience is a local, young crowd, which has not been affected badly by COVID. In fact, no one is flying anywhere this year, so malls that appeal to a domestic crowd may actually do well.

Ngee Ann City / Wisma Atria / Paragon

These 3 malls are literally a stone’s throw from each other, and they all cater towards the same kind of affluent shopper.

And they appeal strongly to tourists.

So they’re all suffering now.

But longer term, I do expect the tourists to return, and I expect Orchard Road to recover. So as long as I can hold on longer term, and the REIT doesn’t go insolvent in the meantime, there could be quite an attractive recovery in the medium term.

Of these 3 properties, I like Ngee Ann City the most, followed by Paragon, then Wisma Atria. Wisma is probably the weakest of the 3 because of its size, layout and tenant mix.

But frankly speaking, Ngee Ann City and Paragon are pretty close, and which you like more will ultimately come down to a personal choice.

Winner: In today’s market, Lendlease REIT because 313@Somerset caters towards a domestic audience. But when the recovery happens, Starhill and SPH REIT look equally strong to me.

3. Valuations

|

|

Lendlease REIT |

Starhill Global |

SPH REIT |

|

Price (22 Oct) |

$0.66 |

$0.435 |

$0.795 |

|

P/B |

0.77 |

0.55 |

0.78 |

|

Yield (ttm) |

4.6% (June 2020) |

6.8% (June 2020) |

3.4% (Aug 2020) |

Valuations are where it gets interesting.

Starhill Global is just so much cheaper than Lendlease REIT or SPH REIT.

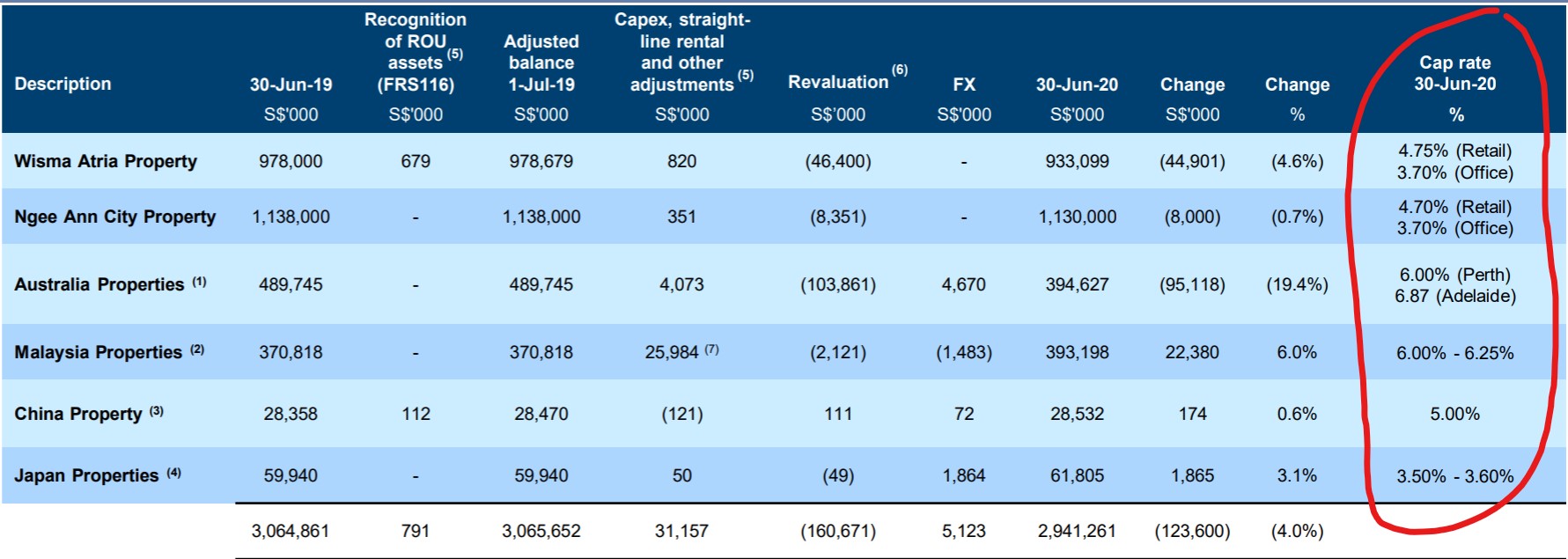

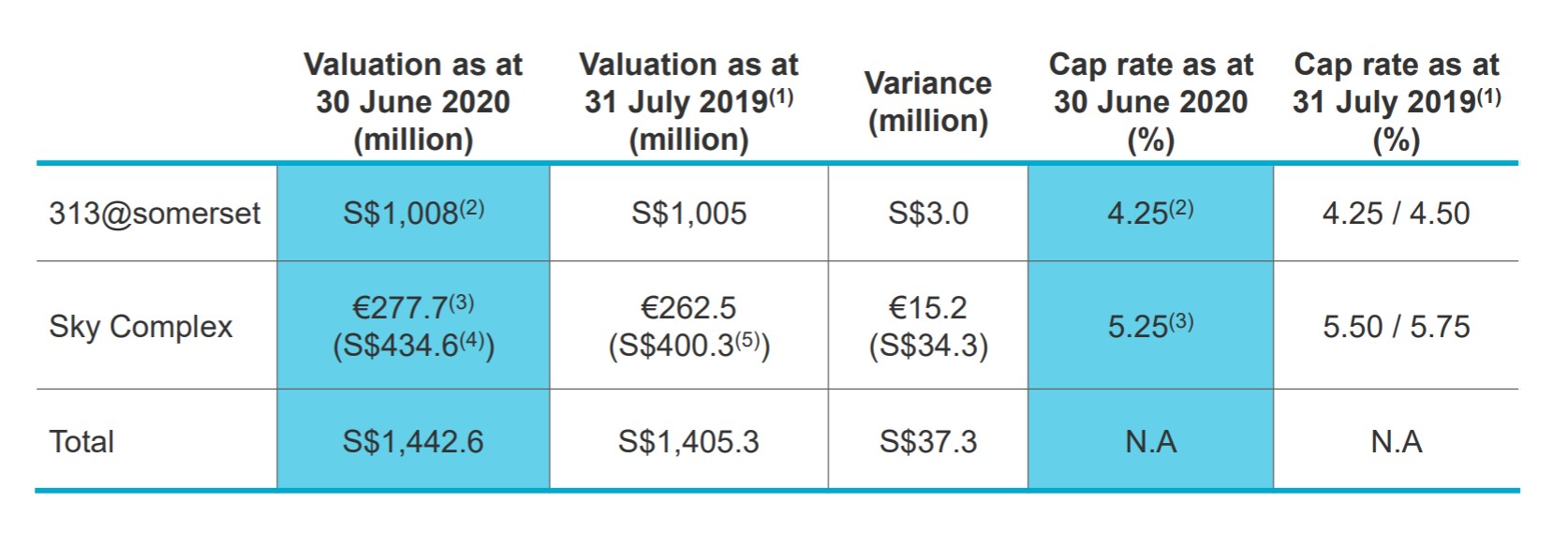

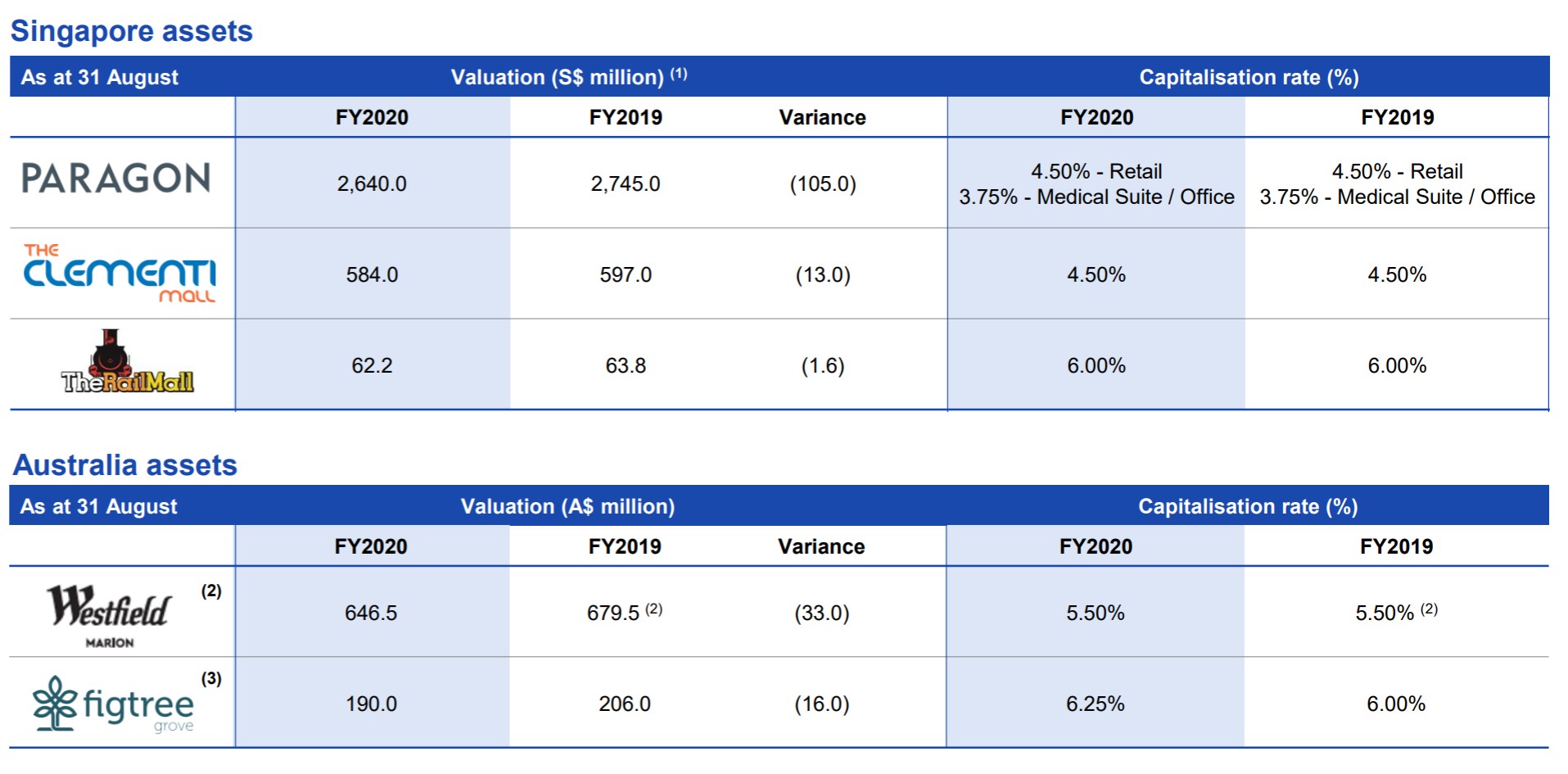

Cap Rates

Sometimes when the difference is this big, it could be because the REIT is playing around with capitalization rates (cap rates) used to value the property.

The cap rate basically tells you how the property is valued. So a 4.5% cap rate means that for a $100 million property, you get $4.5 million in rental each year.

It’s really as simple as that.

So a higher cap rate means the property is valued conservatively, which is good. A low cap rate means the property is valued aggressively, which would raise alarm bells.

I dug into their cap rates for the 3 REITs, and to summarise:

- Starhill Global uses a 4.7% cap rate

- Lendlease REIT uses 4.25%

- SPH REIT uses 4.5%

That’s actually pretty close to each other.

Which means that no, there’s no funny cap rate shenanigans going on here.

Lendlease having the lowest cap rate kind of makes sense too given that 313@Somerset caters to a domestic audience, and should be the least impacted of the Orchard malls.

Why is Starhill Global so cheap?

I dug around quite a bit, and I couldn’t actually find any good reasons why Starhill Global is trading so cheap compared to Lendlease/SPH.

This makes me nervous, because there’s nothing worse than not knowing what you don’t know.

I have some theories but nothing really convincing to explain such a big valuation gap.

So if you know something I don’t, please leave a comment below! What am I missing with Starhill Global?

Winner: Starhill Global is the cheapest on a valuations basis by a mile. SPH REIT and Lendlease REIT are tied.

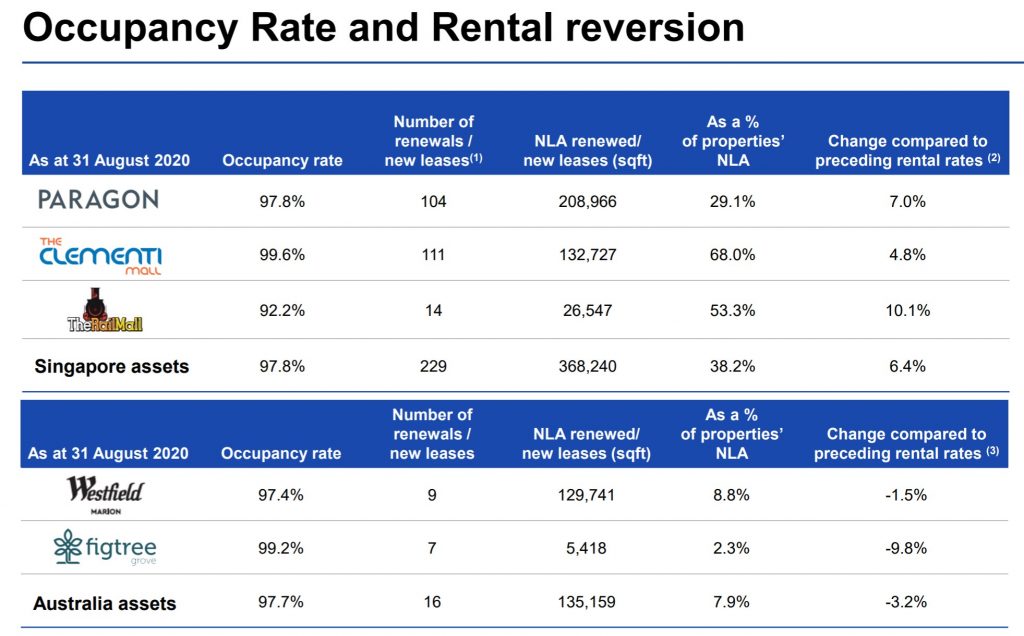

4. Operational Metrics

Pandemic? What Pandemic?

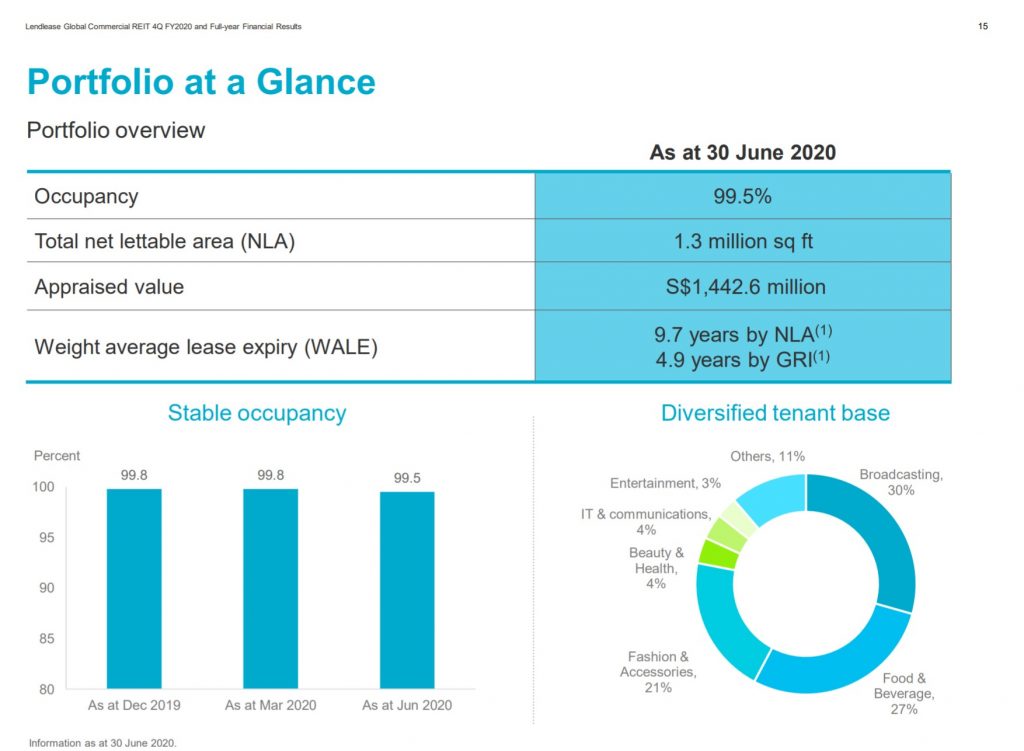

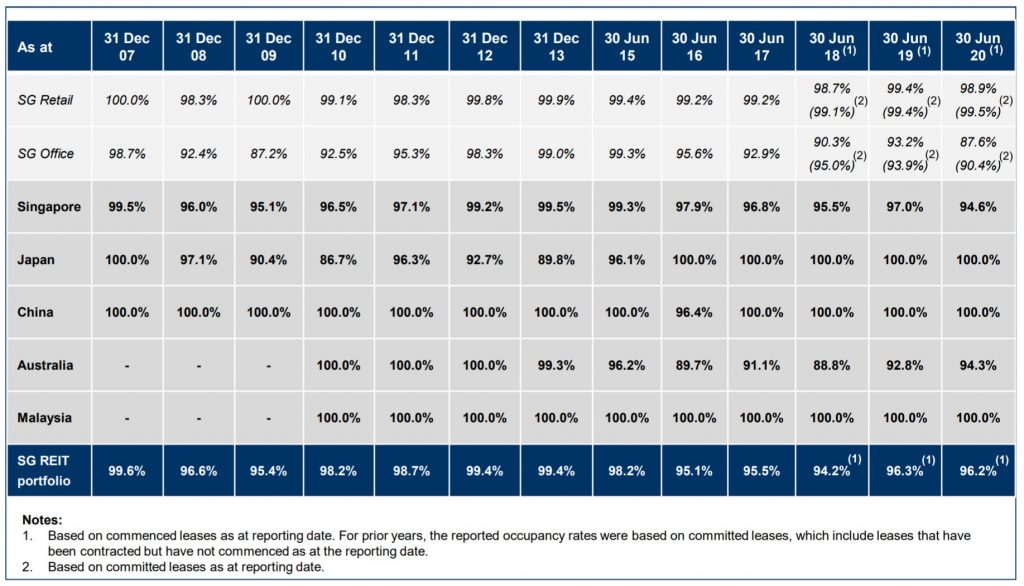

Occupancies are very high across the board. We’re talking > 96% occupancies for all 3 REITs.

Lendlease is highest, followed by SPH, then Starhill Global.

Even Ngee Ann City is at 97% occupancy.

It’s like COVID-19 never even happened.

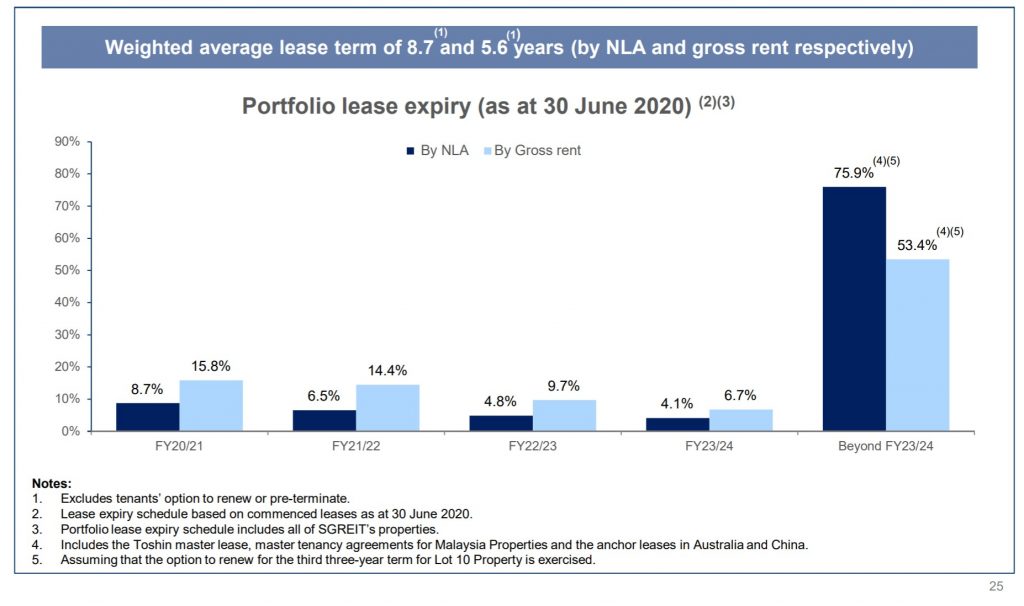

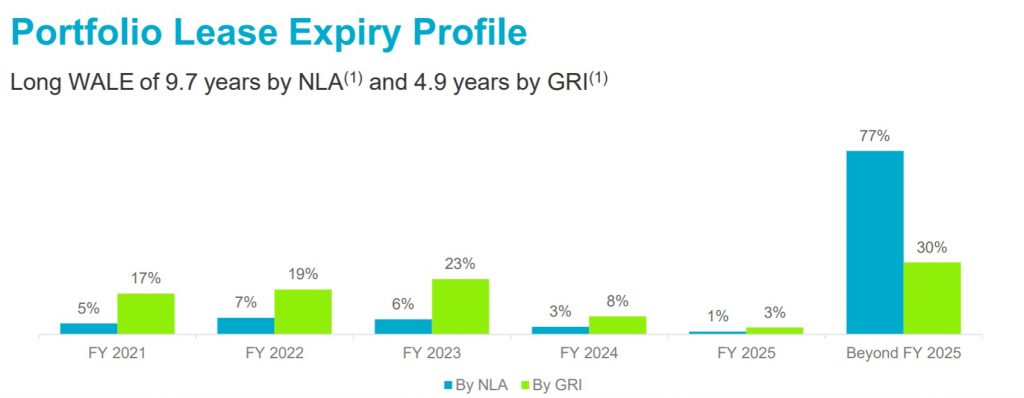

WALE

WALE or weighted average lease expiry, basically measures the average lease expiry date. In this climate, technically speaking a longer WALE is good, because you want to lock in a long term lease at lst year’s rentals.

But practically speaking, I wouldn’t read too much into WALE numbers right now.

With all the government support going around (rental relief / not paying rent), most tenants that want to renegotiate their lease, will get a chance to do so. So having a long WALE doesn’t really mean all that much right now, and could actually lull you into a false sense of security.

In any case, Starhill Global has the best WALE, followed by Lendlease.

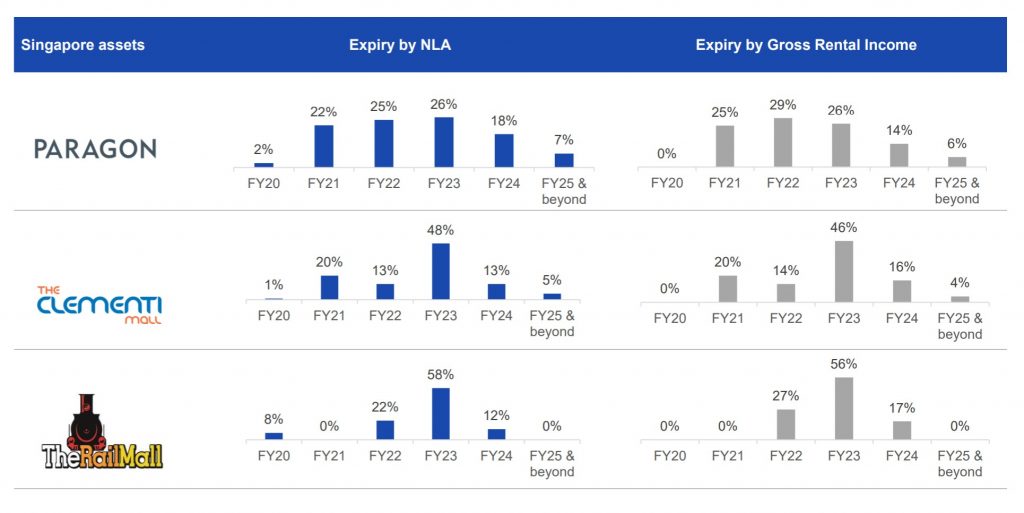

SPH REIT is the worst – In Paragon, almost 73% of their rentals are up for renewal in the next 3 years. That’s a lot of leases to renegotiate.

I’ve added the charts below in gallery form if you want to browse:

Winner: It’s a very close fight. I would say Lendlease, then Starhill Global and SPH tied.

Which is the best Orchard Road REIT? Lendlease REIT v Starhill Global v SPH REIT

A quick message from the sponsor of this article, Syfe:

If you’re looking to get diversified exposure to S-REITs, Syfe REIT+ is a great option worth considering, better than the REIT ETFs on the market (in my view). You get exposure to 20 of the largest S-REITs, and there is no minimum investment amount or minimum brokerage fees, which makes this a good option if you’re investing smaller amounts. Find out more here.

Seriously though, Syfe REIT+ is better than REIT ETFs in my view. Do check them out if you hate REIT picking and just want to buy a diversified REIT portfolio.

I’ve set out the summary of the results below:

|

| Lendlease REIT | Starhill Global | SPH REIT |

|

Sponsor |

1st |

2nd |

2nd |

|

Properties |

1st |

2nd |

2nd |

|

Valuations |

2nd |

1st |

2nd |

|

Operational Metrics |

1st |

2nd | 2nd |

From this chart, you would think that Lendlease REIT is the winner of the bunch.

I don’t quite agree with that though, and I think this illustrates the problem with ranking REITs in a binary way.

Because in real estate, price matters… a lot.

A fantastic piece of real estate in the best location, but at the wrong price, will still not be a good investment.

While a mediocre piece of real estate, at a fantastic price, can still be a fantastic investment.

It’s a concept that many of us intuitively understand when we go house-hunting, but forget when buying REITs.

Each REIT has its pros and cons

I know it’s a cliché, but it’s also absolutely true.

Each of these 3 REITs has its own pros and cons. What is good for a certain kind of investor, may not be so good for others. It really depends on what you’re looking for, and your holding period.

Lendlease REIT

Lendlease REIT to me will be the most resilient in the short term, because of its domestic target audience. It’s just not as affected by the lack of tourists.

Very attractive pipeline for future growth as well – so many great assets the Sponsor Lendlease can inject in.

Starhill GLobal

Starhill Global on the other hand, is really cheap right now. But then again, tourist arrivals probably won’t recover so soon, so it may not do so well short term. Also means that the Singaporeans who used to buy their luxury items overseas, now need to go to Orchard. So it may balance out, who knows.

Long term DPU has also been on a downtrend since about 2016, so that’s a warning sign to watch out for.

But Ngee Ann City and Wisma Atria are both very solid assets at reasonable cap rates, so I’m not sure whether the massive discount (45% from book) is justified.

At this price, there’s a big margin of safety baked in.

SPH REIT

SPH REIT is the odd one out in my view.

Paragon is a good property, but no so much better than Ngee Ann City to justify the premium valuation.

The rest of the portfolio (Clementi Mall, Rail Mall and the Aussie assets) are not amazing either.

It feels like you’re paying extra just for the SPH name, which doesn’t make sense because this isn’t Mapletree or CapitaLand. At the same Price/Book, Lendlease REIT is probably a better buy to me.

Which REIT would I buy?

Of course, here on Financial Horse, we don’t shy away from sharing our personal view. And I would never leave you with a waffly answer like that.

So of the 3 REITs, which would I buy? Lendlease REIT, Starhill Global, or SPH REIT?

And I think the answer for me will be Starhill Global REIT.

I featured Starhill Global as one of my top 3 REIT picks a few months back, and after this article my view remains.

Ngee Ann City is one of the more iconic properties on Orchard Rd, and I do see a future for it once COVID goes away. And at a 45% discount to book (at a 4.7% cap rate), it just looks very attractively priced right now. The long term declining DPU is a bit of a red flag though, so I’ll definitely be watching the upcoming earnings very closely.

I’m very nervous about what I’m missing on this REIT though. So do let me know if there’s any big red flag I’m missing here.

Full disclosure: I have a position in Starhill Global, and I may add to the position going forward.

I like Lendlease REIT too, but at today’s prices it’s not an amazing buy to me. If there is a dip in price it will definitely be on my watchlist though. I think the long term pipeline for Lendlease REIT is amazing, reminiscent of CMT back in the early 2000s when they only had Plaza Sing.

But again, what works for me may not work for you. I have a fairly long-term holding period, and I’m comfortable holding through any short-term drops.

If you prefer something more short term, Lendlease REIT could be worth checking out (read more in our review here).

As always, this article is written on 22 Oct 2020 and will not be updated going forward. Latest thoughts (and my stock watch and personal portfolio) are available on Patron.

Love to hear your thoughts. Which is your favourite Orchard Road REIT right now?

Support the site as a Patron and get access to my personal stock watch list, as well as my personal portfolio allocation.

Do like and follow our Facebook Page, or join the Telegram Channel. Never miss another post from Financial Horse!

Join our Facebook Group to continue the discussion, everyone is welcome!

Looking for a comprehensive guide to investing that covers stocks, REITs, bonds, CPF and asset allocation? Check out the FH Complete Guide to Investing.

Or if you’re a more advanced investor, check out the REITs Investing Masterclass, which goes in-depth into REITs investing – everything from how much REITs to own, which economic conditions to buy REITs, how to pick REITs etc.

Both are THE best quality investment courses available to Singapore investors out there!

Lendlease is over hype, to me. I live near Parkway Parade. Its a ghost town on weekdays, except during lunch hours and some nearby school and JC kids going there to eat fast food. Weekends also not packed. Injecting PP into the reit is a no-no to me.

I have a small position in Lendlease and a medium size in Starhill.

Ngee Ann City is so iconic on Orchard Road that its hard to miss. The rich will still spend, recession or not. Its quite well managed by someone’s brother and the Yeoh family. The issue is YTL is quite low profile. Those are just my opinion.

That’s a good point, thank you for raising this. 🙂